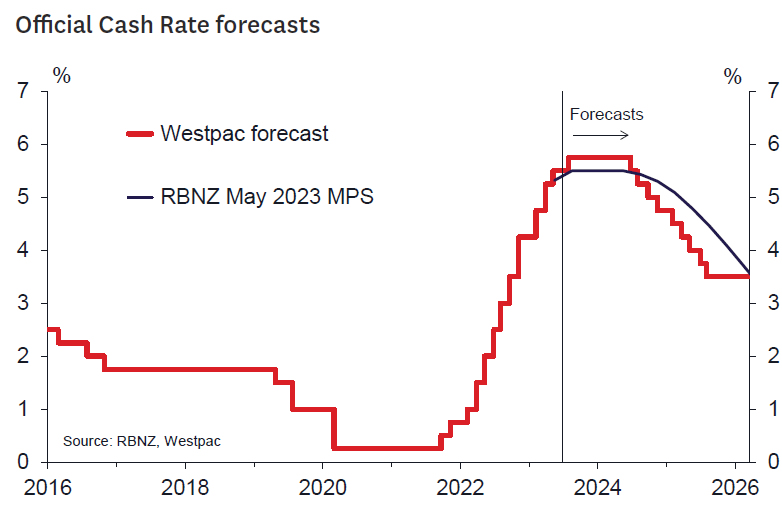

- As expected, the OCR remains at 5.5 %.

- The RBNZ displayed confidence and comfort with the level of the OCR.

- The RBNZ sees the balance of risks around its inflation forecasts as balanced.

- There was little in the RBNZ commentary for the hawks or the doves.

- Westpac still sees a 5.75 % OCR in August

The Reserve Bank left the Official Cash Rate unchanged at 5.5 % as universally expected by market analysts and as largely priced by financial markets.

The tone of the accompanying statement and MPC minutes displayed confidence and comfort with the level of the OCR. There were no indications of a change in view from that presented in the May Monetary Policy Statement where the RBNZ indicated that the OCR would remain on hold until the second half of 2024.

The RBNZ appears more confident in its forecasts, noting that “monetary conditions are constraining domestic spending as expected” and that the risks around the inflation outlook were evenly balanced. There appears to be some upgrade in the RBNZ’s view on house prices which are now seen as “more balanced” compared to their previous forecasts of some further small fall in prices. On the other hand, the RBNZ acknowledges the growth outlook in China has weakened and that March quarter GDP was a bit weaker than forecast. It seems that the net of these factors has left their view unchanged and hence the stance of policy is seen as appropriate. Migration trends are assessed to have evolved as expected and are supporting the housing market, although interest rates are seen to be managing risks of a significant increase in prices.

There is little here for either the hawks or the doves. The kiwis are comfortably resting in the nest. The commentary was short, indicating a less controversial discussion at the MPC, and indeed there was a consensus for unchanged rates this time around. Keeping the commentary short probably also reflected a desire to not say anything that might disturb expectations, as we had indicated would be likely in our MPR preview.

Westpac remains of the view that the OCR will be increased by 25 basis points to 5.75 % at the August Monetary Policy Statement. As we noted in our MPR preview, there wasn’t enough data since the May Statement to significantly shift the RBNZ’s strong view for a protracted period of unchanged rates. However, the month ahead will see some key information in the form of the June quarter Consumers Price Index and Labour market report that should tell us more on the persistence of core inflation pressures and the strength of the labour market, and hence prospects for falling GDP through the second half of this year. Partial indicators suggest the labour market has not cracked yet. This raises the potential that the RBNZ will need to upgrade their growth forecasts for this year closer to those of our own, which will add some upside risks to the inflation outlook and would lengthen the already protracted period over which inflation will take to return to the target range. The kiwi may need to get a waddle on yet although the hurdle to get it moving is pretty high!

{kind=link}