No surprise from Fed. Below is the full statement.

Federal Reserve issues FOMC statement

Information received since the Federal Open Market Committee met in June indicates that the labor market has continued to strengthen and that economic activity has been rising at a strong rate. Job gains have been strong, on average, in recent months, and the unemployment rate has stayed low. Household spending and business fixed investment have grown strongly. On a 12-month basis, both overall inflation and inflation for items other than food and energy remain near 2 percent. Indicators of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that further gradual increases in the target range for the federal funds rate will be consistent with sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective over the medium term. Risks to the economic outlook appear roughly balanced.

In view of realized and expected labor market conditions and inflation, the Committee decided to maintain the target range for the federal funds rate at 1-3/4 to 2 percent. The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

Voting for the FOMC monetary policy action were: Jerome H. Powell, Chairman; John C. Williams, Vice Chairman; Thomas I. Barkin; Raphael W. Bostic; Lael Brainard; Esther L. George; Loretta J. Mester; and Randal K. Quarles.

But for now, EUR/JPY is held well below 132.40 resistance, GBP/JPY below 150.92, and USD/JPY below 106.63. There is confirmation of bullish trend reversal in these pairs yet.

But for now, EUR/JPY is held well below 132.40 resistance, GBP/JPY below 150.92, and USD/JPY below 106.63. There is confirmation of bullish trend reversal in these pairs yet.

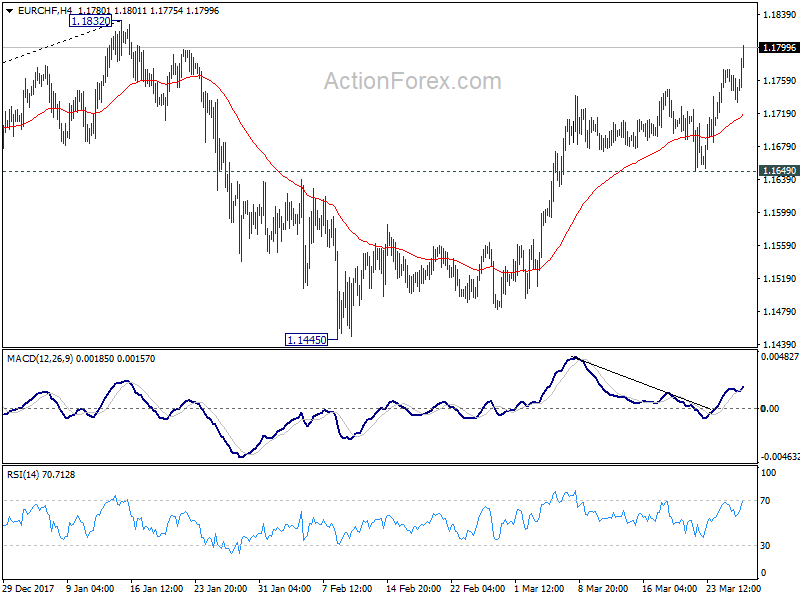

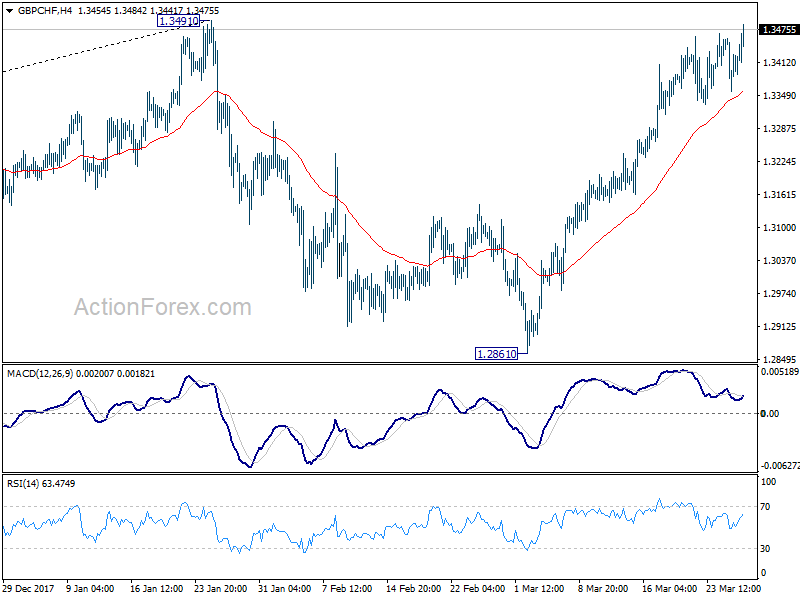

Based on current momentum, 1.1832 in EUR/CHF and 1.3491 in GBP/CHF could be taken out without much problem.

Based on current momentum, 1.1832 in EUR/CHF and 1.3491 in GBP/CHF could be taken out without much problem.

US durable goods orders dropped -17.2%, ex-transport orders dropped -7.4%

US durable goods orders dropped -17.2% to USD 170.0B in April, better than expectation of -18.1%. That’s still the second month of sharp decline, following -16.6% in March. Ex-transport orders dropped -7.4%. Ex-defense orders dropped -16.2%.

Full release here.