Dollar opened the week broadly higher, following last week’s late recovery. Swiss Franc also picks up some buying, especially against Euro and Sterling. Commodity currencies are mixed for now, with Canadian Dollar having an upper hand. Yen is also mixed as corrective trading continues. The week is relatively light with holidays. But there are still some focuses like RBNZ rate decision, PMIs, and Fed and ECB minutes.

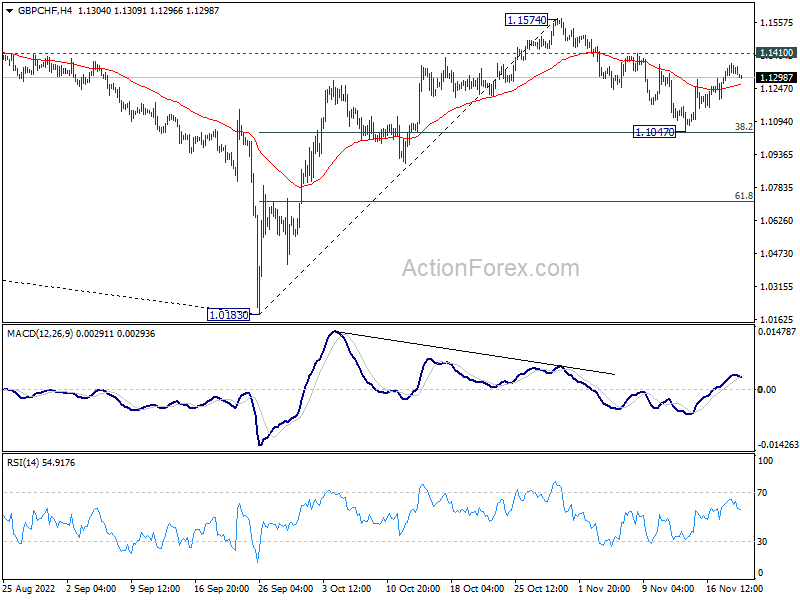

Technically, while GBP/CHF recovered last week after drawing support from 38.2% retracement of 1.0183 to 1.1574 at 1.1043. But recovering stalled ahead of 1.1410 resistance, keeping risks on the downside. Break of 1.1047 will prompt deeper decline to 61.8% retracement at 1.0714, even as a corrective move. Nevertheless, break of 1.1410 will revive near term bullishness for retest of 1.1574 resistance first. Development in GBP/CHF could be a hint on whether EUR/GBP is heading through 0.8827 resistance, or 0.8570 support.

In Asia, Nikkei rose 0.16%. Hong Kong HSI is down -1.68%. China Shanghai SSE is down -0.52%. Singapore Strait Times is down -0.81%. 10-year JGB yield dropped -0.0023 to 0.251.

Fed Bostic: 75 to 100 basis points of additional tightening warranted

Atlanta Fed President Raphael Bostic said on Saturday, “If the economy proceeds as I expect, I believe that 75 to 100 basis points of additional tightening will be warranted… It’s clear that more is needed, and I believe this level of the policy rate will be sufficient to rein in inflation over a reasonable time horizon.”

“In terms of pacing, assuming the economy evolves as I expect in the coming weeks, I would be comfortable starting the move away from 75-basis-point increases at the next meeting,” he added.

Bostic expected Fed to pause at some point to “let the economic dynamics play out,” given that it may take 12-24 months for the effect of rate hikes to be “fully realized.”

“I do not think we should continue raising rates until the inflation level has gotten down to 2%. Because of the lag dynamics I discussed earlier, this would guarantee an overshoot and a deep recession,” he said.

Bitcoin down again, ready for 2019 levels?

Both Bitcoin is some selling pressure and looks heading back to this month’s low. Negative news for cryptocurrencies are neverending, with reports that giant Digital Currency Group could be in trouble after its crypto lender Genesis was forced to pause withdrawals. The earlier collapse of FTSE was put to blame.

Technically, Bitcoin’s consolidation pattern from 15541 might have completed. Break of this low will resume larger down trend to 100% projection of 25198 to 18144 from 21460 at 14406, or even further to 2019 high at 13855. Break of 17134 resistance will delay the bearish case and extend the consolidations first.

RBNZ to hike 75bps; Fed and ECB to publish minutes

RBNZ is widely expected to step up tightening effort and raise the Official Cash Rate by 75bps to 4.25% this week. The central bank should continue to maintain hawkish bias. There are expectations there the OCR would peak at 5.00% by early next year. In terms of central bank activities, Fed and ECB will publish meeting minutes, but they’re unlikely to reveal anything new, given the frequency of comments from officials.

Regarding economic data, PMIs from Australia, Eurozone, UK and Japan will catch most attention. Germany will release Ifo business climate and Gfk consumer sentiment. Canada and New Zealand will release retail sales. US will release durable goods orders.

Here are some highlights for the week:

- Monday: Germany PPI.

- Tuesday: New Zealand trade balance; UK public sector net borrowing; Eurozone current account; Canada retail sales, new housing price index.

- Wednesday: Australia PMIs; RBNZ rate decision. Eurozone PMIs; UK PMIs; US durable goods orders, jobless claims, PMIs, new home sales, FOMC minutes.

- Thursday: Japan PMI manufacturing; Germany Ifo business climate; ECB meeting accounts.

- Friday: New Zealand retail sales; Japan Tokyo CPI; Germany GDP final, Gfk consumer sentiment.

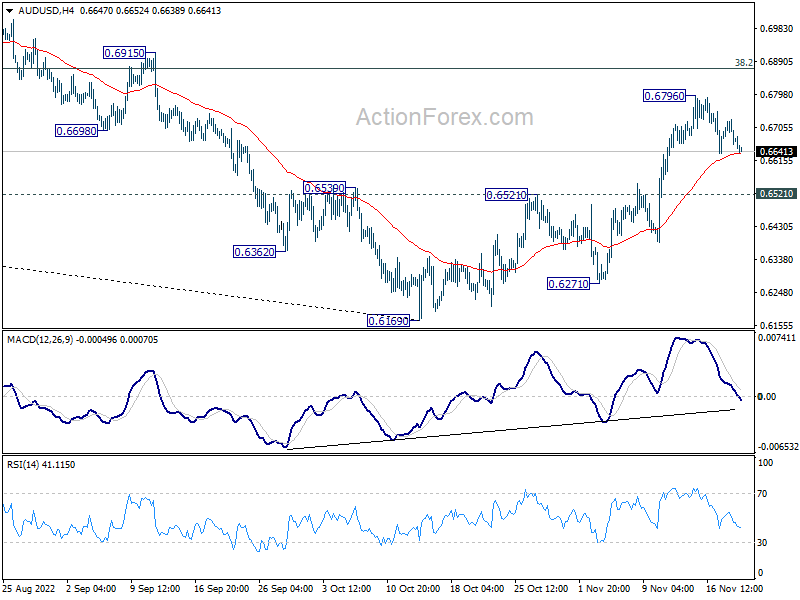

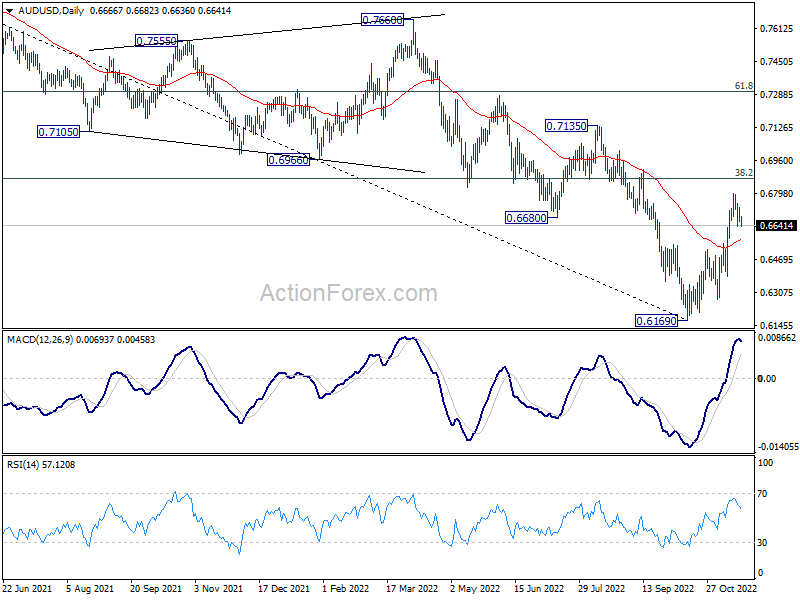

AUD/USD Daily Report

Daily Pivots: (S1) 0.6650; (P) 0.6690; (R1) 0.6719; More…

Intraday bias in AUD/USD stays neutral at this point. Further rally is expected as long as 0.6521 resistance turned support holds. On the upside, break of 0.6796 will resume the rise from 0.6169 to 0.6871 fibonacci level. However, sustained break of 0.6521 will argue that whole rebound from 0.6169 is over, and bring deeper fall to retest this low.

In the bigger picture, a medium term bottom is in place at 0.6160 already. But it’s too early to call for trend reversal. Nevertheless, even as a corrective move, rise from 0.6169 should target 38.2% retracement of 0.8006 to 0.6169 at 0.6871. Sustained trading above 55 week EMA (now at 0.6923) will raise the chance of the start of a bullish up trend. This week now remain the favored case as long as 0.6521 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:00 | EUR | Germany PPI M/M Oct | 0.90% | 2.30% | ||

| 07:00 | EUR | Germany PPI Y/Y Oct | 41.50% | 45.80% |

{kind=link}