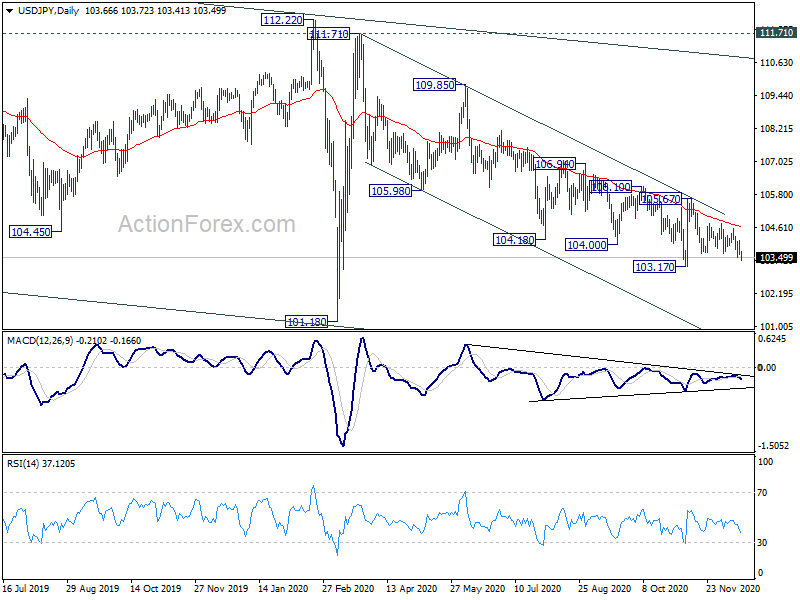

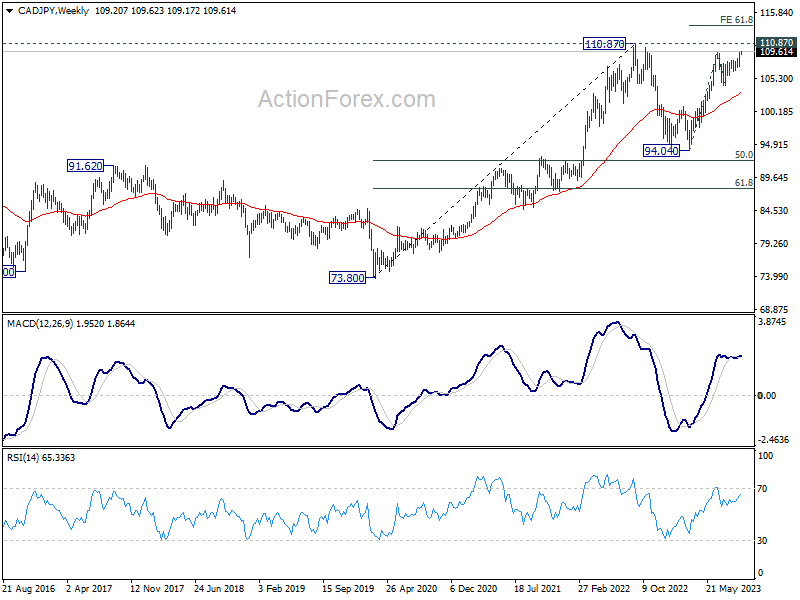

Yen rally accelerates as risk aversion intensifies in US session. At the time of writing, DOW is down -0.44%, S&P 500 down -0.47%. NASDAQ is suffering serious selling and is down -1.22%. In Europe, DAX led the decline and closed down -1.36%, CAC down -1.10% and FTSE down -1.16%.

In the currency markets, Australian Dollar is the second strongest one, New Zealand Dollar the third. Sterling is the weakest, followed by Euro and Canadian.

We see some reports blaming Asia and China for risk aversion. But this is apparently wrong and ignorant considering the lack of weakness in Aussie and Kiwi. Italy is the problem for Europe as Italian yield rose 0.1602 to 3.566. Germany 10 year yield, on the other hand dropped -0.0442 to 0.533. One might argue that Swiss Franc is steady. But the Franc has proven itself recently that it showed more reactions to emerging markets like Turkey and Argentina rather than Italy. Another factor for risk version is of course US yield.

Having said that, we don’t mean it’s problem free for Asia. Given that Chinese Yuan suffers some renewed pressure today, it’s just a matter of time when China’s stock break through that critical 2700 handle, or USD/CNH breaking 7. It’s reported that the US Treasury is concerned with Yuan depreciation. When the US is in an “easy to win” trade war with China, it’s the most reasonable outcome for China’s economy to get hurt and the exchange rate reflect that fundamental and falls. And further depreciation in Yuan will without a doubt drags down Chinese stocks.

France PMI services finalized at 50.3 in Apr, first expansion in eight months

France PMI Services was finalized at 50.3 in April, up from march’s 48.2. That’s the first expansion reading in eight months. PMI Composite was finalized at 51.6, up from 50.0 in March, first expansion for eight months too.

Eliot Kerr, Economist at IHS Markit said: “The key takeaway from the latest release of PMI data is that following a prolonged period of downturn, underlying demand conditions are now beginning to recover as vaccine roll-outs give firms the confidence to look beyond the crisis. That demand has translated into new business and increased activity levels across the service sector as a whole.”

Full release here.