Hong Kong stocks tumble sharply today as China confirmed that it’s going to impose its own national security laws in the city. The new legislations are expected to ban any sedition, secession and subversion of the central government run by the Chinese Communist Party. Most importantly, the method used will bypass the city’s own legislative body, effectively violating the “One-Country, Two-Systems” as promised. Hong Kong’s special international status granted by the US and other countries due to the high degree of autonomy is seen as in severe jeopardy..

US President Donald Trump warned that “if it happens we’ll address that issue very strongly.” Senate Majority Leader Mitch McConnell also said, “a further crackdown from Beijing will only intensify the Senate’s interest in re-examining the U.S.-China relationship.” State Department spokesperson Morgan Ortagus urged China to “honor its commitments and obligations to the Sino-British Joint Declaration” of guaranteeing Hong Kong a “high degree of autonomy” until at least 2047. She added, those commitments are “key to preserving Hong Kong’s special status in international affairs, and, consistent with US law, the United States’ current treatment of Hong Kong”.

The last British governor of Hong Kong, Chris Patten, called the move a “comprehensive assault on the city’s autonomy”. “At best, the integrity of ‘one country, two systems’ hangs by a thread,” he added. “Unless the Chinese Communist regime sees sense, this will be hugely damaging to Hong Kong’s international reputation and to the prosperity of a great city.” “UK should tell China this is outrageous”.

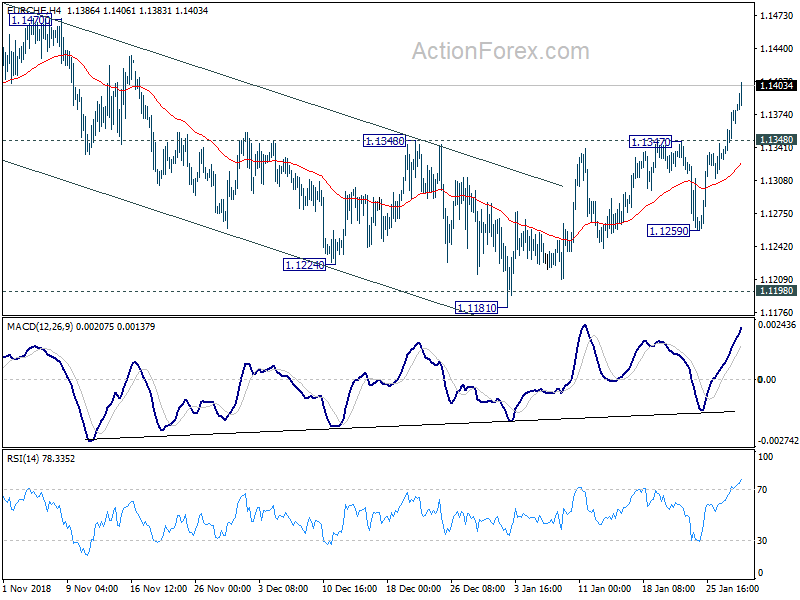

HSI gapped lower today and it’s currently down nearly -4% at the time of writing. The multiple rejection by 55 day EMA, and the break of 23483.31 support today, suggest that corrective rebound form 21139.26 has completed at 24855.47. Deeper fall is now expected for retesting 21139.26 low, or even further to resume the medium term down trend. It remains to be seen if the selloff in Hong Kong stocks would spillover to other markets.

ECB Cœuré: “Winding back globalisation is the wrong solution”

ECB Executive Board member Benoît Cœuré warned of “consequence of protectionism” in a speech at a workshop today.

A few from the speech to note:

Here is the full speech.