Sample Category Title

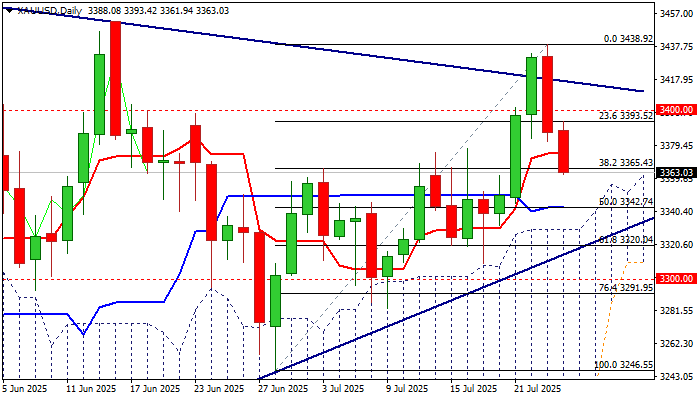

XAU/USD: Gold extends pullback on growing risk sentiment

Gold price falls for the second day, as growing optimism over possible US-EU trade deal continues to fuel risk appetite and deflates safe-haven demand.

Fresh weakness emerged after bulls failed to register a clear break above trendline resistance (daily chart triangle’s upper boundary) with return below the trendline signaling a false break higher and generating bearish signal.

The yellow metal’s price lost around 2% since Wednesday’s opening and cracked pivotal support at $3365 (Fibo 38.2% of $3246/$3438, reinforced by 10DMA, with sustained break here to confirm reversal signal, following Wednesday’s completion of bearish engulfing and close below psychological $3400 support.

Technical picture on daily chart has weakened, although studies are still positive overall, suggesting that current weakness needs to find ground above the top of daily Ichimoku cloud ($3330) to keep larger picture bullishly aligned.

Otherwise, violation of cloud top and nearby lower triangle boundary ($3317) would generate stronger bearish signal and bring the downside at increased risk.

Res: 3393; 3400; 3419; 3438.

Sup: 3342; 3330; 3317; 3309.

FTSE 100 Breaks Records as Euro Area Private Sector Growth Hits 11-Month Highs, ECB Meeting Ahead

Asia Market Wrap - Sentiment on the Up

Global stocks hit a new record high, boosted by a 1% rise in Asia. Japanese markets surged up to 2%, driven by strong performance in the financial sector, while the yen strengthened as investors believed a trade deal could lead to an interest rate hike.

Nasdaq 100 futures climbed 0.3% after Alphabet's earnings, but Tesla shares fell in after-hours trading due to a weak forecast.

Easing global trade tensions have calmed investors, reducing fears of a long trade war and driving market gains. Many believe the US will take a practical approach to avoid tariffs significantly hurting company profits.

President Trump hinted he wouldn’t lower tariffs below 15% as he prepares new trade rules before the August 1 deadline.

Euro Area PMIs

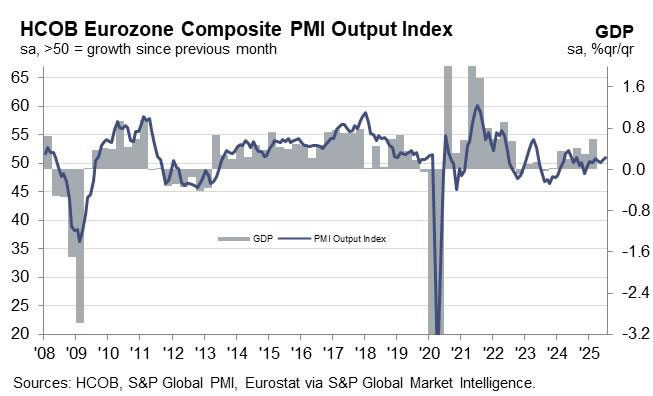

The HCOB Eurozone Composite PMI rose to 51 in July 2025, up from 50.6 in June, showing the fastest growth in private economic activity in 11 months and slightly beating expectations of 50.8.

The growth was driven by stronger performance in the services sector (51.2 vs 50.5 in June) and a near recovery in manufacturing (49.8 vs 49.5), which had its least negative result in three years. New orders remained steady, ending 13 months of decline, which helped boost output in both sectors.

This positive trend in new business encouraged companies to hire more staff for the first time in five months. On prices, input costs rose at a slower pace, allowing firms to keep their prices steady after two months of cuts. However, business confidence dipped slightly, likely due to ongoing concerns about US tariff threats.

European Open - US/EU Trade Negotiation, ECB Meeting

Optimism about a trade deal pushed global stocks to new record highs on Thursday. This came ahead of key global economic data, a European Central Bank meeting, and an unexpected visit to the Federal Reserve by US President Donald Trump.

Reports that the EU and US were nearing a deal on 15% tariffs, with exceptions for some industries, followed a recent agreement with Japan. This boosted the MSCI world stock index for the seventh day in a row.

In Europe, the positive trend continued as Germany's DAX index, which relies heavily on exports, rose over 1%, and the STOXX regional index gained 0.6%.

Deutsche Bank's better-than-expected results sent its shares up more than 4%, lifting banking stocks to their highest level since the 2008 financial crisis. However, Nestle's shares dropped 4.5% after it announced its first-half results and plans to sell one of its businesses.

The pound fell by 0.28% to 1.3544 after reaching a two-week high of 1.3588 earlier in the session.

The dollar gained slightly against the euro and yen following progress in trade talks.

The pound also weakened against the euro, which dropped 0.16% to 86.81. Last week, the euro reached 86.98, its highest level since April 11.

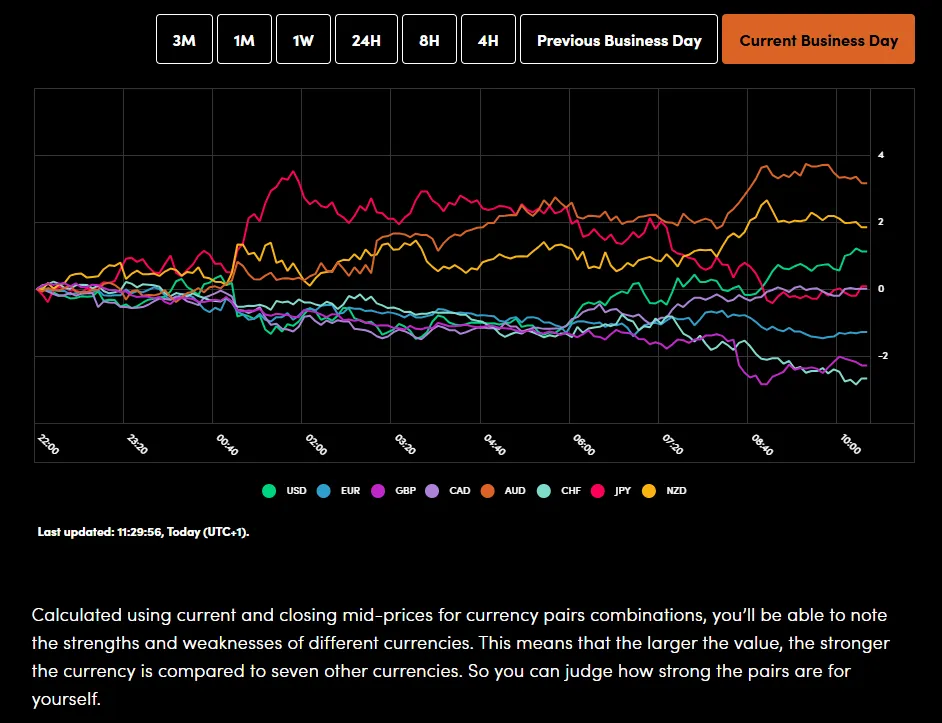

Currency Power Balance

Source: OANDA Labs

In commodity markets, oil prices went up as traders speculated that recent trade deals would boost global growth. Prices also rose due to a bigger-than-expected drop in US crude stockpiles. US crude increased by 0.52% to 65.59 per barrel.

Meanwhile, gold prices dipped slightly to $3,370 per ounce as investors showed more interest in riskier assets, reducing demand for safe-haven options like

Economic Data Releases and Final Thoughts

Looking at the economic calendar, we are finally getting some high impact later today.

First we have the ECB meeting where the Central Bank is expected to keep rates on hold, with 90% probability based on LSEG data.

Earnings season continues today and then later in the US session we will get the latest PMI numbers from the world's largest economy as well.

This will be the first glance for market participants from the mag 7 stocks which could stoke some interesting market reactions depending on the release.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Day - FTSE 100 Index

From a technical standpoint, the FTSE 100 index has continued its rise with an amazing four-hour candle close this morning.

Improved trade deal sentiment and the impressive rally on Wall Street could be the driving force.

The FTSE is now comfortably in overbought territory and we are seeing a slight pullback this morning.

Immediate support rests at 9110 before the 9048 and 9000 handles comes into focus.

The upside does not have any historical data to focus on and thus I will look toward psychological numbers like 9250 and potentially 9500.

FTSE 100 Daily Chart, July 24. 2025

Source: TradingView.com (click to enlarge)

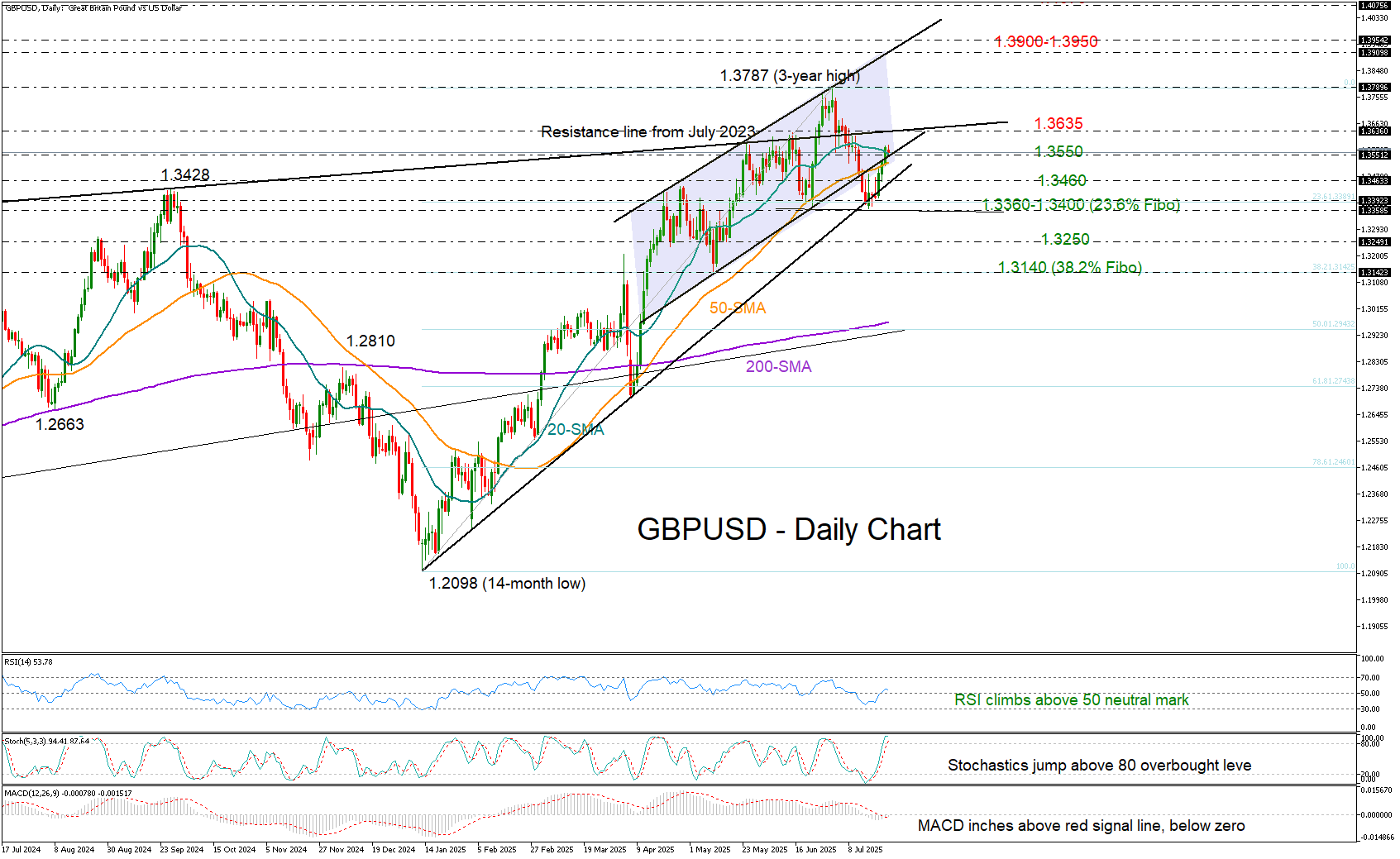

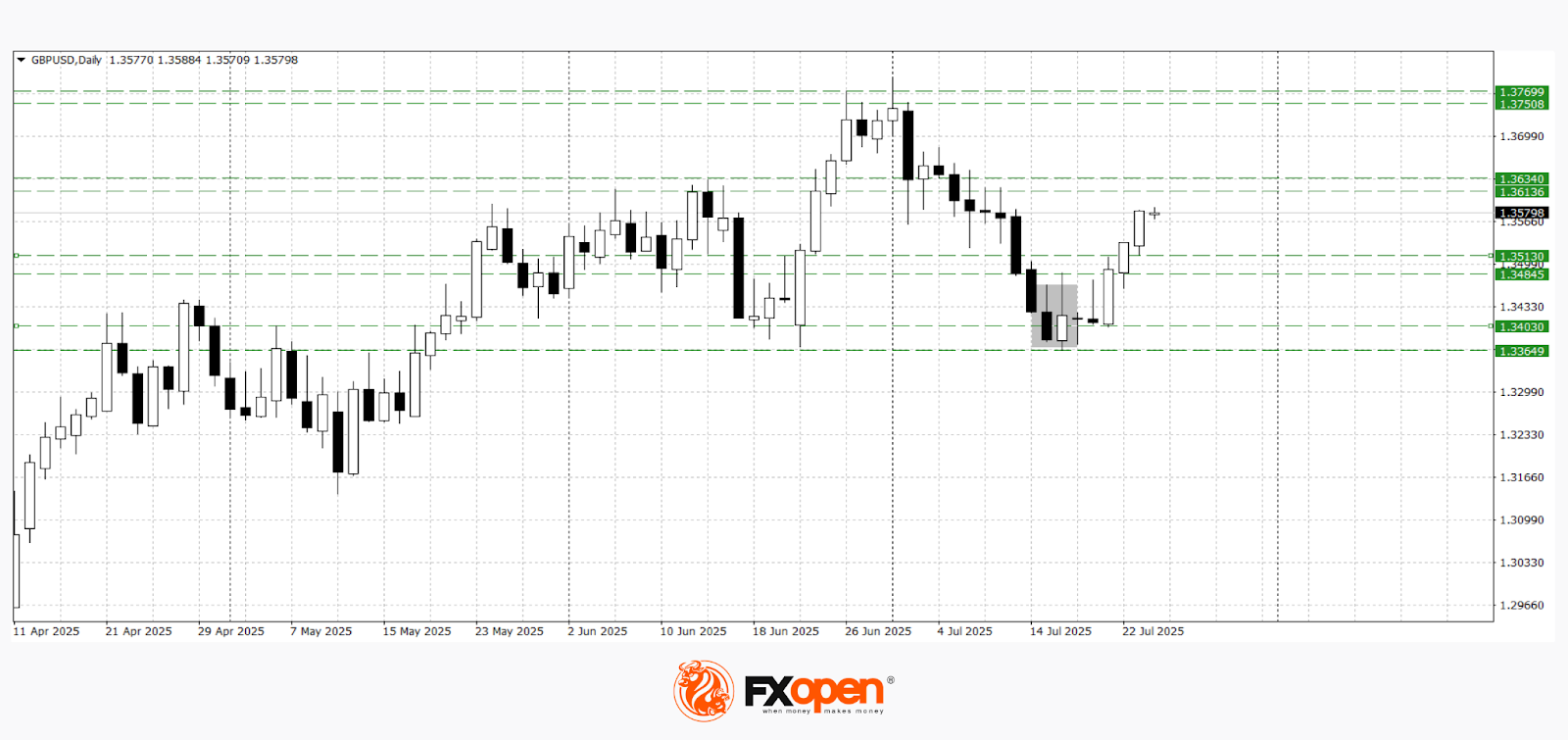

GBP/USD Recovery Faces Key Test

- GBP/USD retraces half of July’s losses, edges above short-term SMAs.

- Technical risk is skewed to the upside, but another challenge looms near 1.3635.

GBP/USD escaped a drop below the 1.3390–1.3400 support area last week, helped by dollar weakness, and is now attempting a close back above its 20- and 50-day simple moving averages (SMAs) near 1.3550.

The latest rebound preserved the nearly 14% year-to-date rally, but for bullish sentiment to strengthen, the pair must also clear the resistance line drawn from July 2023 at 1.3635. A decisive move above the three-year high of 1.3787 could then pave the way toward the 1.3900 round level, where the upper boundary of the short-term bullish channel lies. Beyond that, the price could pause near the 161.8% Fibonacci extension of the prior decline at 1.4070, before potentially heading toward the psychological 1.4200 mark.

Both the RSI and MACD indicators suggest that upward momentum could continue. However, with the stochastic oscillator surging into overbought territory, some caution is warranted. In any case, sellers are likely to remain on the sidelines unless the price breaks below the 1.3360 support zone, which would bring the 1.3245 area into focus. Further losses could trigger a deeper decline toward the 38.2% Fibonacci retracement of the 2025 uptrend at 1.3140.

In brief, GBPUSD bulls may retain control in the short term if the pair establishes a solid foothold above 1.3550 and overcomes the 1.3635 barrier too. Failure to do so could signal a false breakout, raising the risk of a bearish head and shoulders formation.

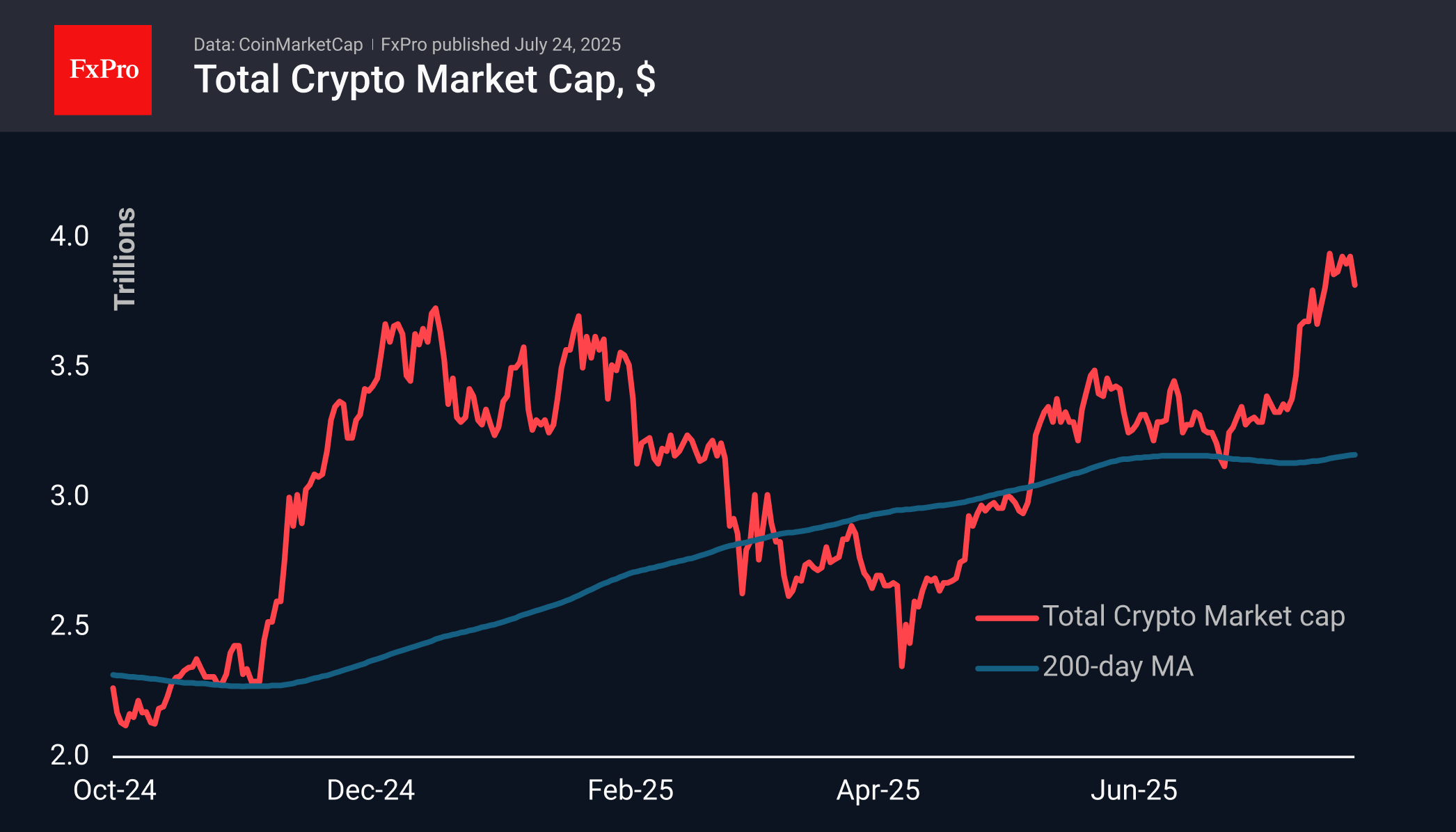

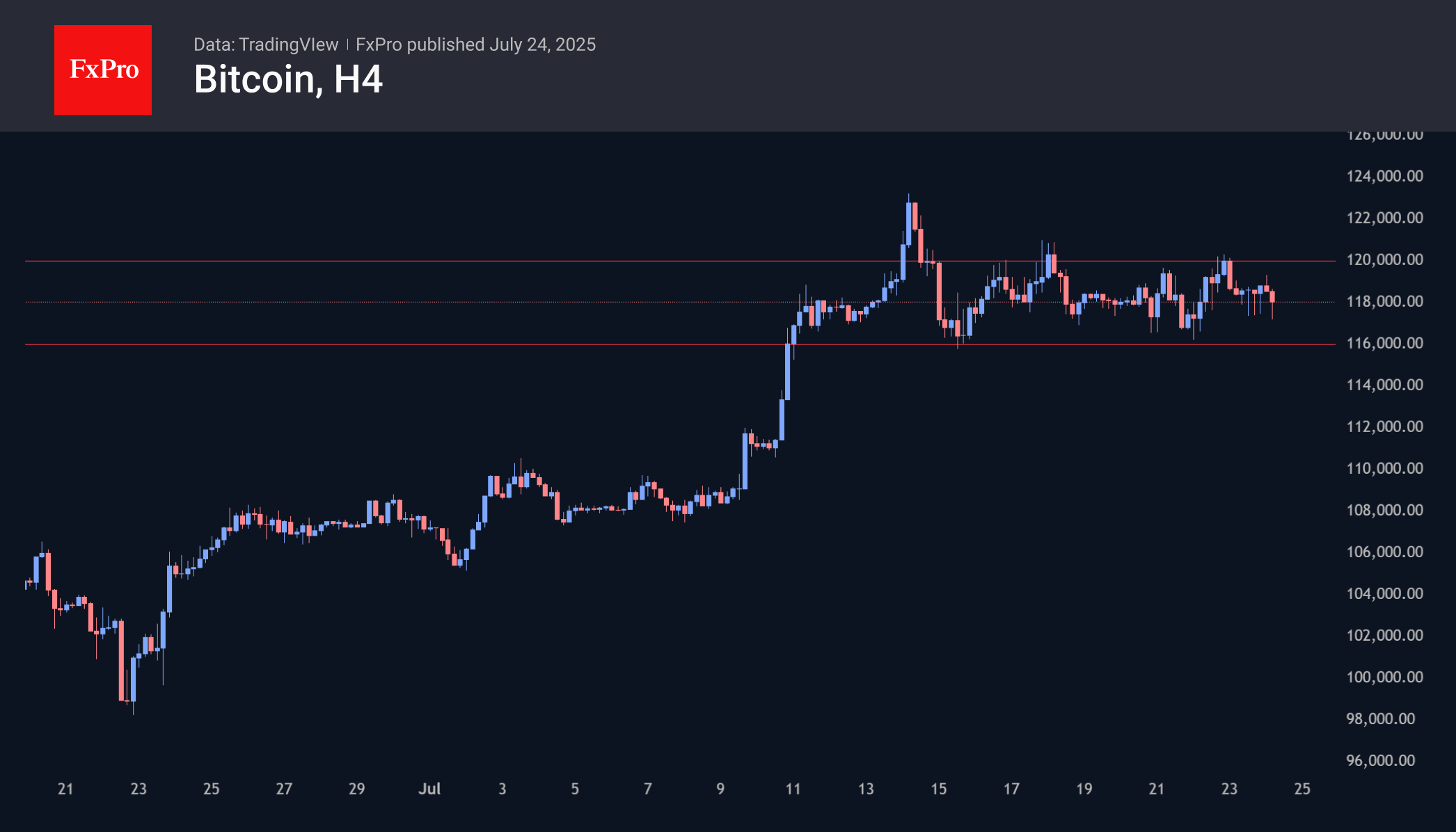

Crypto Market Nosedive

Market Overview

The crypto market took a nosedive, losing almost 4% of its market cap over the last 24 hours. Without Bitcoin’s growth, altcoins, which had been driving the market upwards in previous days, found themselves on sale. Forty-eight of the top 100 altcoins are losing double-digit rates over 24 hours, while only three are growing.

The first cryptocurrency has been facing both a price drop and an outflow from ETFs over the past couple of days, while Ethereum continued to attract new capital to funds. Meanwhile, BTC remains stuck in a narrow range. At $117.3K on Thursday morning, it was on its way to the lower limit of $116K. A reversal to growth will be needed to stop the build-up of pessimism for the entire crypto market, where corrective sentiment is intensifying. If we look only at BTCUSD, a decline to $111K — the area of previous peaks — fits well into the pattern of a corrective pullback.

News Background

According to LVRG Research, institutional investors remain optimistic about Ethereum. There is an outflow of funds from Bitcoin to ETH, which often happens before a surge in altcoin growth.

Bitwise notes that the key driver of the Ethereum rally is high demand from ETFs and corporate treasuries. Since mid-May, Ethereum ETFs have attracted more than $5 billion in investments. Companies such as Bitmine and SharpLink bought 2.83 million ETH for $10 billion. During the same period, the network issued only 88,000 ETH.

According to Lookonchain, there is significant activity in the crypto market from large BTC and Ethereum holders, which may be due to a desire to lock in profits after price increases. EmberCN confirms the flow of large batches of coins to Binance, which are probably for sale.

The BNB cryptocurrency has updated its historical highs made last December and exceeded $800, taking fifth place in the CoinMarketCap ranking and pushing Solana aside. The growth may have been facilitated by the inflow of institutional capital into ETF products.

Upexi announced the acquisition of 100,000 Solana coins for $17.7 million at an average price of $176.77. Upexi’s total reserves reached 1,818,809 SOL ($331 million), acquired for $273 million.

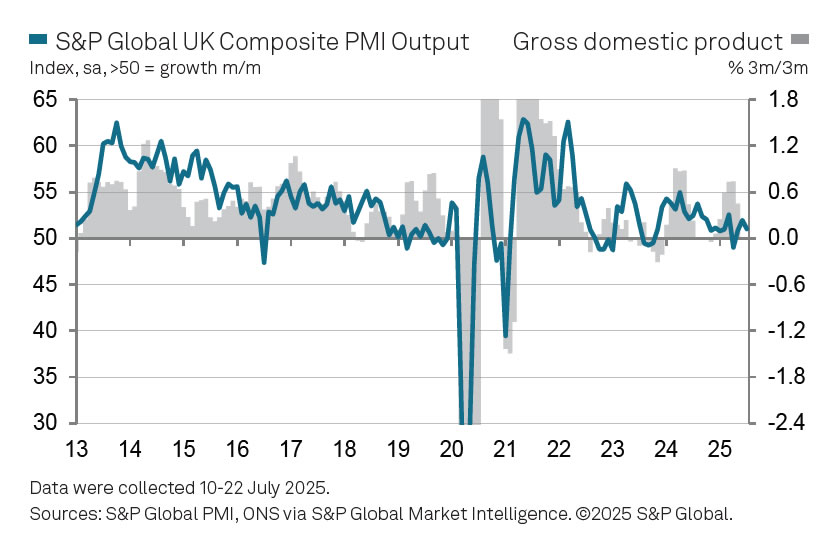

UK PMI composite falls to 51, BoE cut pressure builds

The UK economy showed signs of losing momentum in July, with Composite PMI falling from 52.0 to 51.0. A modest rise in Manufacturing PMI to 48.2 from 47.7 failed to offset a sharp slowdown in services activity, which dropped from 52.8 to 51.2. Overall, the data point to a fragile expansion at the start of Q3.

Chris Williamson at S&P Global Market Intelligence warned that output growth is now consistent with just a 0.1% quarterly GDP gain, and that “risks are tilted to the downside.” Persistent job shedding across sectors underscores the underlying weakness, raising concerns about near-term demand conditions.

With growth stalling and the labor market softening, Williamson said that will add pressure to the BoE to deliver another rate cut in August. While recent inflation data surprised to the upside, the BoE could “look through” those pressures and prioritize support for a struggling economy.

Pound Strengthens: Trade Tariffs and Economic Data Boost GBP/USD

The GBP/USD pair climbed to a two-week high on Thursday, holding near 1.3578, bolstered by improved global risk sentiment following the US-Japan trade agreement.

The deal, which replaces previously proposed 25% tariffs with a 15% levy, also includes the creation of a $550 billion investment fund to support the US economy. President Donald Trump hailed the agreement as mutually beneficial, further lifting market confidence.

Investors are now turning their attention to key UK economic indicators. PMI forecasts suggest the smallest contraction in manufacturing activity in six months, accompanied by the sharpest rise in services sector growth in nearly a year. Retail sales are also expected to rebound, aided by recent warm weather.

However, concerns linger after the UK reported a June budget deficit of £20.7 billion – the second-highest June figure since 1993. Rising inflation-linked bond repayments pushed debt servicing costs to £16.4 billion, adding pressure on public finances.

Amid these developments, speculation is mounting that Chancellor Rachel Reeves could announce tax increases as early as the autumn to address fiscal challenges.

Technical Analysis: GBP/USD

H4 Chart:

On the H4 chart, GBP/USD completed an upward wave to 1.3535, forming a consolidation range around this level. A breakout above this range could extend gains towards 1.3593. However, a subsequent correction downwards to 1.3530 remains possible. This scenario is supported by the MACD indicator, where the signal line sits above zero and is pointing firmly upward.

H1 Chart:

The H1 chart shows the pair finding support at 1.3462, with the current growth wave reaching its initial target of 1.3585. A short-term pullback to 1.3530 may occur before another upward move towards 1.3593. The Stochastic oscillator aligns with this outlook, as its signal line hovers below 5 and is trending downward towards 20.

Conclusion

The GBP/USD rally reflects an improvement in risk sentiment and anticipation of stronger UK economic data. However, fiscal concerns and technical indicators suggest potential volatility ahead. Traders should monitor PMI releases and fiscal policy announcements for further direction.

EUR/USD Rises to 2.5-Week High Ahead of ECB Meeting

Today at 15:15 GMT+3, the European Central Bank (ECB) will announce its interest rate decision, followed by a press conference at 15:45 GMT+3. According to Forex Factory, the main refinancing rate is expected to remain unchanged at 2.15% after seven consecutive cuts.

In anticipation of these events, the EUR/USD exchange rate has risen above the 1.1770 level for the first time since 7 July. Bullish sentiment is also being supported by expectations of a potential trade agreement between the United States and the European Union. According to Reuters, both sides are reportedly moving towards a deal that may include a 15% base tariff on EU goods entering the US, with certain exemptions.

Technical Analysis of the EUR/USD Chart

From a technical perspective, the EUR/USD pair has shown bullish momentum since June, resulting in the formation of an ascending channel (marked in blue).

Within this channel, the price has rebounded from the lower boundary (highlighted in purple), although the midline of the blue channel appears to be acting as resistance (as indicated by the arrow), slowing further upward movement.

It is reasonable to assume that EUR/USD may attempt to stabilise around the midline—where demand and supply typically reach equilibrium. However, today’s market is unlikely to remain calm. In addition to the ECB’s statements, volatility could be heightened by news surrounding Donald Trump’s unexpected visit to the Federal Reserve.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

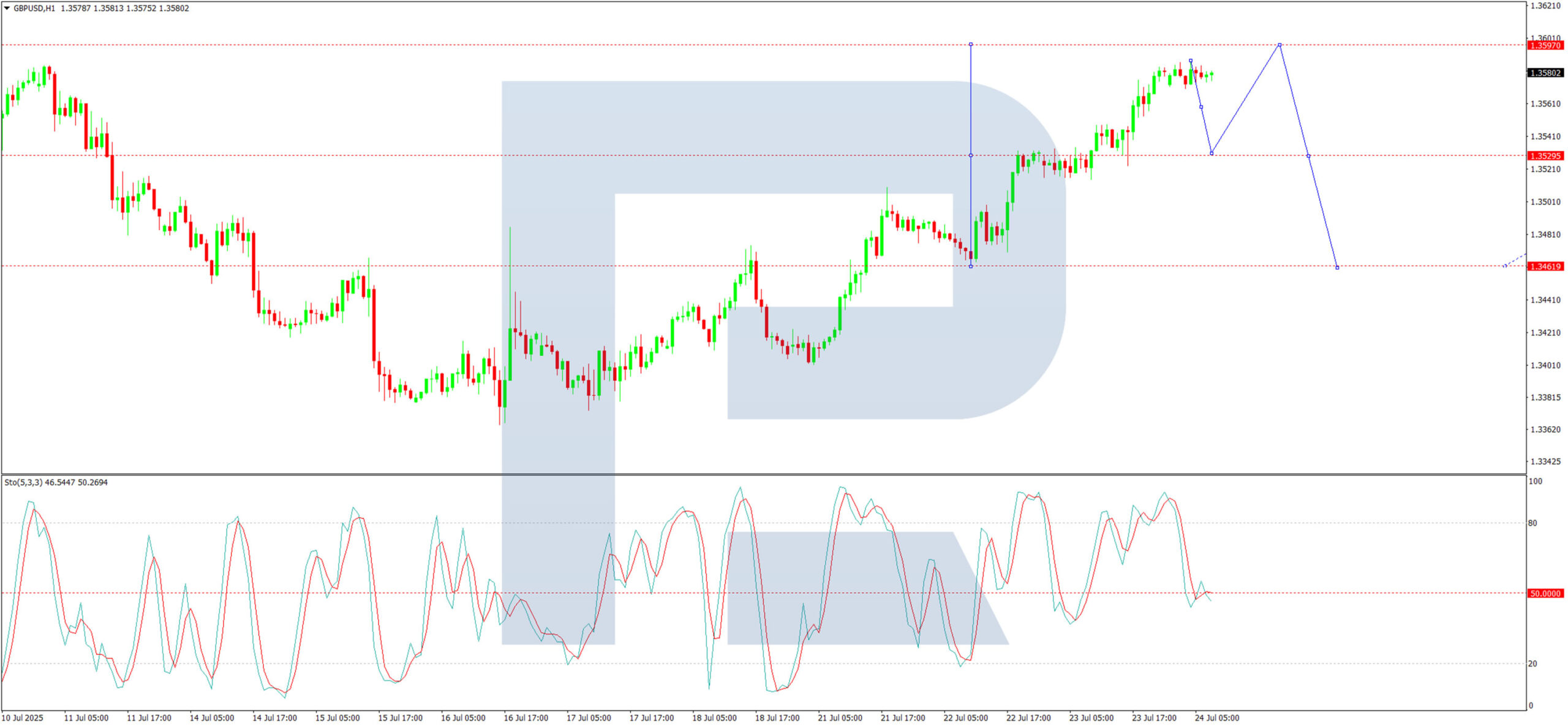

Pound Strengthens After Testing Key Support Levels, Retail Sales Data in Focus

The British currency continues its recovery following a test of key technical support levels. GBP/USD and GBP/CAD have risen amid moderate US dollar weakness and mixed Canadian macroeconomic data. Investor attention remains focused on upcoming economic indicators, which are due to be released over the next trading sessions. Today, the market is closely watching a batch of data from the US and Canada, including updated statistics on initial jobless claims, total continuing claims, and the Chicago Fed National Activity Index. On Friday morning, markets await the release of June retail sales figures from the UK. Against this backdrop, the pound remains highly sensitive to economic data and monetary policy signals. Should UK data prove neutral or stronger than expected, the current upward momentum may persist.

GBP/USD

Following a test of the key support range at 1.3370–1.3400, GBP/USD formed a bullish piercing line pattern. Technical analysis suggests the potential for further upside towards the 1.3610–1.3640 area. However, in the event of weak UK macroeconomic data, the pair may retreat towards 1.3480–1.3510.

Key events likely to influence GBP/USD movement:

- Today at 11:30 (GMT+3): UK Services PMI

- Today at 11:30 (GMT+3): UK CBI Industrial Order Expectations

- Today at 16:45 (GMT+3): US Manufacturing PMI

GBP/CAD

GBP/CAD has been consolidating within the 1.8340–1.8490 range for several days. A breakout above the upper boundary could see the pair test resistance at 1.8540–1.8570. However, if Canadian data proves strong or UK figures disappoint, a pullback towards 1.8300–1.8340 cannot be ruled out.

Key events likely to influence GBP/CAD pricing:

- Today at 15:30 (GMT+3): Canada Core Retail Sales

- Tomorrow at 09:00 (GMT+3): UK Core Retail Sales

- Tomorrow at 18:00 (GMT+3): Canada Federal Budget Balance

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Asian Stocks Rise on AI Optimism, US-EU Trade Hopes, EUR/GBP Bullish Trend Intact as ECB Looms

S&P 500 and Nasdaq 100 E-mini futures continued to edge higher in Asia’s Thursday session, up 0.1% and 0.3% respectively. Gains were supported by upbeat sentiment from Wednesday’s US session, despite mixed Q2 results from Tesla and Alphabet. Investor optimism was further boosted by President Trump’s new executive orders to bolster US artificial intelligence capabilities and improve prospects for a US-EU trade agreement.

Tesla drops on earnings miss, while Alphabet rises on AI demand

Tesla shares tumbled 4.4% in after-hours trading as Q2 earnings fell short of expectations ($0.40 EPS vs. $0.48 consensus). CEO Elon Musk’s cautious outlook—citing the phase-out of EV incentives and slow driverless tech deployment—added to the negative sentiment. In contrast, Alphabet shares rose 1.7% after beating earnings forecasts ($2.31 EPS vs. $2.16), buoyed by strong AI-driven sales growth.

US stocks rally to fresh highs, led by Dow and tech giants

The S&P 500 climbed 0.8% to a new all-time high, while the Nasdaq 100 gained 0.4%, led by Nvidia (+2.3%). The Dow Jones Industrial Average outperformed with a 1.1% jump to 45,010—just shy of its record high from December 2024. All major US indices remain in strong short-to-medium-term uptrends.

Asia markets track Wall Street gains as US-EU Trade talks advance

Asia-Pacific equities mirrored the US rally amid growing optimism that the 1 August US-EU trade deadline may yield a breakthrough. Media reports suggest progress toward a 15% tariff on most EU imports, replacing prior sticking points in negotiations.

Nikkei nears record high; STI and Hang Seng extend gains

Japan’s Nikkei 225 surged 1.7% to 41,870, closing in on its all-time high of 42,427. Hong Kong’s Hang Seng Index added 0.4%, marking its fifth straight daily gain. Meanwhile, Singapore’s Straits Times Index rose 0.8%, poised to log a 14th consecutive record close,up 11% from its 23 June low.

Japanese yen leads FX moves ahead of ECB, Gold slides toward support

The US dollar weakened further during Asia hours, with the Japanese yen outperforming major peers, gaining 0.4%. The Australian dollar also advanced by 0.3%.

The euro and sterling traded almost unchanged from Wednesday’s US session close as traders await the European Central Bank (ECB) monetary policy decision out later today, where the consensus has priced in no rate cut to maintain its key deposit rate at 2% after eight consecutive cuts.

ECB President Lagarde’s press conference will be pivotal as market participants look out for more hints to indicate ECB is at the end of its interest rate cut cycle. If such hawkish hold guidance materialises, the EUR/USD is likely to have more impetus to maintain its recent minor short-term bullish uptrend phase that kickstarted last Wednesday, 17 July.

Meanwhile, gold (XAU/USD) extended its decline, shedding 0.3% intraday after a 1.3% drop yesterday. The precious metal is now nearing a key short-term support at US$3,260, where buyers may return.

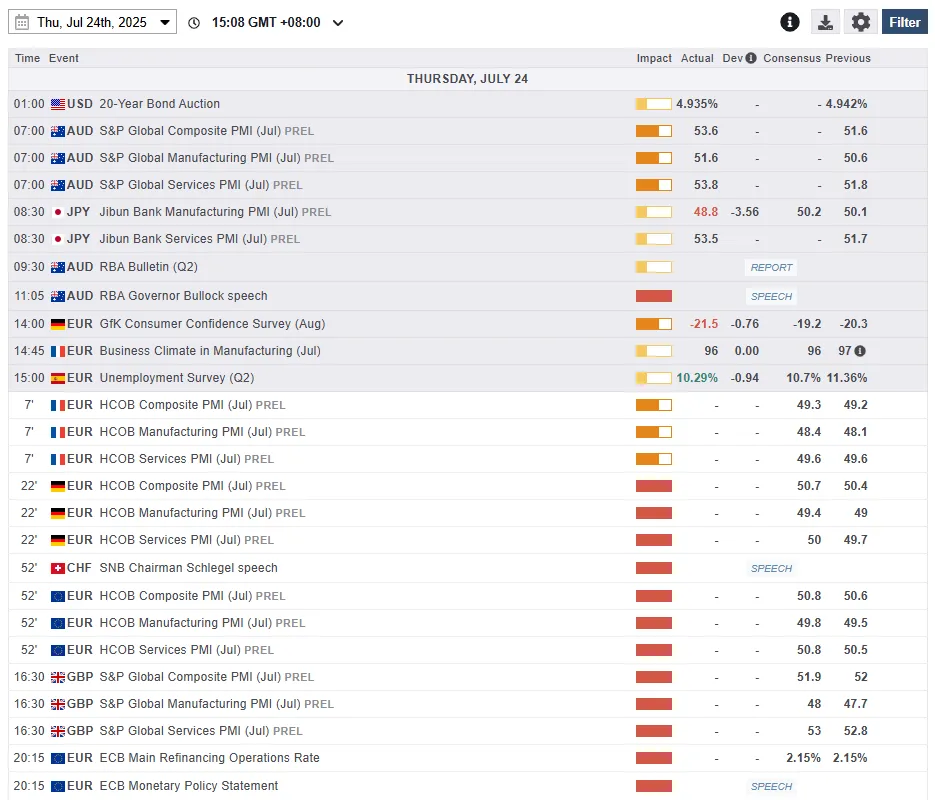

Economic data releases

Fig 1: Key data for today’s Asia mid-session (Source: MarketPulse)

Chart of the day – EUR/GBP looks set to resume its bullish move as ECB looms

Fig 2: EUR/GBP minor & medium-term trends as of 24 July 2025 (Source: TradingView)

The recent slide of 58 pips seen on the EUR/GBP cross pair from its 15 July swing high area of 0.8700 has hit a key inflection point for the bulls to resume a potential bullish impulsive up move sequence with its short-term minor uptrend phase in place since 27 June 2025 low.

Firstly, the price action of EUR/GBP has staged a bounce right above the lower boundary of its medium-term ascending channel from 29 May 2025 low, and its rising 20-day moving average.

Secondly, the hourly RSI momentum indicator has formed a “higher low” after it hit a recent oversold reading on 23 July, which suggests a potential short-term bullish momentum revival.

Watch the 0.8640 short-term key pivotal support, and a clearance above 0.8700 increases the odds of a fresh bullish impulsive up move sequence to see the next intermediate resistances coming in at 0.8740/8770 and 0.8800 (see Fig 2).

However, a break below 0.8640 invalidates the bullish scenario for a minor corrective decline to expose the next intermediate supports at 0.8600 and 0.8540 (also the 50-day moving average).

Eurozone PMI composite hit 11-month high, gradually regaining momentum

Eurozone private sector activity accelerated in July, with Composite PMI rising from 50.6 to 51.0—its highest level in 11 months. Manufacturing PMI improved slightly from 49.5 to 49.8, a 36-month high, edging closer to the 50-mark that separates expansion from contraction. Services PMI climbed to a six-month high of 51.2, from 50.5, pointing to broad-based improvement across sectors.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, said the data suggests the Eurozone economy is "gradually regaining momentum." The manufacturing recession is "coming to an end," while services growth has picked up. Their GDP Nowcast model indicates the region is on track for “robust economic growth” in Q3, with Germany likely to show slight expansion while France may post a mild contraction, partly due to its domestic political uncertainty.

For the ECB, the data offers some relief. Services inflation—a key focus for policymakers—continued to ease in July. While goods prices stabilized, a stronger Euro and ongoing US tariffs are expected to put downward pressure on price levels in the months ahead.