Sample Category Title

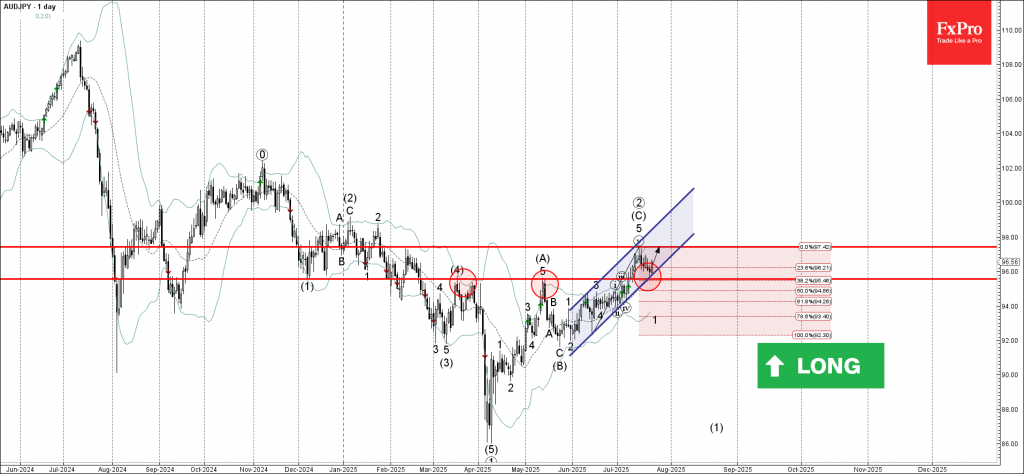

AUDJPY Wave Analysis

AUDJPY: ⬆️ Buy

- AUDJPY reversed from support zone

- Likely to rise to resistance level 97.40

AUDJPY currency pair recently reversed up from the support zone located between the pivotal support level 95.55 (former monthly high from March and May), 20-day moving average and support trendline of the daily up channel from May.

This support zone was further strengthened by the 38.2% Fibonacci correction of the upward impulse from June.

AUDJPY currency pair can be expected to rise to the next resistance level 97.40, former monthly high from February, which also stopped the earlier impulse wave earlier this month.

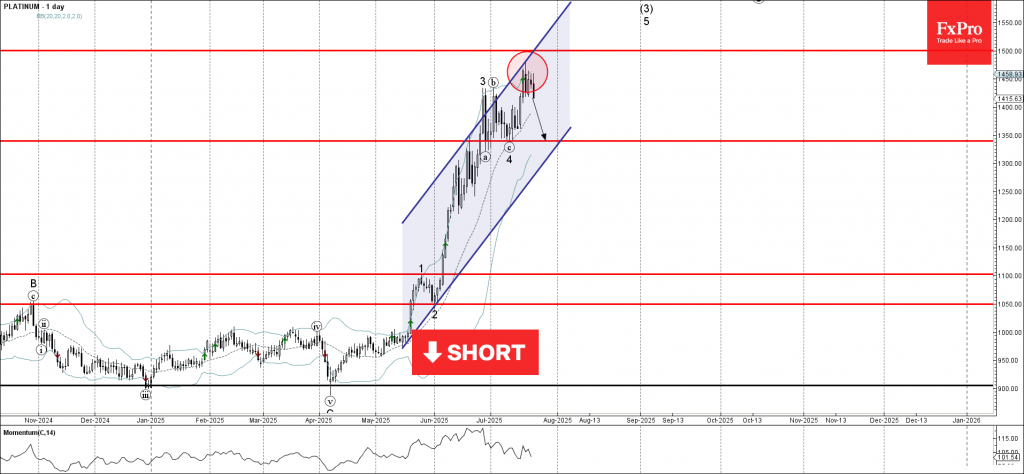

Platinum Wave Analysis

Platinum: ⬇️ Sell

- Platinum reversed from resistance zone

- Likely to fall to support level 1350.00

Platinum recently reversed down from the resistance zone located between the round resistance level 1500.00, upper daily Bollinger Band and the resistance trendline of the daily up channel from May.

The downward reversal from this resistance created the daily Japanese candlesticks reversal pattern Bearish Engulfing.

Given the weakening daily Momentum (showing bearish divergence), Platinum can be expected to fall to the next support level 1350.00 (low of the previous correction 4).

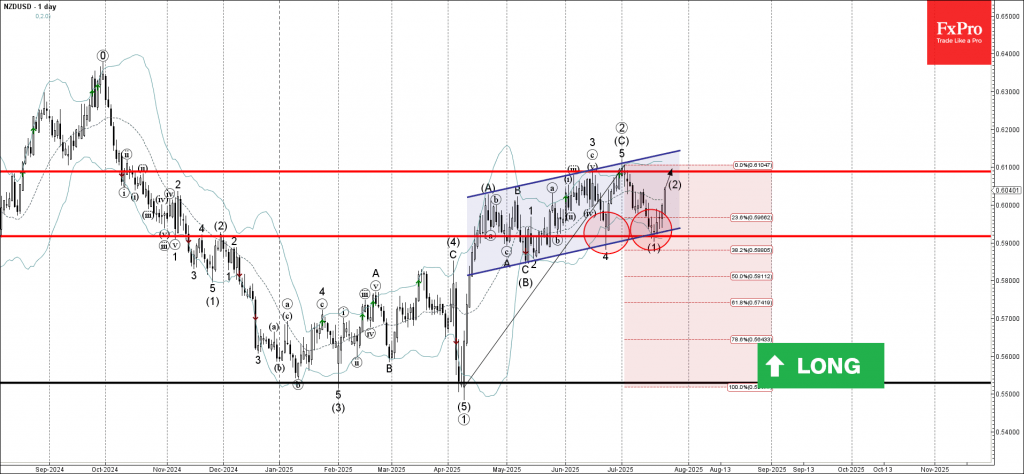

NZDUSD Wave Analysis

NZDUSD: ⬆️ Buy

- NZDUSD reversed from support zone

- Likely to rise to resistance level 0.6100

NZDUSD recently reversed up from the support zone located between the key support level 0.5920 (which stopped wave 4in the middle of June), lower daily Bollinger Band and the support trendline of the daily up channel from April.

The upward reversal from this support zone started the active intermediate correction (2).

Given the clear daily uptrend, NZDUSD can be expected to rise to the next resistance level 0.6100, target price for the completion of the active correction (2) (which has been reversing the price from June).

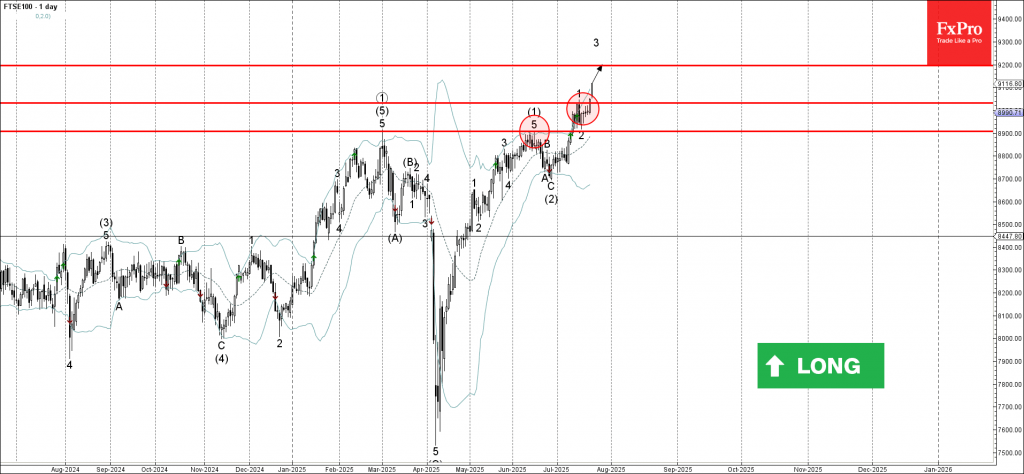

FTSE 100 Wave Analysis

FTSE 100: ⬆️ Buy

- FTSE 100 broke resistance level 9030.00

- Likely to rise to resistance level 9200.00

FTSE 100 Index recently broke above the resistance level 9030.00, which stopped the previous minor impulse wave 1 at the start of July.

The breakout of the resistance level 9030.00 continues the active minor impulse wave 3 – which belongs to the intermediate impulse wave (3) from the end of July.

Given the clear daily uptrend, FTSE 100 Index can be expected to rise to the next resistance level 9200.00 (target price for the completion of the active impulse wave 3).

Gold Retraces Slightly But Holds Near Historic Levels

The precious metal has seen a major bounce in the past two days but is currently seeing some heavy selling after the US-Japan Tariff Deals have been reached.

In prior sessions, Gold was profiting from the selloff in the US Dollar but the dynamics have changed today as sentiment on global trade outlook is turning more positive.

Silver, Copper and Palladium are still moving upwards but Platinum and Gold are struggling today.

Let's take a look at multiple timeframes to spot the zones of interest to gain your edge.

Gold multi-timeframe Technical Analysis

Daily Chart

Gold Daily Chart, July 23 2025 – Source: TradingView

Since our preceding analysis, the precious metal had formed multiple small scale bounces on the 2025 upwards trendline and thsi led to Monday's impulsive move up.

On the bigger picture however, the price action is mostly rangebound as prices have failed to breach the Key resistances that would at least point towards another visit to its all-time highs ($3,500)

One thing that can't be said however, is that the price action is looking weak – bounces are usually strong and bulls are in control as long as prices hold above the 3,350 Pivot Zone.

Levels of interest for trading:

Support Levels:

- $3,350 to $3,375 Pivot Zone

- 50-Day MA $3,335

- $3,300 to $3,330 Major Support

- $3,000 Longer-run Psychological Support

Resistance Levels:

- $3,439 Daily highs

- Immediate Resistance Zone 3,410 to 3,440

- $3,500 all-time highs

Potential Resistance Zones in the case of an upside breakout, from Fib Extensions:

- Potential Resistance 1 between $3,640 to $3,705

- Potential Resistance 2 around $3,800

Gold 4H Chart

Gold 4H Chart, July 23 2025 – Source: TradingView

Looking closeer, we see how the deal led to the ongoing strong 4H Bear candle after marking daily highs at 3,439, bringing back 4H RSI momentum to neutral

The move from the past few days has been strong but before prices actually breakout, the range is still confirmed.

With prices holding above the Current Pivot Zone, the ball is still in the buyers' hand, with the 4H 50-period MA (currently at 3,363) being a key barometer for the intermediate trend.

If bears fail to close the session around or below the Pivot Zone, bulls will stay in control.

30m Chart

Gold 30m Chart, July 23 2025 – Source: TradingView

Looking closer to the 30-minute chart, the selloff that had started in the past 2 hours is finding some support at the upward intraday trendline formed after the last swing low.

Prices are contained between the 2 key 30m MAs, with the 50 acting as resistance ($3,423) and the 200 acting as immediate support (3,378) – Spot for the breaching of any of these two for relative measurement of bull and bear strength

Safe Trades!

Pump-Fake from US Dollar

One of the themes that had driven markets since the beginning of the month was the US Dollar recovering some strength which marked some tops and bottoms for many Currency pairs.

Starting the 1st of July and amplified by a streak of positive data, the Greenback saw its heavy-selling positioning reverse largely.

Particularly after the NFP report and the July CPI, most flows surrounded a re-shifting of funds back towards the US which notably propelled the Nasdaq and S&P 500 through multiple all-time highs.

This USD strength seems to have been just a temporary retracement however, with the Dollar Index having sold off close to two handles from its Thursday swing high (98.50 highs, currently around 97.20) – That move had much more influence in Forex than stocks.

As a matter of fact, the Dow Jones is flying and trying to catch up to its peers. The industrial-focused index just breached the 45,000 Key landmark and is coming closer to its all-time highs. You can take a look at an in-depth analysis of the Index right here:

Since the last mid-week report, there hasn't been much in terms economic data for either the US or Canada except for a strong beat in US Retail Sales last Thursday (0.6% vs 0.1% expected) which further boosted the run in Equities but did not prevent the profit taking that happened on last Friday.

Although, the week is far from over and between PMI releases and key earnings, Markets should still await some volatility.

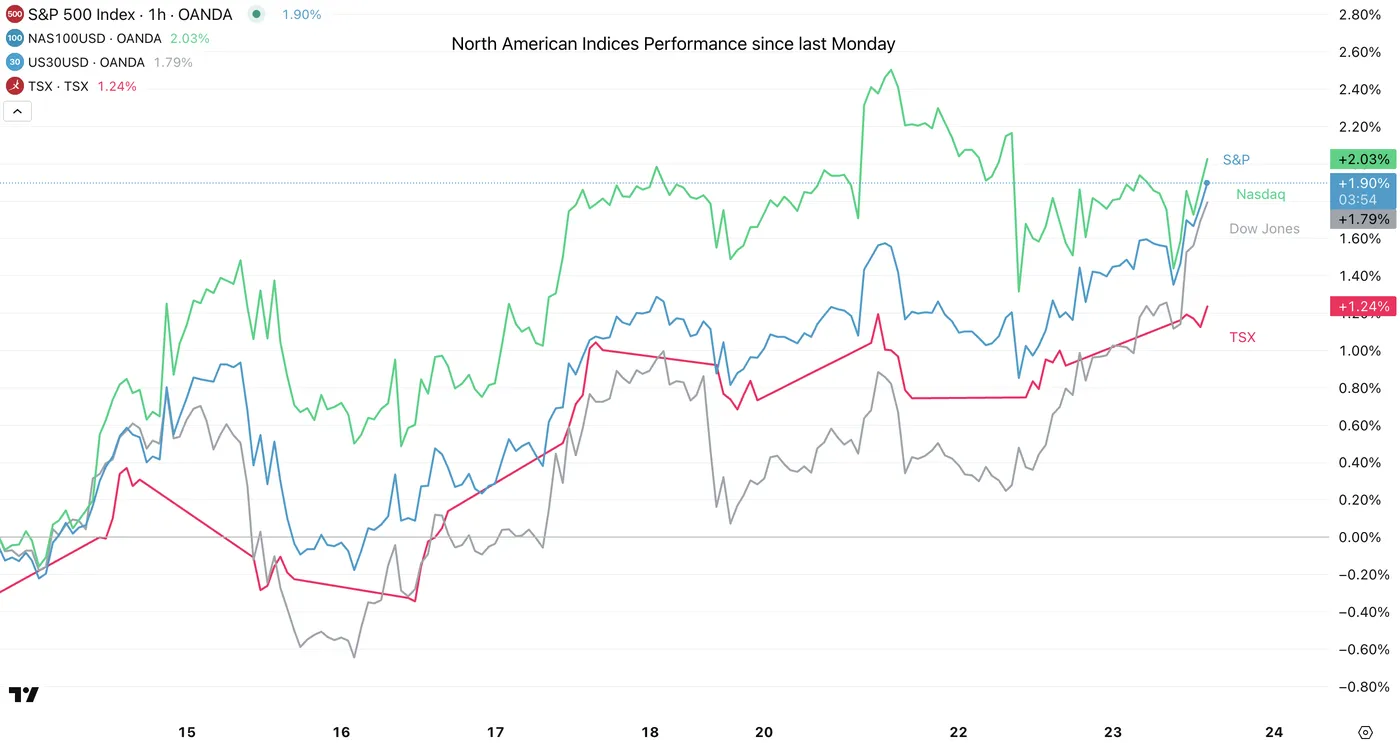

North-American Indices Performance

North American Top Indices performance since last Monday, July 23, 2025 – Source: TradingView

The S&P 500 is taking the crown since last Monday, with some choppy retracements but strong bullish moves.

On the current rewiring however, the Dow Jones is catching up with its peers relatively fast – Something to keep in check for the upcoming weeks.

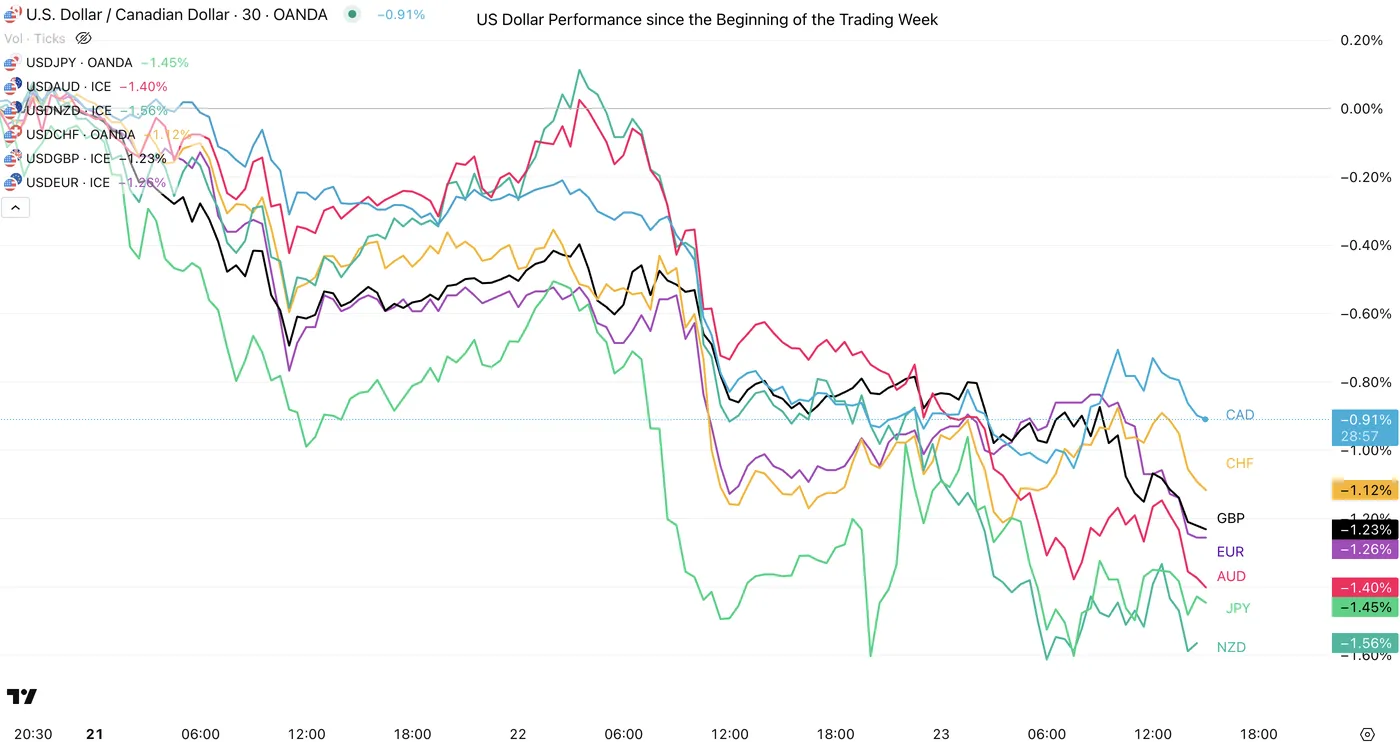

US Dollar Mid-Week Performance vs Majors

USD vs other Majors, July 23, 2025 - Source: TradingView.

There hasn't been much pity for the Greenback as it gave up most of its gains, back towards July 10th levels.

The USD is down between 0.95% to 1.60% against all of its major counterparts.

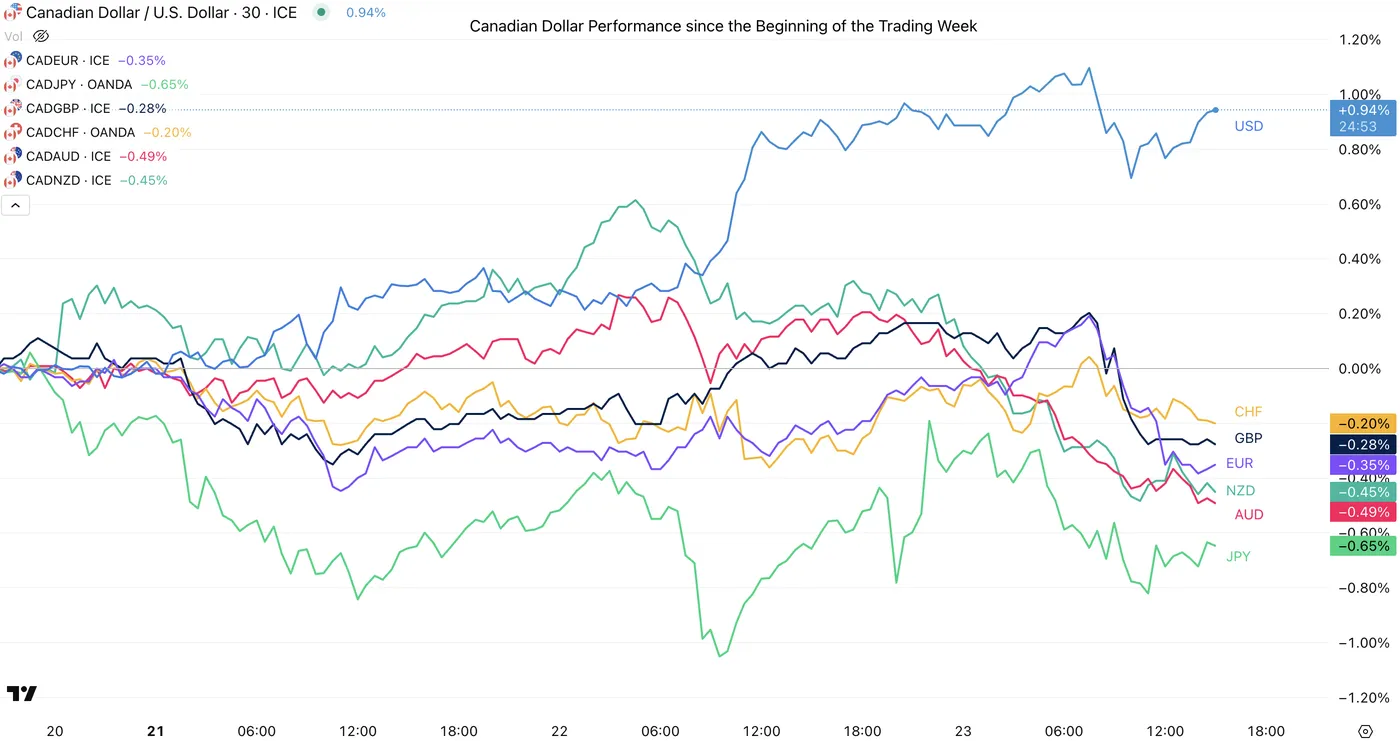

Canadian Dollar Mid-Week Performance vs Majors

CAD vs other Majors, July 23, 2025 - Source: TradingView.

Its been many weeks now that the Canadian Dollar hasn't seen much independent movement from the US Dollar.

It seems that the ongoing bigger picture in Forex is flows that are moving from Europe to Asia-Pacific Currencies in tandem and dragging both NA Currencies at the same time.

It was almost the contrary last week.

The performance from the Loonie is definitely not as bad as the one from the US Dollar.

Intraday Technical Levels for the USD/CAD

USDCAD 2H Chart, July 16, 2025 – Source: TradingView

Almost nothing has changed since our last analysis of the pair and the action is still rangebound.

The ongoing USD selloff is pretty strong, but odds are not for a breakout as markets tend to consolidate towards incoming key Data (tomorrow will see the release of the US PMIs, more details further in the article)

Support Levels:

- Higher Timeframe Key support Zone 1.3560 to 1.36

- 1.3540 (2025 Lows)

- 1.35 Psychological level

- 1.3450 October 2024 lows

Resistance Levels:

- Pivot zone 1.3675 to 1.3686

- 1.3740 Pivot turned Resistance

- 1.38 Main Resistance

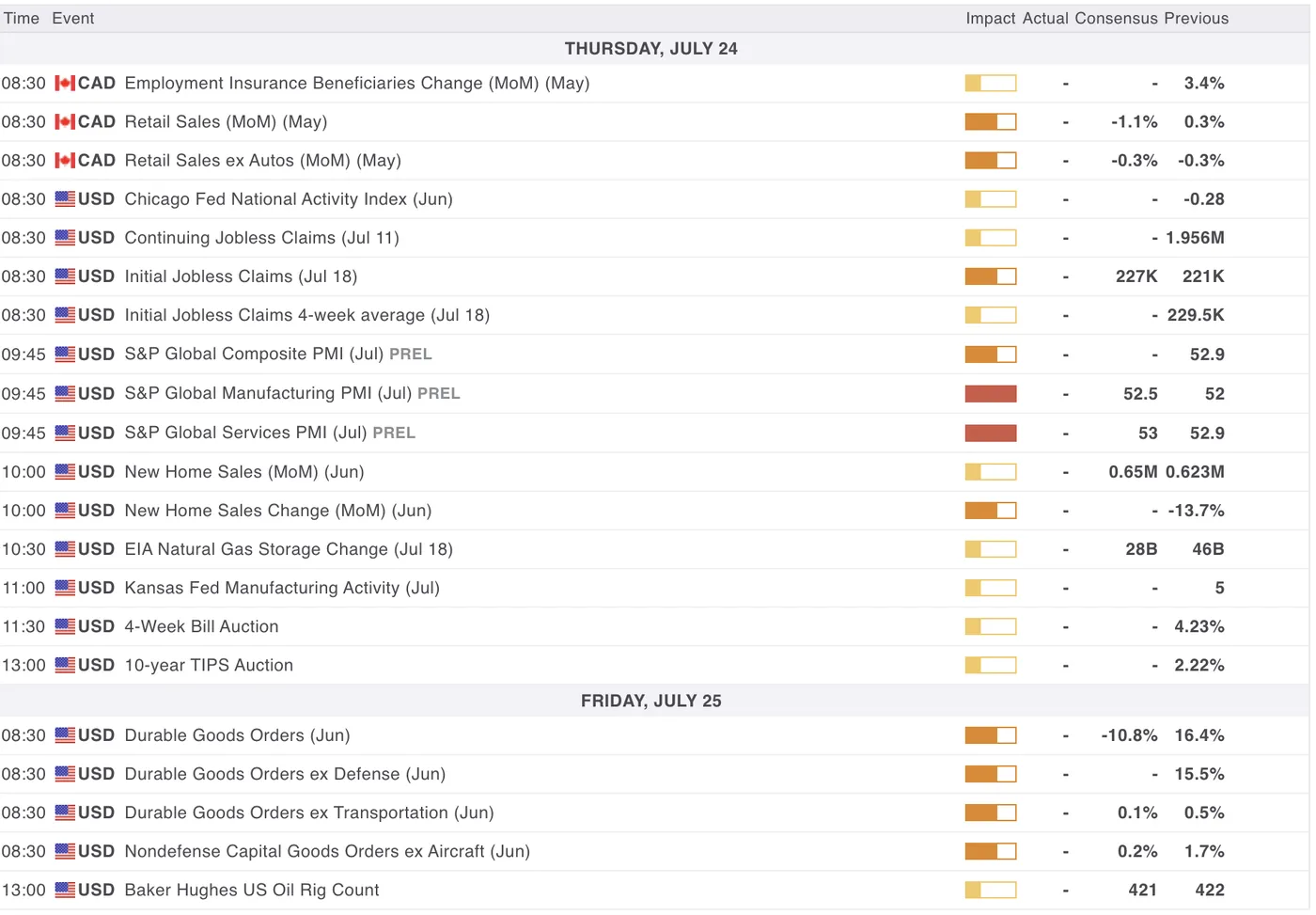

US and Canada Economic Calendar for the Rest of the Week

US and Canadian Data for the rest of the week, MarketPulse Economic Calendar

The rest of the week is promised to be more instructive in terms of Economic data releases.

Tomorrow (Thursday 24th) will see the release of Canadian Retail Sales at 8:30 A.M. with the Headline number at -1.1% Consensus.

Do not forget the weekly Jobless Claims (exp 227K)

The day will shortly follow with US Manufacturing (exp 52.5) and Services PMIs (exp 53) at 9:45 A.M. ET.

Friday should be lighter however with mostly the Durable Goods order data, which can be interesting data to look at the impacts of the Trump Policies in further detail.

Oil Traders should also monitor the Baker Hughes Oil Rig Counts at 13:00 on Friday.

Safe Trades for the rest of the week!

Dow Jones Rebalancing Continues After US-Japan Trade Deal

The week has been calm in terms of economic data releases and despite the ongoing Earnings season, Markets have been looking for headlines.

And headlines they received! Yesterday evening saw the announcement of a much anticipated US-Japan Trade Deal that would largely diminish announced tariffs from 25% and more to an actual of 15% on Auto Imports.

You can read more on the deal right here. – Except for wishy-washy trading in USDJPY, Equities have appreciated the news. The Nikkei closed the Asia session up around 4.50% and European stocks have also been lifted by the news.

In the US, the Indices have opened positive but the trend that started in the beginning of the week is currently continuing:

The Nasdaq is seeing some profit-taking and these flows are going towards the Dow Jones, with Futures and CFD prices still positive since the start of the day but the actual open is mixed, seeing some selling.

AT&T have released earnings beating EPS and Revenues by a decent margin, setting the stage for some more confidence in US Stocks.

The Industrial-focused Index has been strong within its ongoing range, and in the waiting of the Alphabet (Google) and Tesla earnings, the relative strength for the Dow is poised to continue.

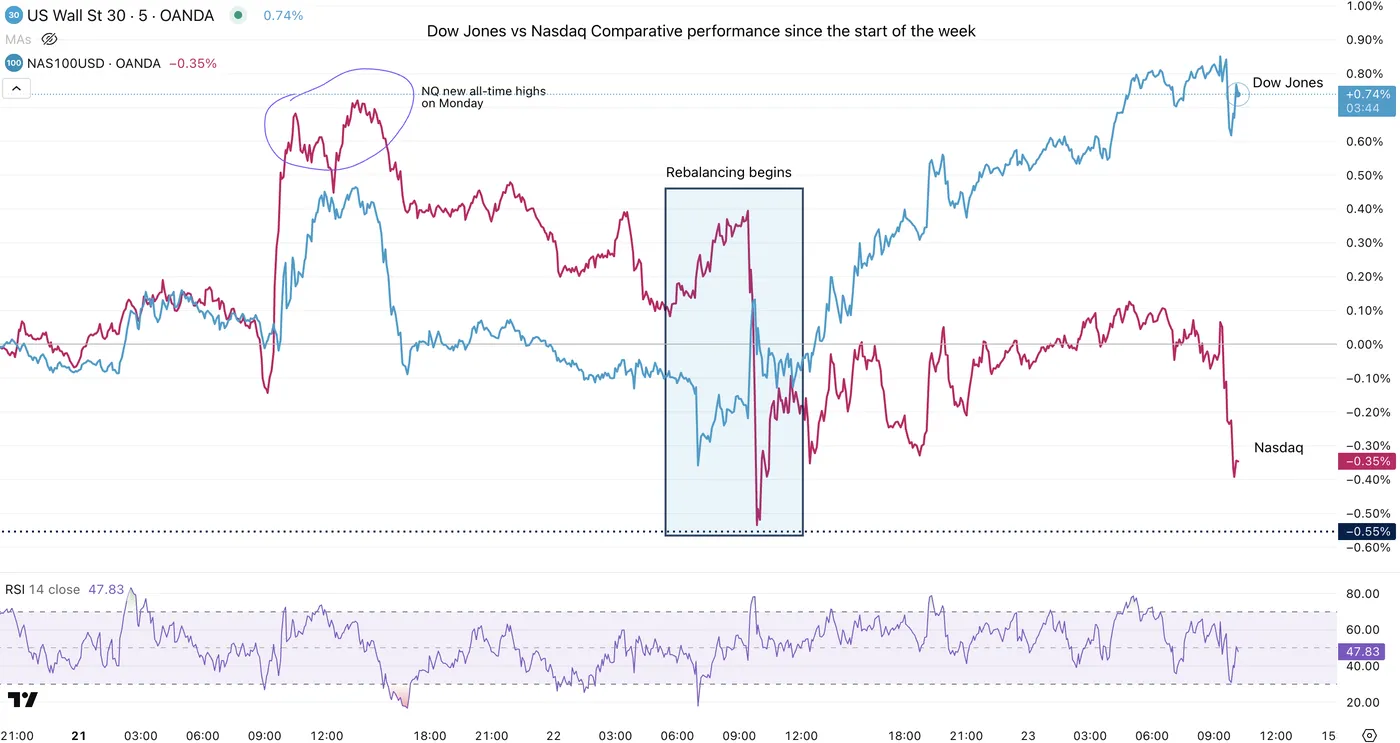

Dow Jones vs Nasdaq Comparative weekly performance

Dow Jones vs Nasdaq Relative Strength, July 23 2025 – Source: TradingView

Tech had started the week on a strong note but since the middle of yesterday's session, there has been some powerful rewiring of positioning in the US Indices, with Tech struggling vs Healthcare, Banking Consumer Cyclical and Defensive stocks – A reverse of the prior year trend.

This is allowing the Dow to shine again in today's session.

Dow Jones Intraday Technical Analysis

1H Timeframe

Dow Jones 1H Chart, July 23 2025 – Source: TradingView

The Dow has officially broken out of the descending channel that was occuring within the ongoing July Range (44,912 highs and 43,788 Lows).

With the ongoing relative strength in the US 30, bulls have broken above the 75% percentile of the range on a clear, lower timeframe double bottom and prices are currently consolidating just above this point that was precedently resistance, now pivot.

These levels are:

Support Levels:

- Immediate Pivot (preceding Resistance): 44,600 to 44,700

- 50-Period 1H MA 44,515

- Strong Support on Double Bottom and 200-H MA – 44,200 to 44,300

- 43,780 to 44,100 Major Support

Resistance Levels:

- 44,810 Daily Highs

- 44,912 July Highs

- 45,060 All-time Highs

15M Timeframe

Dow Jones 15m Chart, July 23 2025 – Source: TradingView

Buyers have held a strong intraday uptrend that had formed yesterday afternoon.

RSI Momentum is currently neutral after coming back from overbought, with bulls having to maintain above the Pivot to keep their strong hands – Monitor momentum as the price action is mixed on the lower timeframe but the latest 15m bull candle is a strong one.

Breaking above 44,812 (Daily highs) will point towards the July highs, but after that, there won't be much until the All-time highs.

Failing to hold above the 44,600 to 44,700 Pivot will re-affirm the preceding range and point to more balanced price action.

Safe Trades in the waiting of this afternoon's key earnings!

Euro Rally Fizzles, ECB Expected to Hold Rates

The euro has edged lower on Wednesday after a three-day rally which saw the currency climb 1.4% against the US dollar. In the North American session, EUR/USD is trading at 1.1724, down 0.25% on the day.

ECB projected to hold rates at 2.0% on Thursday

The European Central Bank will announce its rate decision on Thursday and the money markets are widely expecting that the ECB will maintain the key deposit rate at 2.0%.

The ECB has trimmed rates by a quarter-point for seven consecutive meetings. At the June meeting, ECB President Lagarde signaled that the central bank was nearing the end of its easing cycle, which began in June 2024 when the deposit rate stood at 4.05%.

Inflation in the eurozone is largely contained. In June, headline CPI remained steady at 2.0%, the ECB's target, and core CPI was unchanged at 2.3%. These inflation levels would allow the ECB to continue lowering rates but ECB policymakers face the big unknown of President Trump's tariff policy, with no trade agreement yet between the US and the European Union. Trump has threatened the EU with 30% tariffs if no deal is reached by August 1.

The EU has vowed to respond forcefully, saying it will impose a 30% tariff on a range of US goods if Trump makes good on his threat. That could set into motion retaliatory tariffs from the US and trigger an ugly trade war between two of the largest economies in the world. The US and Japan announced today that they had reached a trade deal and there is hope that the EU will follow suit. This would provide much needed clarity for the ECB and make it easier to forecast growth and inflation.

EUR/USD Technical

- EUR/USD is testing support at 1.1731. Below, there is support at 1.1702

- There is resistance at 1.1784 and 1.1813

EURUSD 1-Day Chart, July 23, 2025

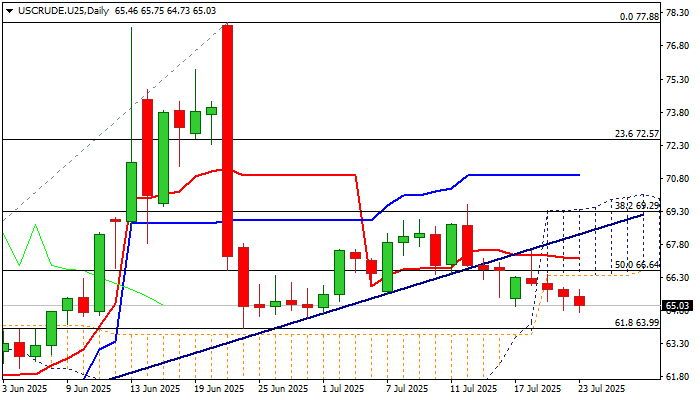

WTI Oil: Bears Hold Grip as Trade Issues Continue to Sour sentiment

WTI oil price remains in red for the fourth consecutive day and trading near new three-week low on Wednesday.

Bears hold grip despite a partial relief from announcement of US trade deal with Japan, as dissonant tone come from the EU (the bloc did not reach a deal yet but considering countermeasures on US tariffs) and China, that continues to sour the sentiment.

Markets also focus on the signals of impact from the latest package of EU sanctions on Russia, which mainly target Russian oil industry, as well comments that the US would consider sanctioning Russian oil that are assumed as supportive factors.

Increased supply after Azerbaijan oil exports resumed today after being paused for a couple of days, contribute to existing pressure on oil prices.

Technical picture weakened after the price broke below ascending and thickening daily Ichimoku cloud, while daily Tenkan/Kijun-sen remain in bearish configuration.

Bears attack again 100DMA ($64.93) after faced several rejection at the indicator, with firm break here to expose next significant support at $63.99 (Fibo 61.8% retracement of $55.70/$77.88 rally).

Daily cloud base ($66.37) marks solid resistance which should ideally cap potential upticks.

Res: 65.80; 66.37; 67.18; 68.28.

Sup: 64.50; 63.99; 63.05; 62.18.