Dollar is back under mild pressure as US trading gets underway, with markets reacting to a softer-than-feared inflation report from the US. While headline CPI surged in March, the print missed expectations, easing fears of a more aggressive inflation shock. The key relief came from the core reading. Despite the sharp rise in headline inflation driven by energy, underlying price pressures remained contained. This has reassured markets that the inflation spike is not yet broadening into the wider economy.

As a result, the Fed is unlikely to shift its stance. Policymakers have long emphasized their willingness to look through energy-driven inflation shocks, and the latest data does little to challenge that framework. There is no immediate pressure for the Fed to pivot back toward tightening. Market pricing reflects this view. Futures are assigning around a 35% probability of a rate cut before year-end, slightly higher than earlier in the week, suggesting expectations for policy easing remain delayed but not abandoned.

However, the inflation outlook remains tightly linked to geopolitics. The Strait of Hormuz remains shut, and tensions persist despite the two-week ceasefire, with both the US and Iran accusing each other of violations. These developments underscore the fragility of the current truce. Ongoing exchanges involving Israel and Hezbollah, alongside continued disruptions to oil flows, highlight that the situation remains far from resolved. Attention now turns to the upcoming US-Iran talks in Islamabad, which represent a critical inflection point. Markets are waiting to see whether the ceasefire can evolve into a more durable agreement or unravel further.

Beyond the US, the energy shock is once again feeding into global rates markets. Yields in Germany and the UK have surged following reports of potential jet fuel shortages within three weeks, based on the intrinsically linked “energy-inflation-interest rate” cycle. The development has taken EUR/JPY and GBP/JPY notably higher.

Overall for the week so far, Dollar is still the worst performer, followed by Yen, and then Loonie. Kiwi is the best, followed by Aussie and then Sterling. Euro and Swiss Franc are positioning in the middle.

In Europe, at the time of writing, FTSE is up 0.40%. DAX is up 0.80%. CAC is up 0.64%. UK 10-year yield is up 0.099 at 4.777. Germany 10-year yield is up 0.056 at 3.045. Earlier in Asia, Nikkei rose 1.84%. Hong Kong HSI rose 0.55%. China Shanghai SSE rose 0.51%. Singapore Strait Times rose 0.25%. Japan 10-year JGB yield rose 0.045 to 2.442.

US CPI at 3.3% Misses Expectations, Second-Round Effects Still Limited

US inflation surged in March, driven by a sharp jump in energy prices, particularly gasoline. But beneath the headline spike, core inflation remained subdued, showing little sign of broader price pressures. The lack of second-round effects suggests the shock may stay contained—for now. Read More.

Canada Employment Rebound 14.1k in March, Wage Growth Picks Up

Canada’s labor market showed signs of stabilization in March, with employment beating expectations after two months of sharp losses. At the same time, wage growth accelerated to its strongest pace since late 2024, adding another layer to the outlook as policymakers weigh growth risks against inflation pressures. Read More.

BoJ’s Himino Sees No Stagflation Yet, Warns of Oil-Driven Policy Dilemma

BoJ Deputy Governor Ryozo Himino said Japan is not facing stagflation for now, with inflation near target and growth still holding up. But he warned that a prolonged Middle East conflict could change that dynamic—pushing inflation higher while dragging on growth and creating a difficult policy trade-off. Read More.

Japan PPI Accelerates to 2.6% in March as Import Costs Surge 7.9%

Japan’s producer prices picked up more than expected in March, driven by a sharp rise in import costs and higher energy and industrial input prices. The surge in import prices points to renewed upstream inflation pressure, raising the risk that cost increases could feed through more broadly into the economy. Read More.

China PPI Turns Positive for First Time Since 2022 as CPI Softens

China’s factory prices returned to growth for the first time since 2022, driven by rising energy and commodity costs. But consumer inflation is losing momentum, with CPI and core prices slowing sharply—highlighting a growing gap between upstream cost pressures and weak domestic demand. Read More.

NZ BNZ Manufacturing Falls to 53.2, Slower Expansion as War Concerns Weigh on Sentiment

New Zealand’s manufacturing sector is still expanding, but momentum is clearly slowing. PMI eased in March as production and new orders softened, while inventories rose—hinting at cooling demand. Read More.

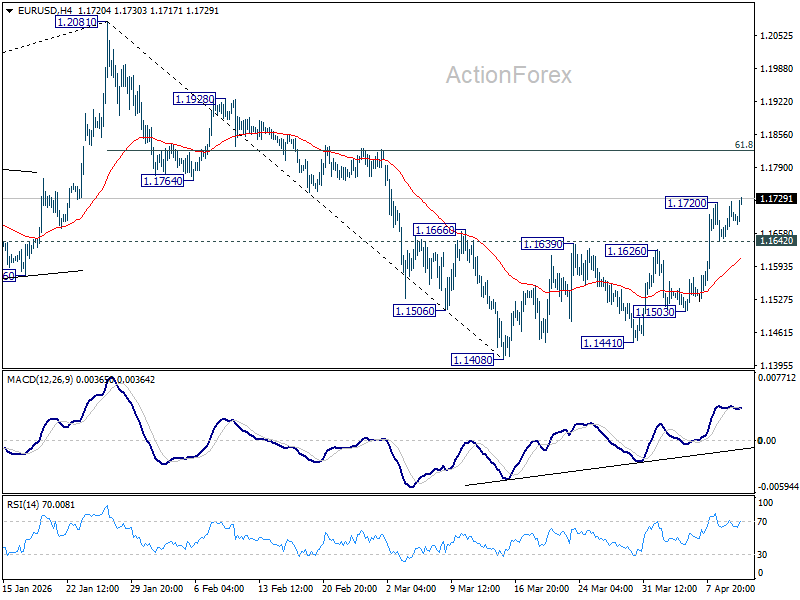

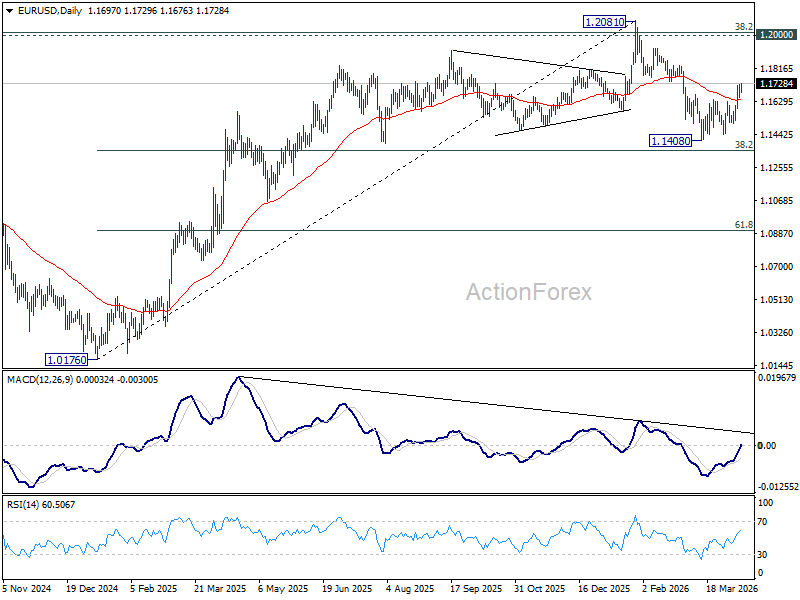

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1658; (P) 1.1692; (R1) 1.1733; More….

Intraday bias in EUR/USD is back on the upside with break of 1.1720 temporary top. Rise from 1.1408 is resuming and should target 61.8% retracement of 1.2081 to 1.1408 at 1.1824. Decisive break there will pave the way to retest 1.2081 high. On the downside, below 1.1642 minor support will turn intraday bias neutral again first.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1505). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

{kind=link}