Sample Category Title

Silver Maintains Around 2011 Levels

Silver has had quite a run this month, up 7.40% only since the 10th of July.

Today we'll take a quick look at an update of a multi-timeframe Silver analysis to spot the ongoing trends and see if the trend has still some juice.

This article is a continuation of the article posted on the 15th of July where we only looked at intraday timeframes.

Now let's take a step back.

Silver Weekly Chart

Silver Weekly Chart, July 24 2025 – Source: TradingView

Momentum is strong for the metal but starting to test the upper bound of the RSI with around $2 to $3 missing towards the highs of the ongoing light blue weekly channel.

This is a good drawing to keep on your charts to maintain a good view of where we are in the current trend.

Silver Daily Chart

Silver Daily Chart, July 24 2025 – Source: TradingView

The precious metal has made an impulsive move higher reaching the $39 to $39.50 Resistance we observed last week.

There is still work to do to test the high of the weekly channel, but the overbought conditions in the metal will make it difficult for an immediate move to happen.

The 20 Day Moving Average is slowly catching up to the current prices, currently at $37.50.

The two last impulsive moves (black arrows on the chart) have happened at around 20 days after the 20-Day MA rejoined the growing prices, after momentum retracted back to neutral.

The higher probabilities are pointing towards a consolidation/small retracements to the trendline rather than an immediate break higher. Of course, anything can happen.

Silver 4H Chart

Silver Daily Chart, July 24 2025 – Source: TradingView

Looking at the immediate price action, there are still some probabilities of an upside breakout, however a strong move higher on good volume with a daily close above the 39.51 previous highs would be necessary to up these odds (a simple retest won't do it for now).

If a retracement lower happens, the consolidation has a high chance to hold between 37.50 (2012 Support) and 39.50 (Current resistance), particularly as these levels coincide with the May upwards trendline.

If buyers maintain the prices above $39 throughout the end of the week, the odds of an upside breakout increase strongly

Support Levels:

- Immediate intraday support 146.37 and 30m MA 50

- 146.00 Pivot Zone (+/- 100 pips)

- Overnight lows 145.85

- Main Daily Support 142.00 region

Resistance Levels:

- Resistance $39 to $39.5

- 39.51 last swing highs

- $40.50 to $41 potential Resistance at ATH and top of Rising Channel

A look back to the 2011 Silver chart

Silver 2011 Daily Chart (all-year) – Source: TradingView

It's interesting to look back at past performances especially when assets or financial products come back to previous historic levels.

Spot the levels of major reactions on this chart, this could be interesting to watch if Silver reaches similar prices

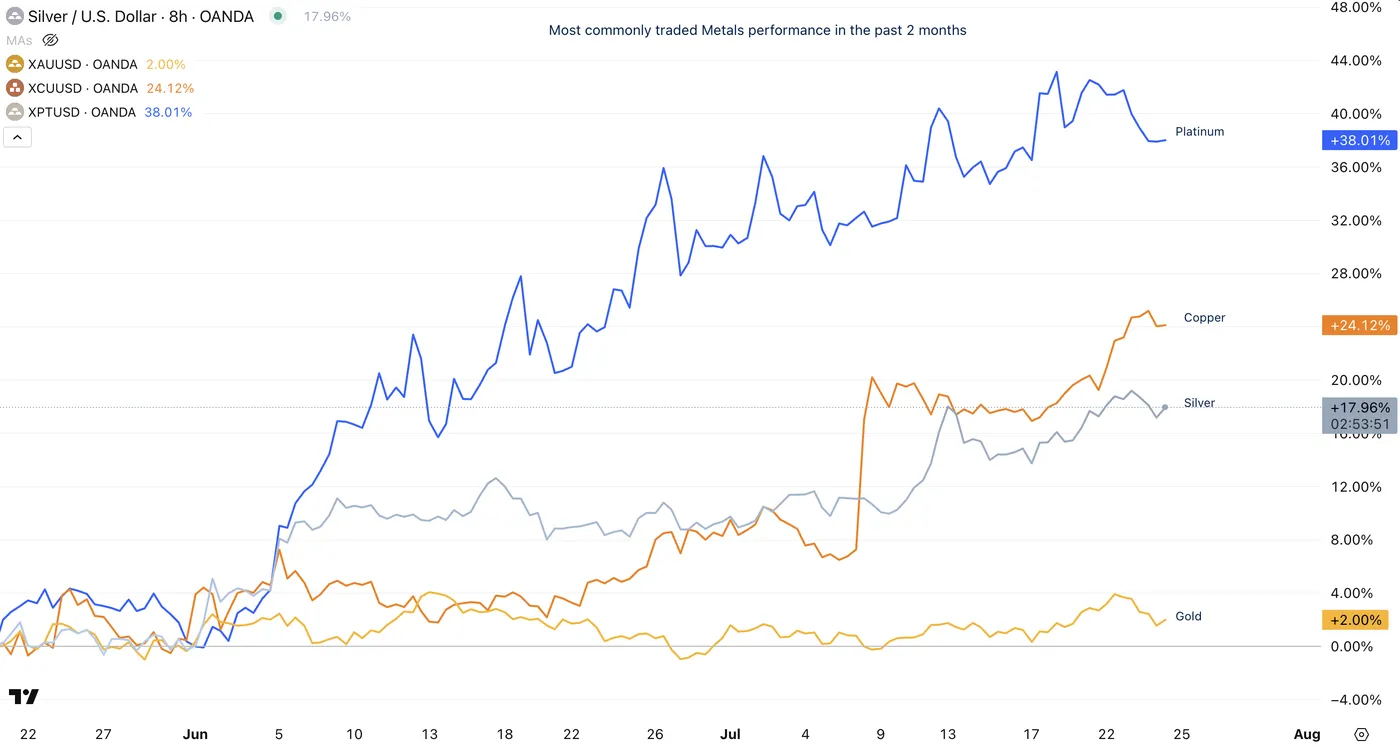

Most commonly traded Metals performance since May 2025

Metals comparative performance since the past 2 months, July 2025 – Source: TradingView

Metals are ongoing a mighty move higher, similar to what happened between 2008 and 2011.

Higher deficits seem not to have an end, and except for surprising rate hikes (unexpected for now), there doesn’t seem to be many reasons for metals to retrace essentially

(except for a sudden cancelling of tariffs, substantially low odds of this happening.)

Safe Trades!

Tokyo CPI core slows to 2.9%, but stays elevated

Tokyo’s core CPI (ex-fresh food) eased slightly from 3.1% to 2.9% yoy in July, coming in just below expectations of 3.0% yoy, but still notably above the BoJ’s 2% target.

Headline inflation also slowed from 3.1% yoy to 2.9% yoy. Core-core measure—excluding fresh food and energy—held steady at 3.1%. The stickiness in core-core inflation highlights persistent underlying price pressures.

The figures will feed into the BoJ’s upcoming July 30–31 policy meeting, where the board is widely expected to upgrade its inflation forecast for the current fiscal year. While the data alone may not push the BoJ to act immediately, it strengthens the case for further normalization as inflation remains well above target.

Narrow Path-Dependence

RBA minutes and Governor’s Anika speech clarify forward view. But the near-term forward path again seems to come down to small differences in outcomes for trimmed mean inflation versus expectations.

- RBA Monetary Policy Board (MPB) minutes and Governor’s Anika Foundation speech this week provide additional colour on the MPB’s split decision to keep rates on hold. The minutes gave the views of both members who voted to hold and members who voted to cut a good airing.

- The RBA’s view of productivity and supply-side issues is evolving and likely to continue to do so, with more internal work going on ahead of the August meeting and Statement on Monetary Policy. There are some important nuances and intellectual traps in this debate, though. Path-dependence can become a factor: tight labour markets might draw more workers in, making them more integrated into the labour market and boosting labour supply in the longer run.

- Since no single MPB member can front-run the decision of the whole Board, future inter-meeting communication is unlikely to endorse or push back against market pricing. This implies that markets will be surprised more often than in countries like the United States, where the central bank puts more weight on avoiding surprising the market. This approach should not, however, rule out making the RBA’s own interpretation of the data or its analytical models clearer when misconceptions arise.

This week’s minutes and Anika Foundation speech provided plenty to consider about how the RBA is seeing the economy. Inflation has come down significantly, which was welcomed. Unlike many other economies, this has not been at the expense of significantly higher unemployment. (For the technically minded, this means the ‘sacrifice ratio’ has been low.) While the Governor stopped short of claiming vindication, the contrast with other peer economics such as Canada and New Zealand did highlight the role of the RBA Board’s strategy to raise the policy rate by a bit less than in those other countries. Still, the MPB clearly remains nervous about inflation and some members want to see actual data to support their expectation that it is still declining towards 2½%, the midpoint of the RBA’s 2–3% target range. For this reason, we cannot lock in the cash rate cut in August just yet. We do, however, think it is the most likely outcome, especially if the quarterly inflation numbers come in as we expect.

Supply, productivity and path-dependence: the plot thickens

Unsurprisingly given the government’s upcoming roundtable, productivity received plenty of attention in the minutes, speech and Q&A. The minutes acknowledged that the expansion of the non-market sector and declining mining sector output had contributed to developments recently. The Governor noted that the staff are doing more work on productivity ahead of the August SMP. It is not clear which way this will go. We know that much of Australia’s living standards challenge stems from the fact that the free kick from rising minerals prices is no longer occurring. This would be true even if productivity growth were robust: when one factor is no longer boosting living standards, something else must adjust to make up the difference.

Concerns about productivity relate to the supply side of the economy. The Governor’s speech acknowledged that much of the surge in inflation following the pandemic stemmed from supply shocks. This is, incidentally, quite an evolution from the RBA’s assessment in late 2023 that inflation was becoming ‘increasingly homegrown and demand driven’. While these supply shocks were more drawn out than some observers initially expected, they did eventually subside. Monetary policy can mostly look through this kind of inflation as long as inflation expectations remain anchored.

But strong demand was also a factor. This was especially an issue in the United States, where fiscal policy remained very expansionary even after the disruptions of the pandemic had passed. The issue was less pronounced in Australia, but the exceptional stimulus during the pandemic and the surge in population when the borders reopened did play a role. (The RBA also today released some interesting findings on the latter.) The differing experiences of economies stemming from different fiscal responses highlights why it is so important that the methods central banks use to disentangle supply and demand shocks are appropriate, and do not fall foul of the ‘other fruit problem’.

More broadly, in the speech Q&A, the Governor acknowledged that weak productivity and weak supply did not necessarily imply anything for demand and so monetary policy. While that clears up any misconceptions that weak productivity growth is necessarily a reason to keep monetary policy tight – a welcome realisation – there are some important nuances here.

In particular, the Governor floated the idea that slow demand growth had less to do with tight policy than with supply being weak. We should not make too much of an off-the-cuff answer in a post-speech Q&A: it’s hard to get all the nuances into a short answer when there is a queue of other people wanting to ask questions. But this does raise the question of which way causation runs, and whether strong demand might in fact induce greater supply or weak demand weigh on supply. If so, tight monetary policy when both demand and supply are weak looks even less defensible.

The difficulty with this line of argument becomes clearer when comparing this discussion with the Governor’s answer to another question, about the labour market. There, Governor Bullock referenced a Bulletin article published the same day showing that the increase in labour force participation since the pandemic had not been a drag on productivity. The additional workers were not so new and green that they reduced the overall quality of the workforce. (This should not be a surprise: much of the increase in participation came from older workers just not retiring, and women returning to the paid workforce after stints demonstrating the executive management skills involved in wrangling small children.) It was a good thing, the Governor said, that a tight labour market had drawn more workers into employment. In this way, a tight labour market begat its own loosening by drawing in more supply. This kind of path dependence – known as ‘hysteresis’ to economists – is central to the understanding of why unemployment was so high in decades past but declined right across developed economies in the 2000s without spurring inflation. (This is the same mechanism that caused people to worry that the pandemic would cause ‘scarring’ in the labour market. There is a growing academic literature on this mechanism.)

In other words, the Governor was allowing for the possibility of some path-dependence in the labour market but had not quite translated this into an implication for the broader economy.

Communicating in many voices

In response to a question from another market economist, the Governor reiterated the point she made after the meeting: that these speeches cannot front-run the MPB meeting, because each member is just one member and does not speak for all. Explicitly taking issue with market pricing of future RBA moves is therefore not something we should expect to happen in future. In response to a media question, the Governor argued that surprising the market was neither a reason to do something or not do something. Put another way, the MPB will put no weight on whether its decision surprises the market. The Board will just try to do what it considers to be the right thing. (That ‘it considers’ language is a relatively recent addition to the final sentence of the media release and minutes, first included in the media release following the May meeting.)

That should not preclude, however, inter-meeting communication that hosed down a misconception in the market about how data is being interpreted. For example, the minutes clarified that models of the so-called ‘neutral rate’ were uncertain and not too much weight should be put on them or recent changes to some of them. It would not have been front-running the other MPB members to say in a speech, as the minutes did, that ‘public discussion of the stance of monetary policy had possibly overemphasised the inferences that could be drawn from these alternative models, especially for the near term’. (Looking back at my own note on the subject, I could have been blunter in my language, too, in my efforts to hose down this view.)

As we noted earlier in the week, though, the view of neutral becomes even more important – and fraught – the closer you get to where you think it is. MPB members who are still nervous about supply constraints and tight labour markets will want to tread slowly. As the Governor said in her speech, ‘[t]he Board continues to judge that a measured and gradual approach to monetary policy easing is appropriate’. That ‘measured and gradual’ language is a bit of an evolution from the ‘cautious and gradual’ language used in the minutes when discussing the views of the members who voted to hold rates in July, and the ‘move cautiously and predictably’ language of the May minutes. These small wording changes are likely to be simply different ways of saying the same thing: this is not a central bank that will rush policy easing

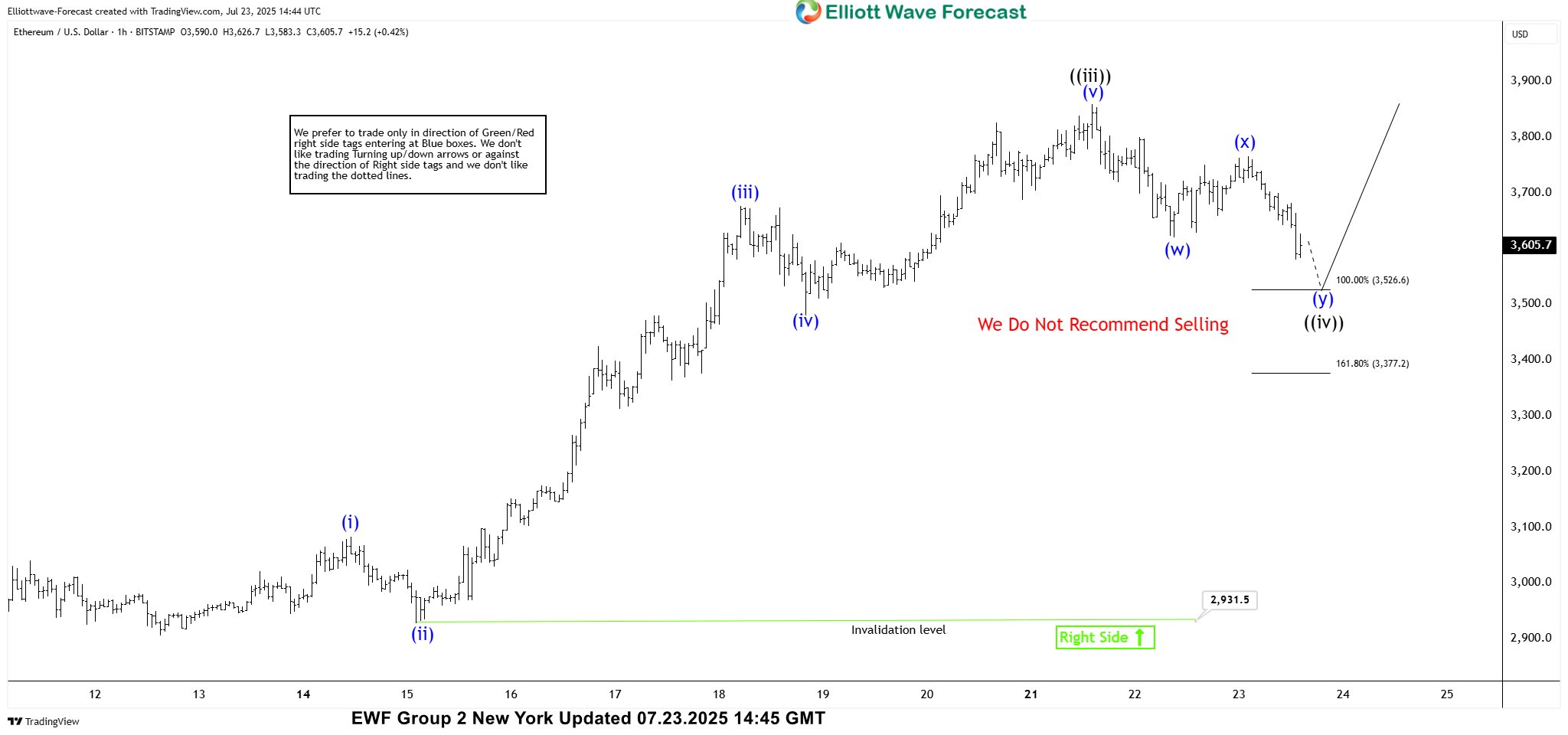

Ethereum (ETHUSD) Elliott Wave : Forecasting the Rally From Equal Legs Zone

Hello fellow traders. In this technical article, we are going to present Elliott Wave charts of Ethereum ETHUSD . As our members know, ETHUSD has been showing impulsive bullish sequences in the cycle from the 2,118.6 low, pointing to further strength ahead. We have been calling for a rally in ETHUSD since the beginning of July, based on the higher high bullish sequences the crypto was forming. Recently we got an intraday pullback labeled wave ((iv)), which landed right in the equal‑legs zone. In the following section, we’ll explain our Elliott Wave count and present the target area for wave ((v))

ETHUSD Elliott Wave 1 Hour Chart 07.23.2025

ETHUSD is currently doing wave ((iv)) black pull back. The correction appears incomplete at this stage. We anticipate further short-term weakness toward the Equal Legs area at 3,526.6-3,377.2. In that zone, we expect buyers to emerge and initiate another rally toward new highs. Therefore, we recommend avoiding short positions within this area.

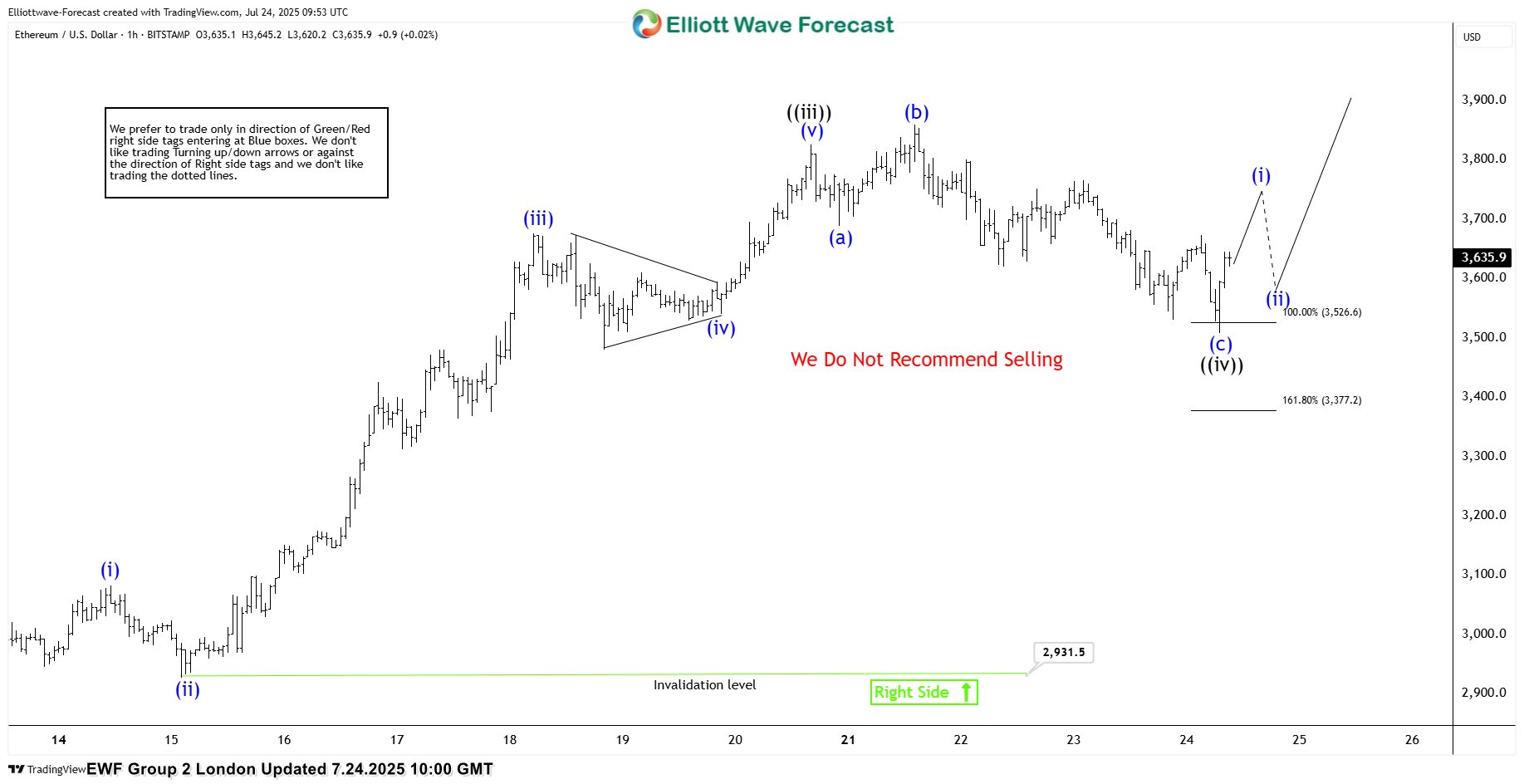

ETHUSD Elliott Wave 1 Hour Chart 07.24.2025

ETHUSD Elliott Wave 1 Hour Chart 07.24.2025

The price extended downward into the marked equal legs area, where ETHUSD found buyers as expected and has already shown a reaction. At this stage, we count the pullback as wave ((iv)), completed at the 3,510 low. As long as price remains above that level, we are likely in wave ((v)), targeting the 3,943–4,077 zone. Alternatively, if the 3,510 low is broken before a new high is made, we’ll likely see a deeper pullback. In that case, we’ll measure a new equal‑legs zone to identify the next buying area.

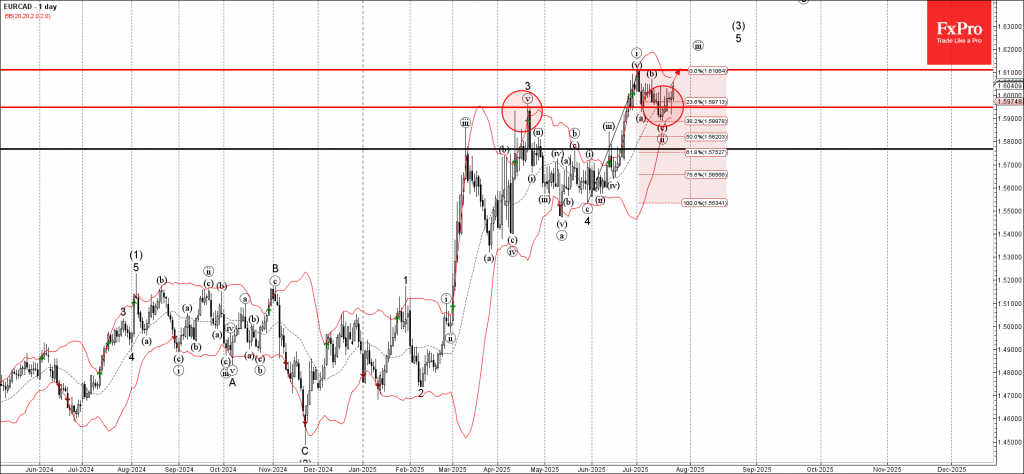

EURCAD Wave Analysis

EURCAD: ⬆️ Buy

- EURCAD reversed from support zone

- Likely to rise to resistance level 1.6100

EURCAD currency pair earlier reversed up from the support zone between the key support level 1.5950 (former monthly high from April), 20-day moving average and the 38.2% Fibonacci correction of the upward impulse from May.

The upward reversal from this support zone started the active minor impulse wave iii – which belongs to the intermediate impulse wave (3) from the end of 2024.

Given the overriding daily uptrend, EURCAD currency pair can be expected to rise to the next resistance level 1.6100 (which stopped the previous impulse wave i in June).

ECB Review – Exceptional Uncertainty, But Still in a Good Place

- ECB decided to leave policy rates unchanged at today's meeting as expected.

- Lagarde struck a positive tone in her economic assessment, although ECB still assess the balance of risk to growth as being tilted to the downside. Trade negotiations and data will likely determine whether to end the cutting cycle or not.

- We still pencil in a final 25bp cut at the September meeting, although risks are tilted towards a hold due to recent data improvement and positive trade news.

ECB decided as widely expected to leave policy rates unchanged at today's meeting, and did not provide any significant news compared to the June meeting. Economic data has overall been aligned with expectations, while underlying inflation continues to soften with wage growth coming lower. Today's statement noted that uncertainty remains 'exceptionally' high due to the US-EU trade dispute, making it unnecessary for the central bank to provide any new signals at this point. ECB still consider the risk for growth as tilted to the downside, but Lagarde repeated that monetary policy remains 'in a good place'. Today's decision to hold rates was unanimous according to President Lagarde.

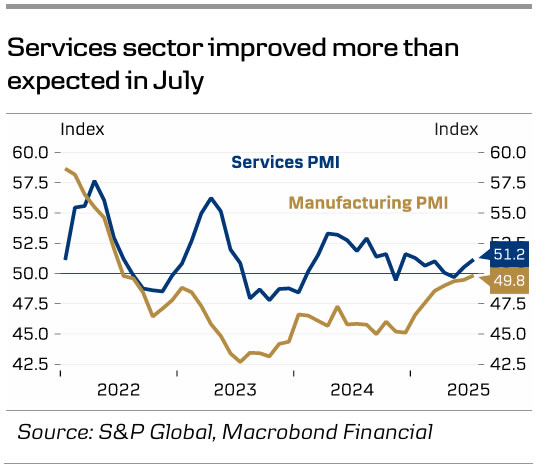

Lagarde struck an optimistic tone in her economic assessment. Particularly, she highlighted that the growth surprise in the first quarter of the year was not only due to Irish front-loading of exports to the US but also domestic demand (consumption and investments) being higher than expected. Hence, growth has been developing a little better than expected. She said that the June baseline projections still hold, when asked about the trade rumors of a 15% tariff rate on the EU. We also highlight that today's services PMI, which rose more than expected to 51.2, is another positive surprise. The weakening of the services sector seen in the past months has been a key argument for a cut in September by the ECB, but this improvement weakens that argument.

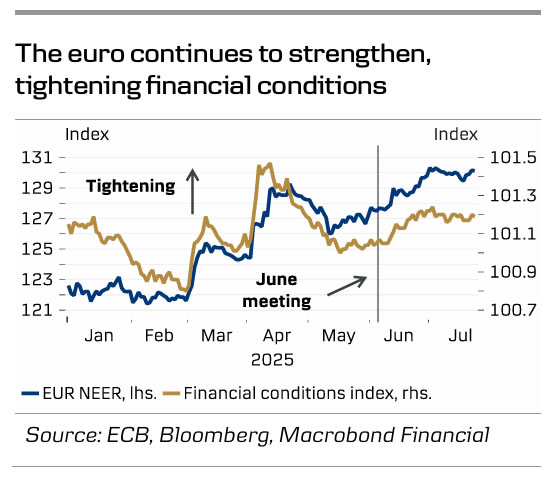

As expected, Lagarde abstained from providing any policy signals in terms of the recent strengthening of the euro. ECB is not targeting the exchange rate, but obviously it matters for the inflationary and economic outlook. But unlike previous comments from GC member De Guindos, Lagarde did not provide any clarity on when the euro appreciation will start complicating the current baseline forecast for inflation. Asked about the risk of inflation undershooting, Lagarde referred to 'three or four' governors who have expressed such concerns. However, the majority of the GC is not worried of the undershooting projection of inflation averaging 1.6% in 2026.

We continue to project a final cut in September, although we admit that both today's strengthening of the euro area services PMIs and the progression in US-EU trade talks have increased the likelihood of another hold. However, a lot can happen in the data coming in between now and the September meeting. We think that the combination of softening wage growth and underlying inflation is still likely to trigger a final 'insurance cut' - especially if trade uncertainty was to persist beyond August 1, which cannot be ruled out.

The slightly hawkish economic assessment from Lagarde at today's meeting triggered renewed upward pressure on EUR rates with the front rising 5bp the remarks. Markets are now only discounting rate cuts worth 7bp for September and 19bp by year-end. EUR/USD also rose 0.5% to 1.178 during the press conference.

USDJPY Re-enters Its Range After US-Japan Trade Deal—Will It Hold?

USDJPY hasn’t failed to generate some volatility in the past few weeks.

The pair, which had seen some steep up moves since the beginning of July, has been met by some sharp realities for its bulls.

Such Daily ranges are strong, and without weekly closes or a substantial fundamental change, Technicals indicate that they are expected to hold.

In today’s analysis, however, we will try to spot if anything from the new situation emerging in Japan has the potential to create a real upside breakout or if the range is deemed to continue.

Also we'll be monitoring the effect of the ISM PMI results on the pair – Services PMI Came in with a beat (55.2 vs 53.0 exp) and Manufacturing PMI missed (49.5 vs 52.5)

The immediate reaction is one of an USD selloff but this is subject to change

For a quick reminder, Japanese elections happened and the Ruling coalition (LDP + Komeito) lost its majority in the Upper House for the first time in a while.

The present government had a lot of influence on the dovish policies from the Bank of Japan, and with the ongoing situation, Japan's PM Ishiba might have to depart from his functions (he indicated he should stay to treat with the US Deals)

As a matter of fact, the Deal got reached yesterday, further confirming the newfound boost in the Yen that had already started to happen around the elections – There has been talks about the Deal not being implemented if "Trump is not happy" Scott Bessent said, but that would be a political mistake.

PM Ishiba pledged to make sure that the deal concludes.

Let's now take a look at the technicals to see if they indicate anything new to tilt the scales further.

Can we learn anything new from Client Positioning?

Trader Sentiment for USDJPY – July 24, OANDA Labs

Positioning isn't giving us much – normally providing us with a decent contrarian indicator and with a small tilt long, the assumption would be for some small downside correction, however the difference in positioning is not so big.

USDJPY Technical Analysis

Daily Chart

USDJPY Daily Chart, July 24 2025 – Source: TradingView

Momentum shut back to neutral after the past 3 sessions of US Dollar selloffs after rejecting the 200-Day Moving Average and participants will now be testing the Immediate 146.00 Pivot region.

Any downside breach would see the 50-Day MA as support (currently at 145.20), with no other key zone for buyers to step in before the 142.00 Main Daily support.

4H Chart

USDJPY 4H Chart, July 24 2025 – Source: TradingView

Sellers regained some strength in the past few sessions and will have to push below the Pivot zone mentioned just before to further maintain the range.

Some mean-reversion happened at the 4H-200 MA at 145.72 which will be a key barometer for immediate momentum (breach below, bearish – Holding above, bullish)

There is some ongoing selling after the PMI data but some decent volumes would be required to retest the overnight levels.

30m Chart

USDJPY 30M Chart, July 24 2025 – Source: TradingView

Looking closer to the 30m intraday timeframe, the rejection at the immediate downwards trendline after testing 146.87 highs in the morning session does shows slightly bearish momentum.

Update: The ongoing selling actually has been met by some buying momentum after a bounce on the 30M MA 50 – buyers will now look to test the highs of the day, monitor any breakout from the immediate trendline.

Monitor reactions at the 146.00 level – some key intraday levels to place on your charts:

Support Levels:

- Immediate intraday support 146.37 and 30m MA 50

- 146.00 Pivot Zone (+/- 100 pips)

- Overnight lows 145.85

- Main Daily Support 142.00 region

Resistance Levels:

- Morning swing high 146.87

- 30m MA 200 147.20

- May Range extremes 147.50 to 148.00

Safe Trades!

Business Activity in the UK is Under Pressure, as is Pound

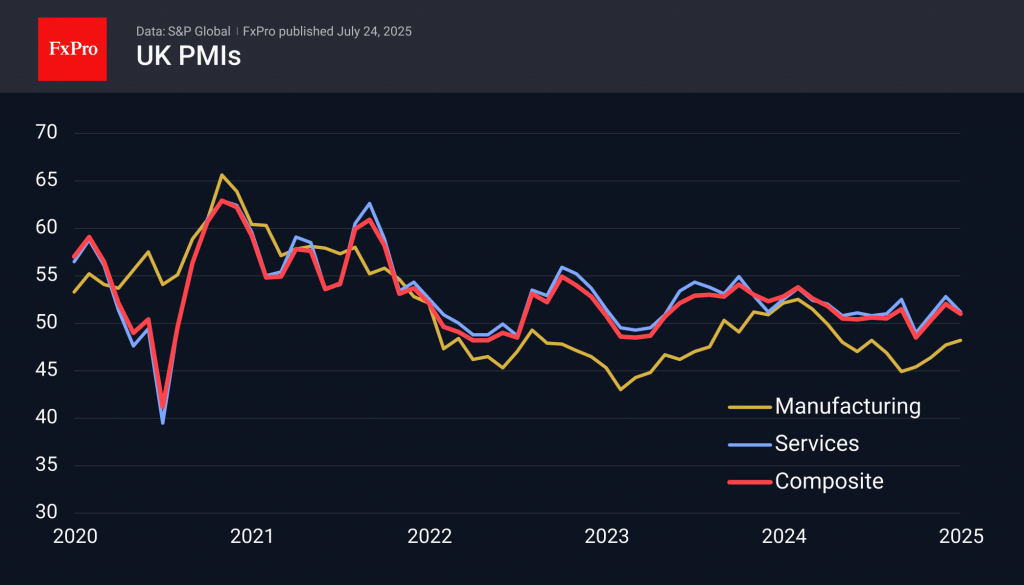

Preliminary estimates of PMI business activity indices showed a slowdown in the growth rate of the services sector, while manufacturing activity slowed slightly.

The manufacturing PMI for July, at 48.2, was better than the average forecast of 47.9 and the previous value of 47.7. However, the indicator has remained in decline (<50) for the last 10 months.

The services PMI fell to 51.2, showing a slowdown after June’s reading of 52.8.

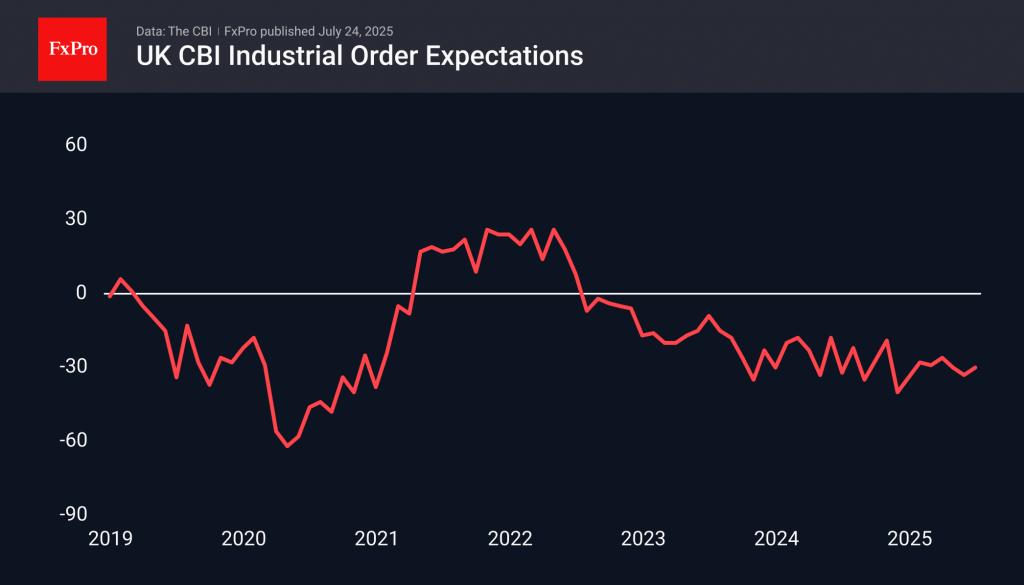

Another report, from the CBI, showed continued pessimism regarding industrial orders. The corresponding index stood at -30, remaining in contraction territory for the last three years.

All this indicates subdued economic activity in the UK. Although the Central Bank has been easing policy for a year now, this could potentially pave the way for further cuts in the key rate.

GBPUSD continued to decline against the background of this news, retesting the 50-day moving average. EURGBP has been trading near 0.8670, at the upper end of the range, since the end of 2023, and it looks like part of an upward drift within the 9-year range of 0.82-0.92.

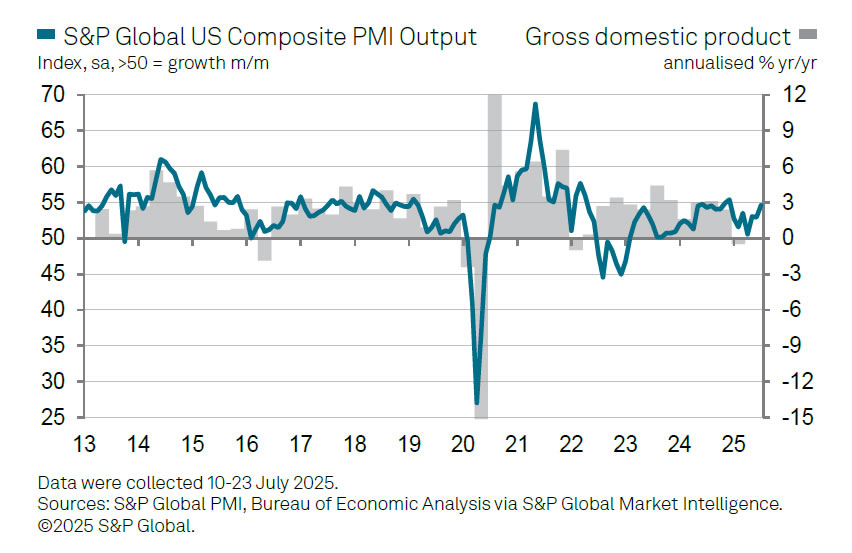

US PMI composite rises to 54.6, but growth uneven, inflation risks rise

US business activity surged in July, with Composite PMI jumping from 52.9 to 54.6, a 7-month high, driven by strength in services. PMI Services rose from 52.9 to 55.2, also a 7-month high. However, the manufacturing index dropped sharply from 52.9 to 49.5, slipping back into contraction for the first time this year.

S&P Global’s Chris Williamson noted the data signaled a sharp pickup in economic growth, with the survey pointing to a 2.3% annualized expansion in Q3, compared to 1.3% in Q2. But the rebound is uneven. Manufacturing is now dragging again, with the prior boost from tariff-related front-loading fading.

Business confidence weakened across both sectors, falling to one of the lowest levels in over two years. Tariff uncertainty and soft demand appear to be weighing heavily on forward-looking sentiment. Even in services, the outlook has dimmed despite the current strength in output.

Price pressures are also building. The survey highlighted one of the largest increases in selling prices in three years, with firms citing tariffs and rising labor costs as key drivers. This suggests upward pressure on consumer inflation will persist into the months ahead, keeping the Fed on edge despite soft spots in manufacturing.