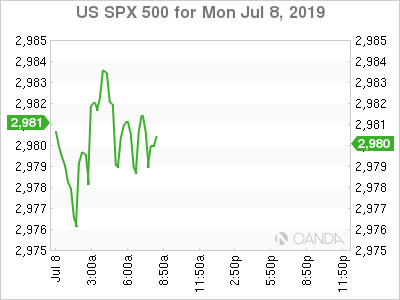

Global equities are quietly softer across the board on softer than expected German data, follow through on Friday’s falling Fed rate cut blues, and a plethora or regional stories that added to the risk-off tone. Deutsche Bank’s mixed review on their radical overhaul, Erdogan’s sacking of his central bank chief, uncertainty on how quickly Iran will raise their nuclear enrichment program, and Morgan Stanley’s downgrade of investment guidance on global stocks are keeping markets in the red.

US stocks markets will likely struggle to rebound until we hear from Fed chair Powell’s testimony to Congress on Wednesday. Markets are still confident the Fed will cut rates at the end of the month, but the strong labor market have many doubting the Fed will signal more rate cuts will come following a small 25 basis point cut at the end of July FOMC meeting.

Financial markets are also waiting for a significant update on the trade front between the Chinese and Americans. If we do not see a meeting setup in Washington DC or Beijing soon, markets will grow nervous that a final deal will get pushed to next year and that uncertainty will derail fourth quarter earnings forecasts. Markets appear convinced the largest four central banks will be pumping up markets, but earnings season could see drastic fourth quarter forecasts downgrades if we don’t have more optimism on the trade front.

Greece

The populist movement is leaving Athens as Greece’s center-right New Democracy party leader Kyriakos Mitsotakis will become prime minister on Monday. The 51-year-old Mitsotakis victory shows markets that Greece is going back to supporting the main stream party. Outgoing Prime Minister Tsipras helped Greece get out of deep austerity measures that crippled the economy in 2015, but now with the economy in recovery mode, Greece is looking for someone deliver more market friendly measures.

Mitsotakis won an outright majority in the snap general election. His business-friendly approach which will likely see him try to reduce taxes and privatize services in the country. He will likely seek to renegotiate budget surplus terms with the EU and that should be the beginning of a new struggle that ultimately should be positive for the Greek economy.

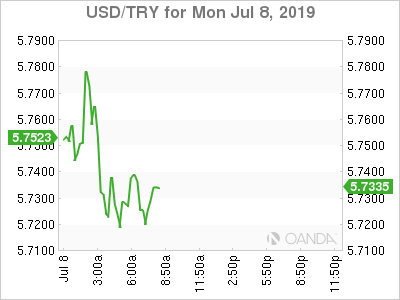

Lira

President Erdogan dismissal of Murat Cetinkaya, the head at the Turkish central bank (CBRT) was due to happen after central bank chief policy decisions disagreed that higher interest rates cause inflation. It is clear that central bank independence does not exist in Turkey and the lira will suffer. The Turkish president wants a low-interest rate policy put in place and the market has already priced in a major cut for its next policy meeting on July 25th. Before the firing the CBRT’s stance was to keep policy steady in the current tightening cycle as inflation continues to remain three times above their target.

Erdogan is under growing pressure after losing the rerun mayoral race in Istanbul. Turkey’s recession is being blamed on Erdogan, who made the push for increased bank lending and public spending, only supporting a temporary relief in the economy. The political stimulus effects have faded, and the falling lira have dealt a strong blow to the Turkish economy.

The lira is off the lows following the sacking, but that could be temporary, as many analysts view rate cuts as not enough to jump start the Turkey’s economy. Skepticism is also very high on the Erdogan’s appointment of Deputy Gov Murat Uysal. Banks that could see their Turkish assets struggle include Unicredit, BBVA, BNP Paribas and HSBC.

Deutsche Bank

Deutsche Bank’s fifth restructuring program in four years will see the departure of the equities and trading business and a drastic reduction in costs which include the 18,000 layoffs by 2022. An overhaul, removal of the equities business, like this has not been attempted before and abandoning the global business to become a German bank only is not getting a strong vote of confidence on Monday.

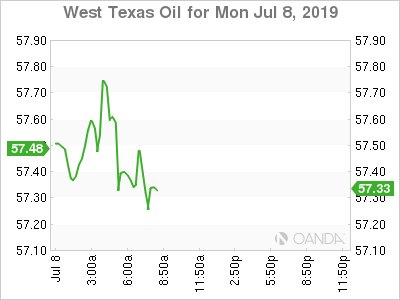

Oil

Crude prices are struggling to stabilize even as Iran signals they will breach the levels of uranium enrichment under the 2015 nuclear accord. While the situation remains tense in the Middle East, crude is not surging as Europe and Iran are communicating and optimism is growing that we could see Europe deliver some relief to Tehran’s economy in exchange for upholding the nuclear accord. Crude is also looking heavy as the global demand picture remains ugly following softer than expected German industrial production data.

The main event for financial markets this week is the Fed’s Powell testimony to Congress this week. Investors who are calling for a massive start to the easing cycle are nervous the blockbuster jobs report could have the Fed possibly wait till September. If Fed fund futures start to price in a growing risk that we will not see a cut this month, the dollar could rally, bring down commodity prices down across the board.

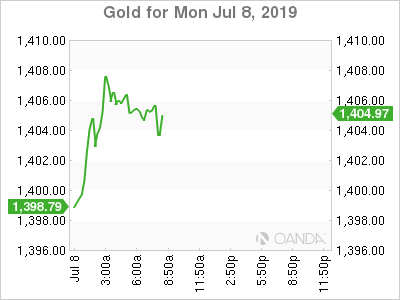

Gold

Gold is rising on softer than expected industrial production data from Germany, growing concern we will see major downgrades with fourth quarter outlooks this upcoming earnings season and nervousness Powell will not be dovish enough this week. With peak summer upon Wall Street, markets are likely to see lower volumes until we get to big events.

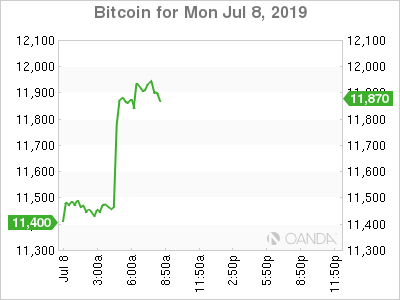

Bitcoin

Bitcoin remains stuck in the $11,000 to $12,000 range as the rally that stemmed from the revival in retail and institutional interest has run its course. Mainstream commerce is a lengthy project that eventually will provide consistent demand for cryptocurrencies, but for now we could see a little exhaustion in the crypto news space.

{kind=link}