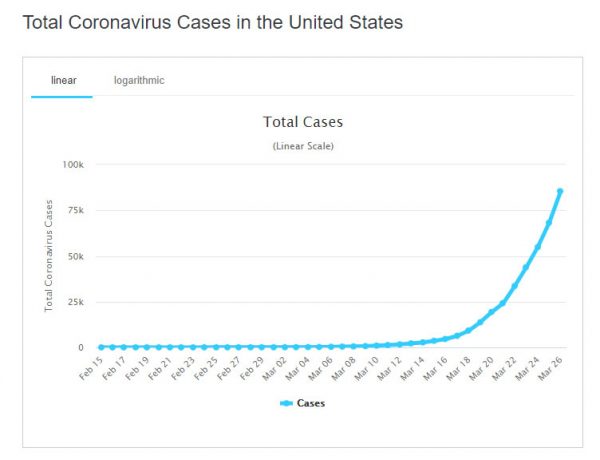

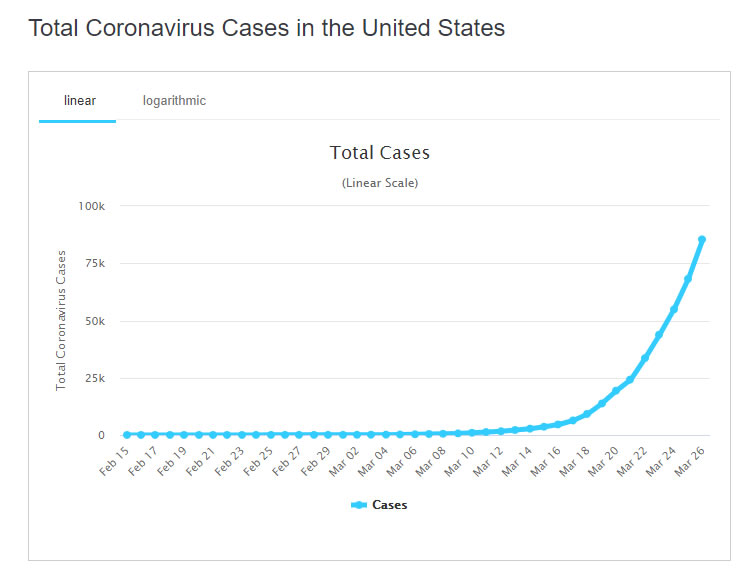

Strong rebound in US stocks continued overnight with DOW wrapped up its strongest three-day rally since 1931. At the same time number of confirmed coronavirus cases in the US surged through China, and Italy, as the pandemic worsens. Total infections now reached 85,594, versus 81,340 as “reported” in China and 80,589 in Italy. Coronavirus deaths in the US hit 1,300, relatively low comparing to Italy’s 8,215, Spain’s 4,365 and China’s “reported” death of 3,292.

New York state is hardest hit with 38,977 infections and 466 deaths. New Jersey (6,876), California (4,044), Washington(3,207) and Michigan (2,856) are quite far behind. New York Governor Andrew Cuomo warned, “any scenario that is realistic will overwhelm the capacity of the healthcare system.” The projected shortfall in ventilators is “astronomical” according to Cuomo.

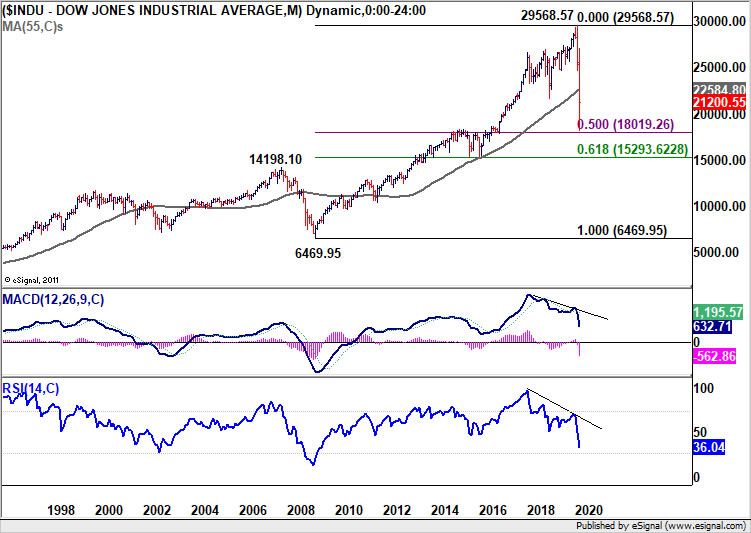

DOW rose 1351.62 pts or 6.38% to close at 22552.17. Corrective target of 38.2% retracement of 29568.57 to 18213.65 at 22551.22 is met already. Upside momentum is starting to diminish as seen in hourly MACD. But there is no sign of topping yet. Thus, further rally could still be seen into early part of next week.

However, we’d expect the correction to complete anywhere between 22551 and 61.8% retracement at 25230.99. Break of 55 hour MACD would likely indicate completion of the rebound and bring retest of 18213.65 low.

BoC cuts overnight rate to 0.25%, starts government securities purchases

In an unscheduled announced, BoC decided to lower overnight rate by -50bps to 0.25%. Bank rate is then correspondingly at 0.50% and deposit rate at 0.25%. BoC said, “this unscheduled rate decision brings the policy rate to its effective lower bound and is intended to provide support to the Canadian financial system and the economy during the COVID-19 pandemic.”

Additionally, BoC launches two new programs. Firstly, the Commercial Paper Purchase Program (CPPP) will help to alleviate strains in short-term funding markets and thereby preserve a key source of funding for businesses. Secondly, to address strains in the Government of Canada debt market and to enhance the effectiveness of all other actions taken so far, the Bank will begin acquiring Government of Canada securities in the secondary market. Purchases will begin with a minimum of $5 billion per week, across the yield curve.

Full statement here.