It’s going to be an action-packed week, with three major central bank meetings and a storm of economic data likely to keep traders glued to their screens. The European Central Bank is unlikely to signal anything radical, so the euro might be driven mainly by the bloc’s PMI data. The Bank of Japan meeting could also be a snoozer, though there is a case to be made for the Bank of Canada to adopt a more dovish tone. In Britain, the preliminary PMIs may be the deciding factor of whether the Bank of England will cut rates later this month.

ECB sidelined, eyes on PMIs for rate clues instead

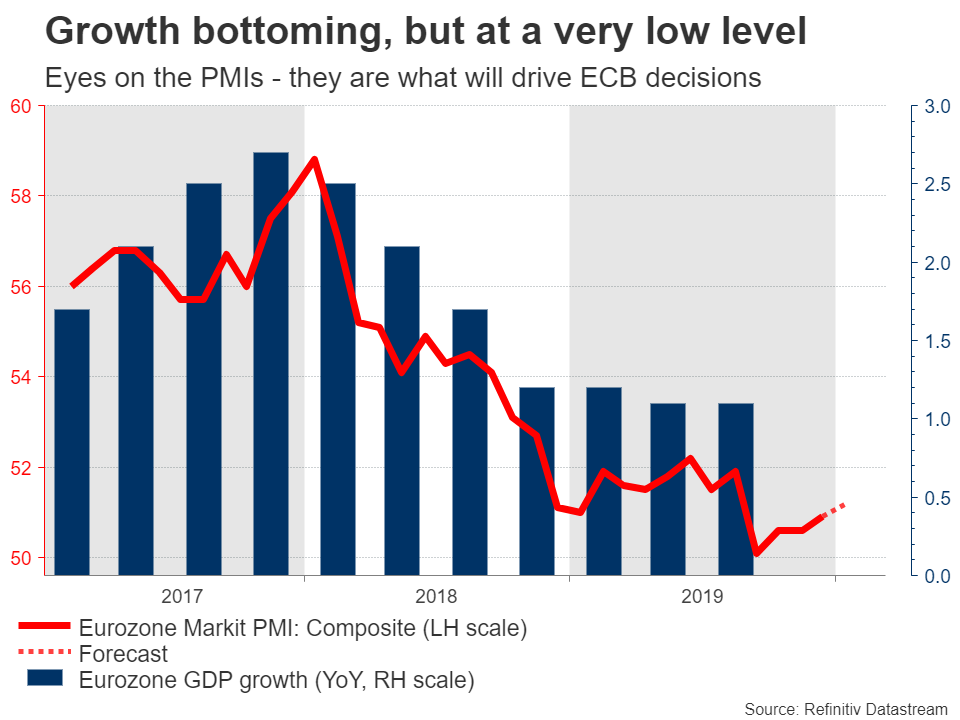

The Eurozone closed 2019 on a more positive note, amid hopes that the uncertainty that almost brought the economy to its knees earlier in the year was finally dissipating. The US-China ceasefire and fading Brexit risks were central to this narrative, as were some early signs from PMI surveys that economic growth was stabilizing after a dramatic slowdown.

Alas, investors seem to be focusing too much on the positives. Growth may be bottoming, but at an alarmingly low level, so there’s not much to celebrate. The manufacturing sector is still contracting, and risks remain to the downside with the threat of US tariffs on European cars looming. And while Brexit worries have taken a back seat, that may not remain the case for very long, as the brinkmanship and drama could resume once the EU-UK negotiations restart.

In this light, the European Central Bank (ECB) is unlikely to either do or say much when it meets on Thursday. If there is any change in tone, it might be towards a less dovish one, given the signs of ‘green shoots’ in the data and deescalating political tensions. Even in this case though, any upside reaction in the euro is unlikely to be large.

Rather, a much bigger force in determining the euro’s broader direction will be the preliminary PMIs for January, which are due on Friday. This is probably the most important data set for the direction of monetary policy. If they reaffirm that the economy is getting its feet under it, that could help establish a floor under the euro – otherwise, any more weakness could reignite concerns about a potential recession.

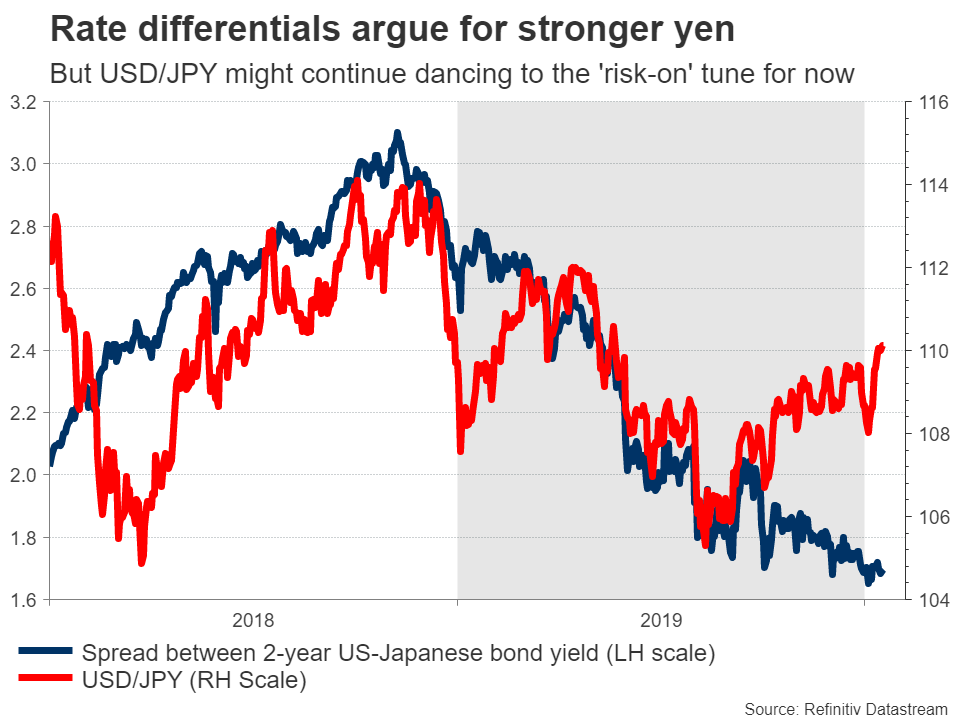

Yen to take its cue from risk appetite, not BoJ

The Bank of Japan (BoJ) will announce its own rate decision early on Tuesday. No action is expected, partly because economic data have improved somewhat – especially on the inflation front – and partly because the government’s recent spending package is expected to stimulate growth, allowing the BoJ to preserve some of its limited firepower for a stormy day.

Of course, this wouldn’t be any surprise and therefore, the yen is unlikely to react much. Indeed, the safe-haven currency hasn’t reacted to BoJ decisions for years now, something likely owed to how loose monetary policy is already. Since there’s very limited scope to ease any further, and since tightening policy is out of the question, BoJ decisions and economic data just don’t have the same impact on the yen.

Instead, the Japanese currency will probably continue to trade mainly as a function of risk appetite, given its defensive status. On that front, the near-term risks around the yen still seem tilted to the downside, as the two biggest threats facing global markets – trade and Brexit – have abated and are unlikely to rekindle in the coming weeks. Further out, though, it might be a different story. Even if trade fears stay dormant, Brexit risks could come back and investors could also turn cautious ahead of the US presidential election, particularly if one of the progressive candidates – Sanders or Warren – secure the Democratic nomination.

Inflation figures for December, alongside the minutes of the BoJ’s December meeting, will be released early on Friday.

BoC may be more interesting – another asymmetric risk for loonie

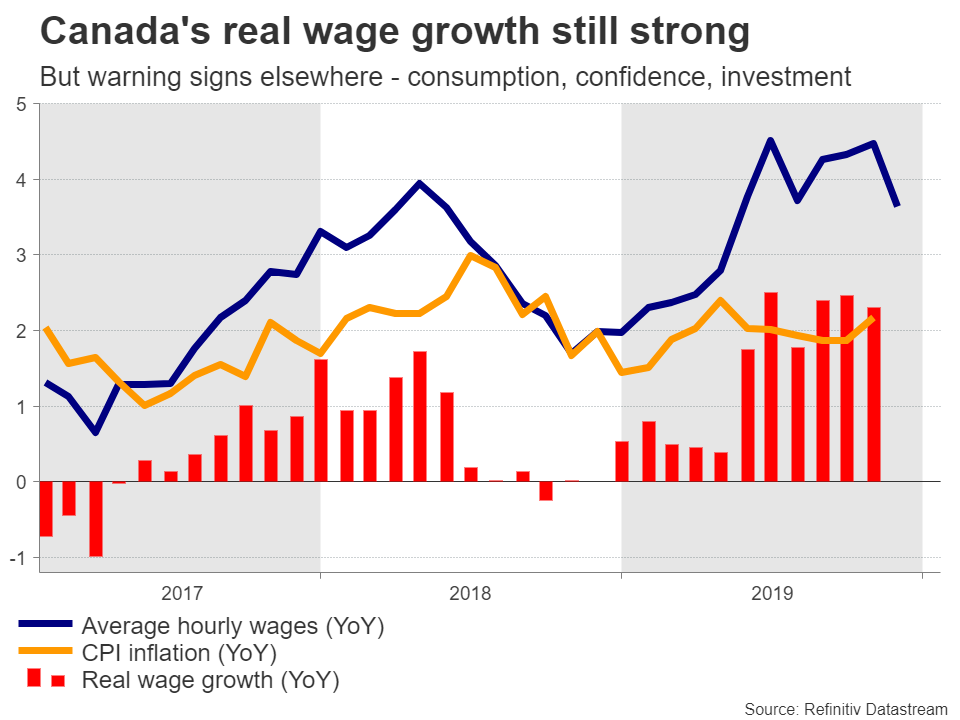

In Canada, the local central bank meets on Wednesday, and although rates are almost certain to be kept unchanged, the signals by policymakers could still generate volatility. Overall, the Canadian economy is still in a good place, with inflation running near the 2% target, wages rising at a healthy clip, the housing market recording solid gains, and external trade risks subsiding.

Yet, there have also been some warning signs lately. Consumption slowed significantly towards the end of 2019, business investment moderated, jobs and wage growth both cooled a little – albeit after a strong run – and consumer confidence fell markedly. Meanwhile, the latest business survey by the BoC itself was mixed despite easing trade frictions, suggesting that this ‘soft spell’ might continue.

Turning to this week’s meeting, while the most probable outcome is the BoC maintaining its neutral stance, that might not produce much market reaction as its already priced in. Markets assign a mere ~30% chance for a rate cut by July, so if the BoC stays neutral, that could lift the loonie – but only a little. On the contrary, should policymakers shift to a more dovish tone and signal they might cut rates if this weakness persists, the loonie could fall notably as the path for monetary policy is repriced.

On the data front, we get the nation’s CPI inflation numbers for December on Wednesday ahead of the policy meeting, while retail sales figures for November will follow on Friday.

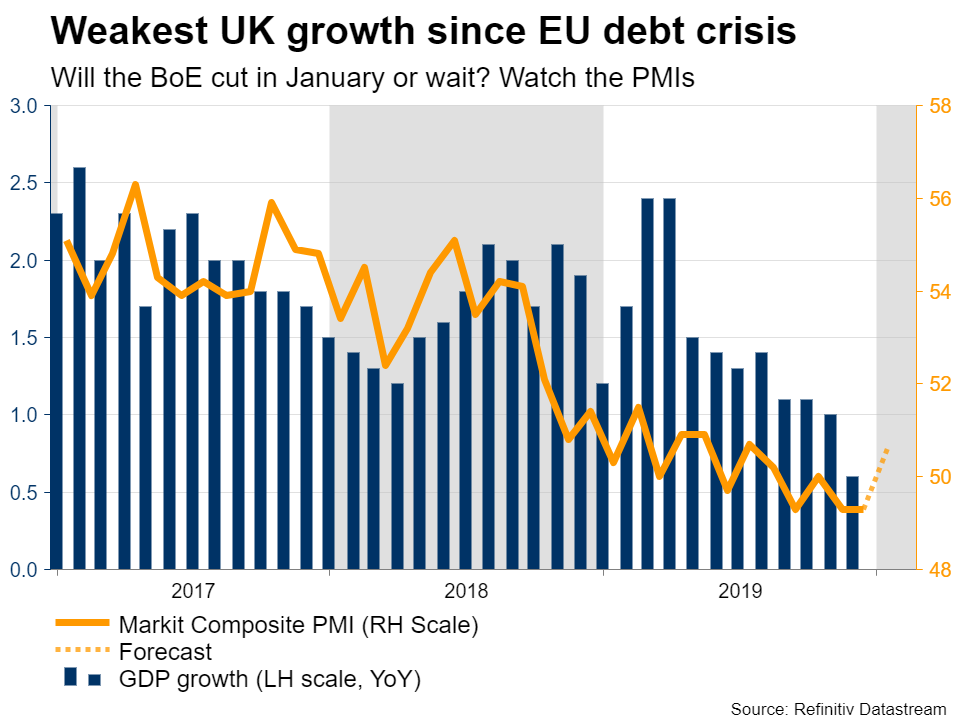

UK PMIs: Will the BoE slash rates in January?

In Britain, with Brexit out of the spotlight for now, market attention has shifted to the Bank of England (BoE) and the prospect of a rate cut. A string of disappointing economic data fueled expectations for cuts, as did some remarks from several BoE officials – including from Governor Carney – that the case for extra stimulus is growing stronger. UK GDP growth clocked in at 0.6% in annual terms in November, which is the weakest since 2012, when concerns around the European debt crisis spilled over into Britain too.

Faced with a slowing data pulse, markets are now pricing in a ~67% probability for an immediate rate cut at the January 30 meeting.

Therefore, the question facing the pound now is how soon a rate cut will come, and that might be decided by the upcoming PMIs. Policymakers seem keen to examine some post-election data before drawing any real conclusions about the outlook, so if the preliminary PMIs for January – that are due on Friday – do not show a convincing enough rebound to calm the BoE’s nerves, then the implied probability for a January cut could shoot higher. That would likely be negative for the pound.

Employment data for November will be released earlier on Tuesday, but may be viewed as somewhat outdated.

Antipodeans look to key data for fuel after trade deal

It’s a busy week in Australia and New Zealand too, with the former releasing employment data for December early on Thursday, and the latter inflation numbers for Q4 during the early Asian session on Friday.

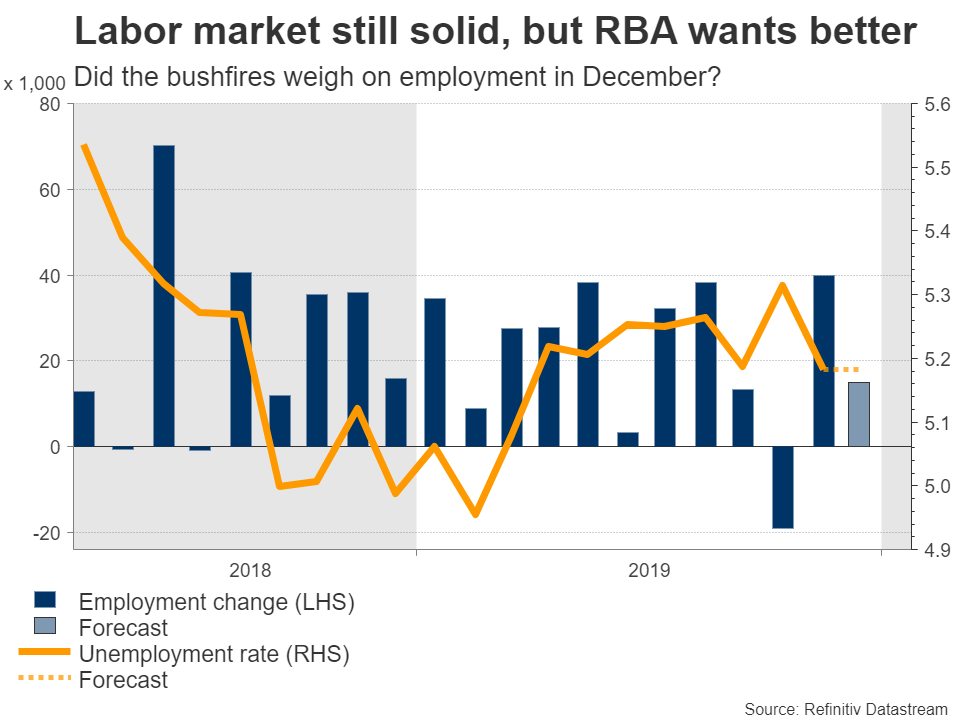

The probability of a rate cut by the Reserve Bank of Australia (RBA) in February dropped to ~42% lately, amid a rally in iron ore prices and cooling trade tensions. Alas, gauges of the labor market – such as the ANZ job ads tracker – suggest that the bushfires weighed on employment in December, which if confirmed by the upcoming data could see rate-cut chances rise again and by extension, hurt the aussie a little.

A similar story is true in New Zealand, where markets are pricing in less than a 40% chance for a cut this year. The CPI numbers for Q4 could reaffirm this narrative, as trackers of inflationary pressures (ANZ monthly inflation gauge) point to another solid quarter. Considering that the Q4 2018 print – which will now drop out of the yearly calculation – was very soft, this means that the annual CPI rate is likely to rise now. If so, that might add some fuel to the kiwi’s recovery.

In Switzerland, world leaders and leading central bankers will gather for the annual World Economic Forum. High-profile attendees include US President Trump, Treasury Secretary Mnuchin, and ECB President Lagarde. Markets will be on high alert for any relevant comments, especially from the erratic US commander in chief.

Finally, in America, the preliminary Markit PMIs for January are coming out on Friday, but markets typically pay more attention to the ISM numbers.

{kind=link}