Selloff in European majors, led by Sterling, intensify in European session today. It now looks like Brexit negotiation has not just stalled, but regressed. UK Prime Minister Theresa May’s spokesman James Slack said the Cabinet has backed May in Brexit and expects them to continue to do so. But apparently, May is starting to lose support even from the remain camp in her party. May is moving backward.

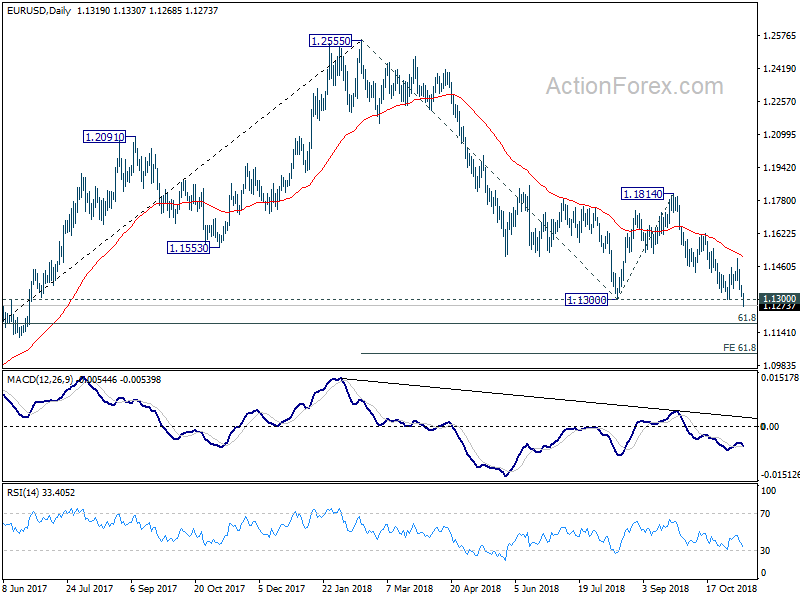

Euro is not far behind with EUR/USD taken out 1.13 key support firmly. EUR/JPY also broke 128.60 near term support. Italian Prime Minister office denied that there would be a cabinet meeting on budget today. Deputy Prime Minister Luigi Di Maio continued with populist rhetoric and said respecting EU budget limit is suicidal. We’ll see what revised plan they’re going to re-submit to the European Commission tomorrow.

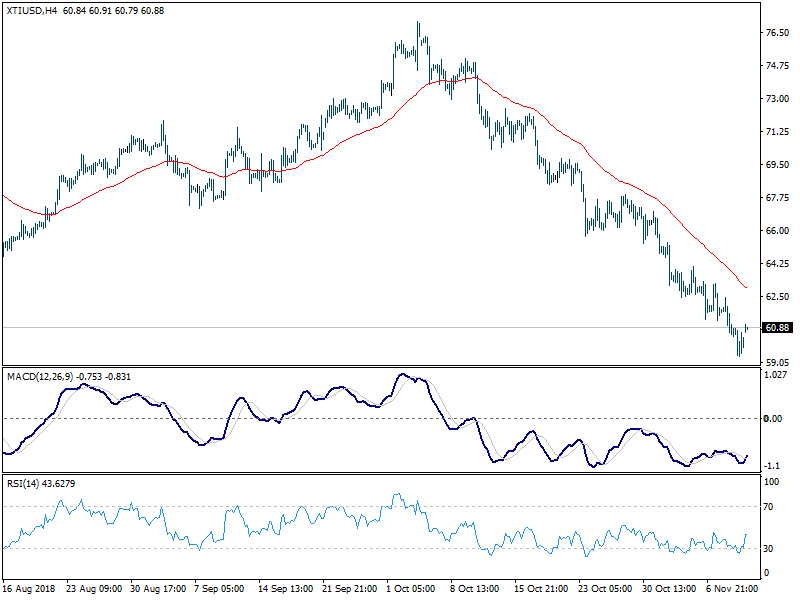

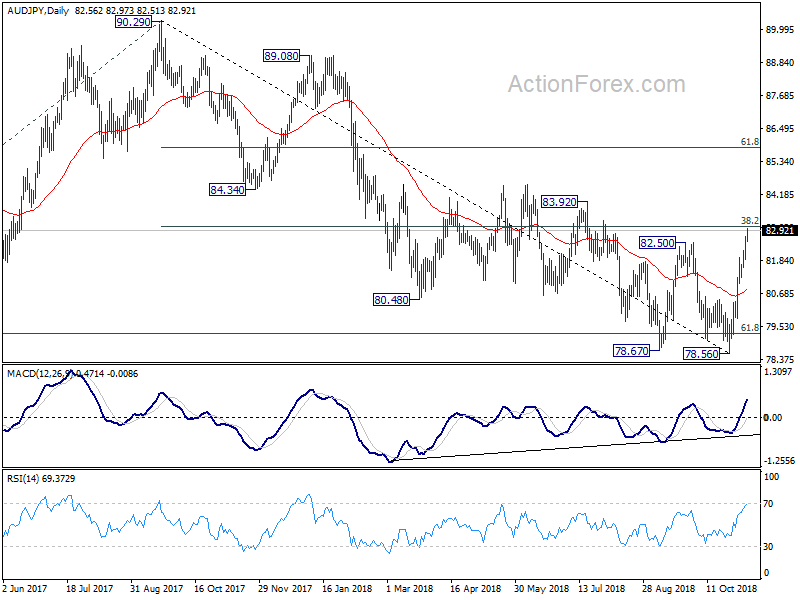

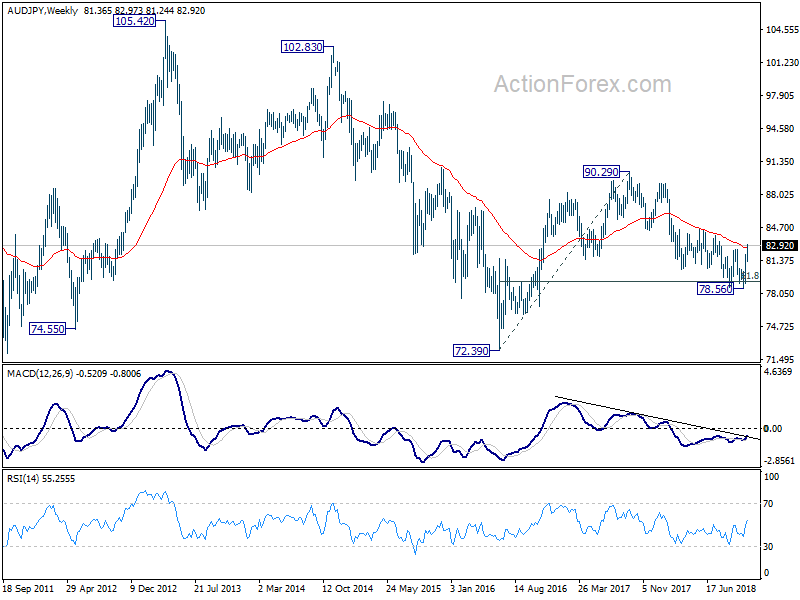

For now, Canadian Dollar is trading as the strongest one for today. But that’s firstly because it’s digesting last week’s broad based loss. Secondly, Canada is not at the center of any storm for now. Third, WTI crude oil recovers today on Saudi Arabia’s export cut and is back above 60. Dollar is the second strongest, followed by Yen and both are showing promising technical developments.

In other markets, major European indices are soft today. At the time of writing:

- FTSE is flat

- DAX is down -0.70%

- CAC is down -0.16%

- German 10 year yield is down -0.0198, at 0.389, back below 0.4

- Italian 10 year yield is up 0.034 at 3.432. That is, spread with German is back above 300

Earlier in Asia:

- Nikkei rose 0.09% to 22269.88

- Hong Kong HSI rose 0.12% to 25633.18

- China Shanghai SSE rose 1.22% to 2630.52. But that’s seen mainly as gap covering.

- Singapore Strait Times dropped -0.32% to 3068.15

Sterling off low as main elements of Brexit text ready. But EU also said some key issues remain under discussion

Sterling is given a lift off today’s low after Financial Times reported that the main elements of a Brexit treaty text are ready. According to EU chief Brexit negotiator Michel Barnier, the documents could be presented to the UK cabinet on Tuesday.

However, it should be noted that it’s a “known” that the “main elements” are ready. A few weeks ago, it was like 95% completed. Now it maybe 99.9%. But it’s not done until all is done. There is so far no news regarding the Irish backstop. So the piece of news is not so much news.

Also, Barnier briefed EU ministers on negotiation progress today. The post meeting statement is rather reserved. The EU statement noted:

—

The Commission’s chief Brexit negotiator, Michel Barnier, informed the EU27 ministers of the situation following negotiations with the UK over the last few weeks. Michel Barnier explained that intense negotiating efforts continue, but an agreement has not been reached yet. Some key issues remain under discussion, in particular a solution to avoid a hard border between Ireland and Northern Ireland.

“In these final stages of the negotiations, ministers showed again today that we are determined to keep the unity of the EU 27. We have reconfirmed our trust in the negotiator. And we support his efforts to continue working towards a deal.”

Gernot Blümel, Austrian Federal Minister for the EU, Art, Culture and Media

During the meeting, ministers however also recalled the need to continue the work at all levels on preparations for every possible scenario.

Full statement here.

—

It doesn’t sound like there is any breakthrough.