Sample Category Title

The Weekly Bottom Line: Trade Deals Trickle in Ahead of August 1st

Canadian Highlights

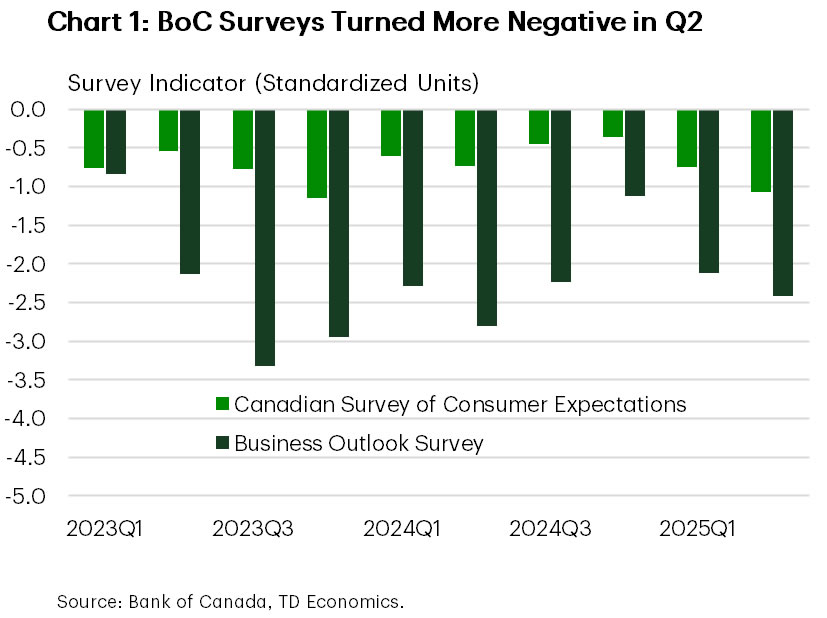

- This week offered a clearer picture of business and consumer sentiment. Both surveys turned more negative in Q2, with domestic demand expected to remain soft and investment outlook flashing a weak signal for Q3.

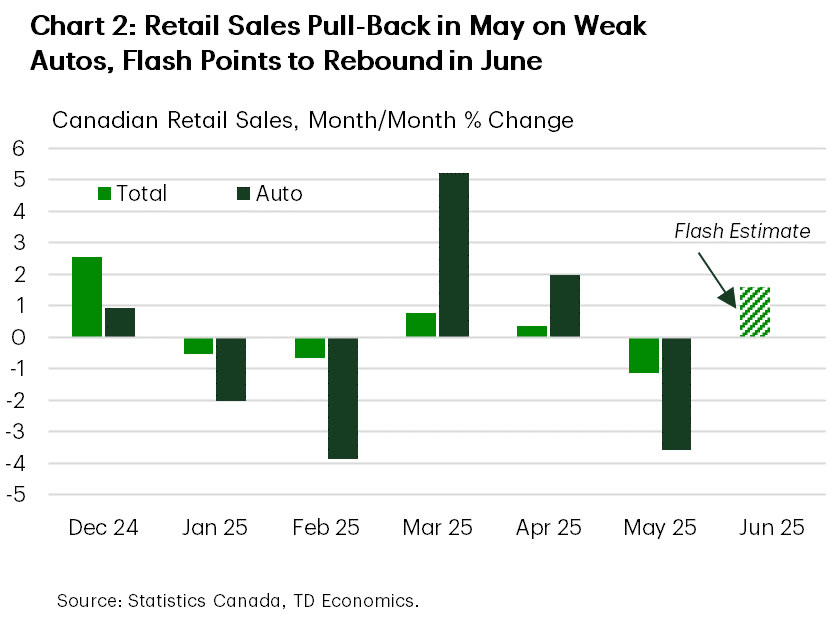

- The retail sales report showed a sharp pull-back in May spending, led by autos. The advance estimate for June suggests a rebound, likely keeping quarterly goods spending steady overall.

- Longer-term consumer inflation expectations ticked slightly higher, though are unlikely to cause much concern for the BoC. July’s rate decision is essentially locked in as a hold – the real question is whether the Bank stays on hold in September and beyond.

U.S. Highlights

- President Trump announced a few trade deals this week, most importantly with Japan. Under this “deal” Japanese imports will still face a 15% “reciprocal” tariff, which is lower than the 25% threatened in the past. The deal included a $550 billion Japanese investment package, but the details remain scarce.

- Existing home sales weakened more than expected in June, with the level of sales holding near GFC lows. However, median home prices rose 2.0% y/y, a slight improvement from the month prior.

Canada – Not Strong Enough to Cheer, Not Weak Enough to Cut

This week’s economic calendar wasn’t expected to move markets. Equity markets drifted higher on optimism around U.S. trade deals, while bond yields edged up modestly after falling for most of the week.

Instead, the data offered a clearer picture of business and consumer sentiment, along with a detailed look at May’s retail spending. Both the business and consumer surveys turned more negative in Q2, reversing the cautious optimism that had emerged late last year (Chart 1). However, the interviews, conducted from late April through May, came after the temporary relief was granted to CUSMA-compliant trade, which helped ease some pressure. Recession fears among firms and households ticked lower, and businesses reported modest improvement in some areas affected by trade.

Despite easing recession fears, the tone from businesses was far from upbeat. Domestic demand is expected to stay soft. Firms’ future sales expectations turned negative for the first time in a year. The outlook for exports sales improved for all but the manufacturing and auto-related sectors. The investment outlook, while slightly better than last quarter, remains well below average and just a quarter of where it stood in late 2024. Even then, most firms are sticking to routine maintenance rather than expanding capacity or improving productivity – a weak signal for the third quarter investment outlook.

On the consumer side, the Bank’s new sentiment index showed a second straight quarterly decline, reflecting slowing spending growth. That was confirmed by May’s retail sales report, which showed nominal spending down 1.1% and inflation-adjusted spending down 1.4% month-on-month. The sharp pull-back was led by auto sales, as the tariff-driven front-loading in March and April reversed course (Chart 2). Core sales, which excludes auto sales and receipts at gas stations, were flat in nominal and real terms. The flash estimate for June sales points to a rebound, which could keep quarterly goods spending steady overall. But services will determine the broader trajectory of personal consumption – and if consumers act on what they are saying in the survey, it will likely remain subdued.

Meanwhile, longer-term consumer inflation expectations ticked slightly higher, though are unlikely to cause much concern for the Bank of Canada. Firms also expect somewhat stronger input costs due to tariffs, though most say that they’ll absorb them through profit margins given weak demand. Services inflation remains the sticking point. According to CMHC, new rents are falling thanks to increased supply. However, existing rent inflation remains elevated, even as it has slowed relative to last year.

In short, the data doesn’t signal a collapse, but it doesn’t suggest strength either. This week’s releases don’t shift the dial for the Bank with July’s rate decision now essentially locked in – the employment report sealed a hold. The real question now is whether it stays on hold in September and beyond. For now, markets are only pricing in half a cut by year-end.

U.S. – Trade Deals Trickle in Ahead of August 1st

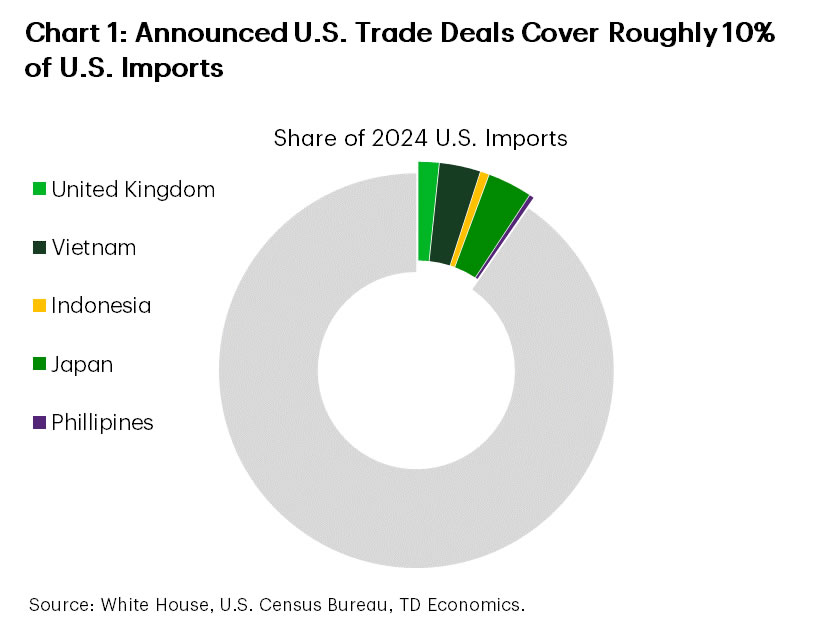

This fourth week of July was light on the data front, with only housing data on the docket. Trade developments continued to dominate the limelight, with trade “deals” announced with Japan, the Philippines and Indonesia. Progress on the trade front appeared to prop up financial markets, with the S&P 500 up 1.3% on the week.

U.S.-Japan goods trade is worth about $227 billion, so a trade deal is certainly a welcome development. Imports from Japan ($148.4 billion last year) will now face a 15% so-called reciprocal tariff, which is lower than the 25% that had been threatened in the past. The deal also reportedly included a $550 billion Japanese investment package, but the fine details on it remain scarce. Shares of Japanese carmakers rose on the news, but the largest American carmakers expressed concern that the deal could put them at a disadvantage. The trade deal with the Philippines received less attention. Imports from the Philippines will face a slightly higher tariff of 19%, slightly higher than the 17% announced on Liberation Day. This adds to a string of recent agreements, including those with the U.K., Vietnam and Indonesia (Chart 1). But the more important ones, such as those with China, Canada, Mexico and the EU, have yet to be reached.

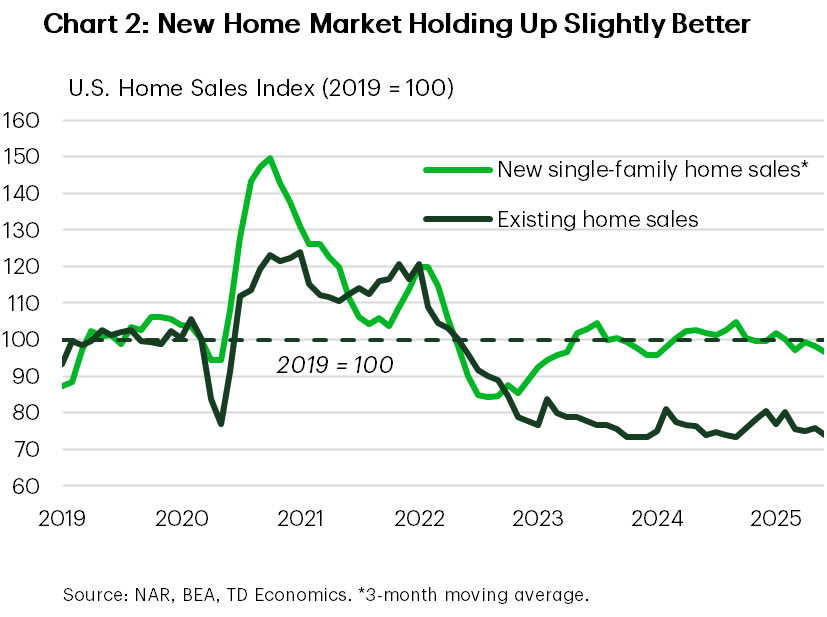

On the data front, the housing market continues to struggle under the weight of high mortgage rates. Existing home sales fell 2.7% m/m in June, coming in well-below expectations for a lighter pullback. Sales were down 8% from the end of last year and at a level of 3.93 million (seasonally adjusted annual rate) continued to hover near GFC lows. The months’ supply of inventory improved slightly, coming in at a seasonally adjusted 4.4 months from 4.3 in May. Amidst this backdrop, home price growth remained in the slow lane, but did see a modest improvement, rising to 2.0% year-on-year (y/y) from 1.6% in the month prior. With mortgage rates holding stubbornly near 7%, we’re unlikely to see a sustained turnaround in resale activity over the near-term. An improved interest rate backdrop expected later this year should help at the margin. High mortgage rates also continue to take a toll on the new home market, even as activity in this small corner of housing is holding up slightly better, with builder incentives likely providing some modest support (Chart 2).

Next week is sure to be more action packed. Aside from the potential for more trade deals to emerge ahead of Trump’s August 1st deadline, a host of important data reports are slated to be released next week. This includes second-quarter GDP, June’s PCE inflation, the July jobs report, and an FOMC rate-setting meeting. Market odds suggest the Fed is all but certain to keep the policy rate unchanged next week. That said, it appears that there will be at least one dissenter among the voters with Fed Gov. Waller recently urging for a July cut, while Fed Gov. Bowman has also expressed her openness to this. Signs of a growing divide within the Fed could lead to more volatility. In this vein, next week’s FOMC decision will be parsed over thoroughly for any of these signs and any potential clues as to how soon the committee could begin cutting rates, with September our current base case.

Weekly Economic & Financial Commentary: How to Finance President Trump’s Agenda?

Summary

United States: Housing Market Enters an Early Winter

- This week’s data highlighted the mounting challenges facing home buyers, sellers and builders. Both existing and new home sales came in below market expectations in June. High rates and economic uncertainty also continued to exert pressure on durable goods orders, which set the stage for a weaker equipment spending print in Q2.

- Next week: GDP (Wed.), Employment (Fri.), ISM Manufacturing (Fri.)

International: European Central Bank Pauses, and So Do Europe's Economies

- The European Central Bank (ECB) held its Deposit Rate steady at 2.00% this week. In the U.K., July PMI data showed modest improvement in the Eurozone. Meanwhile, data reinforced expectations for a 25 bps Bank of England rate cut in August. Finally, Turkey surprised markets with a larger-than-expected 300 bps cut to 43.00%.

- Next week: Australia CPI (Wed.), Bank of Canada Policy Rate (Wed.), Bank of Japan Policy Rate (Thu.)

Interest Rate Watch: How to Finance President Trump's Agenda?

- We do not expect any major policy shifts at the upcoming quarterly refunding announcement from the U.S. Treasury. In our view, Treasury's current coupon auction schedule is well-suited to meet its financing needs for the next few quarters, and any unexpected swings in the government's financing needs can be met by an expansion or contraction in the supply of Treasury bills.

Credit Market Insights: Lending Hesitation Remains but Financial Conditions Ease

- The July Beige Book revealed that credit markets remain subdued, with most Federal Reserve districts reporting flat or modest loan growth. Lending has been affected, as borrowers delay activity in response to elevated risk. Despite these headwinds, financial conditions have eased from their post-tariff lows, suggesting some resilience in the broader economy.

Topic of the Week: If Your Friends Slashed Rates, Wouldn't You?

- Slowing economic growth and softer inflation reports have led many major G10 central banks to ease monetary policy. The Federal Reserve isn't following the same pace, partly due to relatively firmer upside pressures amid more resilient growth and uncertainty over the inflationary impulse of higher tariffs.

Fed Preview: September Cut on the Horizon

- We expect the Fed to maintain its monetary policy unchanged in the July meeting, in line with consensus and market pricing.

- With no new economic projections, all eyes will be on Powell’s remarks. Unclear data will not allow the Fed to pre-commit, but Powell could verbally open up the door for a cut in the September meeting.

- Market is pricing around 16bp worth of cuts by September, and cumulative 43bp by year-end. Risks are skewed towards a modestly dovish reaction on Wednesday evening, but further out we think downside potential to USD rates is limited.

The Fed is inching towards resuming its cutting cycle but now is not yet the time. The June meeting was characterized by divided views across the FOMC – few participants did not see cutting rates this year as appropriate at all, while others favoured cutting already in July. Governor Waller has continued to signal that he could dissent in favour of a cut.

Since then, macro indicators have shifted in favour of further cuts, but data remains distorted. Higher realized and expected inflation were flagged as hawkish risks in the June minutes, but both have surprised to the downside since then. The July flash manufacturing PMI was weaker than expected, but the decline at least partly reflected slowdown in front-loading and firms awaiting clarity on tariffs.

The uncertain outlook for tariffs beyond 1st of August make pre-committing difficult at this stage, but we still think a cut in September looks likely. Needless to say, Powell will dodge any questions regarding political motivations for monetary policy changes.

As tariff payments continue to rise, firms will eventually have to either start passing through the costs to higher prices or look for ways to cut costs elsewhere. While we do pencil in accelerating goods and food inflation towards the fall, we are more concerned with the risk of tariffs causing weaker labour markets, than persistent inflation.

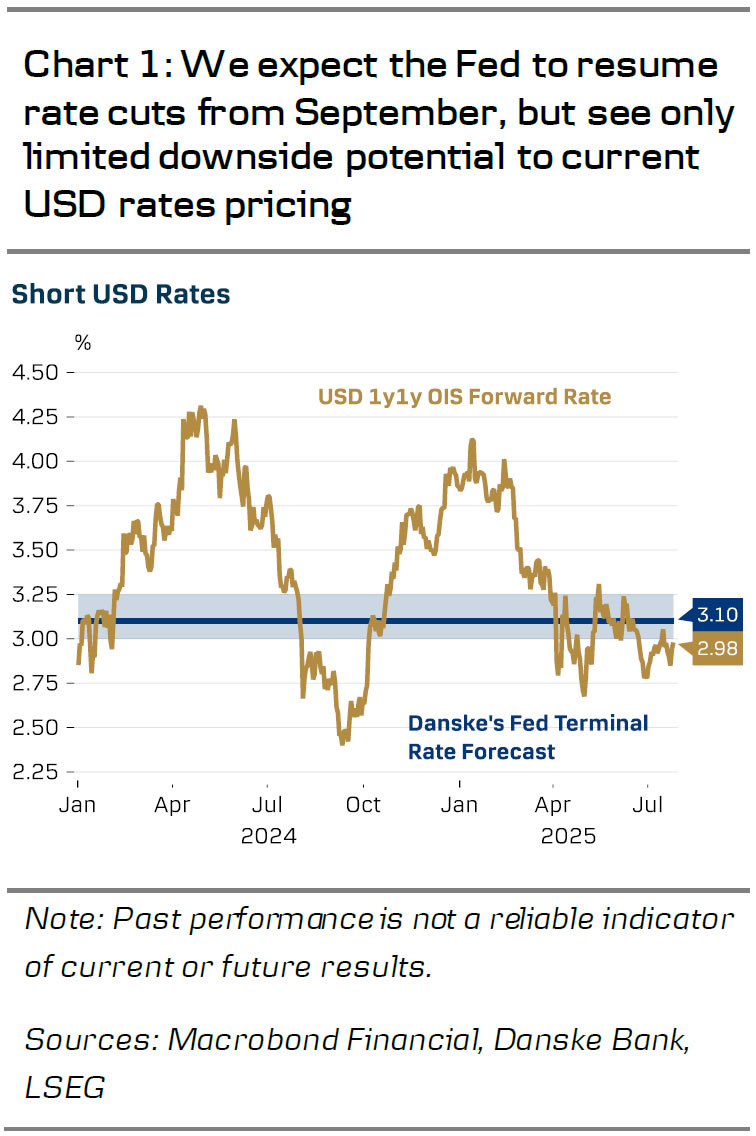

Beyond September, we pencil in quarterly 25bp reductions until the Fed Funds Rate target reaches 3.00-3.25% in September of 2026. Risks around the outlook are balanced in our view. We can easily sketch a scenario, where the Fed ends up cutting in every meeting after September, if macro data begins to undershoot expectations. But on the other hand, the renewed fiscal support from the start of 2026 could also ease the need for further cuts.

Altogether, we think the downside potential to USD rates is limited from current level. In the short-end of the curve, market is pricing cumulative 43bp worth of cuts by the end of 2025 – slightly less than we forecast. But from 2026 onwards, the pricing is well aligned with our call. In the long-end, we think the recent decline in term premium is unlikely to last given the fiscal outlook. We forecast the 10y UST yield at 4.50% in 12M horizon.

We still forecast further weakening for the broad USD, and maintain our 12M EUR/USD target at 1.23. We think the persistent policy uncertainty and structurally slowing economic growth are likely to weigh on the attractiveness of USD denominated assets even if our relative rates view is more neutral for the cross.

Week Ahead – Fed Decides Ahead of NFP and Tariff Deadline – BoC and BoJ Meet Too

- Fed to hold rates, unlikely to bow to Trump’s pressure.

- US GDP, PCE and jobs reports eyed too as August 1 deadline looms.

- BoC and BoJ decisions, Eurozone and Australian CPI also in focus.

Fed to likely stay on pause, risk Trump’s wrath

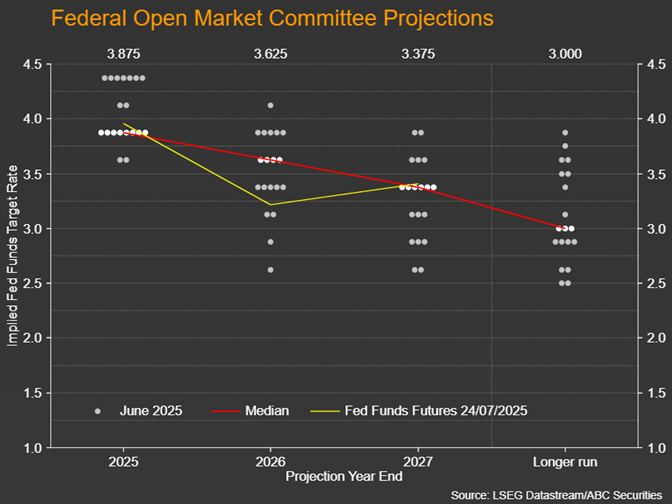

The Federal Reserve meets on Tuesday amid a cooling trade war and is widely expected to leave interest rates unchanged on Wednesday for the fifth time this year, even as President Trump relentlessly pressures the central bank to slash borrowing costs. But aside from the drama with the White House, the July meeting will be significant nevertheless, as a dovish tilt is possible, amid the doves within the Fed becoming more vocal. Not only that, but September is one meeting away and some kind of messaging will be necessary if a rate cut then is on the cards.

The latest dot plot and minutes of the June meeting revealed an almost 50-50 split among FOMC participants between those that prefer to lower rates sooner rather than later and those that are inclined to remain on pause for the foreseeable future. Not so long ago, there was growing talk that the Fed might surprise with a cut in July, but the subsequent data quashed the speculation.

CPI inflation measures edged up in June and there was a solid increase in nonfarm payrolls. Unfortunately for the Fed, the next NFP report isn’t due until two days after it meets, while the next inflation data – the PCE price indices – will be released the following day. This makes the July gathering a tricky one for Chair Jerome Powell, who faces a daily barrage of insults by Trump.

But Powell himself had left the door open to a July cut, amid lack of clarity about the strength of the economy and the inflationary effects of Trump’s tariffs, and his instincts may be right. Underneath the hood, the June jobs report wasn’t so strong as there was a notable slowdown in private sector employment. And with the number of trade deals being agreed finally gathering pace, the risk of a sharp jump in average import duties on August 1 has come down substantially.

Thus, the Fed is on track to resume its easing cycle in September as the majority of policymakers have been predicting. Flagging the likelihood of a rate cut in September while holding them steady for now is probably the best compromise Powell can achieve at this moment in time. This would unlikely be enough to satisfy his critics, but all the indications are that Trump is not currently planning on firing Powell – whether by upping the pressure on him to resign or finding legal grounds to do so such as using the costly renovations of the Fed headquarters building to allege misconduct.

All eyes on NFP, PCE and GDP reports

On the data front, it’s going to be a jam-packed agenda, as apart from the NFP and PCE inflation figures, there’s also the advance GDP report, as well as a slew of other releases.

First up on Tuesday are the S&P CoreLogic Case-Shiller 20-City Composite Home Price Index, the consumer confidence index for July and the JOLTS job openings for June. Pending home sales and the ADP employment change will follow on Wednesday, while on Thursday, Challenger Layoffs and the Chicago PMI for July will be the other second-tier releases.

All those indicators will be watched closely for wider clues on the health of the economy but are unlikely to attract as much attention as the week’s data highlights, the first of which is Wednesday’s advance GDP reading for the second quarter.

The jump in imports in the first quarter before higher tariffs kicked in was a big drag on GDP, which contracted by 0.5%. It’s expected to have rebounded by 2.5% in the June quarter as most tariffs were put on pause. Still, this data will be seen as somewhat outdated as investors and policymakers are more eager to see where the economy is headed.

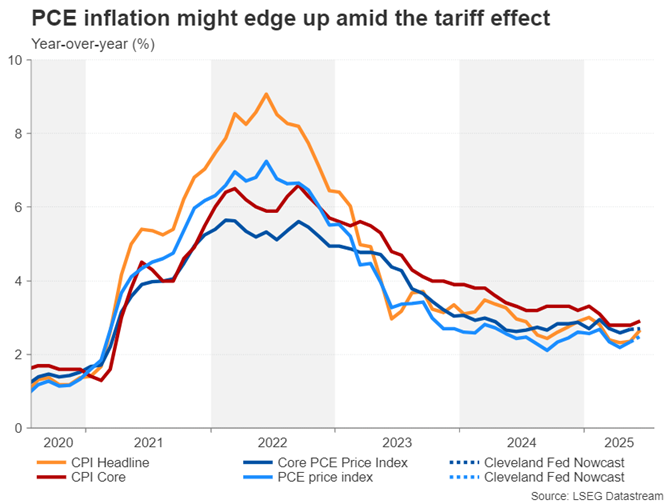

The Fed is worried about how much inflation will rise over the coming months while keeping one eye firmly on the labour market. The June CPI numbers already pointed to some price hikes due to higher tariffs. If Thursday’s PCE inflation readings do the same, particularly core PCE, then the Fed might even forego September, and this is why a 25-bps rate cut at that meeting is only two-thirds priced in.

The Cleveland Fed’s own Nowcast model isn’t predicting any fireworks, however. The core PCE price index is estimated to have stayed unchanged at 2.7% year-on-year in June, but headline PCE is forecast to have picked up to 2.5% from 2.3%.

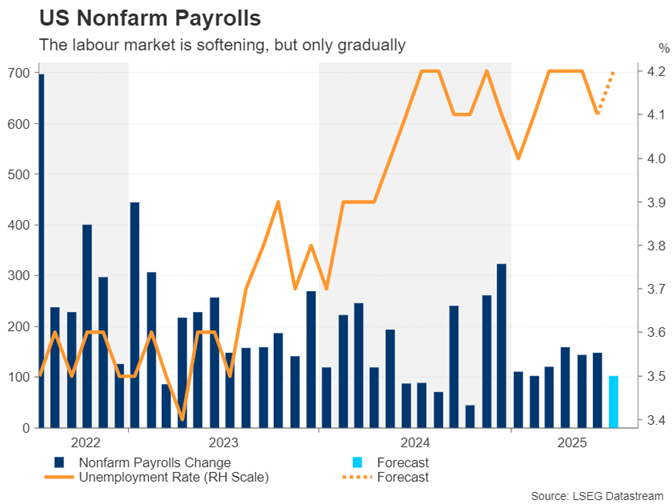

Potentially even more crucial will be the July payrolls numbers out on Friday. The headline print is expected at 102k, down from 147k in the prior month. The unemployment rate is projected to tick up to 4.2%, and growth in average hourly earnings to accelerate slightly to 0.3% month-on-month.

Also important on Friday will be the ISM manufacturing PMI, which is expected to improve from 49.0 in June to 49.6 in July.

Any weakness in the upcoming data would likely boost rate cut bets for September but investors are increasingly sceptical about the possibility of a third reduction in 2025 so the downside risks to the US dollar are somewhat limited.

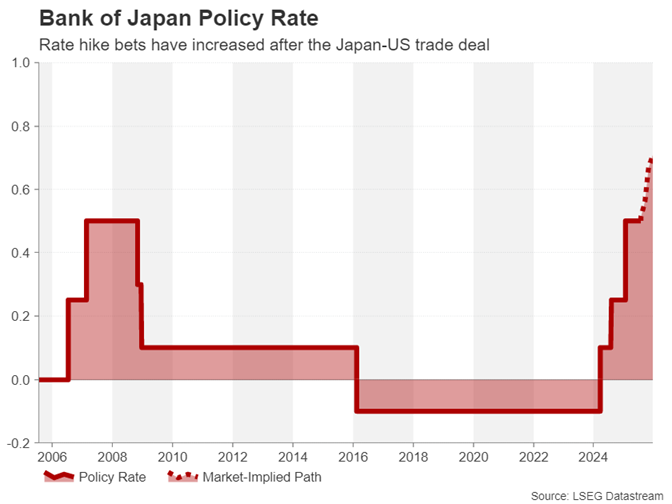

Will the BoJ talk up rate hike expectations?

If the greenback does come under greater selling pressure, it’s more likely to be down to the strength of other currencies, such as the yen, which received a leg up from the US-Japan trade agreement.

Whilst there’s a sizable risk that Japan’s economy will take a hit from this new deal, as it still leaves Japanese exporters worse off from where they were before the trade war, the end of the uncertainty does potentially pave the way for the Bank of Japan to restart its tightening campaign. The BoJ last hiked rates in January and following the deal, investors have ratcheted up their bets of another 25-bps increase in the policy rate by year end, helping the yen to recover from near the 150 level against the dollar.

For the July meeting, which takes place on Wednesday and Thursday, the odds of a policy change are near zero, although the Bank will publish its latest quarterly outlook report. Should policymakers revise up their forecasts for inflation and see reduced risks to growth, rate hike expectations could further intensify, boosting the yen.

In terms of data, preliminary industrial output for June is out on Thursday, along with retail sales for the same month.

BoC to stay on hold as Canada hopes to avert 35% tariffs

Before the Fed and Bank of Japan decisions, it will be the Bank of Canada’s turn on Wednesday to set rates. But the meeting could turn out to be a non-event as the BoC is not anticipated to announce any changes, keeping its overnight rate at 2.75%.

It’s been a tough few months for Canadians, least of all for BoC policymakers who’ve had to worry about both a resurgence in inflation and a recession as the country’s biggest trading partner is threatening tariffs of up to 35%. Although the steeper levy rate won’t apply to goods covered under the USMCA agreement, it could nevertheless cause significant disruption to trade between the two neighbouring countries, potentially pushing the economy into a recession.

According to the BoC’s latest outlook survey, businesses are a little less pessimistic than in the prior quarter, as the recent trade deals have boosted hopes that Trump and Prime Minister Mark Carney will be able to reach some kind of an agreement before August 1.

But with more than 70% of Canada’s exports destined for the United States, it’s probably too soon to rule out a recession. (Thursday’s monthly GDP reading will provide an update for May). At the same time, Canada’s retaliatory tariffs of 25% on certain US goods is pushing up prices domestically. Even before the onset of the trade war, underlying inflation in Canada began to head higher and this limits the scope for rate cuts should the economic picture deteriorate further.

For now, and in the absence of a trade deal announcement over the next few days, the BoC will likely maintain the same tone as in the June meeting, with the risks to the Canadian dollar being tilted sightly to the downside.

Eurozone data may fail to excite

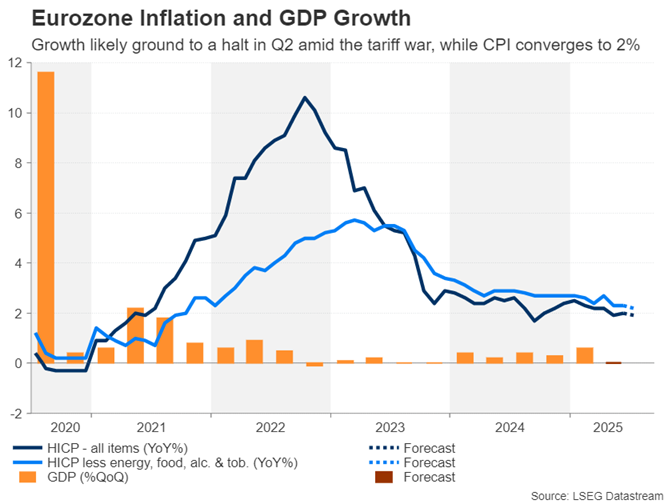

It’s not just Canada that’s in a rush to reach a trade agreement with the US as the European Union has also not struck a deal yet, although reports suggest that negotiators are closing in on one. The European Central Bank has already done its bit to safeguard the Eurozone economy from the trade war risks and decided to keep rates on hold in July for the first time in eight meetings, having halved the deposit rate to 2.0%.

Policymakers likely want to retain some firepower in case trade tensions with America escalate again as time is running out before the August 1 deadline. But assuming that a deal is agreed, it could be several months before the ECB cuts again, if at all. Hence, next week’s data may not spur much reaction in the euro.

The preliminary GDP estimates for the second quarter are due on Wednesday, followed by flash CPI numbers for July on Friday.

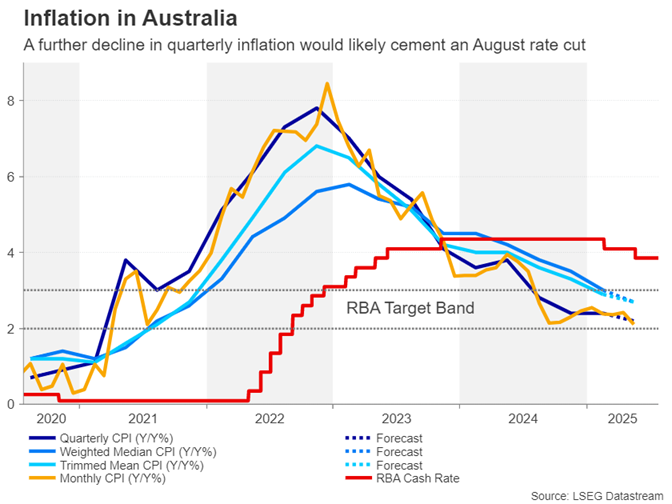

Will Australian CPI give RBA the green nod?

In Australia, quarterly CPI data could be crucial for the Reserve Bank of Australia’s next policy decision, something that Governor Michelle Bullock had referenced when justifying the surprise hold in July.

Australia’s statistics office won’t begin publishing a complete monthly CPI dataset until November. Until then, the RBA is putting more weight on the quarterly release than the experimental monthly reads.

The second quarter figures are due on Wednesday when the RBA will be hoping to see a further moderation in the core CPI measures. As for headline CPI, it dipped to 2.1% in May, but the RBA wants to see a similar decline in the quarterly print before trimming rates again.

A rate cut at the RBA’s next meeting in August is not fully priced in so the Australian dollar could extend its recent gains if the CPI figures are stronger than expected, further denting easing bets. Meanwhile, traders will also be watching Chinese manufacturing PMI due on Thursday.

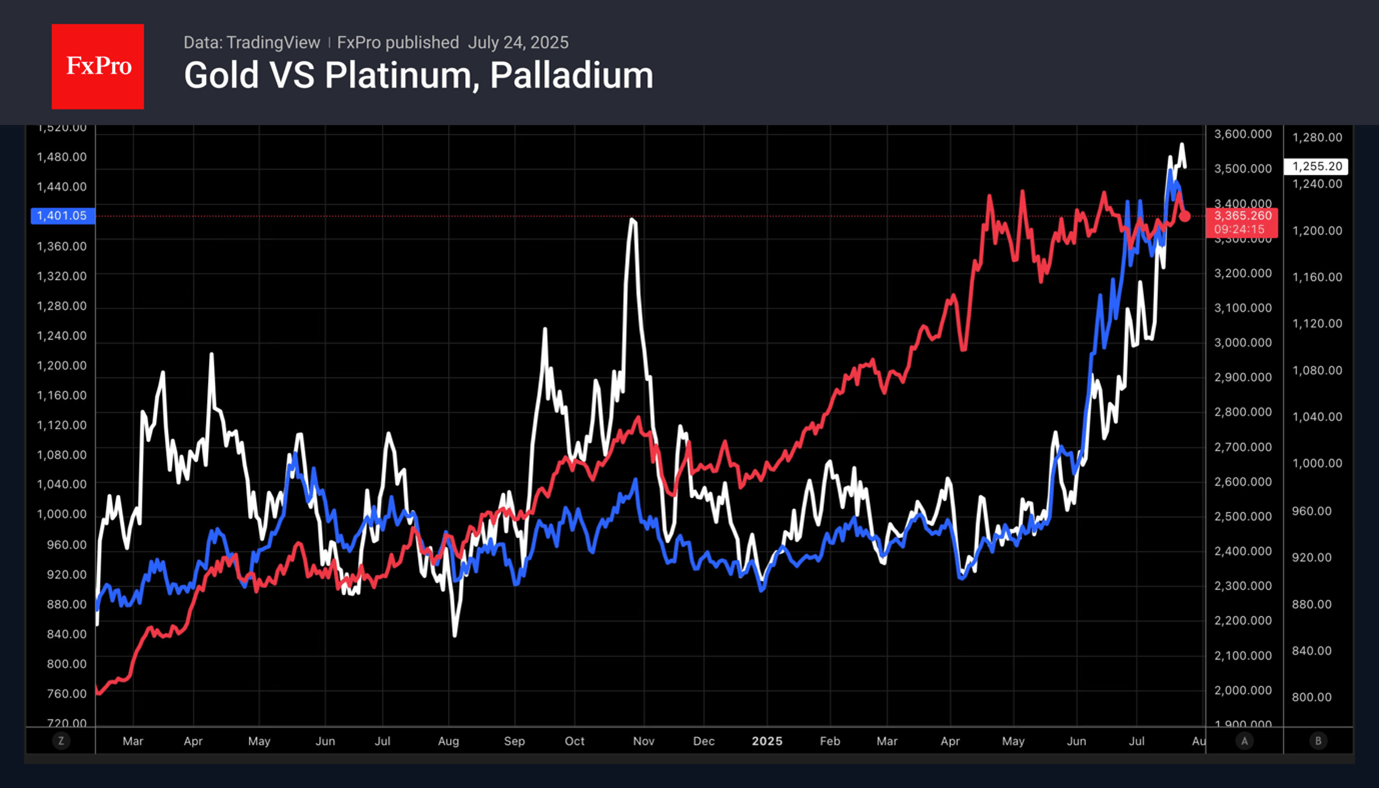

Retreating from the Ceiling Again, Gold Risks Correction

Concerns about the trade war between the US and the European Union and the retreat of platinum group metals allowed gold to break above the upper limit of the medium-term consolidation range of $3250-3400 per ounce. However, the White House’s trade agreement with Japan and the reduction of import duties on Japanese goods brought gold back to the centre of the latest consolidation range.

Platinum and palladium, which showed impressive results in 2025, were the main beneficiaries of rumours that gold was overbought. Investors diversified their portfolios in favour of less expensive metals. However, due to the high share of demand from the automotive industry, platinum group metals are highly sensitive to tariffs. A reduction in import duties could restore the upward trends and put pressure on gold against the background of renewed capital outflows.

The leader of the precious metals sector is also vulnerable due to expectations of a reduction in the federal funds rate. The futures market forecasts 1-2 acts of monetary expansion in 2025 and is confident of three in 2026. The sooner the Fed begins to ease monetary policy, the better for gold.

At the same time, gold failed to consolidate above $3,450 for the fourth time since April. On the one hand, this is a sign of abundant supply at highs and the desire of players to close their long positions in gold, looking for alternatives. On the other hand, gold has been benefiting from strong catalysts this year: it was the first of the popular exchange-traded instruments to return to new highs after the shock of Trump’s tariffs, and in recent weeks it has been rising in line with the recovery in risk appetite.

By the end of the week, the price of gold had fallen back to its 50-day moving average. A sharp drop below this line in the new week will be an important signal of a transition from consolidation to correction — roughly what we are seeing with Bitcoin at the end of this week. If gold moves into a correction, there is potential for a rapid move to $3,150 or even $3,050. The upper target is the area of highs before the ‘liberation day’ and 61.8% of the rally since the end of last year. The lower target is already close to half of this growth and not far from the 200-day moving average.

Bank of Canada Poised to Hold Rates Steady, Unveil New Projections

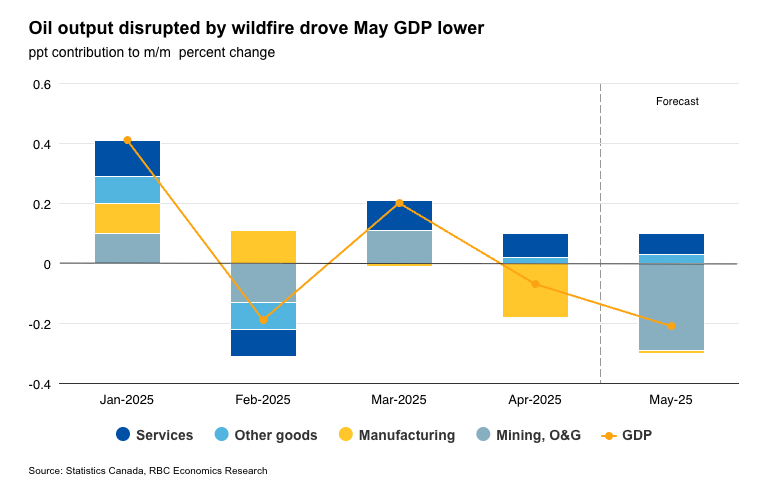

We’re expecting the Bank of Canada to leave the overnight rate unchanged again on Wednesday, while Thursday’s May’s gross domestic product (GDP) report for Canada will likely show a larger 0.2% decline, though most of it is expected to have reversed in June.

Manufacturing activity likely remains soft from ongoing trade disruptions, but we expect the bulk of May’s GDP decline could be attributed to a sharp decline in oil production, as wildfires in Alberta significantly disrupted operations.

Retail activity was also soft, dragged down by lower auto sales that reversed earlier gains in March and April when consumers pulled purchases forward to front-run tariffs.

Losses from both factors – lower retail purchases and oil production – are expected to have at least partially recovered in June. Statistics Canada’s preliminary estimate was for a 1.6% increase in nominal retail sales in June following the 1.1% May decline. Additionally, rebuilding efforts following natural disasters could also have supported GDP growth in other sectors.

On a quarterly basis, Q2 GDP growth is tracking close to flat— aligning with the more optimistic of the two scenarios the BoC projected in its April forecast. In its last Monetary Policy Report, the central bank took the unusual step of not providing a base case growth forecast but scenario analysis, given the enormous uncertainty tied to international trade at the time.

We’ll be watching Wednesday’s MPR closely for new projections but don’t expect any surprises regarding the decision to hold the overnight rate steady. The BoC has remained on the sidelines for the past two meetings after cutting the overnight rate by 225 basis points since June 2024.

What’s holding the BoC back?

Trade tensions remain heightened and economic data is still soft. However, the Canadian labour market showed signs of bottoming out in June, and sentiment indicators, which took a nosedive in March, have also partially recovered.

Critically for Canada, CUSMA exemptions are allowing the vast majority of Canadian goods exports to enter the U.S. duty-free. Echoing business reports from the latest BoC outlook survey, we continue to consider the most severe economic scenarios as less probable than earlier in spring, and expect the economy will remain soft over the second half of this year but won’t contract.

More unnerving for the BoC are recent inflation reports that have surprised broadly to the upside. Its preferred core measures have edged higher in 2025, driven mostly by building pressures among domestic services components. This contradicts earlier expectations that softening in domestic demand would lead to further disinflation and easing in core inflation.

Overall, sticky inflation readings, a weakening but relatively resilient economic backdrop and prospects for larger fiscal spending are reasons why we do not expect the BoC will cut again in this cycle.

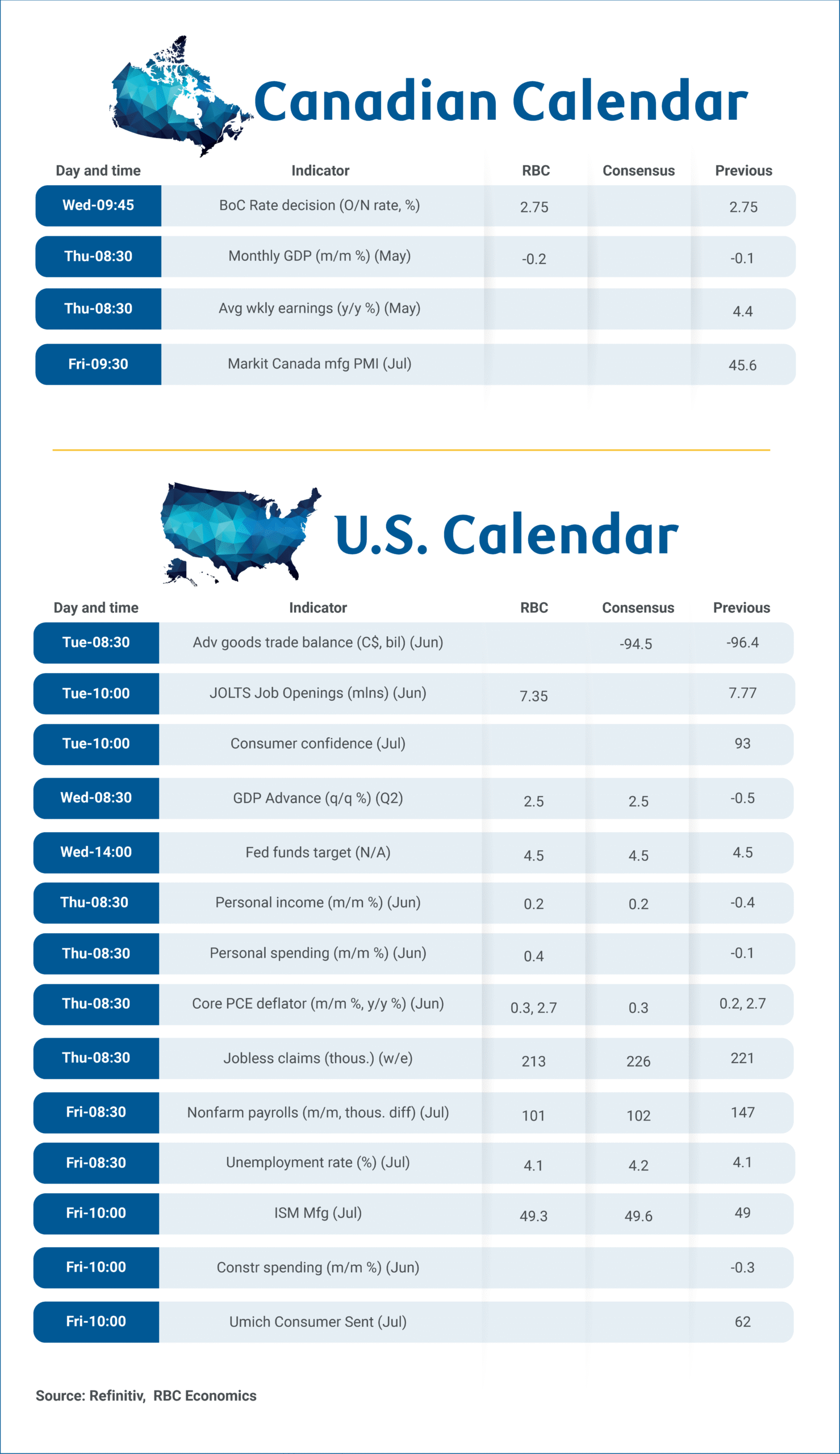

Week ahead data watch:

Job vacancies in May’s Canadian Survey of Employment, Payrolls, and Hours (SEPH) data on Thursday will be analyzed for signs of softening in the labour market. Alternative job openings data from Indeed.com have stabilized in the summer after declines earlier in the year.

The U.S. data calendar is also crowded next week. U.S. Q2 GDP On Wednesday is expected to show an annualized increase of 2.5%, reflecting in part the reversal of a statistical quirk that distorted trade and inventory figures in Q1. The Fed meeting that afternoon is expected to maintain current rates and otherwise uneventful Friday's July payrolls data is forecast to show a moderately slower but still robust pace of job growth. The unemployment rate from the separate Household Survey is expected to have remained unchanged at 4.1%.

Is S&P 500 Losing Steam?

This week saw one of the most mixed price action towards the newly formed all-time highs for the 500 best US Companies – The ongoing opening bell is not showing much juice to retest the overnight highs and other global indices are also correcting on the session.

The Earnings season has been more than decent but looking at the price action, buyers seem to have come to an exhaustion point.

Despite a Daily Golden Cross leading to 11 consecutive new highs, the price discovery for the S&P looks to be stalling at a key zone of interest, coming short of the 6,400 psychological level for both the CFD and actual Index.

Many of the best performing assets in the year have started to form local tops: looking at the strong retracement in Gold, Bitcoin, the freshly formed Double top in the Nasdaq that sellers are starting to lean up on and the Dow Jones just retesting its ATH just yesterday without breaching the level.

This week had some decently positive news that could have boosted momentum for equities further such as Trump confirming he won't fire Jerome Powell and the finalized US-Japan Trade Deal.

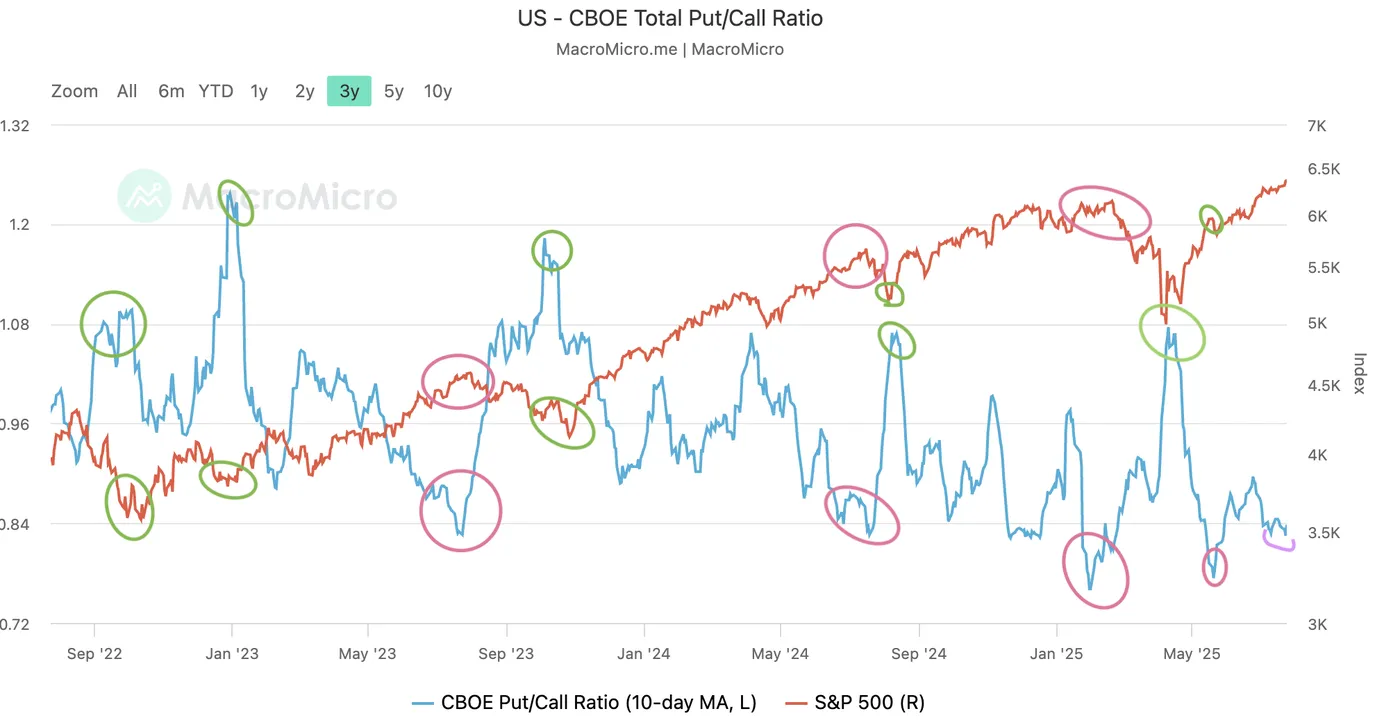

Positioning and Sentiment at an extreme

S&P 500 and CBOE Put/Call Ratio – July 24 2025 – Source: MacroMicro

Wherever you look, Market participants mention how strong the ongoing US Trend is and how such strong momentum cannot be faded – This is far from an invitation to sell highs but to trade with more caution looking ahead.

The S&P 500 Put/Call Ratio is coming at a trough and such positive & negative spikes tend to coincide with some tops, particularly amid extreme Fear/Greed levels.

I remember the 2022 Bear Market concluding on an extreme put ratio against calls – The trough isn't forming such a spike today but the extremes are close.

S&P 500 Technical Analysis from the Daily to intraday charts

S&P 500 Daily

S&P 500 Daily Chart, July 24 2025 – Source: TradingView

The S&P 500 has been flying upwards particularly since the end of the Israel-Iran conflict after forming lows at 5,930.

There hasn't been much selling, with almost no daily candle closing below the prior with this pushing Daily RSI to overbought levels.

Overbought RSI is by definition a standard in such strong trends – Such technical signs don't always traduce with a correction but at least an exhaustion in the move.

You may also take a peek at the Potential Supply trendline that is not too far from current trading – But a closer look is more than required for further analysis.

S&P 500 4H

S&P 500 4H Chart, July 24 2025 – Source: TradingView

Looking closer, we can spot candles that are looking less strong particularly as buyers are stepping against the 1.272 Fib-Extension from the War lows to the July 3 Local top.

Momentum is currently retracting from overbought and momentum is starting to become slightly more neutral.

Buyers will want to re-enter above the longer-run upwards Channel formed with the April 2025 bottom and will need to breach the current highs on strong momentum – Local CFD Highs at 6,391, Index at 6,381.

S&P 500 1H Chart

Looking even closer, buyers haven't given up just yet, especially with RSI momentum not breaching the neutral line.

Except for the higher timeframe warning signs, holding above the 1H-MA 50 still give the short-term hand to the bulls, but they will have to break the last swing highs to gain further traction.

Levels of interest to place on your charts:

Support Levels:

- Mini-Support and 50-H MA 6,370

- 200-H MA 6,315

- Key Support 6,300

- Past week lows 6,230

Resistance Levels:

- 6,390 to 6,400 Current highs resistance

- Potential Resistance at Fib extension 6,420

- Level to breach for new ATH 6,391

Safe Trades!

Lower Global Trade Uncertainty Supports Risk Appetite

US dollar

The US has signed agreements with Japan, Indonesia and the Philippines. Tariffs range from 15% to 19%. Tokyo has secured a reduction in import duties on cars from Washington from 25% to 15%. Looking at this deal, the European Union also wants to get 15% tariffs. Brussels does not intend to activate the anti-coercion mechanism and respond with reciprocal duties of €100 billion.

The reduced risk of a large-scale trade war between the US and the EU is increasing global risk appetite and putting pressure on the US dollar as a safe-haven asset. At the same time, the reduction in trade uncertainty is giving the Fed a free hand to ease monetary policy. A sharp cut in the federal funds rate may happen sooner than expected, contributing to the dollar’s decline.

The futures market expects an acceleration of easing in 2026 due to Jerome Powell’s departure from the Fed chair. Donald Trump should choose the nominee, and obviously, it will be a very dovish person who aligns with the president’s opinion. Recently, he demanded that the Fed cut rates by 300 basis points.

Stock indices

The US economy is not falling off a cliff since trade deals are reducing uncertainty. The Fed is moving towards easing monetary policy, and corporate earnings are positive. What else do stock indices need for a rally? The S&P 500 continues to break historical highs and eagerly awaits data from the so-called Magnificent Seven. Analysts expect those companies to report 14% profit growth compared to just 3% growth for the other 493 companies in the broad stock index.

So far, actual data for the second quarter has been better for 83% of reporting issuers. The average for the last 5 and 10 years is 78% and 75%, respectively. A weak dollar supports the S&P 500. Due to the enormous size of the US domestic market, only 13% of corporate profits come from abroad. Companies included in the broad stock index are more international. For Goldman Sachs, for example, the figure is 28%.

How long will the euphoria last? If tariffs push the US economy toward stagflation, corporate earnings will fall, and the S&P 500 will slide.

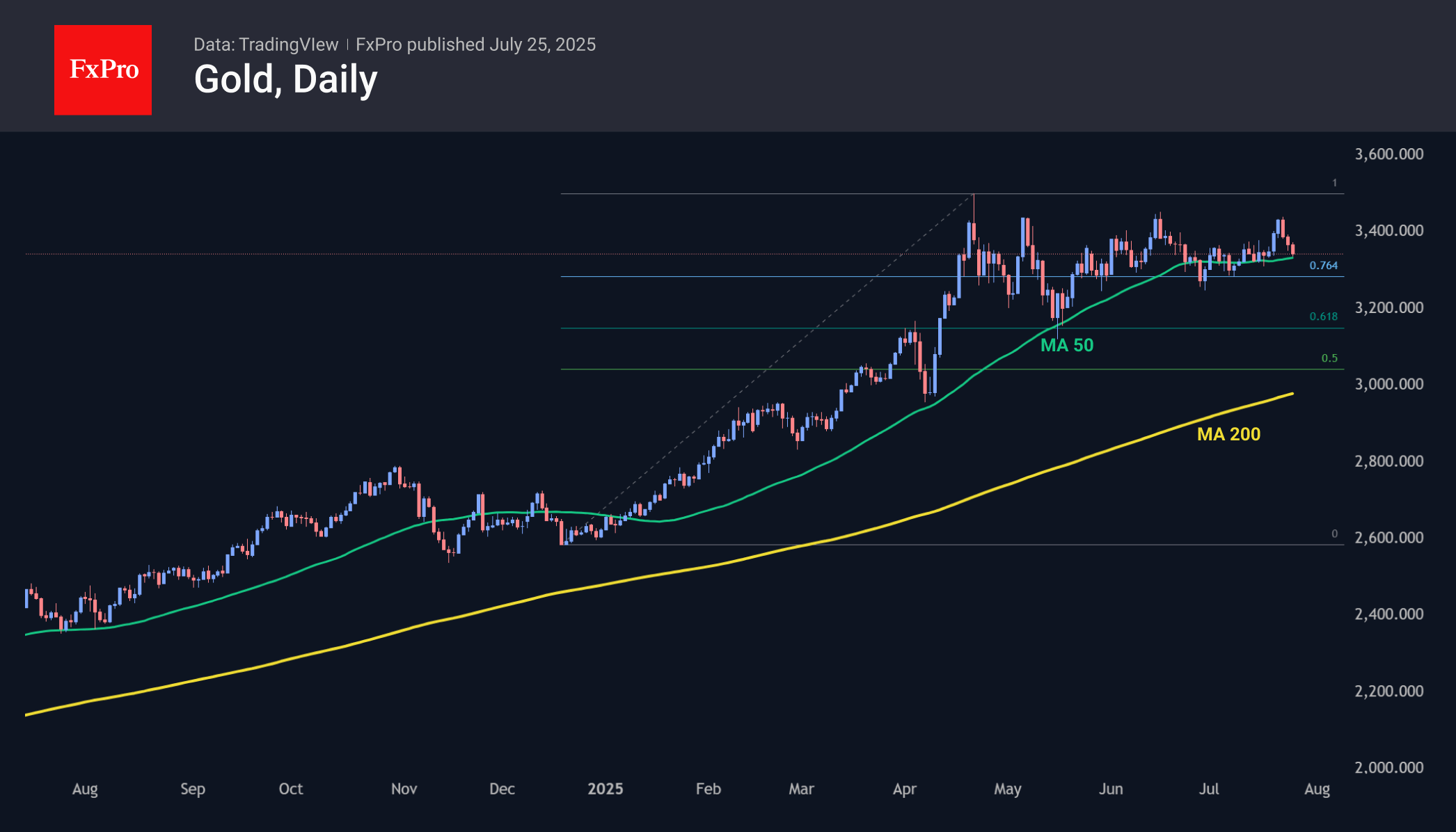

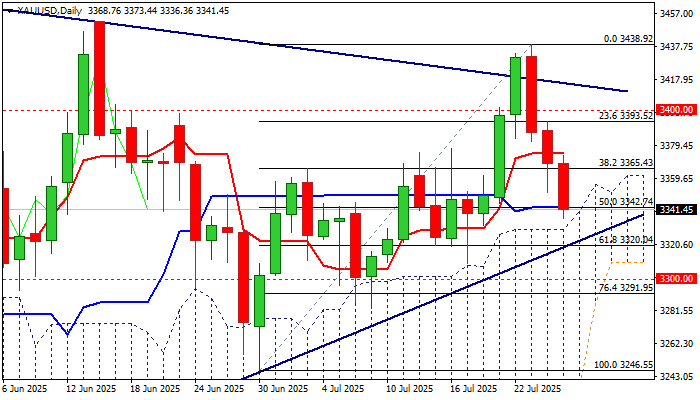

XAU/USD: Gold Bears Regained Control and Look for Test of Key Supports

Gold price continues to trend lower for the third consecutive day, deflated by stronger dollar and optimism on signs of progress in US-EU trade talks.

Bears regained control after a double upside rejection and false break above the bear-trendline connecting ($3500 record high and June 16 lower top at $3452) with formation of bearish engulfing pattern on daily chart, providing fresh bearish signal.

Strong acceleration pushed the metal’s price down by over 2.5% in past three days, to retrace over a half of recent $3246/$3438 upleg (Fibo 50% at $3342, reinforced by 20DMA) and approach key support at $3330 (daily Ichimoku cloud top) as rising daily cloud supported the action since mid-Jan and cloud top contained a number of attacks in past two months.

Penetration of daily cloud and violation nearby other pivotal support at $3320 (trendline support / Fibo 61.8%) would sideline larger bulls and risk further losses towards $3300/$3290 zone (psychological / Fibo 76.4%).

Weaker technical studies on daily chart (14-d momentum hits the centreline in attempts to break into negative territory / price fell below 10 and 20DMA’s) support the notion, with formation of weekly Gravestone Doji candle signaling that sellers currently dominate.

However, it will be important to watch reaction at daily cloud top, as cloud still marks very significant support that may limit dips one more time.

Res: 3350; 3365; 3374; 3393.

Sup: 3330; 3320; 3309; 3300.

Sunset Market Commentary

Markets

European bonds extended declines in the wake of yesterday’s ECB policy meeting. President Lagarde sounded pretty optimistic on the economy, saying it perhaps withstood the trade uncertainty better than expected. The comment took markets a bit by surprise since they were discounting another rate cut somewhere later this year. That base case is now seriously put into question, especially against the backdrop of a (rumoured) potential trade deal between the US and EU in the very near future. The classic “Bloomberg sources” at the ECB later hit the wires, saying that those at the Governing Council calling for further cuts face an uphill battle, reinforcing the move. Yields shot up, especially at the front end of the curve. That upward momentum rolled over in today, be it in a bear steepener this time around. Net daily changes vary between +1 and +3.2 bps in Germany, with a slight underperformance vs swap as well as other core areas. US yields eke out around 0-2 bps while UK rates add up to 2.5 bps at the front. The latter is a bit surprising after the recent string of disappointing data that began with yesterday’s PMIs and moved to this morning’s poor UK GfK consumer confidence and lower-than-expected rebound in June retail sales. Similarly striking is the muted response of front-end Japanese yields to news agency Bloomberg citing officials at the Bank of Japan who see a growing case for a rate hike by year-end after the trade deal reduced uncertainty. Markets give it an unchanged probability of around 80%. Both JPY and GBP are today’s underperformers on the FX market. USD/JPY bounces to 147.88, helped higher by a touch of dollar strength as well. EUR/GBP pierces through 0.87 and prepares for an attack of the post-Liberation Day high which more or less coincides with the 50% recovery on the 2022-2024 decline (resp. 0.8738 and 0.8744). GBP/USD, helped with the aforementioned USD strength, is headed for a back-to-back loss, declining to the 1.343 area. EUR/USD (1.172) loses some ground but remains near the multi-year July high.

The all-in-all muted market moves today shouldn’t surprise given the loaded eco and event calendar for next week. It may even start already this weekend with a possible trade agreement between the EU and US. If not this weekend, then probably early next week since Trump’s renewed tariff deadline lapses on Friday, August 1. In the run-up to that, we have US-Sino trade talks starting on Monday, European inflation prints as well as US and Eurozone Q2 GDP numbers. Friday’s US labour market report will as usual be closely watched for any potential clues regarding Fed rate cuts. Last month’s good edition in any case ruled out such a move at next week’s policy meeting. Fed aside, the Bank of Canada and Bank of Japan also meet. All this happens against the backdrop of the most busiest earnings week.

News & Views

IFO sentiment among German companies has improved somewhat. The index rose to 88.6 in July, up from 88.4 in June. Companies were slightly more satisfied with current business (86.5 from 86.2). Expectations remained largely unchanged (90.7 from a downwardly revised 90.6). Ifo concludes that the upturn in the German economy remains sluggish. The manufacturing index went up (-11 from -13.9) as companies see their current situation as noticeably better. Expectations also brightened further, but incoming orders still lack momentum. Services’ sector business climate deteriorated (2.7 from 3.8). Current business activity was assessed less favorably, while expectations were also revised slightly downward. Trade (-20.2 from -19.2) also weakened due to more pessimistic expectations. The construction subindex rose again (-14.0 from -15.1) on both the current and expected situation.

The IMF today published its 2025 Article IV Consultation with the UK economy. The IMF expects 1.2% growth this year and sees activity improving to 1.4% next year as monetary easing, positive wealth effects, and an uptick in confidence bolster private consumption and offset the drag of trade tensions. Current rise in inflation is seen as temporary due to regulated price increases. Inflation is expected to drop to 2.3% next year. On fiscal policy, the IMF indicates that difficult decisions will likely be needed beyond the medium term to address new expenditure pressures and rebuild fiscal buffers. Short-term the IMF advices a strategy maintaining more headroom so that small changes in to outlook do not compromise assessments of rule compliance. In this respect a once in a year assessment of the self-imposed rules at the time of the autumn budget is preferred rather than twice yearly review.