Sentiment in the markets sinks again after Russian President Vladimir Putin put Russia’s nuclear deterrent on high alert on Sunday, in response to unprecedented sanctions by the West, including blocking Russian banks from SWIFT. Meanwhile, Ukraine is holding on to defending from Russian invasion, with increasing support from Europeans and others in the world.

Asian markets are trading notably lower, but losses are “relatively” limited, while US futures also tank. Gold and oil jump but both are held below last week’s highs. Dollar is leading Yen and Swiss Franc higher while Euro is under most pressure. But most major pairs and crosses are held inside last week’s wide range for now.

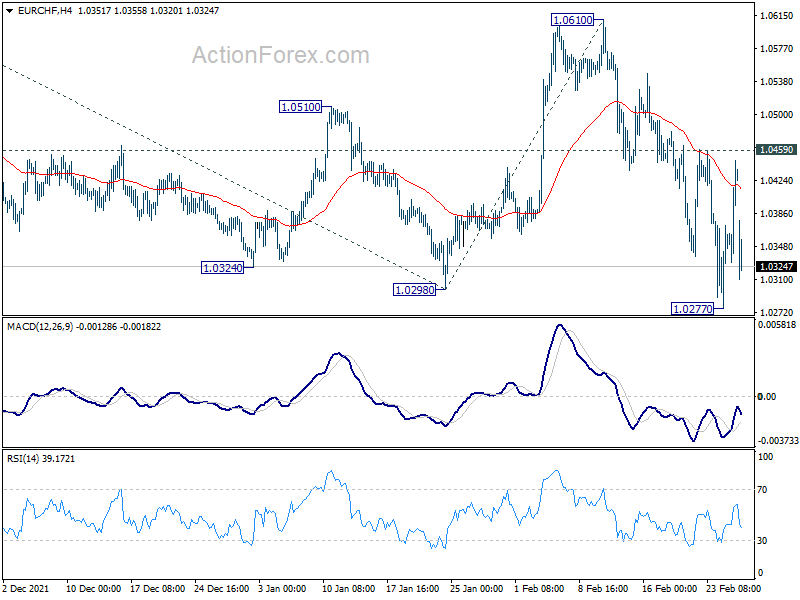

Technically, we’ll keep an eye on EUR/CHF for today. 1.0277 temporary low is back in radar with today’s gap down. Overall, recent down trend is expected to continue with 1.0459 resistance intact. Break of 1.0277 will confirm down trend resumption. That might be followed by break of 1.1105 temporary low in EUR/USD and 127.90 temporary low in EUR/JPY.

In Asia, at the time of writing, Nikkei is down -0.04%. Hong Kong HSI is down -1.24%. China Shanghai SSE is down -0.10%. Singapore Strait Times is down -2.05%. Japan 10-year JGB yield is down -0.0182 at 0.190.

Japan industrial production dropped -1.3% mom in Jan, retail sales rose 1.6% yoy

Japan industrial production dropped -1.3% mom in January, worse than expectation of -0.7% mom. Output declined for the second month, after the -1.0% mom contraction in December. Production of cars and other motor parts slumped -17.2% mom, falling for the first time in four months.

Nevertheless according to survey by the Ministry of Economy, Trade and Industry (METI), output is expected to bounce back by 5.7% mom in February and 0.1% mom in March. But the forecasts were taken before Russia’s invasion of Ukraine, which impact is still unknown.

Retail sales rose 1.6% yoy, above expectation of 1.1% yoy, fourth consecutive month of expansion.

Australia retail sales rose 1.8% mom in Jan, above expectation

Australia retail sales rose 1.8% mom in January, above expectation of 0.4% mom.

Director of Quarterly Economy Wide Statistics, Ben James said: “The emergence of the Omicron variant and rising COVID-19 case numbers, combined with an absence of mandated lockdowns has resulted in a range of different consumer behaviours. We have seen the type of spending previously associated with lockdowns occurring simultaneously with those associated with the easing of lockdown conditions.”

“This had led to variations across the industries with Food retailing recording a rise in sales consistent with previous COVID-19 outbreaks as consumers exercise caution amidst surging case numbers. However, the absence of lockdowns meant that other discretionary industries which would usually see a fall during the pandemic have recorded mixed results.”

Also released, private sector credit rose 0.6% mom, versus expectation of 0.7% mom.

New Zealand ANZ business confidence dropped to -51.8, a challenging year in 2022

New Zealand ANZ business confidence dropped to -51.8 in February, down from December’s -23.2. Own activity outlook dropped from 11.8 to -2.2. Export intentions dropped from 8.8 to 0.9. Investment intentions dropped from 11.4 to 4.5. Employment intentions dropped from 10.5 to 2.3. Cost expectations rose from 88.2 to 92.0. Profit expectations dropped from -13.1 to -32.7. Pricing intentions rose from 63.6 to 74.1. Inflation expectations rose from 4.42 to 5.29.

ANZ said, “All up, 2022 is shaping up to be a challenging year economically, and getting on top of super-charged inflation without an outright recession is looking increasingly difficult. But with CPI inflation heading well over 6% the RBNZ has no choice but keep right on hiking. And now global geopolitical developments threaten yet more imported inflation via energy markets. Buckle up.”

RBA to stand pat, BoC to hike, US to publish NFP

Two central banks will meet this week. RBA is expected to keep interest rate unchanged at 0.10%The central bank is expected stick to script that the comparatively lower inflation rate to other countries gives it room to wait and see. It might wait until getting Q2 inflation data before finally lifting interest rate in August. BoC, on the other hand, is expected to raise interest rate by 25bps to 0.50% and maintains hawkish bias. Meanwhile, Fed’s Beige Book and ECB meeting accounts will also be featured.

The data calendar is ultra busy. US ISMs and non-farm payrolls will take center stage. But also important are Eurozone CPI, Canada GDP, Australia GDP, China PMIs, etc. Here are some highlights for the week:

- Monday: Japan industrial production, retail sales; Australia retail sales; Japan housing starts; Swiss retail sales, KOF economic barometer, GDP; Canada current account, IPPI, RMPI; US goods trade balance, wholesale inventories, Chicago PMI.

- Tuesday: Australia AiG manufacturing, current account, RBA rate decision; Japan PMI manufacturing final; China PMIs; Germany CPI flash, Swiss PMI manufacturing; Eurozone PMI manufacturing final; UK PMI manufacturing final, M3 money supply, mortgage approvals; Canada GDP, PMI manufacturing; US ISM manufacturing, construction spending.

- Wednesday: New Zealand building permits, overseas trade index; Japan monetary base, capital spending; Australia GDP; Germany unemployment; Eurozone CPI flash; BoC rate decision; US ADP employment, Fed’s Beige Book.

- Thursday: Australia AiG construction, building approvals, trade balance; China Caixin PMI services; Japan consumer confidence; Swiss CPI; Eurozone PMI services final, ECB meeting accounts; UK PMI services final; US Challenger job cuts, jobless claims, non-farm productivity, ISM services, factory orders.

- Friday: Japan unemployment rate; Germany retail sales, trade balance; France industrial production; UK PMI construction; Eurozone retail sales; Canada building permits, labor productivity, Ivey PMI; US non-farm payrolls.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.21; (P) 129.75; (R1) 130.77; More….

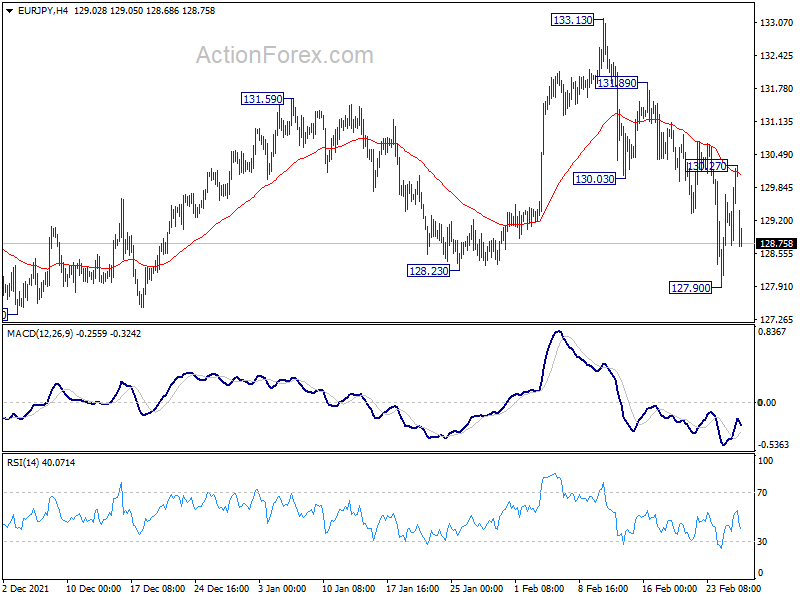

EUR/JPY dropped sharply after failing to sustain above 4 hour 55 EMA and drops sharply today. On the downside, break of 127.90 will resume the decline from 133.13, as another falling leg of the corrective pattern from 134.11, through 127.36 support to 126.58 fibonacci level. For now, risk will remain on the downside as long as 130.27 minor resistance holds.

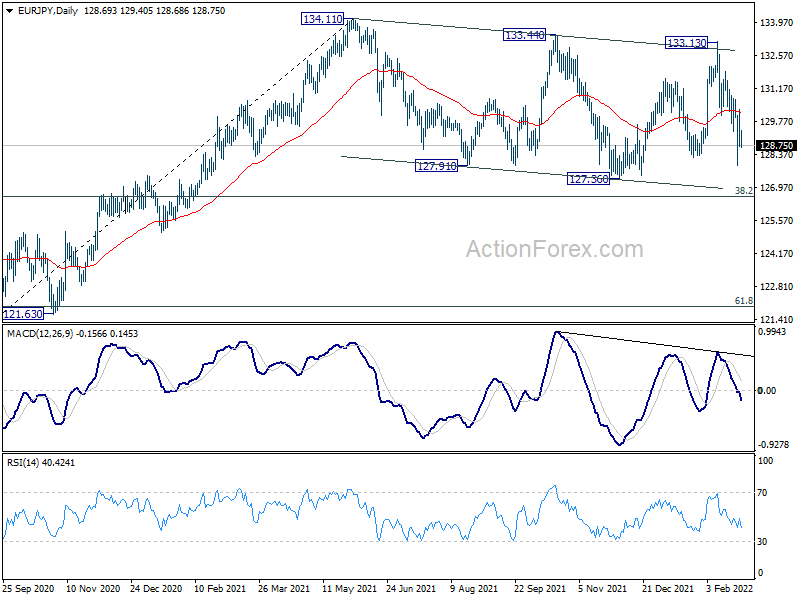

In the bigger picture, price actions from 134.11 are currently seen as a consolidation pattern only. As long as 38.2% retracement of 114.42 (2020 low) to 134.11 at 126.58 holds, up trend from 114.42 is still in favor to continue. Break of 134.11 will target long term resistance at 137.49 (2018 high). However, sustained break of 126.58 will raise the chance of bearish reversal. In this case, deeper decline would be seen to 61.8% retracement at 121.94, and possibly below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Jan P | -1.30% | -0.70% | -1.00% | |

| 23:50 | JPY | Retail Trade Y/Y Jan | 1.60% | 1.10% | 1.40% | 1.20% |

| 00:00 | NZD | ANZ Business Confidence Feb F | -51.8 | -23.2 | ||

| 00:00 | AUD | TD Securities Inflation M/M Feb | 0.50% | 0.40% | ||

| 00:30 | AUD | Private Sector Credit M/M Jan | 0.60% | 0.70% | 0.80% | |

| 00:30 | AUD | Retail Sales M/M Jan | 1.80% | 0.40% | -4.40% | |

| 05:00 | JPY | Housing Starts Y/Y Jan | 2.10% | 2.60% | 4.20% | |

| 07:30 | CHF | Real Retail Sales Y/Y Jan | 0.40% | -0.40% | ||

| 08:00 | CHF | KOF Economic Barometer Feb | 108.5 | 107.8 | ||

| 08:00 | CHF | GDP Q/Q Q4 | 0.40% | 1.70% | ||

| 13:30 | CAD | Industrial Product Price M/M Jan | 0.40% | 0.70% | ||

| 13:30 | CAD | Raw Material Price Index M/M Jan | -0.20% | -2.90% | ||

| 13:30 | CAD | Current Account (CAD) Q4 | 2.2B | 1.4B | ||

| 13:30 | USD | Goods Trade Balance (USD) Jan P | -98.5B | -101.0B | ||

| 13:30 | USD | Wholesale Inventories Jan P | 0.90% | 2.20% | ||

| 14:45 | USD | Chicago PMI Feb | 63.9 | 65.2 |

{kind=link}