Live Comments

UK PMI Manufacturing at Four Month Low, but Faster Output Growth Points to Resilient Recovery

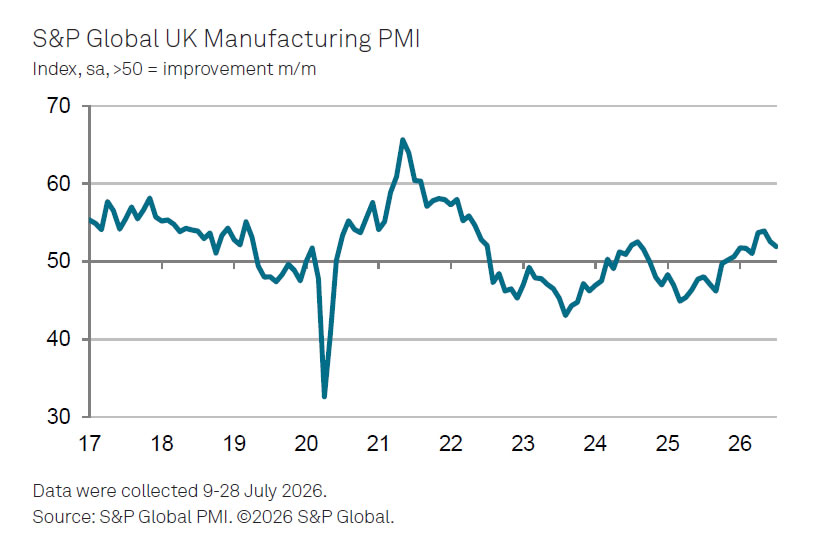

The UK's manufacturing sector lost some momentum in July, with the final S&P Global Manufacturing PMI easing to 51.9 from 52.5 in June, its lowest level in four months. Even so, the index remained above the 50 threshold for a ninth consecutive month, indicating that the sector continues to expand despite a moderation in the pace of improvement.

The details of the survey painted a more encouraging picture than the headline suggested. Manufacturing output rose for a fourth straight month, with production growth accelerating to its fastest pace in nearly two years as stronger market conditions boosted new orders and export demand. Four of the five PMI components remained consistent with improving operating conditions, while the decline in the headline index mainly reflected a sharp reduction in stocks of purchases, slower hiring and a smaller deterioration in supplier delivery times. Growth, however, remained uneven, with medium and large manufacturers outperforming smaller firms, where production declined modestly.

S&P Global also pointed to improving supply and cost conditions. Input cost inflation slowed to a five-month low as supply-chain delays eased to their weakest level since the outbreak of the Middle East conflict, offering manufacturers some relief after months of disruption. Although hiring growth nearly stalled, the first increase in backlogs of work in more than four years suggests labor demand could strengthen if new orders continue to improve. Still, business confidence remained subdued, with geopolitical developments, global trade tensions and the new UK government's industrial and tax policies likely to shape the outlook in the months ahead.

Economic Data

| Indicator | Actual | Previous |

|---|---|---|

| Manufacturing PMI | 51.9 | 52.5 |

| Manufacturing Output | Near 2-year high | Expanded |

| New Orders | Expanded | Expanded |

| New Export Orders | Accelerated | Expanded |

| Employment | Increased | Increased |

| Input Cost Inflation | 5-month low | Higher |

Market Takeaways

- Manufacturing PMI eased from 52.5 to 51.9, a four-month low, but remained above the 50 threshold for a ninth consecutive month, signalling continued expansion.

- Factory output accelerated to its fastest pace in almost two years, supported by stronger domestic and export demand.

- The softer headline PMI largely reflected lower stocks of purchases, slower hiring and a smaller deterioration in supplier delivery times rather than weaker demand.

- Input cost inflation slowed to a five-month low, while supply-chain delays eased to their lowest since the outbreak of the Middle East conflict, providing relief for manufacturers.

- Employment growth nearly stalled despite stronger production, although the first increase in backlogs of work in more than four years suggests hiring could improve if demand remains firm.

- The recovery remained uneven, with medium and large manufacturers outperforming smaller firms, where production continued to decline modestly.

Eurozone PMI Manufacturing At Three-Month High, but Recovery Still Lacks Fresh Demand

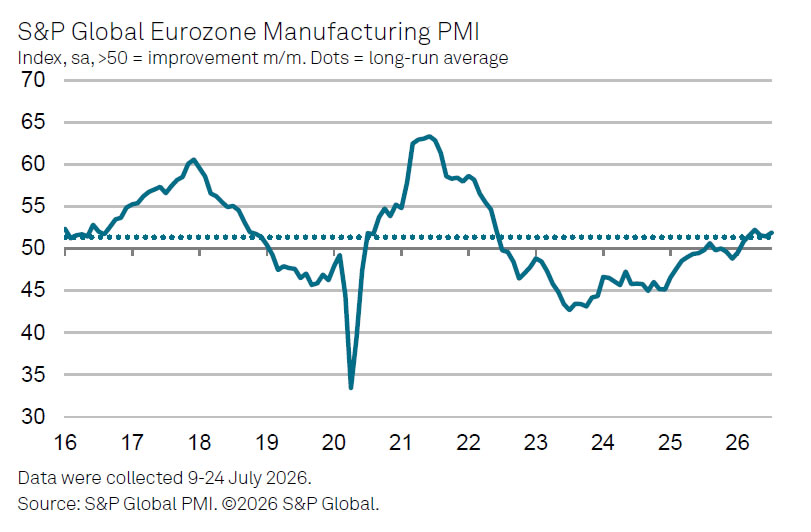

Eurozone manufacturing extended its recovery in July, with the final S&P Global Manufacturing PMI rising to 51.9 from 51.4 in June, marking a three-month high and the strongest improvement in factory conditions since April. Factory output was an even brighter spot, with the Output Index jumping to 52.9 from 51.7, its highest level in 52 months, suggesting production continued to accelerate at the start of the third quarter.

Beneath the headline strength, however, the survey painted a less convincing picture of demand. Output growth was supported largely by manufacturers working through existing order backlogs rather than a meaningful pickup in new business. While new orders continued to increase, the pace remained sluggish, prompting firms to rely on orders secured in previous months to keep production lines running. At the same time, manufacturers continued to trim headcounts, reflecting concerns that current demand may not be sufficient to sustain production once existing backlogs are exhausted.

The recovery also remained highly uneven across the region. Germany led the way with one of its strongest PMI readings in more than four years, while Italy stayed in expansion despite losing some momentum. By contrast, manufacturing activity in France and Spain was broadly stagnant, underscoring the uneven nature of the region's industrial recovery. According to S&P Global's Chris Williamson, several economies continue to struggle with weak demand, elevated prices and lingering supply constraints despite recent improvements.

The survey also suggested that geopolitical risks remain an important headwind. Although supply bottlenecks and energy-related cost pressures eased somewhat in July, tensions in the Middle East continued to keep supply chains under strain and energy prices elevated. With new orders still growing only modestly, the durability of the current recovery will depend on whether demand strengthens enough to replace the backlog-driven boost to production. Until then, the impressive rise in output may prove stronger than the underlying health of the manufacturing sector.

Economic Data

| Indicator | Actual | Previous |

|---|---|---|

| Eurozone Manufacturing PMI | 51.9 | 51.4 |

| Eurozone Output Index | 52.9 | 51.7 |

Market Takeaways

- Eurozone Manufacturing PMI rose from 51.4 to 51.9, reaching a three-month high and signalling the strongest improvement in factory conditions since April.

- The Output Index jumped from 51.7 to 52.9, its highest level in 52 months, pointing to a sharp acceleration in manufacturing production.

- Production growth continued to outpace demand, with manufacturers relying on existing order backlogs as new orders increased only modestly.

- Germany remained the region's manufacturing leader, while Italy stayed in expansion despite slowing. France and Spain were broadly stagnant, highlighting an uneven regional recovery.

- Manufacturers continued to reduce employment, reflecting concerns that current production may not be sustainable without a stronger pickup in new business.

- Although supply bottlenecks and energy-related cost pressures eased slightly, Middle East tensions continued to keep supply chains under strain and inflationary pressures elevated, posing risks to the durability of the recovery.

Swiss CPI Slips to 0.4% in July on Lower Fuel and Airfare Costs

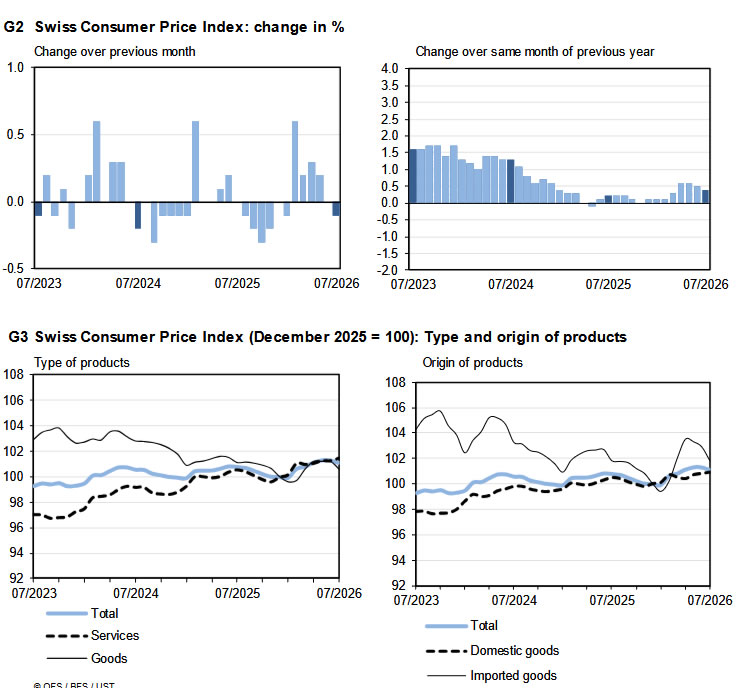

Switzerland's CPI fell -0.1% mom in July, pulling annual inflation down to 0.4% from 0.5% in June, according to the Federal Statistical Office. The decline was largely driven by lower prices for air transport, diesel and petrol, while seasonal discounts also pushed clothing and footwear prices lower. Despite the softer headline reading, inflation remained positive on an annual basis, extending Switzerland's low-inflation environment.

The broader breakdown suggests price pressures eased mainly through imported goods rather than domestic demand. Imported product prices fell -1.1% mom on the month, a much steeper decline than June's -0.4% fall, leaving annual imported inflation at 0.0% yoy. By contrast, domestic product prices rose 0.1% mom on the month and held steady at 0.5% yoy, while core inflation remained unchanged at 0.3% yoy despite a -0.1% mom decline.

Not all price categories weakened during the month. The FSO said prices for other parahotel accommodation, heating oil, car rental and car sharing all increased, partially offsetting declines elsewhere. Overall, the July report reinforces the picture of subdued inflation in Switzerland, with lower energy and transport costs continuing to suppress headline inflation even as domestic price pressures remain relatively stable.

Economic Data

| Indicator | Actual | Previous |

|---|---|---|

| CPI (m/m) | -0.1% | 0.0% |

| CPI (y/y) | +0.4% | +0.5% |

| Core Inflation (m/m) | -0.1% | 0.0% |

| Core Inflation (y/y) | +0.3% | +0.3% |

| Domestic Products (m/m) | +0.1% | +0.1% |

| Domestic Products (y/y) | +0.5% | +0.5% |

| Imported Products (m/m) | -1.1% | -0.4% |

| Imported Products (y/y) | 0.0% | +0.2% |

Market Takeaways

- Headline CPI eased from +0.5% y/y to +0.4% y/y, while consumer prices fell 0.1% m/m, reflecting another month of subdued inflation.

- Lower airfares, diesel, petrol, and seasonal discounts on clothing and footwear were the main drivers of the monthly decline.

- Core inflation held steady at +0.3% y/y, suggesting underlying inflation pressures remained contained despite the softer monthly reading.

- Domestic inflation remained stable at +0.5% y/y, indicating price pressures generated within the Swiss economy have changed little.

- Imported prices were the main source of disinflation, falling 1.1% m/m and leaving annual imported inflation at 0.0%, highlighting the continued influence of lower energy and other imported costs.

- Higher prices for other parahotel accommodation, heating oil, car rental and car sharing only partly offset the broader decline in consumer prices.