The Bank of England’s monetary policy meeting looks set to be the main highlight of the coming week amid a sudden reversal of rate hike expectations. The Reserve Bank of New Zealand will also be holding a policy meeting. Eurozone data will be sparse but US inflation indicators, Chinese trade figures, Australian retail sales and Canadian employment numbers should keep traders busy.

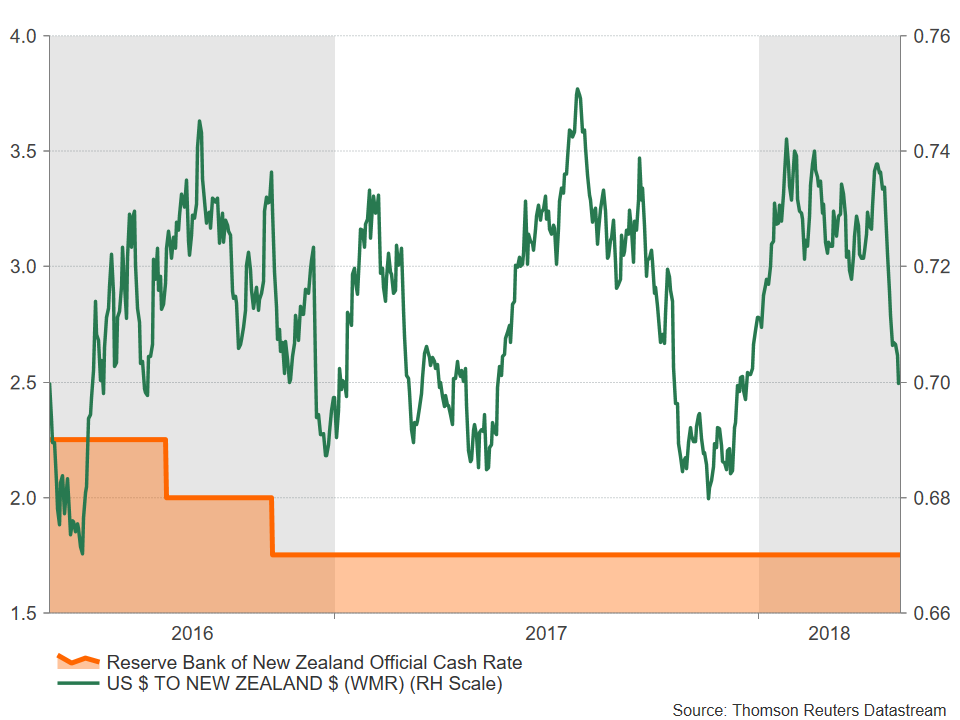

RBNZ to stand pat

The new governor of the RBNZ, Adrian Orr, will hold his first monetary policy meeting on Thursday under the Bank’s new mandate, which now includes employment in addition to inflation targeting. While the policy statement and subsequent press conference may attract more attention than usual, Orr has already signalled that the revised mandate will not lead to a significant change in monetary policy. The RBNZ is widely expected to keep its overnight cash rate unchanged at 1.75% and will likely maintain a neutral stance.

However, with inflation currently running just above the lower band of the Bank’s 1-3% target range, the RBNZ could lower its forecasts in its latest quarterly outlook report. The New Zealand dollar, which slumped to four-month lows versus the US dollar this week, could extend its losses on any sign of a delay to how soon the Bank expects to raise rates.

The Australian dollar also fell to multi-month lows this week before rebounding on better-than-expected trade data. Retail sales figures due on Tuesday could help the aussie extend its gains if there are more positive surprises. Also to watch out of Australia next week are business and consumer confidence gauges by the NAB and Westpac on Monday and Wednesday respectively, as well as housing finance numbers on Friday.

Canadian jobs report eyed

The Canadian dollar has been forming a ceiling at C$1.29 to the greenback over the past week or so, resisting any further advances by its US counterpart. Better-than-expected monthly GDP growth was one of the factors providing the loonie with support. If Friday’s employment report shows another solid set of numbers, the loonie could find fresh impetus to strengthen to below the C$1.28 level. It would also reignite expectations that the Bank of Canada could raise rates at its May or July meetings, especially after Governor Stephen Poloz appeared to be striking a more hawkish tone in recent remarks.

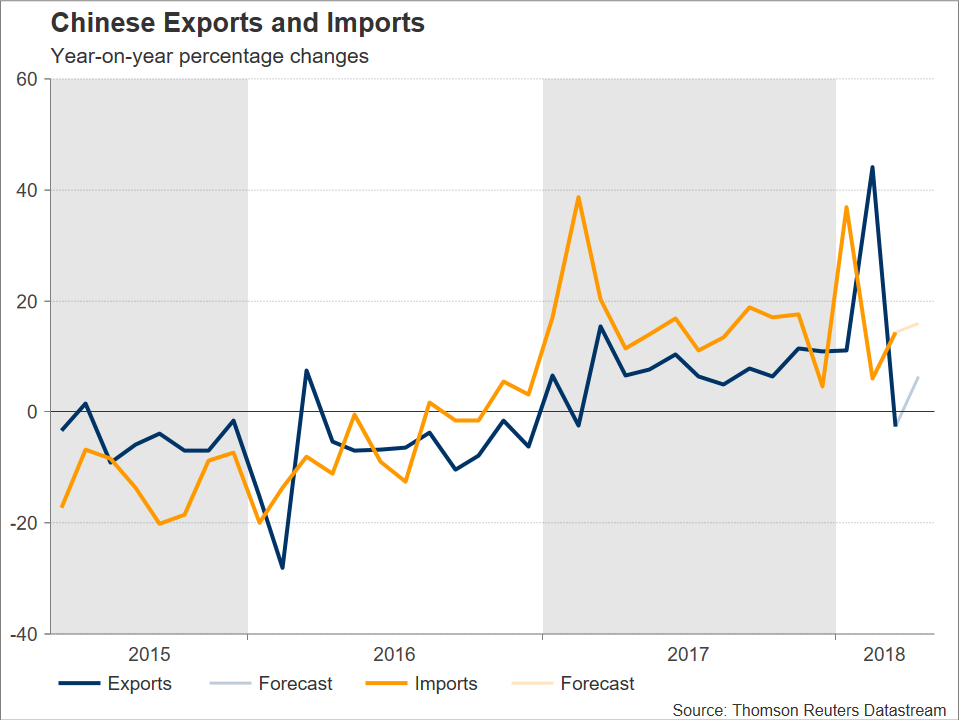

Trade and inflation in focus in China

China will release trade and inflation figures next week, with the April trade data first up on Tuesday. Exports from China posted their first annual decline in 13 months in March. With Sino-US trade tensions still simmering, investors will be hoping for a strong rebound in April – analysts project a rise of 6.3% y/y – to ease concerns that the uncertainty about the trade outlook has already started to impact exports by the world’s second largest economy. On Thursday, CPI and PPI data will be watched as further easing in inflationary pressures in April could raise some doubt about the strength of domestic demand in China.

Bank of Japan to publish minutes and summary

The minutes of the BoJ’s March policy meeting are due to be published on Monday. However, these are likely to be overshadowed by the summary of opinions of the Bank’s more recent meeting in April. The summary of opinions out on Thursday will be scrutinized by analysts to learn the views of the BoJ’s two new deputy governors, particularly that of Masazumi Wakatabe, who is known to be a dove. Wakatabe disappointed some by not dissenting at the April meeting in calling for further loosening of monetary policy. However, should the summary reveal some more dovish voices, the yen could come under pressure on the expectation that further easing in the future is more likely under the new board composition if the BoJ continues to miss its 2% inflation target. In terms of data, household spending on Tuesday will be the main release out of Japan.

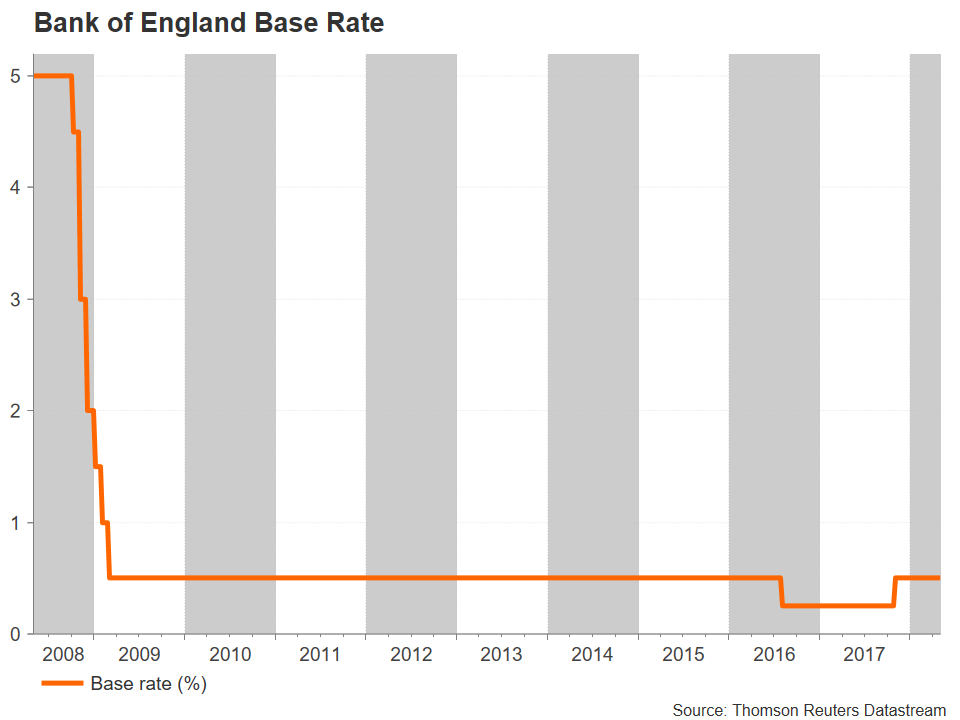

BoE: Will they or won’t they?

Monetary Policy Committee (MPC) members of the Bank of England will have a tricky task at their two-day meeting on May 9-10 as they try to balance the downside risks presently facing the economy with projections that inflation will struggle to fall to the 2% target in two years’ time. Having deliberately raised market expectations that a May rate hike was forthcoming, MPC members will now have to decide whether to keep to their word or postpone the move to until later in the year, as hinted recently by the Governor, Mark Carney.

The pound has retreated by 6% from its 22-month high of $1.4376 set in April as a series of weak economic data and a faster-than-projected fall in inflation have cast doubt about the need to raise interest rates so soon. Market expectations of a May rate hike have receded dramatically, from more than 90% a month ago to below 10% currently. However, the possibility of a 25-basis point increase in the Bank rate next Thursday shouldn’t be totally dismissed as the BoE could raise in May, arguing that it is looking ahead to future inflation expectations, and pause after that. Some analysts agree with this view, with sterling anticipated to reverse sharply higher in the event the BoE delivers a shock hike.

The final possible clue to the Bank’s decision will arrive just hours before the announcement with the release of trade, industrial and manufacturing output figures for March. Positive month-on-month growth is forecast for both industrial and manufacturing production in March.

Germany and France will also publish industrial output data next week, on Tuesday and Wednesday respectively. But otherwise, the euro area calendar will be unusually light, with the Sentix index due on Monday being the only major Eurozone release.

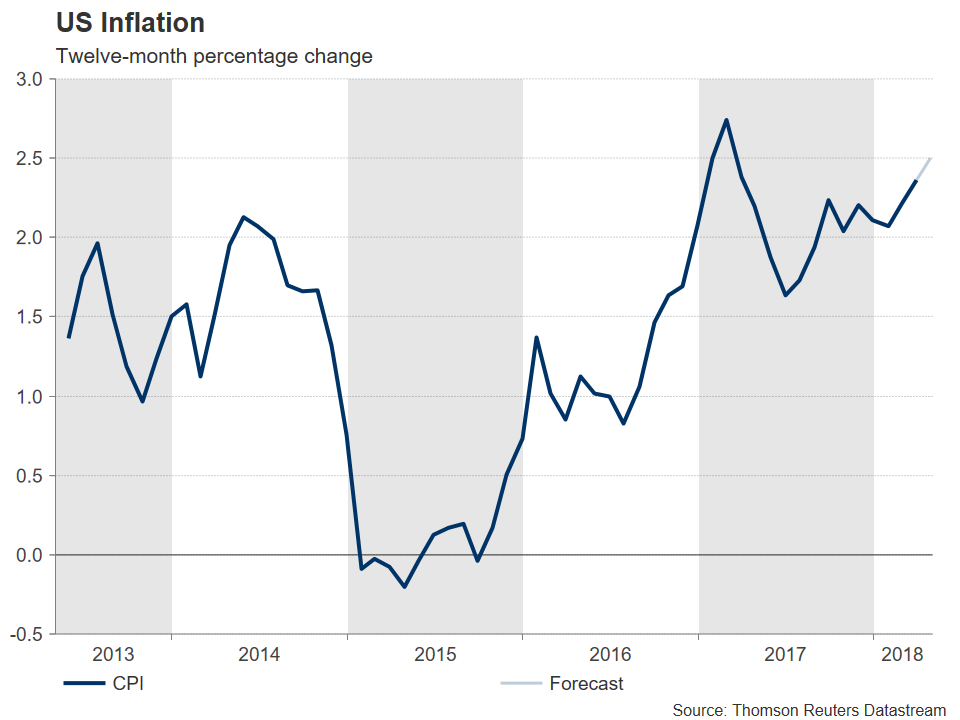

After Fed, US inflation back in spotlight

The Federal Reserve may have eased concerns of a faster pace of rate increases at this week’s FOMC meeting but US inflation data due in the coming days could keep expectations of a fourth rate hike during 2018 alive. Producer price figures out on Wednesday will likely show factory prices easing somewhat in April. However, the consumer price index is forecast to edge up further on Thursday. The annual rate of CPI is expected to rise from 2.4% to 2.5% in April, which would be the highest since February 2017. A stronger-than-expected reading could help the dollar re-challenge the 110-yen barrier after flirting with the level this week.

In other data, April import and export prices should be watched on Friday, along with the University of Michigan’s consumer sentiment index. The preliminary reading of the consumer sentiment index for May is forecast to rise to 99.5 from 98.8 in April.