Sample Category Title

ECB forecasters see no enduring disinflation from tariffs

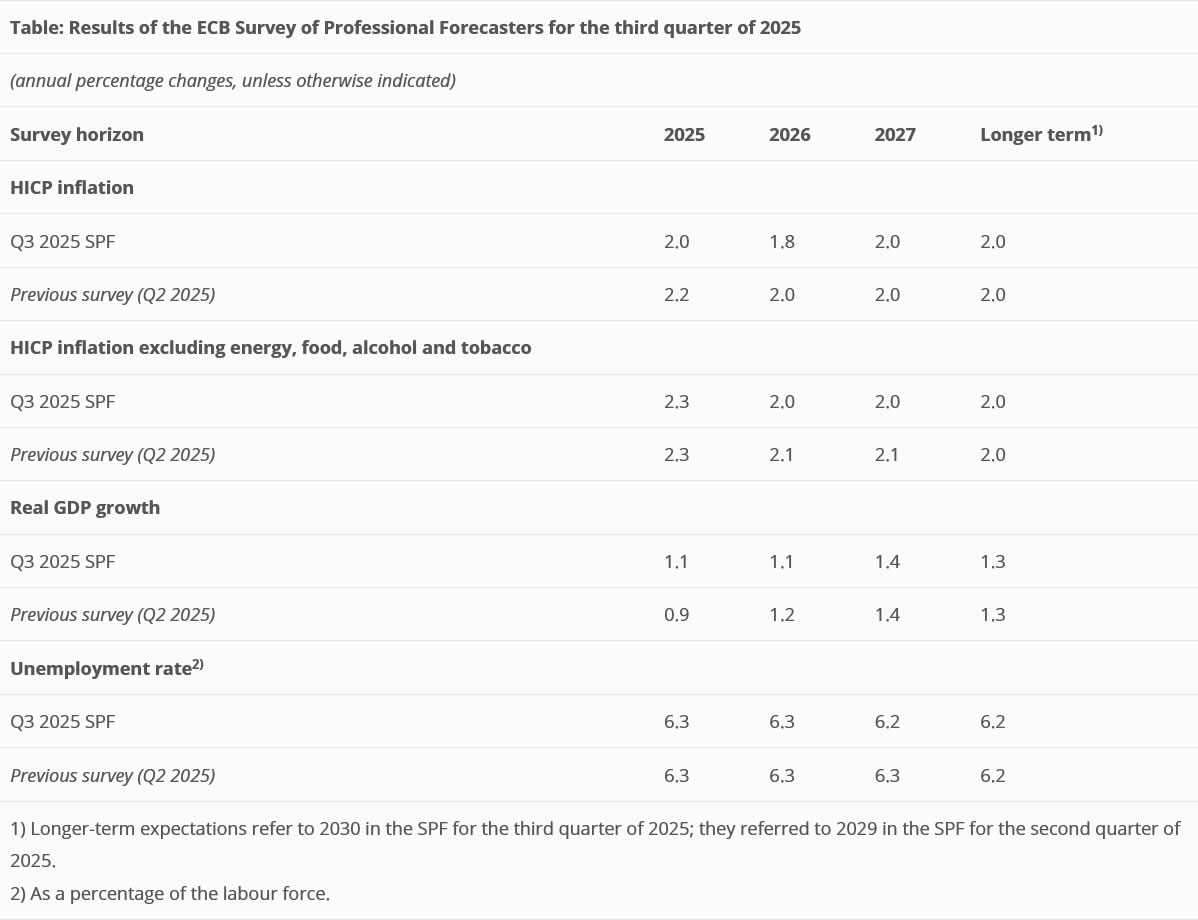

The ECB’s Q3 Survey of Professional Forecasters showed that headline inflation expectations have been revised down across the medium term. HICP inflation is now projected at 2.0% for 2025 (down from 2.2%) and 1.8% for 2026 (down from 2.0%), while 2027 remains unchanged at 2.0%. Core HICP inflation for 2025 is unchanged at 2.3%, but was revised down from 2.1% to 2.0% for both 2026 and 2027.

Respondents cited tariffs as having a small downward effect on inflation in the short term, subtracting roughly -0.06 percentage points from the HICP in both 2025 and 2026, but anticipated no lasting impact beyond that.

On growth, forecasters revised up their 2025 GDP forecast by 0.2 percentage points, trimmed 2026 by 0.1 points, and left 2027 unchanged at 1.4%.

German Ifo rises to 88.6, but recovery still sluggish

Germany’s Ifo Business Climate Index edged up from 88.4 to 88.6 in July, indicating only marginal improvement in business confidence. Current Assessment Index also ticked higher from 86.2 to 86.5, while Expectations Index held steady at 90.7. The Ifo Institute noted the recovery remains “sluggish,” with no clear acceleration in sight.

By industry, sentiment in manufacturing improved from -13.9 to -11.8, while construction also saw a modest rebound to -14.0. However, services weakened slightly to 2.7, and trade sentiment deteriorated again to -20.2.

ECB’s Kazaks sees pause to continue as inflation settles at 2%

Latvian ECB Governing Council member Martins Kazaks said there is now “value in holding rates at the current levels,” signaling that the era of obvious rate hikes or cuts is over. Speaking in an interview, the central banker stressed that a “steady-hand policy is appropriate,” suggesting little urgency for additional easing from the ECB in the near term.

Kazaks further emphasized that unless the Eurozone economy suffers a major blow, there’s limited justification for lowering interest rates. His stance comes after ECB President Christine Lagarde also struck a cautious tone following yesterday’s decision to keep the deposit rate unchanged at 2.00%.

Separately, Lithuanian Governing Council member Gediminas Šimkus noted “inflation is expected to stay at 2% level in the medium term.”

EURCAD Analysis: Bullish Sequence Extends From Blue Box

Hello traders. Here is another blue box blog post. In a post like this, we review some of the latest blue box trades that Elliottwave-Forecast members took. In this post, the spotlight will be on the EURCAD currency pair.

EURCAD is clearly in a bullish sequence from August 22, 2022, in the primary degree wave count. This cycle forms a 3-wave structure. Wave ((A)) ended in April 2023. Then, a wave ((B)) pullback followed and completed at the September 2023 low. From that low, the pair rallied and breached the wave ((A)) high, kickstarting wave ((C)).

As a result of that breach, a bullish sequence is now confirmed. Ideally, traders should buy dips in a bullish market and sell bounces in a bearish one. Wave (1) and (2) of ((C)) ended in November 2023 and November 2024, respectively. Then, wave (3) began from the November 2024 low.

Currently, wave (3) is nearing completion. In such a strong trend, there will be opportunities to buy from pullback extremes. The most recent was in mid-July 2025, marking the end of wave ((iv)) of 5 of (3). Wave ((C)) should ideally reach the 1.6400 equal leg for completion.

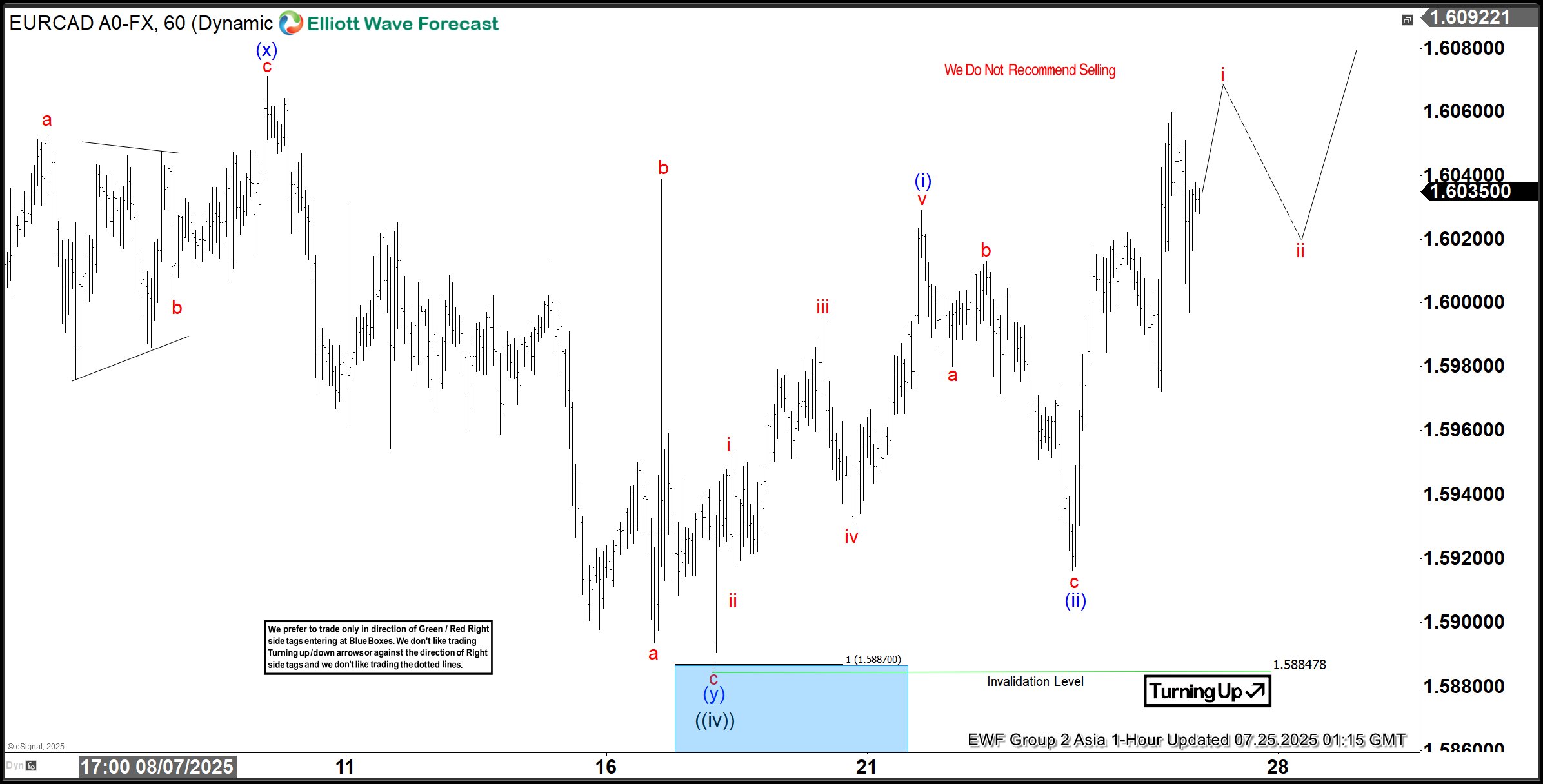

EURCAD Bullish Setup – 17th July 2025

On July 17, 2025, we shared the chart above with members. Earlier, we had identified a 7-swing pullback as wave ((iv)). In addition, we marked the 1.5886–1.5771 area as the blue box extreme. From that zone, we recommended a Long opportunity to members.

EURCAD Bullish Setup – 25th July 2025

On July 25, 2025, we shared the chart above with members during the Asia update. The H1 chart showed price hitting the blue box and bouncing off it immediately. Buyers have now closed half of their positions in profit and moved the rest to breakeven.

Looking ahead, price may either break into a new high within the April cycle or complete a 3-swing bounce from the blue box and turn lower for a deeper ((iv)) via a 15-swing pullback. In either scenario, we already have a trade plan. So, nothing catches us by surprise.

EURCAD has rallied over 150 pips from the blue box. If the setup plays out fully, members could gain around 270 pips in total profit.

Asia Stock Markets Pull Back as USD Rebounds, Hang Seng Index (Chart of the Day)

A seven-day rally in global equities paused during Thursday’s Asian session, following a mixed overnight performance on Wall Street. The Dow Jones Industrial Average and Russell 2000 slid 0.7% and 1.4%, respectively, while the S&P 500 and Nasdaq 100 pushed to fresh record highs, up 0.1% and 0.3%. Gains were driven by mega-cap tech names including Nvidia (+1.7%), Amazon (+1.7%), Microsoft (+1%), and Alphabet (+0.9%).

Asia’s longest winning streak since January ends

Asia-Pacific markets snapped their longest winning streak of the year. Hong Kong’s Hang Seng Index dropped 0.9% intraday after hitting a 3.5-year high, while Japan’s Nikkei 225 fell 0.9%, just shy of its all-time peak at 42,427. Singapore’s Straits Times Index also saw profit-taking, down 0.3% after a record-breaking 14-session rally.

Profit-taking and the US dollar rebound pressure Asian equities

Today’s Asian regional pullback likely reflects overbought conditions and a technical rebound in the US dollar after a four-day losing streak. The US dollar Index’s intraday firm tone is weighing on risk assets in Asia as traders reassess their short-term bullish momentum.

The worst performers against the US dollar at this time of writing are CAD (-0.17%), AUD (-0.16%), and GBP (-0.13%)

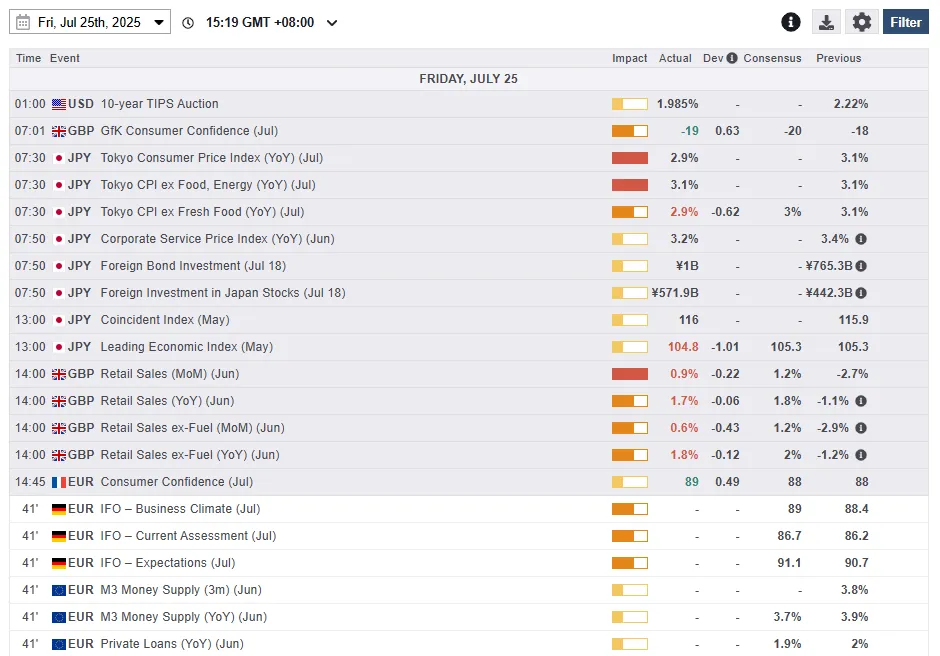

The intraday bounce seen in the US dollar is also reinforced by a slowdown in growth in Japan’s leading inflation gauge, where Tokyo’s core-core CPI (excluding food and energy) advanced at a slower pace of 2.9% y/y in July, a drop from 3.1% recorded in June.

Gold slips further as US dollar firms, support levels in focus

Gold (XAU/USD) declined for the third straight session, falling 0.4% intraday. The yellow metal is now approaching key support at its 20- and 50-day moving averages near US$3,333, amid headwinds from a strengthening US dollar.

Economic data releases

Fig 1: Key data for today’s Asia mid-session (Source: MarketPulse)

Chart of the day – Hang Seng Index at risk of minor corrective decline

Fig 2: Hong Kong 33 CFD Index minor & medium-term trends as of 25 July 2025 (Source: TradingView)

The price actions of the Hong Kong 33 CFD Index (a proxy of the Hang Seng Index futures) have rallied as expected. Recap our previous Chart of the day – Start of a potential impulsive bullish sequence for Hang Seng Index.

The two weeks of advancement have hit the upper boundary of a major ascending channel from the January 2024 low, now acting as an intermediate resistance at 25,750. The hourly RSI momentum indicator has just staged a bearish breakdown below a parallel ascending support from 19 June.

These observations suggest that bullish momentum has waned, and the Hong Kong 33 CFD Index is likely to stage a potential imminent minor corrective decline to retrace some of the gains seen from the prior rally from the 4 July 2025 low to the 24 July 2025 high (see Fig 2).

Watch the 25,750 key short-term pivotal resistance, and a break below 25,260 may reinforce the minor corrective decline sequence on the Hong Kong 33 CFD Index to expose the next intermediate support at 24,940/850.

On the flipside, a clearance above 25,750 revives the bullish tone for the continuation of the bullish impulsive up move sequence to seek out the next intermediate resistance at 26,030/26,220 (Fibonacci extension and medium-term swing high areas of 20/26 October 2021).

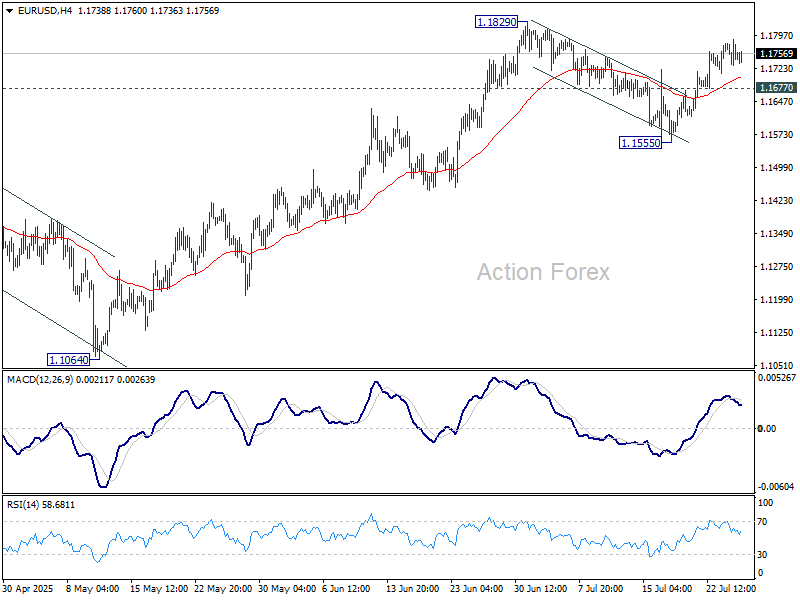

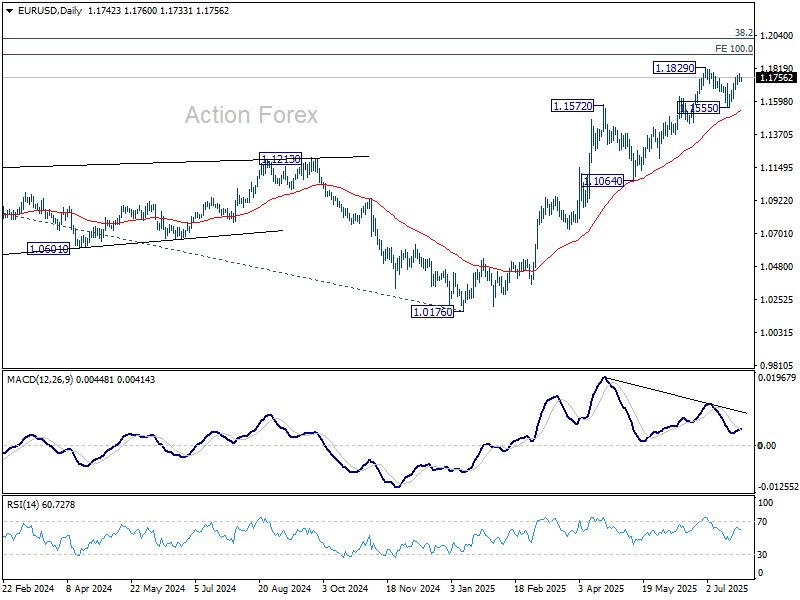

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1723; (P) 1.1756; (R1) 1.1781; More...

Intraday bias in EUR/USD stays mildly on the upside and rise from 1.1555 would extend to retest 1.1829 high. Firm break there will resume whole rally from 1.0176, and target 1.1916 projection level. However, break of 1.1677 will delay the bullish case, and turn intraday bias neutral, with more consolidations below 1.1829 first.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

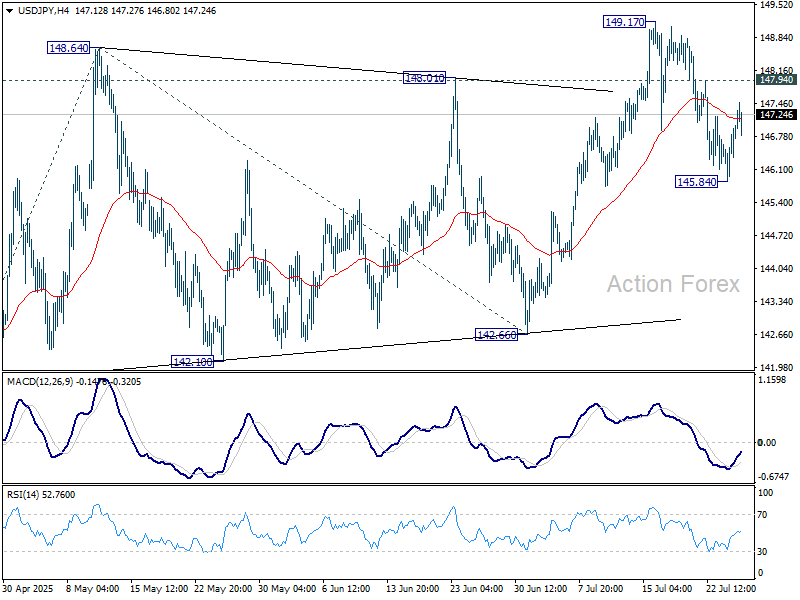

USD/JPY Daily Outlook

Daily Pivots: (S1) 146.23; (P) 146.63; (R1) 147.39; More...

Intraday bias in USD/JPY stays neutral. As long as 55 D EMA (now at 145.97) holds, further rally is still expected. On the upside, above 147.94 minor resistance will bring retest of 149.17. Firm break there will target 100% projection of 139.87 to 148.64 from 142.66 at 151.43. That is close to 61.8% retracement of 158.86 to 139.87 at 151.22. However, sustained trading below 55 D EMA will argue that the whole rebound from 139.87 might have completed and target 142.66 support for confirmation.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. in case of another fall.

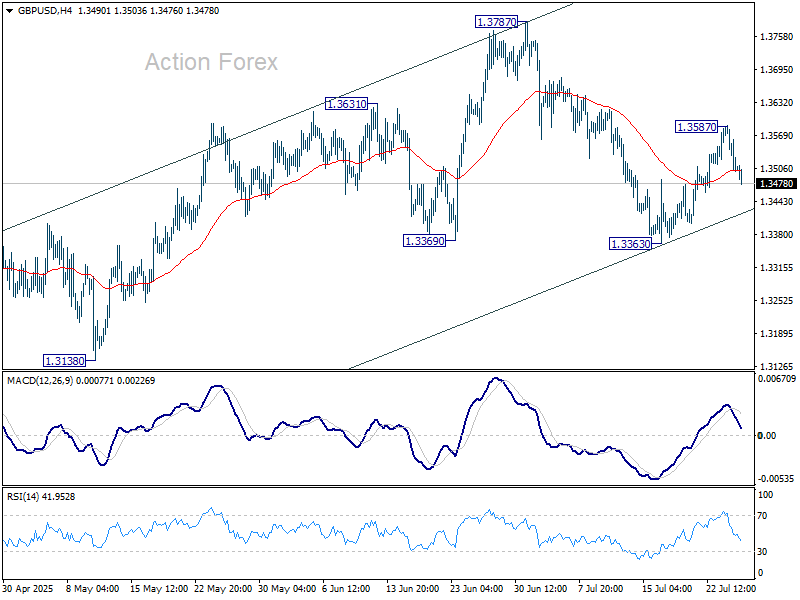

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3476; (P) 1.3533; (R1) 1.3562; More...

Intraday bias in GBP/USD stays neutral for the moment, and some consolidations would be seen. Further rise is expected as long as 1.3363 support holds. Above 1.3587 will turn bias back to the upside for retesting 1.3787 first. However, sustained break of 1.3363 will argue that it's already correcting the whole rally from 1.2099, and target 1.3206 resistance turned support.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3017) holds, even in case of deep pullback.

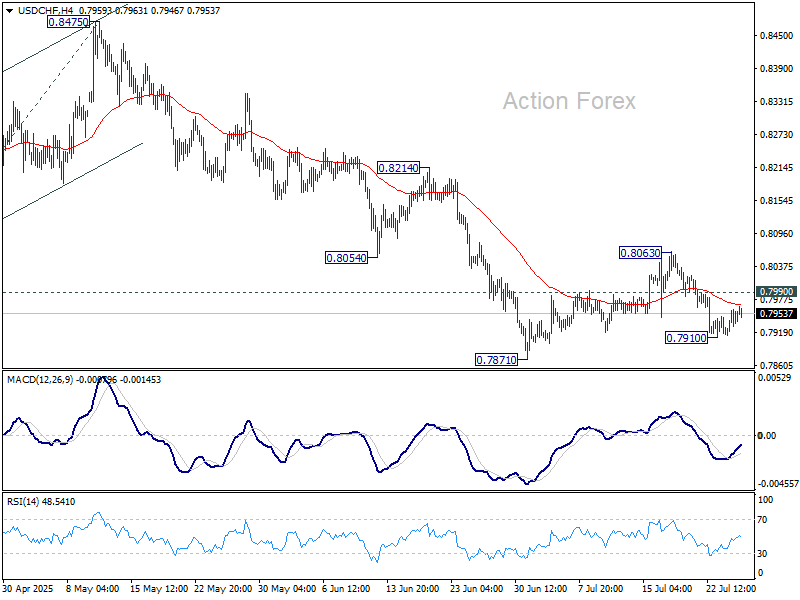

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7928; (P) 0.7944; (R1) 0.7973; More….

Intraday bias in USD/CHF remains neutral for the moment. On the downside, below 0.7910 will bring retest of 0.7871 support. Firm break there will resume larger down trend and target 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757. On the upside, break of 0.7990 minor resistance will bring stronger rebound to extend the corrective pattern from 0.7871.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

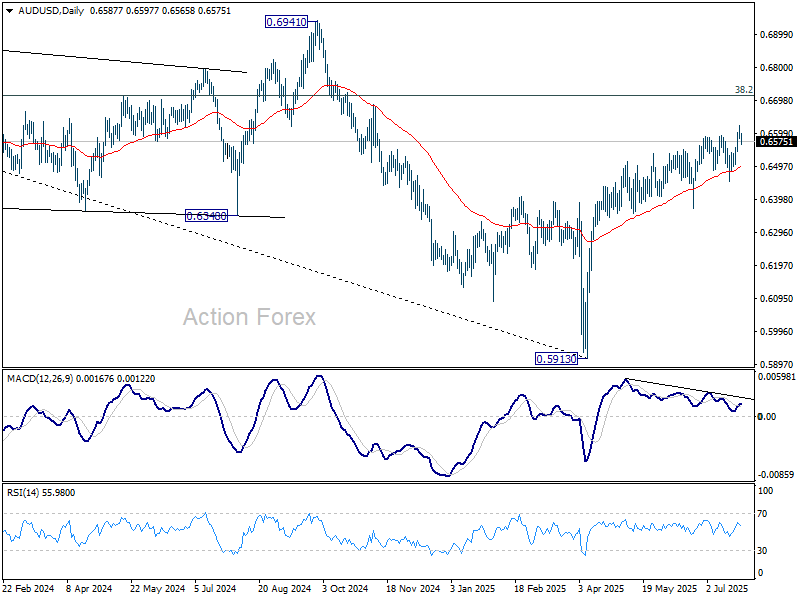

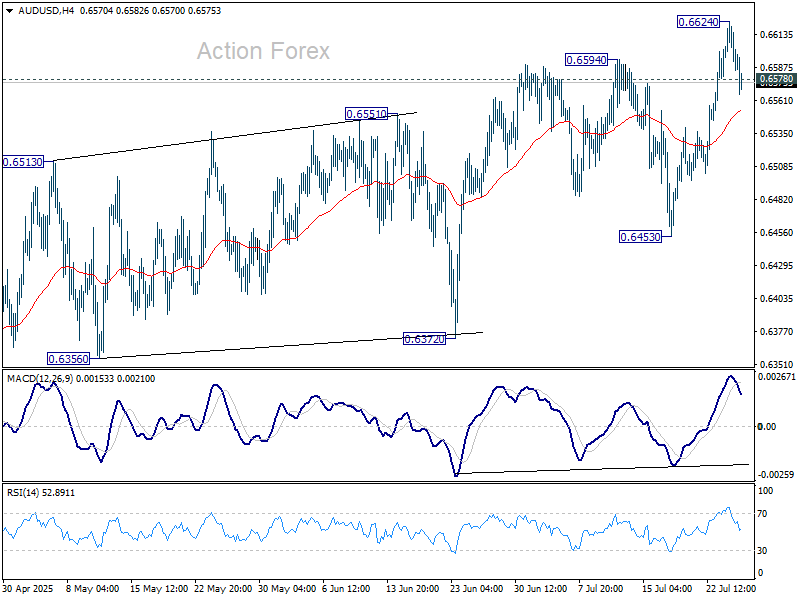

AUD/USD Daily Report

Daily Pivots: (S1) 0.6576; (P) 0.6601; (R1) 0.6615; More...

Intraday bias in AUD/USD is turned neutral first with current retreat. Some consolidations would be seen below 0.6624. But further rally is expected as long as 0.6453 support holds. Break of 0.6624 will resume the rise from 0.5913 towards 0.6713 fibonacci level.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).