Australian Dollar recovered mildly today, but momentum is so far limited. While RBA softened the hawkish stances after standing pat on rates, the left is still left open for more tightening. Governor Michele Bullock emphasized in the post-meeting press conference that the inflationary battle is far from won, while the board would keep this option on the table.

Aussie’s buoyancy was also bolstered by the strong rebound in Chinese and Hong Kong stock markets. A notable boost in investor confidence came from Central Huijin Investment, a subsidiary of China’s sovereign wealth fund, which announced its intention to increase investments in ETFs linked to major stock indices, aiming at market stabilization.

Within the broader currency spectrum, New Zealand Dollar the Canadian Dollar have also shown strength, albeit trailing Australian Dollar. US Dollar, on the other hand, has seen a broad but modest retreat, retaining a significant portion of its gains from the week. Meanwhile, European majors and Yen are finding themselves on the weaker side.

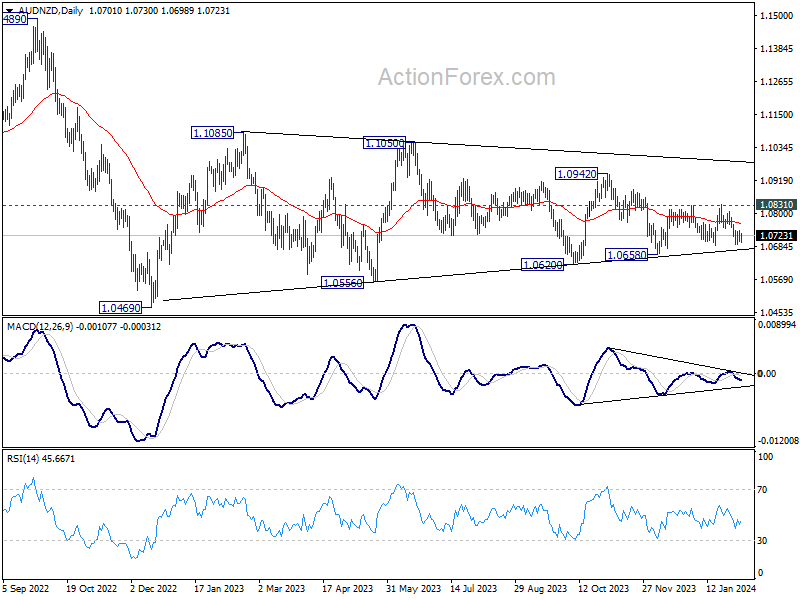

Technically, AUD/NZD is bounded in very tight range despite today’s recovery. The picture suggests that underlying momentum of Aussie remains weak. With the crosses trading below 55 D EMA, risk is mildly on the downside. Break of 1.0658 support would revive near term bearishness through 1.0620 support, possibly to 1.0469 low.

In Asia, at the time of writing, Nikkei is down -0.26%. Hong Kong HSI is up 3.80%. China Shanghai SSE is up 3.58%. Singapore Strait Times is down -0.28%. Japan 10-year JGB yield is down -0.0008 at 0.720. Overnight, DOW dropped -0.71%. S&P 500 dropped -0.32%. NASDAQ dropped -0.20%. 10-year yield rose 0.131 to 4.164.

RBA stands pat, eases hawkish stance without shifting to neutral

RBA maintained cash rate target at 4.35%, aligning with broad market expectations. The hawkish stance has seen a slight moderation, with the acknowledgment that “a further increase in interest rates cannot be ruled out,” hinting at a cautious approach rather than a definitive shift towards a neutral bias.

The updated economic forecasts paint a picture of gradual moderation in inflation pressures. Headline CPI is expected to decelerate from 4.1% at the end of 2023 to 3.2% by the close of 2024, reaching 2.8% at the end of 2025, and further softening to 2.6% by mid-2026.

Trimmed mean CPI mirrors this downward trend, projected to ease from 4.2% at the end of 2023 to 3.1% by the end of 2024, and gradually declining to 2.8% by December 2024, and then 2.6% by June 2026.

Additionally, RBA’s outlook for cash rate assumes a decrease to 3.9% by the end of 2024, followed by a further reduction to 3.4% by the end of 2025, and eventually reaching 3.2% by mid-2026. This assumption aligns with the expectations derived from surveys of professional economists and financial market pricing.

On the growth front, RBA projects a modest GDP expansion of 1.8% in 2024, with an improvement to 2.3% in 2025.

Japan’s labor cash earnings rises 1% yoy, with regular Pay at fastest pace since May

Japan saw a modest improvement in labor cash earnings in labor cash earnings, which increased by 1.0% yoy, accelerating from November’s 0.7% gain. Despite this uptick, the growth fell short of anticipated 1.3% yoy.

A notable positive development was observed in regular pay, which rose by 1.6% yoy, marking the highest reading since May 2023. Additionally, special payments saw a marginal increase of 0.5% yoy, although overtime pay experienced a decline of -0.7% yoy.

With CPI standing at 3.0% yoy, real wages saw a decline of -1.9% yoy, albeit at a slower pace compared to -2.5% yoy observed in the previous month. This marks the slowest decline in real wages since June 2023, suggesting a slight easing in the pressure on household incomes.

However, this positive note is tempered by the latest household spending figures, which saw a -2.5% yoy drop, worse than the expected -2.1% yoy.

BoE’s Pill: Rate reductions now a question of timing

BoE Chief Economist Huw Pill highlighted, in an online event overnight, a shift in BoE’s monetary policy discussions, which has evolved to determining “when” rather than “if” it will be appropriate to commence reductions in the Bank Rate.

Pill pointed out that rate reductions is currently “premature.” However, he suggested that the Bank does not require inflation to fully revert to its 2% target before easing monetary policy, given its current restrictive stance.

The Chief Economist also cautioned that due to developments in the Middle East, inflation is slightly more likely to “surprise on the upside than the downside” over the next year to 18 months. This perspective justifies to “to maintain restriction in the economy for some time”. This scenario would warrant maintaining “for longer” or even increasing the restrictive nature of monetary policy to combat “second round effects”.

Yet, Pill also left room for optimism, suggesting that if inflation dynamics dissipate more quickly than anticipated, there could be scope for more rapid interest rate reductions.

Looking ahead

Germany factory orders, UK construction PMI and Eurozone retail sales will be released in European session. Later in the day, Canada will release building permits and Ivey PMI.

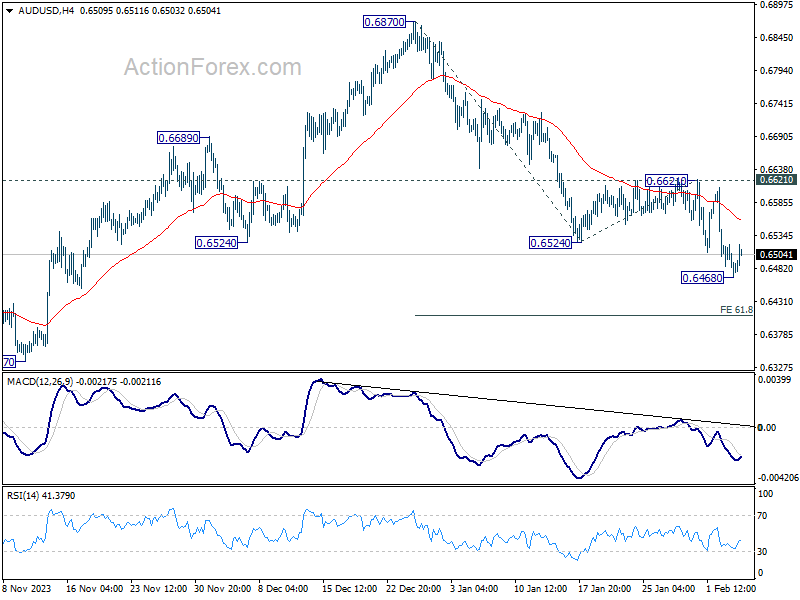

AUD/USD Daily Report

Daily Pivots: (S1) 0.6461; (P) 0.6491; (R1) 0.6513; More…

Intraday bias in AUD/USD is turned neutral with current recovery. But further decline is expected as long as 0.6621 resistance holds. Break of 0.6468 will resume the fall from 0.6870, as part of the down trend from 0.7156, to 61.8% projection of 0.6870 to 0.6524 from 0.6621 at 0.6407 next.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Dec | 1.00% | 1.30% | 0.70% | |

| 23:30 | JPY | Household Spending Y/Y Dec | -2.50% | -2.10% | -2.90% | |

| 03:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.35% | 4.35% | |

| 04:30 | AUD | RBA Press Conference | ||||

| 07:00 | EUR | Germany Factory Orders M/M Dec | 0.30% | 0.30% | ||

| 09:30 | GBP | Construction PMI Jan | 47.2 | 46.8 | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Dec | -1.30% | -0.30% | ||

| 13:30 | CAD | Building Permits M/M Dec | 1.20% | -3.90% | ||

| 15:00 | CAD | Ivey PMI Jan | 55 | 56.3 |

{kind=link}