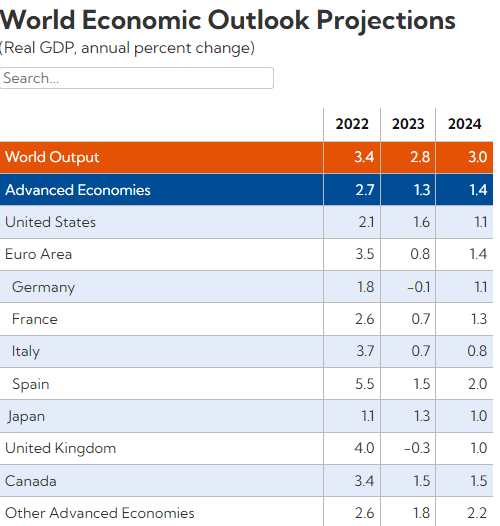

The IMF released its World Economic Outlook, projecting global growth to slow from 3.4% in 2022 to 2.8% in 2023 and bottom there, and then rise to 3.0% in 2024. Global inflation is expected to decelerate from 8.7% in 2022 to 7% in 2023 and further to 4.9% in 2024.

Pierre-Olivier Gourinchas, Economic Counsellor and Director of Research at IMF, said in a blog post, “The global economy’s gradual recovery from both the pandemic and Russia’s invasion of Ukraine remains on track. China’s reopened economy is rebounding strongly. Supply chain disruptions are unwinding, while dislocations to energy and food markets caused by the war are receding. Simultaneously, the massive and synchronized tightening of monetary policy by most central banks should start to bear fruit, with inflation moving back towards targets.”

For 2023, global growth projections were reduced by 0.1% compared to January’s forecast. US growth was revised up by 0.2% to 1.6%, Eurozone growth by 0.1% to 0.8%, and UK growth by 0.3% to -0.3%. However, Japan’s growth projection was revised down sharply by 0.5% to 1.3%. Canada and China’s growth forecasts remained unchanged at 1.5% and 5.2%, respectively.

Regarding interest rates, the IMF believes recent increases in real interest rates are likely temporary. Once inflation is under control, advanced economies’ central banks are expected to ease monetary policy and bring real interest rates back towards pre-pandemic levels.

Full IMF Worl Economic Outlook here.

China to announce retaliation measures to US at 0830GMT

Upcoming at 16:30 Beijing time, 0830 GMT, China’s commerce and finance ministries will hold a press briefing regarding the US Section 301 tariffs. It believed that retaliatory measure will be announced during the briefing. China has pledged to take counter measures at the same intensity and proportionality. But no detail is leaked so far. The worst for the market is that China’s response will prompt counter retaliation by the US. That could lead to escalating tariffs that drastically reduce the trade activities between the two countries.

China’s envoy to the WTO, Zhang Xiangchen criticized that the tariffs on USD 50b of China import to the US is “an intentional and gross violation of the WTO’s fundamental principles of non-discrimination and bound tariffs.” And he urged other WTO members to “join with China in firmly resisting U.S. protectionism”.

Reactions to US announce of the product list of Section 301 tariffs were initially muted. Japan Nikkei has indeed closed up 0.13%. But fear in the stock markets start to build up with Hong Kong HSI suffering sharp fall in the afternoon, and is trading down -1.44%.