Central bank marathon ends with rate decisions from SNB, BoE, and ECB now behind market. Yen emerged as the strongest performer, supported by a hawkish interpretation of BoJ Governor Ueda’s post-meeting remarks. While the BoJ held rates at 0.75%, Ueda signaled that rate hikes remain on the table even if growth weakens, as long as underlying inflation stays intact. This marks a notable shift, suggesting policy will not be constrained by temporary economic softness.

Markets have quickly adjusted, with expectations for an April rate hike moving from a tail risk to a credible scenario. This repricing has provided strong support for Yen, particularly as positioning had previously leaned heavily against it.

At the same time, technical dynamics in USD/JPY have reinforced the move. Traders remain reluctant to push the pair beyond the 160 level, widely viewed as the “red line” for intervention. The inability to break higher has encouraged profit-taking and position unwinding, further supporting Yen.

Sterling also gained ground, following the Bank of England’s surprise unanimous decision to hold rates. While the policy stance itself did not turn explicitly hawkish, the absence of dissenting votes from dovish members has been interpreted as a shift away from easing bias.

Markets have moved quickly to price in tightening, with money markets now fully anticipating a rate hike to 4.00% by June and further increases toward 4.35% by September. While these expectations may be running ahead of official guidance, they have nonetheless provided near-term support for the currency.

Euro is also firmer, underpinned by ECB’s upward revision to inflation forecasts. However, gains remain limited as the simultaneous downgrade to growth projections highlights the emergence of stagflation risks.

In contrast, Swiss Franc has weakened after SNB signaled a stronger willingness to intervene in foreign exchange markets. By explicitly pushing back against excessive currency strength, the central bank has effectively capped safe haven demand, even in a risk-averse environment.

Aussie is among the weaker performers, pressured by a mix of risk aversion and the sharp rise in oil prices, with Brent briefly touching $119. Dollar, meanwhile, is paring back some of its post-FOMC gains. With the Fed’s message now largely priced in, focus has shifted toward global policy divergence.

In Europe, at the time of writing, FTSE is down -2.86%. DAX is down -3.02%. CAC is down -2.45%. UK 10-year yield is up 0.111 at 4.792. Germany 10-year yield is up 0.026 at 2.975. Earlier in Asia, Nikkei fell -3.38%. Hong Kong HSI fell -2.02%. China Shanghai SSE fell -1.39%. Singapore Strait Times fell -0.69%. Japan 10-year JGB yield rose 0.05 to 2.268.

ECB raises inflation forecast, cuts growth as energy shock bites

ECB holds rates unchanged as expected, and revised inflation higher and growth lower, highlighting stagflation risks as energy prices rise and policy uncertainty increases. Read more.

BoE unanimous rate hold surprises as doves abandon cut calls amid energy shock

BoE surprised with a unanimous hold as even dovish members backed a pause, signaling energy-driven inflation risks have delayed rate cuts. Read more.

UK wage growth cools as labor market softens despite stable unemployment

UK wage growth eased and employment showed signs of softening, pointing to moderating inflation pressures as BoE assesses policy path. Read more.

SNB holds rates, signals stronger FX intervention to cap Franc strength

SNB kept rates at 0% but stepped up its intervention signal to limit CHF gains as energy-driven inflation is seen as temporary. Read more.

BoJ holds rates, signals further hikes despite temporary inflation dip

BoJ kept rates at 0.75% and reaffirmed tightening bias, looking through a near-term inflation dip as wage growth and rising oil prices support outlook. Read more.

Mixed Australia employment data: Hiring strong, but job quality slips

Employment jumped 48.9k in February, but unemployment rose to 4.3% as full-time jobs fell and labour supply increased. Underlying softness tempers the strong headline. Read more.

NZ GDP disappoints at 0.2% as momentum fades into year-end

New Zealand GDP rose just 0.2% qoq in Q4, missing expectations and slowing sharply from Q3. Weak construction and flat per capita growth highlight a fragile recovery. Read more.

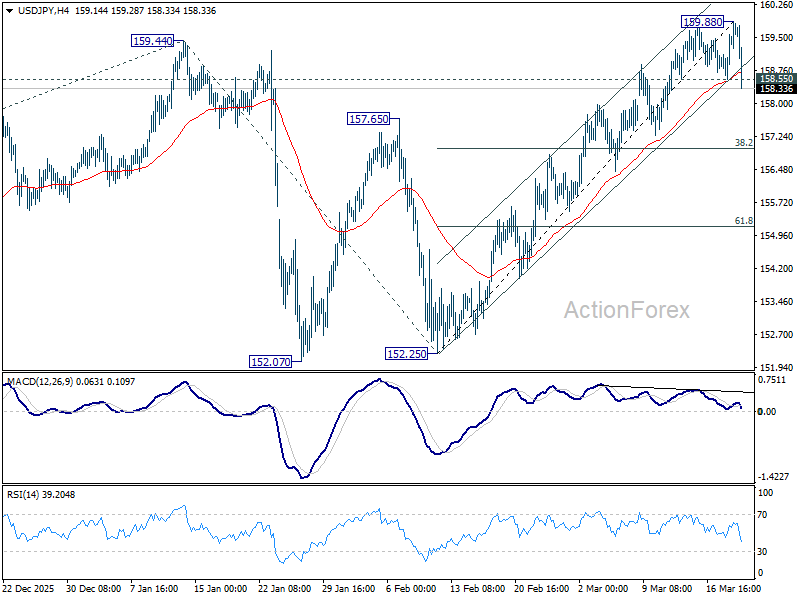

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 159.00; (P) 159.46; (R1) 160.36; More…

USD/JPY’s break of 158.55 support suggests short term topping at 159.88 on bearish divergence condition in 4H MACD. intraday bias is back on the downside. Deeper pullback would be seen to 38.2% retracement of 152.25 to 159.88 at 156.96. For now, near term outlook will be neutral with risk on the downside as long as 159.88 resistance holds, in case of recovery.

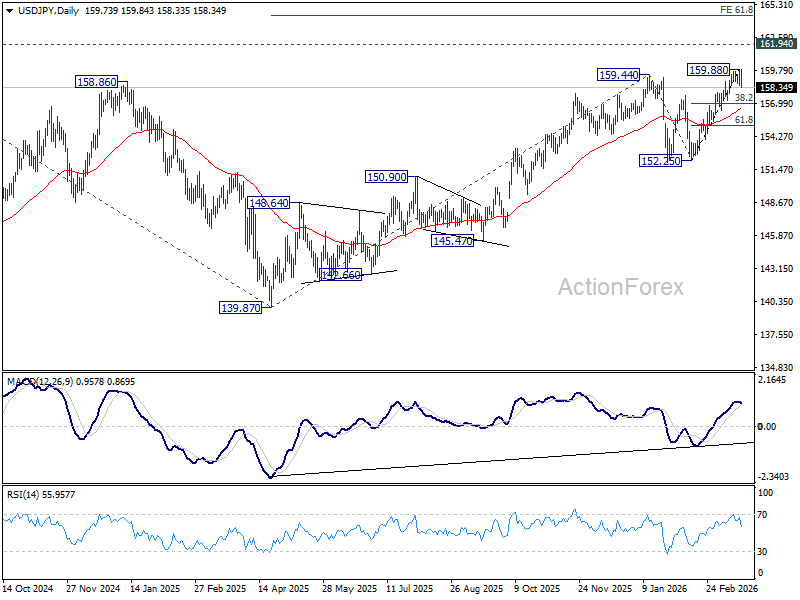

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.70) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

{kind=link}