Trading remains subdued across the forex markets as participants brace for the dual risk events: Fed’s policy decision and the escalating tensions between Israel and Iran. Currency pairs are largely bounded inside last week’s ranges, with traders opting for caution rather than conviction. Aussie and Kiwi lead this week’s performance, while Sterling, Franc, and Yen lag. The Dollar sits on firmer ground but has yet to generate strong directional momentum.

Fed is widely expected to leave interest rates unchanged at 4.25–4.50%, a decision already fully priced in by markets. Attention will center on the updated Summary of Economic Projections and the new dot plot. In March, the median forecast pointed to two rate cuts in 2025, but that view was narrowly held. A shift in just two members’ projections could tilt the median down to a single cut.

Fed Chair Jerome Powell is likely to reiterate the “wait and see” strategy, repeating that policy is appropriately restrictive for now. While markets are leaning toward a rate cut by September, Powell is unlikely to offer strong forward guidance, especially with inflation risks and tariff timelines still unresolved. Recent labor market softness may receive some acknowledgment, but overall, Fed is expected to stick with its existing posture.

Meanwhile, global risk sentiment continues to be tested by the increasingly sharp rhetoric between the US and Iran. President Trump called for the “unconditional surrender” of Iranian Supreme Leader Ayatollah Khamenei, warning that he is an “easy target.” In response, Khamenei vowed resistance and warned that a US attack would bring “irreparable damage.” Despite these threats, markets have yet to show panic, with oil and gold prices largely contained.

Looking ahead, tomorrow’s BoE and SNB decisions will take center stage in Europe, but the Asian session may offer volatility first. New Zealand GDP and Australia’s labor market report could provide fresh momentum for the outperforming Antipodean currencies.

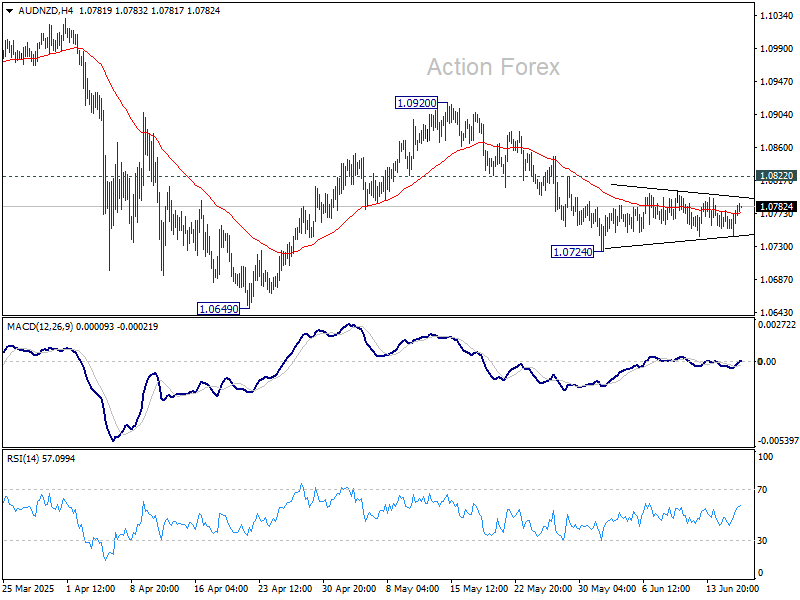

Technically, AUD/NZD turned sideway after falling to 1.0724. Near term outlook stays mildly bearish as long as 1.0822 resistance holds. Firm break of 1.0724 will extend the fall from 1.0920 to retest 1.0649 low.

In Europe, at the time of writing, FTSE is up 0.13%. DAX is down -0.37%. CAC is down -0.24%. UK 10-year yield is down -0.25% at 4.534. Germany 10-year yield is down -0.014 at 2.523. Earlier in Asia, Nikkei rose 0.90%. Hong Kong HSI fell -1.12%. China Shanghai SSE rose 0.04%. Singapore Strait Times fell -0.25%. Japan 10-year JGB yield fell -0.016 to 1.457.

US initial jobless claims fall to 245k vs exp 246k

US initial jobless claims fell -5k to 245k in the week ending June 14, slightly below expectation of 246k. Four-week moving average of initial claims rose 5k to 245.5k, highest since August 19, 2023.

Continuing claims fell -6k to 1945k in the week ending June 7. Four-week moving average of continuing claims rose 13k to 1926k, highest since November 20, 2021.

ECB’s Panetta flags prolonged sub-2% inflation, cites trade and geopolitical risks

Italian ECB Governing Council member Fabio Panetta warned that Eurozone inflation is likely to remain below the 2% target for an extended period. Speaking at a conference today, Panetta said the region continues to face a “persistently weak” economy, which, coupled with subdued price pressures, calls for caution on the monetary policy front.

He pointed specifically to “substantial” risks surrounding US trade policy and the Middle East conflict. These factors, Panetta said, make it “difficult to quantify” the clouded outlook.

“Against this backdrop, the ECB’s Governing Council, at its most recent meeting, reaffirmed a flexible approach, keeping its options open,” he said. “It will continue to take decisions on a meeting-by-meeting basis, without pre-committing to a defined course for monetary policy,” he added.

Eurozone CPI finalized at 1.9% in May, disinflation takes hold as services inflation softens

Final Eurozone inflation figures for May confirmed further softening in price pressures, with headline CPI easing to 1.9% yoy from April’s 2.2% yoy. Core CPI (ex energy, food, alcohol & tobacco) also moderated to 2.3% yoy from 2.7% yoy. Services inflation, a key component closely tracked by ECB, slowed markedly from 4.0% yoy to 3.2% yoy, contributing to the broader disinflation trend across the bloc.

According to Eurostat, the largest contribution to the overall annual inflation rate came from services (+1.47 percentage points), followed by food, alcohol, and tobacco (+0.62 pp). Non-energy industrial goods added a modest +0.16 pp, while energy dragged the headline rate down by -0.34 pp. The moderation in services inflation is especially important given its linkage to wage growth.

Looking across the EU, headline inflation was steady at 2.2%, but divergence across member states is stark. Cyprus, France, and Ireland posted the lowest annual rates at 0.4%, 0.6%, and 1.4% respectively, while Romania, Estonia, and Hungary topped the inflation chart with rates above 4.5%. Annual inflation declined in 14 member states compared to April.

UK CPI slows to 3.3% in May, but goods prices surges to highest since late 2023

UK headline CPI eased from 3.5% yoy to yoy in May, slightly above expectations of 3.3% yoy. Core CPI (excluding energy, food, alcohol and tobacco) also slowed from 3.8% to 3.5%, in line with forecasts.

While the overall trend points to gradual disinflation, markets might pay more attention to the reacceleration in goods prices, which rose to 2.0% yoy, the highest rate since November 2023.

Services inflation, however, showed a more meaningful decline, falling from 5.4% yoy to 4.7% yoy, suggesting underlying pressures are softening.

On a monthly basis, CPI rose by 0.2% mom, matching expectations.

Japan’s exports slide – 1.7% yoy in May as auto tariffs from US take toll

Japan’s trade data for May revealed growing pressure on its export sector, with headline exports falling -1.7% yoy to JPY 8.135T. Imports dropped -7.7% yoy to JPY 8.773T. The resulting trade deficit stood at JPY -637.6B.

Of particular concern was the sharp -11.1% fall in exports to the US, where car shipments plunged -24.7% yoy on the immediate impact of US tariffs.

Despite posting a trade surplus of JPY 451.7B with the US, the bilateral trend was negative. Imports from the US dropped -13.5% yoy. Japanese exporters are now grappling with a 25% tariff on autos and auto parts, plus a 10% baseline levy on all other goods. Steel and aluminum products have also been hit with a 50% tariff in early June.

On a seasonally adjusted basis, exports edged up just 0.1% mom, while imports declined -0.3% mom, leaving a narrower but still negative trade balance of JPY -305B.

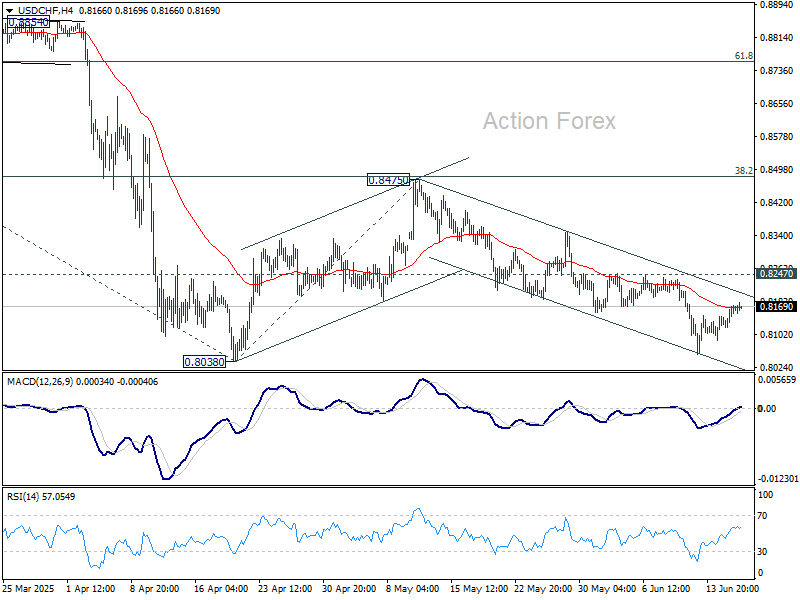

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8133; (P) 0.8153; (R1) 0.8184; More….

Intraday bias in USD/CHF remains neutral and outlook is unchanged. On the upside, break of 0.8247 resistance will argue that corrective pattern from 0.8038 is starting the third leg. Bias will be turned back to the upside for 0.8475 resistance again. However, firm break of 0.8038 will resume larger down trend. Next target will be 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757.

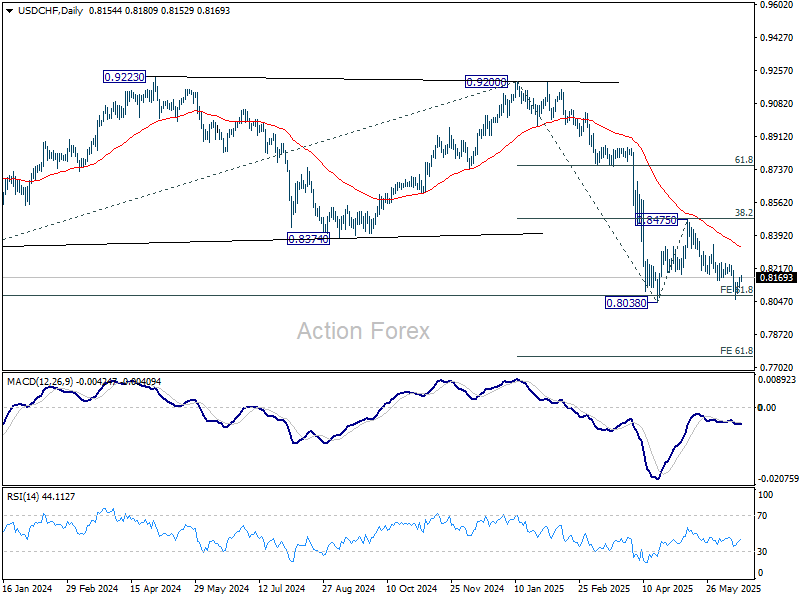

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8656) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

{kind=link}