The coming week will be an unusually quiet one for economic releases but political developments in Britain and Italy will likely provide plenty of volatility for traders. As the UK prime minister, Theresa May, scrambles to save her Brexit deal and the European Commission ponders disciplinary action against Italy, it’s looking like another choppy week for the pound and euro. As for the upcoming data, the focus will be on flash PMIs for the Eurozone, and inflation figures out of Canada and Japan. US housing numbers could also attract attention following the Fed’s Powell citing some concerns this week.

Japan to publish trade and CPI data

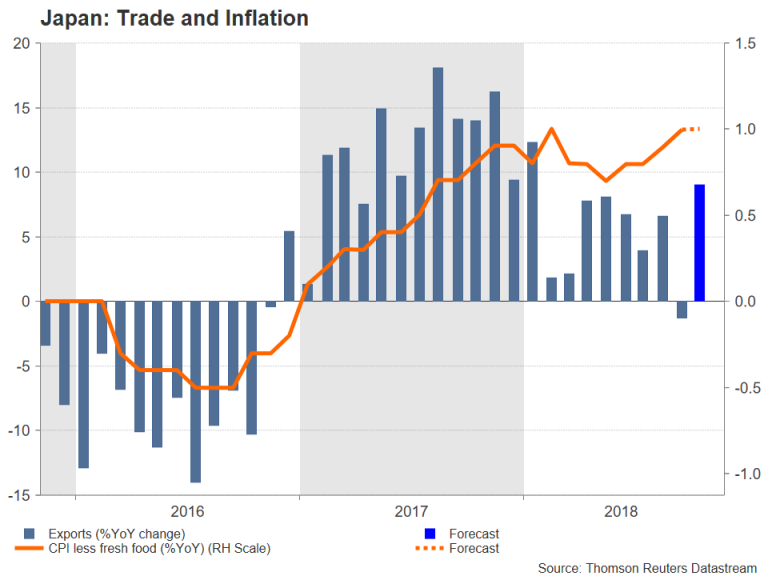

Investors will be looking at the latest trade numbers out of Japan on Monday to gauge how exports performed at the start of the fourth quarter following the past week’s GDP data that revealed the Japanese economy contracted by an annualized rate of 1.2% in the third quarter. Exports fell by 1.8% during the quarter, dragging on growth. They are forecast to have rebounded by 9% year-on-year in October.

On Wednesday, inflation figures will follow and will probably highlight yet again the Bank of Japan’s slow progress in achieving its 2% price target. The core rate of CPI, which excludes fresh food prices and is tracked by the BoJ, is expected to have risen by 1.0% y/y in October, unchanged from the prior month. Also important will be the Nikkei/Markit flash manufacturing PMI for November on Friday.

The yen could firm a little if the above figures are supportive of a stronger Q4. However, any steep appreciation is more likely to be due to risk-off flows than from strong data.

Quiet week for the aussie and kiwi

The Australian and New Zealand dollars are on track for a third week of gains as recent encouraging data and easing trade tensions have bolstered the antipodean currencies despite broader market risk sentiment remaining fragile. However, they could struggle for direction in the coming days in the absence of major releases.

The Reserve Bank of Australia’s minutes of its November 6 policy meeting due on Tuesday could be of some help for the aussie. The central bank is expected to reiterate its upbeat growth forecasts, while remaining cautiously optimistic about a gradual pickup in inflation. Strong employment numbers this week underscored the RBA’s positive outlook.

The kiwi has performed even better than its aussie counterpart, rising to a 3½-month high of $0.6841 on the back of improving economic indicators for New Zealand. The next focus for the kiwi will be third quarter producer prices on Tuesday.

Euro’s weak upside at risk from more poor PMIs

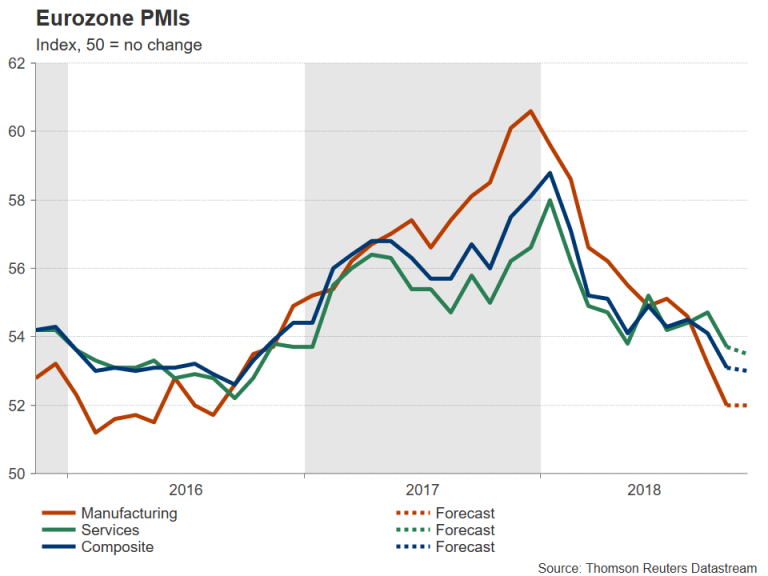

The euro managed to find a floor slightly above the $1.12 level this week, helping it regain posture to recover towards the $1.13 handle. However, this may be just a temporary reprieve for the single currency, which faces the risk of more downside from next week’s flash PMI estimates, due Friday. The euro area’s composite PMI – considered to be an accurate barometer of economic activity – fell to a two-year low in October. It is expected to deteriorate further in November, declining to 53.0 from 53.1 in the preliminary reading. The services PMI is also projected to fall in November, but no change is forecast for the manufacturing PMI.

In other data, Germany’s second GDP print for the third quarter, also out on Friday, is anticipated to confirm that the Eurozone’s largest economy shrank by 0.2% quarter-on-quarter during the period.

With the Eurozone economy continuing to lose momentum throughout 2018, the European Central Bank is nonetheless pressing ahead with winding down its asset purchases by year-end. Analysts will be scrutinizing the minutes of the ECB’s October policy meeting on Thursday for any inclination by policymakers to reconsider their plans given the weaker-than-expected growth performance of the region.

Another potential headache for the ECB is the clash between Italy and the European Commission over Rome’s plans to increase the budget deficit to 2.4% in 2019, well above the previous government’s commitment. The Commission has until November 21 to decide whether Italy’s revised budget submitted this week is in compliance of EU fiscal rules or if it should take the first steps in disciplinary action.

Pound to stay in spotlight regardless of bare UK calendar

Political tensions in Westminster over Brexit are sure to guarantee further gyrations in the pound in forex markets next week even though there will be no significant data releases out of the UK. Indications that Prime Minister May is headed for defeat in a possible no-confidence motion would be strongly negative for sterling, which this week plunged to a two-week low of $1.2722 as several ministers resigned in protest to her Brexit plans.

The Bank of England will likely be the only distraction from Brexit for the British currency next week as the governor, Mark Carney, and other Monetary Policy Committee (MPC) members will testify before the Treasury Select Committee in Parliament on Wednesday. Carney will probably want to steer clear of the Brexit topic but given the recent developments, could sound more cautious about the outlook for the UK economy, which would further weigh on sterling.

Canadian data to be highlight in North America

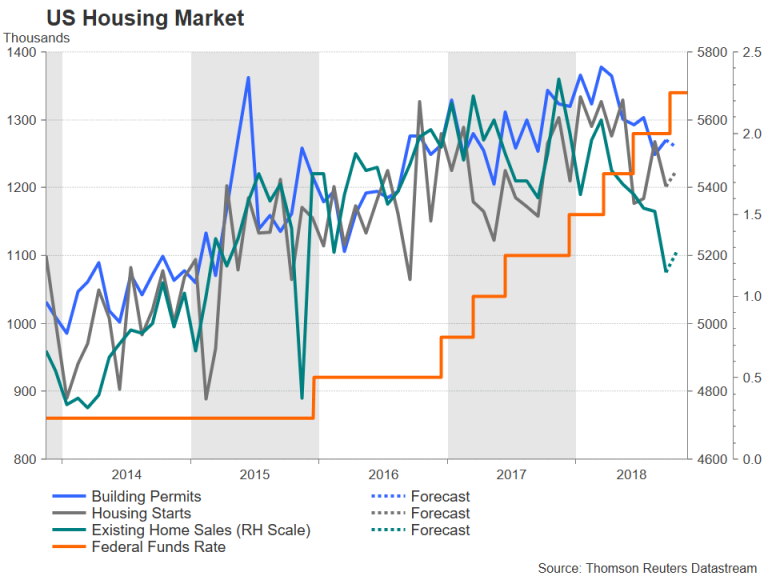

While the US will have the busiest calendar, it’s unlikely to be the main driver for the US dollar, whereas in Canada, domestic data could help the loonie claw back some of its recent losses. Starting with the US, investors’ attention early in the week will be on the housing market, which is showing signs of a downturn as rising borrowing costs make it less affordable for Americans to take out mortgages. The slowdown has captured the attention of the Fed Chairman, Jerome Powell, who this week said he was monitoring the situation. Building permits and housing starts for October are out first on Tuesday, followed by existing home sales on Wednesday. The former is expected to fall marginally, while the latter two are forecast to rise slightly in October from the prior month.

Also due on Wednesday are durable goods orders. They are anticipated to have dropped by 2.5% month-on-month in October. There will be no data on Thursday as the US market will be closed for Thanksgiving, while Friday will be a half-day.

Moving north of the border, traders will be watching the latest inflation and retail sales numbers out of Canada on Friday. Annual inflation moderated to 2.2% in September, but the Bank of Canada maintains that the risks are to the upside given the economy is close to full capacity. An uptick in CPI in October could put the BoC on course to raise rates again early in 2019. Retail sales figures for September will be published alongside the CPI report. A solid set of data could provide the Canadian dollar with a much-needed lift after slipping to 4-month lows this week on the back of the slump in oil prices.

{kind=link}