GBP/AUD extended its medium-term downtrend this week, briefly breaking below the 1.86 handle and falling to its lowest level since late 2023 as markets increasingly favored the Australian Dollar’s strong growth and yield profile over Sterling’s mounting political and policy uncertainty.

On the Australian side, the story remains overwhelmingly supportive.

The Australian Dollar continues benefiting from one of the strongest macro combinations in global currency markets right now: resilient global risk appetite, elevated yield expectations, and continued AI-driven equity optimism. Global stock markets have remained remarkably strong this week, with NASDAQ, Nikkei, and KOSPI all extending toward fresh highs as investors continue pouring into technology and semiconductor-linked assets. As one of the world’s highest-beta major currencies, AUD tends to outperform strongly during periods of broad “risk-on” sentiment.

Yield expectations are providing additional support. Even after three rate hikes already this year, markets are aligning with the RBA’s own projections that the cash rate could climb toward 4.70% by year-end as policymakers continue confronting sticky inflation pressures tied partly to higher energy costs. That hawkish outlook continues widening the policy contrast against other major central banks where uncertainty and caution are becoming more dominant.

Sterling, by contrast, is increasingly trading under a cloud of uncertainty.

Sterling, meanwhile, is weighed down by a growing “uncertainty discount.” Although recent UK economic data has shown some resilience — including stronger-than-expected GDP growth — investors remain increasingly uneasy about both the political outlook and the Bank of England’s policy direction. The BoE’s April decision to hold rates at 3.75% with a heavily split 8–1 vote reinforced the perception that policymakers are trapped between persistent inflation risks and concern about damaging a fragile recovery.

Politics has become the larger problem. Following Labour’s disastrous May 7 local election results, where the party reportedly lost more than 1,300 council seats and control of 35 councils, pressure on Prime Minister Keir Starmer has intensified sharply. Reports of possible leadership challenges later this year have added a growing political risk premium into Sterling pricing as investors worry Britain may face prolonged policy instability just as markets are already becoming more sensitive to fiscal credibility and gilt market volatility.

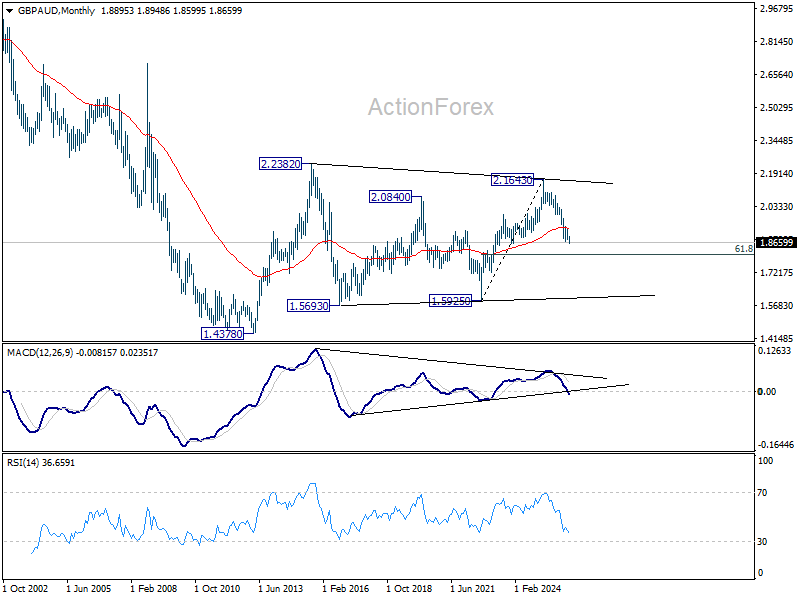

Technically, the break below 1.8690 confirms resumption of the medium term downtrend from 2.1643 (2025 high). Further decline is now expected toward 61.8% projection of 2.0286 to 1.8690 from 1.9399 at 1.8411. Near-term outlook will remain bearish while 1.8954 resistance holds, in case of recovery.

In the long term picture, the break of 55 W EMA (now at 1.9298) suggests that fall from 2.1643 (2025 high) is reversing whole rise from 1.5925 (2022 low). This decline is also viewed as another falling leg inside the sideway pattern from 2.2382 (2015 high). Sustained break of 61.8% retracement of 1.5925 to 2.1643 at 1.8109 will pave the way towards 1.5925.

{kind=link}