As the US dollar heads for fresh two-year highs, next week’s nonfarm payrolls report could be key in deciding whether the dollar’s persistent strength will hold out for much longer. The Australian dollar will also be under the spotlight as the country’s central bank could make its first rate cut in three years. The European Central Bank will meet too as the Eurozone struggles to escape the dark clouds hanging over it. In Canada, the latest employment report will be important after the Bank of Canada reiterated its data-dependent stance.

RBA to cut rates as growth expected to slow

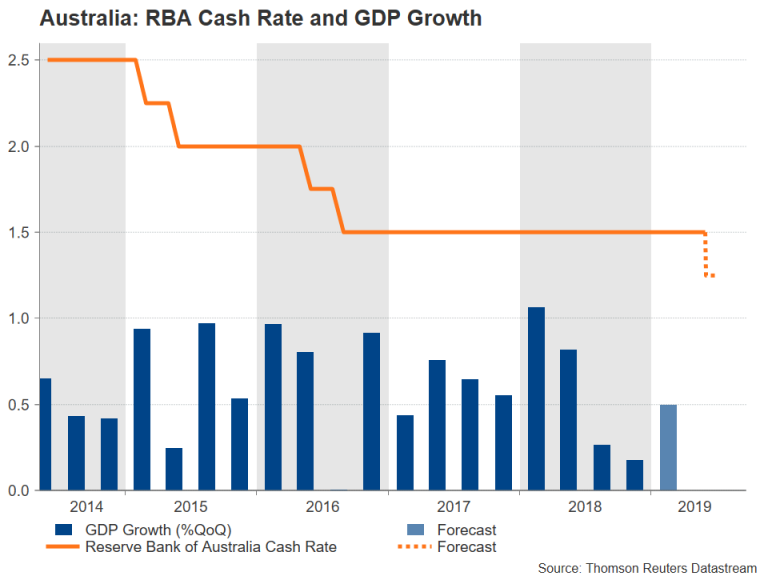

It’s going to be a crucial week for the Australian dollar next week as first quarter growth figures will be published, and the Reserve Bank of Australia could make its first rate reduction in three years. GDP data due on Wednesday is projected to show the Australian economy grew by 0.5% quarter-on-quarter in the first three months of the year. Ahead of the GDP report, there will be plenty of clues on what to expect from it as Q1 business inventories numbers are out on Monday, followed by Q1 net exports contribution on Tuesday.

The barrage of economic stats does not stop there as monthly retail sales, trade and housing finance figures will be released too, on Tuesday, Thursday and Friday, respectively.

But it will probably require a big upside surprise in the data to convince the RBA it does not need to cut rates given that inflation remains stubbornly low and shows no sign of picking up. The RBA is anticipated to lower its cash rate from 1.50% to 1.25% when it meets on Tuesday.

The aussie is therefore likely to face some selling pressure next week, though the extent of the downside will depend on whether the RBA signals further rate cuts in the future. Rising iron ore prices have halted the aussie’s recent slide, and with a rate cut now mostly priced in, only a very dovish RBA or a further escalation in trade tensions risk driving the local dollar to fresh yearly lows.

Disappointing PMIs from China – Australia’s biggest trading partner – is another possible drag on the aussie. The Caixin/Markit manufacturing PMI is due on Monday and is forecast to slip from 50.2 to 50.0 in May, pointing to stagnant growth in manufacturing during the month.

Q1 capital expenditure due from Japan

Japan’s economy may have grown more than expected in the first quarter but that was mostly down to a sharp fall in imports. A more detailed release of quarterly capital expenditure on Tuesday should provide investors with better insight into how business spending fared in specific sectors and whether there is any change to the preliminary reading of -0.3% q/q, which would be an indication of a possible revision to the initial GDP estimates.

Household spending and earnings numbers for April will be watched too on Friday, particularly, the pay growth figures. Earnings in Japan slumped by 1.9% year-on-year in March despite a tight labour market. Further weakness in consumption and wage growth in April would not bode well for Q2 growth.

Nevertheless, the yen looks set to stay supported by safe-haven flows for some time yet so is unlikely to come under much pressure from any worrying data out of Japan.

Can the ECB get more dovish?

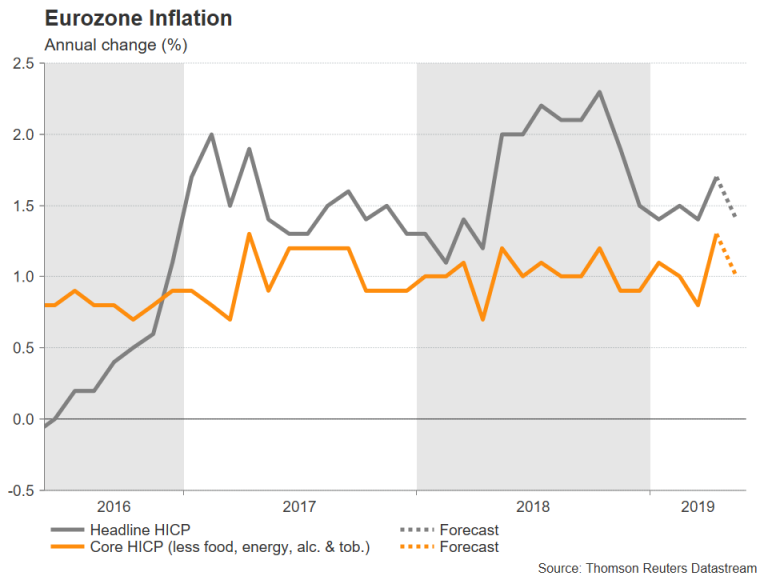

The Eurozone calendar will be quite busy in the coming week with the final IHS Markit PMIs for May out on Monday and Wednesday, the euro area unemployment rate on Tuesday, retail sales and producer prices on Wednesday, as well as revised Q1 GDP figures on Thursday. The highlights in terms of economic releases, however, will be the flash inflation print for May on Tuesday and German industry indicators later in the week. But the main focal point for traders will be the ECB’s policy meeting on Thursday.

Eurozone inflation is expected to ease from 1.7% to 1.3% y/y in May, suggesting it continues to be a tough battle for the ECB to meet its price goal. German industrial orders and output figures for April will be monitored closely on Thursday and Friday, respectively, for signs Europe’s largest economy is on the mend.

ECB President Mario Draghi is sure to comment on the Eurozone economy at his press conference on Thursday, which will follow the ECB’s latest policy announcement. The central bank is expected to keep interest rates unchanged but will probably outline the details of its latest round of Targeted Long-Term Refinance Operations (TLTRO), which will launch in September. Updated economic projections will also be published, so a more dovish sounding ECB cannot be ruled out if growth and inflation forecasts are revised lower.

That would pose downside risks for the euro, which is nearing its 2-year trough plumbed earlier this month.

UK PMIs sole focus for pound as Brexit bill is scrapped

The UK Parliament was due to vote on Theresa May’s fourth version of her Withdrawal Agreement bill next week, but with her resignation comes the demise of her deal. Instead, British politicians will have the pleasure of hosting US President Trump on a state visit, who may have a thing or two to say himself about Brexit whilst he’s there.

But as traders anxiously await who the Conservative party will vote as its next leader, effectively replacing May as prime minister, the latest PMI reports should provide an update on the damage the Brexit drama is doing to the UK economy. The manufacturing PMI for May is up first on Monday, followed by the construction PMI on Tuesday and the services PMI on Wednesday.

The data are unlikely to be of much comfort to the pound even if there are positive surprises, but in the absence of any other news, could provide some near-term direction.

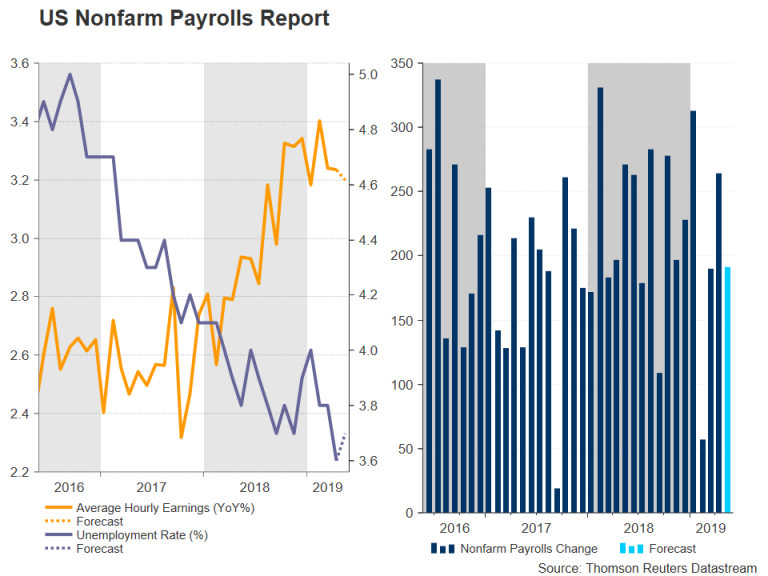

Will NFP report be another catalyst for a strong dollar?

Not even (in what is appearing to be) a complete breakdown in US-China trade talks is able to keep a lid on the greenback’s advances, with the dollar index fast approaching last week’s 2-year highs. And as the US economy so far manages to maintain good momentum, next week’s set of key indicators are not expected to change that picture.

The first big release out of the US is the ISM manufacturing PMI on Monday. The index is forecast to rise from 52.8 to 53.3 in May. The more-important ISM non-manufacturing PMI will follow on Wednesday and is predicted to increase from 55.5 to 56.0. If the numbers come in as expected, they could help 10-year Treasury yields recover from 20-month lows – not that this decline has been much of a deterrent for the dollar bulls.

In other data, April factory orders and the ADP employment report will be watched on Tuesday and Wednesday, respectively, before attention turns to Friday’s nonfarm payrolls report.

The May jobs report is anticipated to be another healthy one for employment growth but lacklustre in terms of wage growth. Total nonfarm payrolls probably slowed somewhat from 263k in April to 190k in May, which is still impressive given that only 100k jobs are needed a month to keep up with population growth and that the economy is in the late stages of the business cycle. The jobless rate is forecast to tick up slightly to 3.7%, but disappointingly, wage growth is forecast to remain unchanged at 3.2% y/y in May.

Without faster wage growth, it will be incredibly difficult for the Fed to lift inflation closer to its 2% target. Investors will be hoping to hear more on the Fed’s stance on inflation and the economy on June 4-5 when a number of Fed regional presidents, as well as Chairman Powell and Vice Chairman Clarida attend the Fed Listens Conference in Chicago.

Jobs numbers eyed in Canada too

The Bank of Canada said it was increasingly confident the slowdown in late 2018/early 2019 was temporary as it kept rates on hold this week. But this wasn’t enough to convince traders that further rate hikes could be on the horizon in the near future, triggering a plunge in the loonie against the US dollar.

Still, the BoC has made it clear it remains very much data dependent. Thus, employment figures for May out on Friday could help the Canadian dollar recoup some of this week’s losses if they are anywhere near as strong as last month’s surge of 106.5k jobs.