Markets will be looking to the September US jobs report for direction after a mostly unchanged dot plot chart by the FOMC this week failed to clear the fog for the 2019 rate outlook. Apart from the nonfarm payrolls report, monthly PMI readings out of China, the United Kingdom and the United States will also be important. In the central bank spectrum, the Reserve Bank of Australia will be the only major bank holding a policy meeting next week. Meanwhile, trade and political developments will remain at the forefront as another NAFTA deadline passes without a deal and the UK prime minister faces her Brexit plan critics at the Conservative party conference.

Aussie eyes RBA meeting and China PMIs

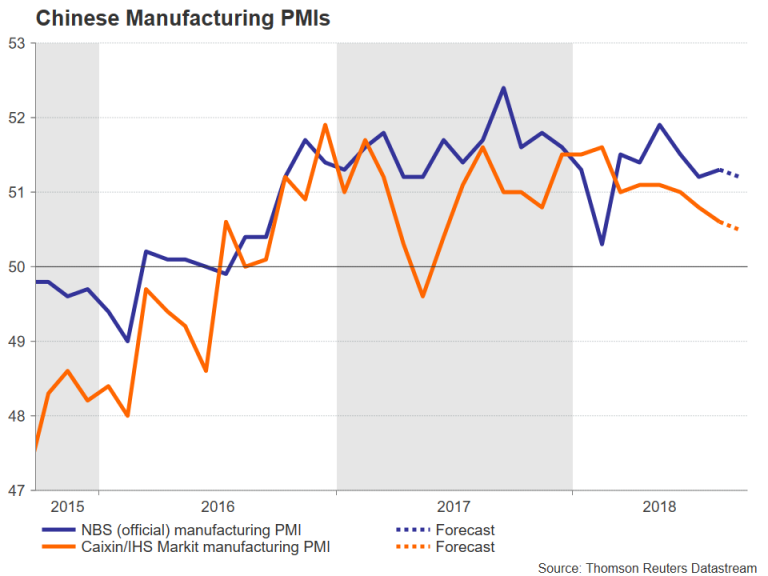

The Australian dollar regained some positive footing in September on the back of increasing evidence from data that supports the RBA’s upbeat forecasts on economic growth. However, lingering global trade tensions have restrained more significant advances and the aussie could face some more negative pressure on Monday if Chinese PMI readings due on Sunday indicate a further easing in manufacturing activity in September. Markets in China will be closed for the whole of next week so both the official and Caixin/Markit PMIs will be released on Sunday. The government’s print on the manufacturing sector is expected to show the PMI index dropping slightly to 51.2 in September. The private Caixin/Markit PMI is also projected to deteriorate, falling from 50.6 to 50.5, which would make it a 15-month low.

Moving to domestic events, the RBA is widely expected to keep its cash rate unchanged at 1.5% on Tuesday and will likely reiterate that inflation and wage growth are anticipated to pick up only gradually, despite stronger economic fundamentals. In terms of data, aussie traders should keep an eye on building approvals on Wednesday, trade figures on Thursday and retail sales on Friday, all for August.

Canadian jobs data to be watched for BoC rate clues

A stalemate in the NAFTA talks has dragged the Canadian dollar away from 3½-month highs reached in mid-September. With Canada refusing to compromise on key issues and subsequently missing a key October 1 deadline, the US looks set to increase the pressure by moving ahead with its bilateral trade deal with Mexico without the participation of the Canadians. However, the slow progress risks an even more drastic action by the Trump administration such as imposing tariffs on Canadian auto imports.

But any escalation in the trade spat between the US and Canada is unlikely to deter the Bank of Canada from raising interest rates in late October and employment figures due on Friday would increase the market odds for a rate hike if jobs growth bounces back in September following a big fall in August. In other data, the September Ivey PMI are out on Thursday, while also on Friday, the trade numbers for August are scheduled for release.

BoJ Tankan survey to point to continuation of moderate growth

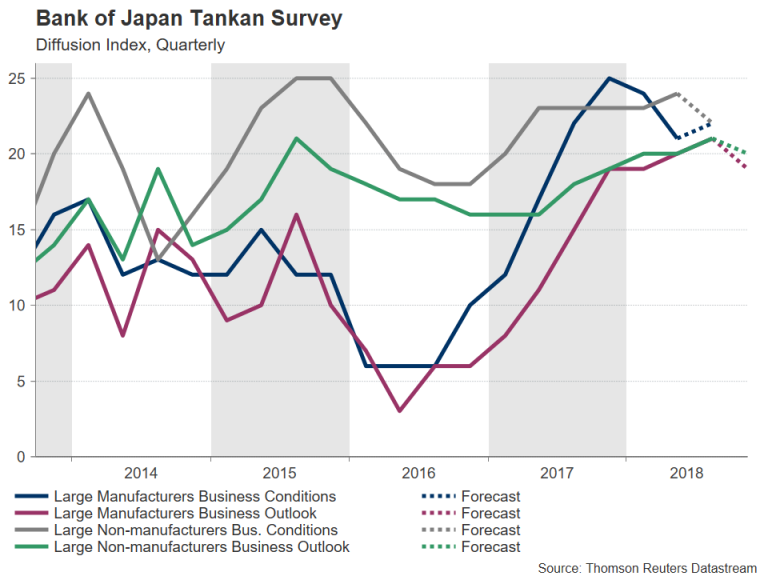

US President Trump had better to words to say for his Japanese counterpart this week than for the Canadian prime minister as the US and Japan agreed on a framework to start bilateral trade talks (something Japan had been resisting until now). The agreement means Japan avoids US duties on its car exports for the time being, in a major relief for the country’s dominant manufacturing sector. However, the Bank of Japan’s closely-watched quarterly Tankan sentiment survey due on Monday will likely show Japanese businesses remain cautious about the prospects for the fourth quarter. A slight dip is forecast for the indices measuring the outlook for big manufacturers and non-manufacturers. As for the current quarter, large manufacturers are expected to become slightly more optimistic, but analysts are anticipating large non-manufacturers to turn slightly less positive.

The yen will probably be unmoved by the Tankan survey but could see some reaction to the latest wage growth numbers coming up on Friday. Overall earnings growth in Japan fell back to 1.6% in July after jumping to a 21-year high of 3.3% in June. A rebound in August would signal that wage growth remains on an upward path and that would bode well for domestic demand. Also out on Friday are household spending figures for August.

Absence of major data to keep euro focus on Italy

The Eurozone economic calendar will consist mostly of mid-tier data, meaning traders’ attention will probably remain on political happenings in Rome as Italy’s coalition government scrambles to put together a budget that satisfies EU fiscal rules as well as meet the parties’ election pledges. First up on the release schedule are the final manufacturing PMI print for September and the August unemployment rate on Monday. They will be followed by August producer prices for August on Tuesday. On Wednesday, the final services and composite PMIs are due, along with retail sales figures for August. Finally, German industrial orders for August will be monitored on Friday for a turnaround in factory orders following two straight months of sharp declines.

UK’s May under the spotlight

British Prime Minister, Theresa May’s Brexit plans will come under the scrutiny of her Conservative party members as the party’s annual conference gets under way on September 30. May will address her divided party on the closing day on Wednesday as she attempts to win the backing from both Conservative remainers and Brexiteers for her controversial Chequers plan.

EU leaders rejected the core elements of the Chequers plan at an informal summit on September 20, driving the pound lower. But hopes that a deal could still be reached led sterling to recover to around the $1.32 level before falling back again. The rebound could be shortlived, however, if May suffers another humiliation at her party conference and senior Conservatives become even more vocal in urging her to ditch her plan in favour of a Canada-style free trade agreement with the EU.

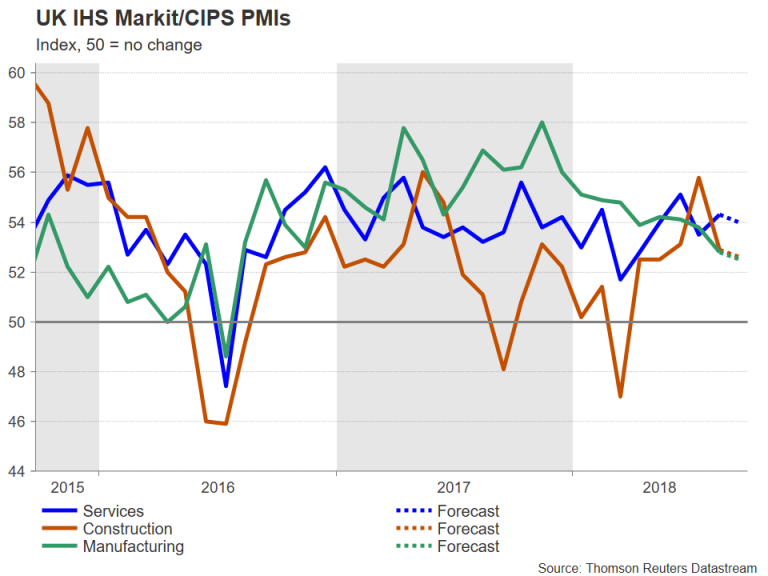

The ongoing Brexit drama could overshadow PMI figures out of the UK in the coming week. The manufacturing PMI, which has been on a downward path since late 2017, is released first on Monday and will be followed by the construction and services PMIs on Tuesday and Wednesday, respectively. All three PMIs are forecast to decline in September.

US wage growth to hit 3%

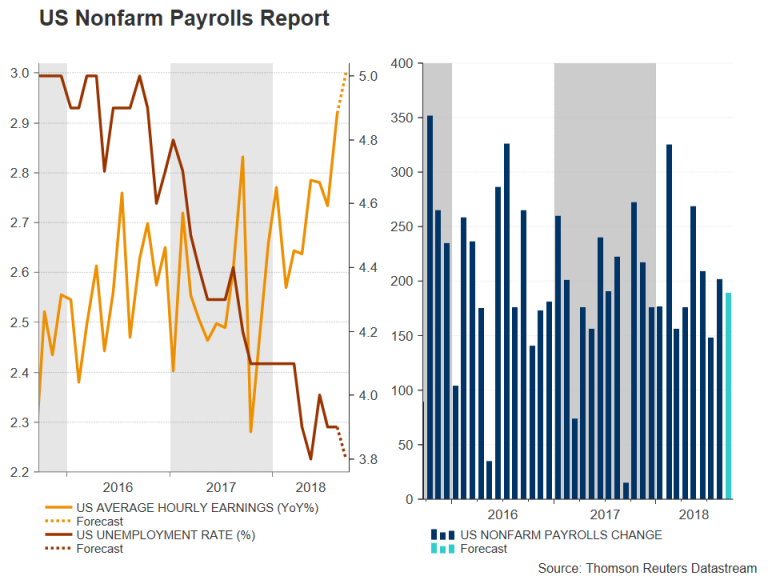

The US dollar got a lift from the Fed’s September policy meeting in the past week as Chairman Jerome Powell signalled that rates would continue to go up even if they are nearing their perceived neutral level. The greenback could get an additional boost from the latest jobs report due on Friday, but before then, there will be plenty of other data for traders to watch.

After a surprise surge in August, the ISM manufacturing PMI is expected to ease marginally in September when released on Monday. The ISM’s non-manufacturing PMI will follow on Wednesday and is also forecast for a slight drop in September. Also out the same day is the ADP employment report, which is often seen as a preview to the official jobs numbers. On Thursday, the only major data will come from the August factory orders before attention turns to the nonfarm payrolls report on Friday. The US economy is forecast to have added 188k jobs in September, somewhat less than the 201k gains seen in the prior month. The jobless rate is expected to inch lower by 0.1 percentage points to 3.8%, signalling a further tightening in the labour market and this will likely be evident in the monthly wage numbers. Average hourly earnings are projected to have risen by 3.0% year-on-year in September, which would mark the fastest rate in nine years.

If the jobs report fails to excite the markets, the dollar could enjoy more action from Fed officials as several FOMC members will take to the podium, including Chairman Powell. Any remarks on the pace of rate increases in 2019, as well as on trade risks, could prove market-moving. In the meantime, trade-related headlines will keep investors on edge, especially if there are any developments in the negotiations with China and Canada.