Live Comments

Fed’s Daly: Businesses Have Limited Ability to Raise Prices

San Francisco Fed President Mary Daly said there are growing reasons to believe inflation will moderate without additional monetary tightening, arguing that businesses are finding it increasingly difficult to pass higher costs on to consumers. Speaking at an economics conference in Tokyo, Daly said she was "completely supportive" of last week's decision to keep interest rates unchanged, stressing that policymakers still need more evidence before deciding whether inflation is being driven by temporary supply shocks or more persistent forces. "We have a lot of information we need to collect" ahead of the September FOMC meeting, she said.

Daly pointed to several factors that could help ease inflation in the months ahead. Most notably, she argued that businesses now have "limited pricing power" and will struggle to pass rising input costs through to customers. She also said there are "good reasons" to believe the supply-driven shocks that have fueled inflation "will not have a lasting impact," adding that an eventual end to the Middle East conflict should lower oil prices and reduce one of the public's biggest inflation concerns. Together, those developments support the case for allowing more time to assess incoming data before adjusting policy.

Even so, Daly emphasized that patience should not be mistaken for complacency. She warned the Fed must remain "vigilant to watch the information as it comes in, but be very prepared to take action" if inflation proves more persistent than expected. While she acknowledged concerns that renewed inflation could become embedded in public expectations, her remarks place her firmly among the policymakers who believe the current evidence still justifies waiting rather than preemptively raising interest rates.

Key Takeaways

- San Francisco Fed President Mary Daly fully supported last week's decision to keep interest rates unchanged, saying policymakers need more data before deciding whether inflation pressures are temporary or persistent.

- Daly argued that businesses now have limited ability to pass higher costs on to consumers, suggesting pricing power is weakening and inflation could moderate without additional tightening.

- She also cited three supportive factors for disinflation: fading supply shocks, the prospect of lower oil prices if Middle East tensions ease, and consumers' sensitivity to energy prices.

- Despite her relatively optimistic outlook, Daly stressed the Fed must remain "vigilant" and "be very prepared to take action" if inflation momentum begins building again.

- Her comments place her firmly in the Fed's wait-and-see majority, contrasting with officials who have recently advocated resuming rate hikes immediately.

Cook Says Fed Can’t Afford to Wait Forever on Inflation

Federal Reserve Governor Lisa Cook said policymakers cannot afford to be complacent after more than five years of above-target inflation, warning that patience has limits if price pressures fail to ease. Speaking on Wednesday, Cook reiterated that "inflation is too high" despite some improvement in June, stressing that she would "not put too much weight on a single data point" given the highly uncertain environment. While she supported leaving interest rates unchanged at last week's FOMC meeting, she made clear that "I am prepared to act by raising rates, if necessary."

Cook argued that inflation risks continue to outweigh labor market risks, citing elevated energy prices linked to the Middle East conflict and AI-driven investment as two unexpected sources of upward pressure on prices. Together, she said, these developments "have shifted the balance of risks toward inflation and away from the labor market." At the same time, she characterized employment as stable in a "low-hire, low-fire environment," with subdued hiring offset by historically low layoffs. That backdrop, in her view, allows the Fed to remain focused on restoring price stability.

Even so, Cook explained why she supported holding rates for now. She pointed to three disinflationary forces already emerging: fading tariff effects, the prospect of lower oil prices later this year, and easing AI-related goods inflation as supply chains adjust. Those factors could help bring inflation back toward target without further tightening. However, she warned that "if I do not see signs of continued disinflation soon, I am prepared to act," adding that "we do not have that luxury" of waiting indefinitely because prolonged above-target inflation risks becoming entrenched in wage- and price-setting behavior.

Key Takeaways

- Fed Governor Lisa Cook said inflation remains "too high" and the Fed "can't afford to wait forever" if price pressures fail to continue easing.

- While she supported keeping rates unchanged last week, Cook stressed she is "prepared to act by raising rates, if necessary" should disinflation stall.

- Cook argued that inflation risks currently outweigh labor market risks, citing higher energy prices from the Middle East conflict and AI-related investment as key drivers of persistent inflation.

- She described the labor market as a "low-hire, low-fire environment," with stable unemployment reflecting subdued hiring but also historically low layoffs.

- Cook identified three potential disinflationary forces—fading tariff effects, lower oil prices later this year, and easing AI-related supply constraints—as reasons to remain on hold for now.

- However, she warned that prolonged above-target inflation risks becoming entrenched, leaving the Fed with less room to wait if inflation progress stalls.

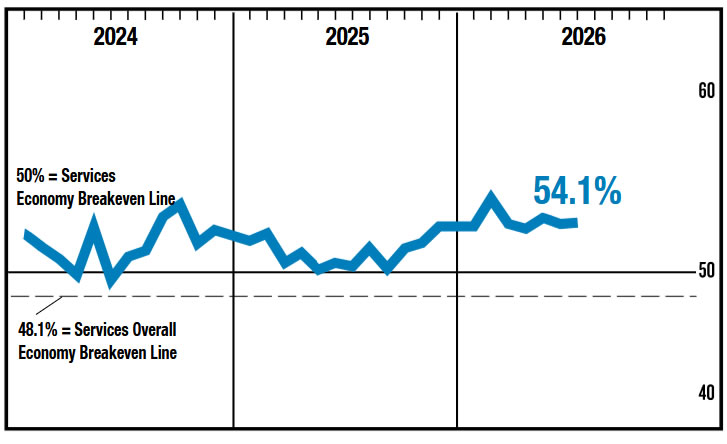

US ISM Services Holds Firm at 54.1 as Employment Contracts, Prices Accelerate

The US services sector continued to expand at a healthy pace in July, suggesting the economy remains resilient even as cracks emerge in the labor market. The ISM Services PMI edged up to 54.1 from 54.0, remaining comfortably above its 12-month average of 53.4. According to ISM's historical relationship, the latest reading is consistent with 1.9% annualized real GDP growth, indicating that overall economic activity continues to expand despite growing uncertainty over monetary policy and the outlook for employment.

Beneath the steady headline, however, the report revealed a more mixed picture. The Employment Index dropped sharply to 47.4 from 51.2, slipping back into contraction after just one month of growth. Survey respondents pointed to modest workforce reductions, with some firms citing AI adoption while others continued shifting jobs to lower-cost overseas locations. The weaker employment reading follows softer ADP payroll data earlier in the day, reinforcing signs that hiring momentum in the US economy is cooling.

Inflation pressures, meanwhile, moved in the opposite direction. The Prices Index climbed to 70.3, up from 67.7, marking the 110th consecutive month of rising input costs and lifting its 12-month average to the highest level since April 2023. The combination of resilient activity, softer hiring and firmer prices leaves the Federal Reserve with a familiar policy dilemma. While slowing employment supports the case for patience, persistent cost pressures are likely to keep policymakers cautious about declaring victory over inflation.

Data Summary

| Indicator | July 2026 | June 2026 | Trend |

|---|---|---|---|

| ISM Services PMI | 54.1 | 54.0 | ▲ Slight improvement |

| Market Expectation | 54.2 | — | Slight miss |

| Business Activity | 59.1 | 55.4 | ▲ Strong acceleration |

| New Orders | 57.2 | 55.1 | ▲ Demand strengthened |

| Employment | 47.4 | 51.2 | ▼ Back to contraction |

| Prices Paid | 70.3 | 67.7 | ▲ Inflation pressures intensified |

| New Export Orders | 52.0 | 50.4 | ▲ Faster expansion |

| Imports | 51.8 | 49.4 | ▲ Returned to growth |

| Backlog of Orders | 50.9 | 54.9 | ▼ Growth slowed |

| Supplier Deliveries | 52.8 | 54.4 | ▼ Delivery delays eased |

Key Takeaways

- ISM Services PMI edged up to 54.1 in July, signaling a 25th consecutive month of expansion and pointing to 1.9% annualized real GDP growth according to ISM's historical relationship.

- Business activity (59.1) and new orders (57.2) accelerated, indicating demand across the services sector remained healthy despite a softer macro backdrop.

- The Employment Index dropped sharply to 47.4, slipping back into contraction after one month above 50 and reinforcing earlier signs from the ADP report that labor demand is cooling.

- Survey respondents cited AI adoption, workforce reductions and continued hiring shifts to lower-cost overseas locations as factors behind weaker employment.

- The Prices Paid Index jumped to 70.3, marking the 110th consecutive month of rising input costs and its highest 12-month average since April 2023.

- The report delivers a mixed signal for the Fed: solid economic activity argues against recession concerns, while weaker hiring supports patience, but stronger price pressures keep inflation risks alive.