Sample Category Title

Japan Deal Fuels Rally Before Fed and BoJ Policy Updates

The big news last week was a surprise trade deal between the U.S. and Japan. The agreement will lower proposed tariffs on Japanese imports from 25% to 15%. This helped boost Japanese stocks, especially car companies, and pushed U.S. stock markets to record highs. Strong earnings from U.S. companies also supported the rally.

Investor mood was positive overall, with hopes that the U.S. might make similar deals with other countries. Economic data was mixed—U.S. services PMI was better than expected, but manufacturing was weaker as companies adjust to higher import costs. In Japan, inflation slowed slightly to 2.9%, down from 3.1% in June.

The U.S. dollar fell early in the week but recovered as traders now think rate cuts may be delayed. Gold rose at first due to trade worries, but dropped after the Japan deal was announced. Bitcoin stayed mostly flat, holding on to gains from earlier weeks.

Markets This Week

U.S. Stocks

The Dow Jones rose slightly last week to reach new record highs, helped by the U.S.–Japan trade deal and hopes for more agreements before the August 1 deadline. Calmer relations between President Trump and Fed Chair Powell also supported market sentiment. However, the Dow’s uptrend is weaker than the S&P 500 and Nasdaq, suggesting short-term range trading is likely. With many key events ahead this week, reacting to news will be important. The medium-term outlook remains positive, and buying on dips continues to be a good strategy. Key support levels are at 44,000, 43,000, and 42,000, while resistance is seen at 45,000, 45,100, and 45,500.

Japanese Stocks

Japanese equities came under pressure early last week after the ruling party performed poorly in the national election, raising expectations that the Prime Minister might step down. However, markets quickly reversed after a surprise U.S.–Japan trade deal was announced. While details were limited, the news was seen as very positive and helped the Nikkei 225 surge above 40,000円, nearing record highs. In the short term, the index appears overbought and may face a pullback in the coming week. However, the trade deal supports a positive medium-term outlook, and buying on weakness near the 40,000円 support level could be a favorable strategy. Resistance is now seen at 42,000円, 42,500円, and 43,000円, while support is at 40,000円, 39,000円, and 38,000円.

USD/JPY

USD/JPY started the week weaker as selling pressure emerged near the May highs, a key resistance area. However, the surprise U.S.–Japan trade deal boosted overall market sentiment and pushed U.S. long-term interest rates higher, helping USD/JPY recover to finish the week nearly unchanged. Looking ahead, this week is critical with both the U.S. Federal Reserve and the Bank of Japan holding policy meetings. While the Bank of Japan has signaled possible rate hikes later this year—which is typically negative for USD/JPY—the pair remains stuck in a range in both the short and medium term. Resistance is now seen at 148 and 149, with support at 146 and 145.

Gold

Gold moved higher at the start of last week, testing key resistance levels from May and June as markets grew concerned the U.S. might finalize major trade deals ahead of the August 1 deadline. However, the surprise announcement of the U.S.–Japan trade agreement eased those concerns, leading to a quick pullback and leaving gold prices nearly unchanged by the end of the week. Despite the short-term dip, gold remains well supported in the medium term, and buying on weakness continues to be the preferred strategy. In the short term, range trading is likely to continue, with resistance at $3,400 and $3,450, and support at $3,300 and $3,250.

Crude Oil

Crude oil traded slightly lower in a narrow range last week, as traders looked for fresh signals to guide the next big move. Prices initially rose on the back of the U.S.–Japan trade deal, but the rally faded, and crude ended the week near its lows. Price action is turning increasingly bearish, with the 10-day moving average now pointing down. In the short term, focusing on selling opportunities appears to be the better strategy. Key levels remain unchanged, with resistance at $70, $75, and $80, and support holding at $65 and $60.

Bitcoin

Bitcoin traded lower last week as profit-taking set in following its recent strong rally. However, support at $115,000 held firmly, with continued backing from the U.S. government helping to keep sentiment positive. In the short term, range trading looks like the best approach, as the 10-day moving average is now moving sideways. Medium-term, the outlook remains bullish, with higher levels still likely. Resistance is seen at $125,000 and $150,000, while support lies at $115,000, $110,000, and $105,000.

This Week’s Focus

- Tuesday: U.S. CB Consumer Confidence, U.S. JOLTS Job Openings

- Wednesday: Australia CPI, E.U. GDP, U.S. GDP, U.S. FOMC

- Thursday: China Manufacturing PMI, Japan Bank of Japan Monetary Policy Statement, E.U, Unemployment Rate, U.S. Core PCE Price Index, U.S. Chicago PMI

- Friday: Australia PPI, E.U. CPI, U.S. Nonfarm Payrolls, U.S. ISM Manufacturing PMI, U.S. Michigan Consumer Sentiment

This week could bring big moves in the markets, with several important events happening. The U.S. Federal Reserve and the Bank of Japan will both meet to decide on interest rates. They are expected to keep rates the same, so traders will focus on what the central banks say about future plans—especially when the U.S. might cut rates and when Japan might raise them.

The most important data comes on Friday with the U.S. jobs report. Before that, markets will also watch for any news about trade talks, especially between the U.S. and Japan, ahead of the August 1 tariff deadline. These events could cause sharp price changes across global markets.

US-EU trade deal delivers Relief, Euro gains but lacks breakout momentum

In a significant breakthrough, the US and EU reached a framework trade agreement on Sunday, averting the imposition of 30% tariffs on European imports. Instead, a reduced 15% rate will apply to most goods. The two sides also agreed to exempt key strategic sectors—such as aircraft, chemicals, and some pharmaceuticals—from any tariffs entirely.

The deal also includes sweeping commitments from the EU, including USD 750B in US energy purchases and USD 600 billion in fresh US-bound investment over current levels.

EU Commission President Ursula von der Leyen called the agreement a win for “stability and predictability,” while acknowledging that the 15% tariff still presents challenges for European automakers. Meanwhile, the EU’s pivot toward US nuclear fuel and LNG also marks a decisive shift away from Russian energy dependency.

US President Donald Trump declared the deal as larger than last week's USD 550B Japan agreement and reiterated that it would significantly deepen US-EU ties across energy, defense, and trade. He claimed “hundreds of billions” in arms sales could follow.

Euro advanced broadly on the announcement, but momentum is restrained. EUR/CHF is still capped below 0.9365 resistance despite today's bounce. Firm break of this level is needed to be the first sign that consolidation pattern from 0.9445 has completed, and the rally from 0.9218 is ready to resume. Otherwise, more sideway trading would likely follow first.

Why RBA’s Job is Only Going to Get Harder

The RBA’s focus is now, rightly, on preserving recent success by ensuring at-target inflation is sustained and the gains in the labour market are retained. However, this may prove difficult.

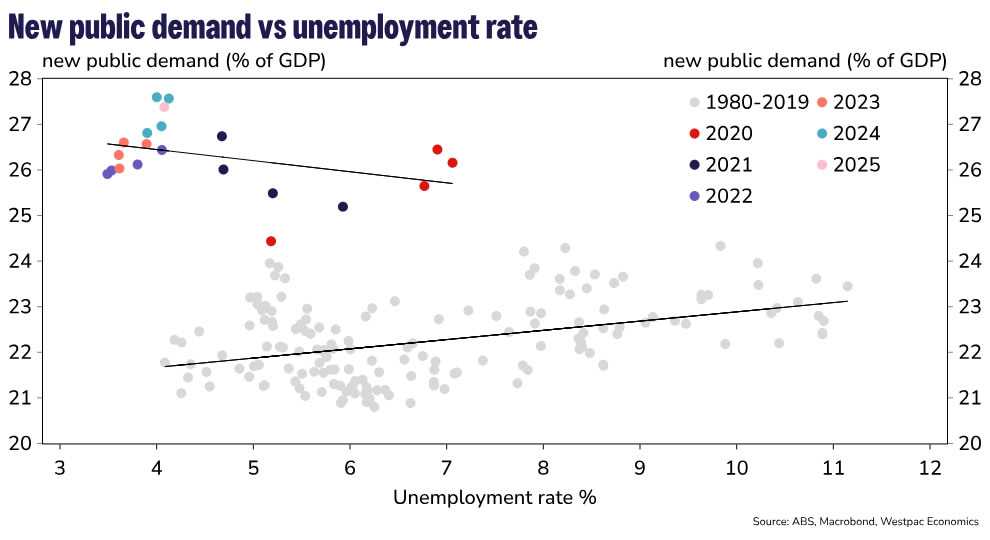

- The huge expansion in Australia’s public demand has supported the labour market more than it has added to inflation, allowing the RBA to focus on taming inflation without having to look over its shoulder at a deteriorating labour market.

- The non-market sector (healthcare, education and public administration) has accounted for 95% of the growth in hours worked in the economy over the past two-years. If non-market job creation over this period had instead run at its pre-pandemic pace, the unemployment rate could be up to 1 percentage point higher today.

- However, public demand is forecast to slow and there is a risk the labour market underperforms as a slowdown in non-market job creation packs a bigger punch. Importantly, the slowing in public demand is unlikely to translate into further downward pressure on inflation dynamics, at least not straight away.

- This could materially worsen the short-run trade-off between the RBA’s inflation and full-employment objectives. Instead of a world where the RBA has headroom to attend to one side of its mandate, it could be faced with a scenario where they increasingly clash.

- Meanwhile, the expansion in public demand has altered the economy’s relative sensitivity to fiscal and monetary policy in favour of fiscal policy decisions, leaving the aggregate economy less sensitive to monetary policy.

- The RBA may find itself navigating a more challenging trade-off between its objectives with a less-effective policy tool. This will see the RBA retain policy flexibility and keep policy guidance to a minimum. Given this, expect less consensus in short-term meeting outcomes and a less predictable RBA – as was on display earlier this month.

In the words of RBA Governor Michele Bullock, “Australia has done remarkably well. Who would have said two years ago we would be sitting here now with inflation at 2 something and unemployment at 4.1%. Not many people”. And we would agree with this, Australia has fared better than many comparable countries, even when including the surprise jump in the unemployment rate to 4.3%.

During her Annika Foundation speech, Bullock recognised that much of this success has come from a reversal of earlier supply disruptions. However, this has not been the only factor behind the normalisation of inflation and the resilient labour market . The huge expansion in public sector demand has supported the labour market more than it has added to inflation, allowing the RBA to focus on taming inflation without having to look over its shoulder at a deteriorating labour market.

The RBA’s focus is now, rightly, on preserving this success by ensuring at-target inflation is sustained and the gains in the labour market are retained. However, this may prove difficult.

The RBA will be navigating an unwind in public demand which could materially worsen the short-run trade-off between its inflation and full-employment objectives. Meanwhile, the economy may have become less sensitive to monetary policy, compounding the challenge facing the RBA.

Labour market decoupled from activity

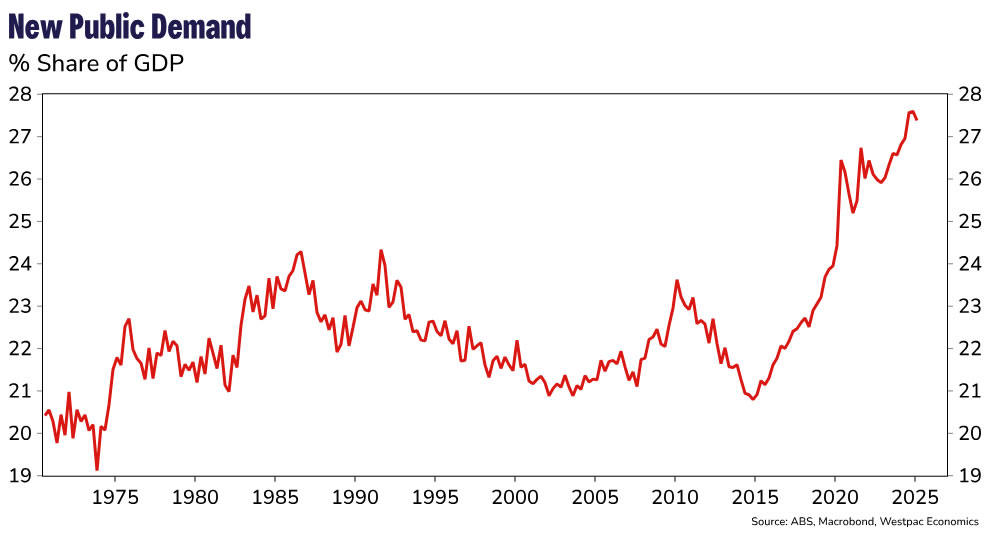

The stronger growth of public demand compared to private demand has been a persistent theme of Australia’s economic activity over recent years. Since the end of 2022 the public sector has expanded at an annualised rate of 4.0%, compared to just 1.5% for the private sector. This has contributed to a rapid surge in public demand as a share of the economy to a record high, a point we have highlighted on several occasions (most recently, here).

The strength of public sector activity has been underpinned by the massive expansion in the care economy and large-scale cost of living support for households and businesses; the latter converted some private-sector consumption, such as on electricity, into public consumption. Meanwhile, soft private sector activity has been centred on weak household consumption more broadly as high inflation, a rising tax take and elevated interest rates weighed on real household incomes. More recently, this weakness has spilled over to business investment outcomes as the boost from surging population growth has gradually faded.

It’s historically very unusual for public demand to be so strong when labour markets are tight. Public demand tends to be counter-cyclical, increasing when the labour market is weak and slowing in the face of capacity constraints. Instead, the strength in public demand, and labour-intensive nature of the care economy, has provided significant support to the labour market as private demand (and hiring) has slowed.

Non-market sector job creation, propelled by the expansion in public demand (particularly in the care economy), has prevented a material increase in unemployment, as would normally be expected given recent weak GDP growth outcomes. In fact, the non-market sector (healthcare, education and public administration), has accounted for 95% of the growth in hours worked in the economy over the past two-years. If non-market job creation over this period had instead run at its pre-pandemic pace, the unemployment rate could be up to 1 percentage point higher today, at 5.25% – back to its pre pandemic level. This scenario assumes an unchanged participation rate and stronger employment growth in the market sector, accounting for around half of the lower non-market employment.

Inflation Impact Has Been Muted

It’s at this stage the economist in the room is quick to point out that strong growth in public demand should put undue upward pressure on inflation and make the RBA’s job more difficult. However, for the most part this has not been the case.

There’s a couple of reasons for this. First, much of the increase in public demand has been an increase and broadening of services provided on behalf of households, such as disability care, childcare, healthcare and aged care. Given these services are largely funded by the government themselves rather than households, they are not measured in the Consumer Price Index (CPI). Marginal increases in demand for these services will add to inflation the government is facing but has less direct impact on consumers.

The impact of rising public demand on measured inflation has also been mitigated by the use of subsidies, which have mechanically reduced headline inflation outcomes in a similar way. The Government temporarily bore part of the burden of higher prices, reducing that faced by the consumer. These subsidies also had second round effects, reducing price gains of those items indexed to headline inflation.

There are some caveats to this. There is little argument that the non-market sector has drawn on resources from the market sector to meet the huge increase in labour demand. This is part of the reason businesses, particularly in sectors where labour is easily substitutable, continue to struggle with labour availability.

Other areas of public demand, such as the massive amount of infrastructure investment across the country are also drawing heavily on capacity in the market sector. Strong employment in the non-market sector has also supported aggregate household income growth, preventing a more significant slowdown in private consumption. These forces have added to inflation outcomes at the margin but are largely second order.

A Purple-Patch for the RBA

Overall, strong public demand has supported the labour market more than it has boosted inflation. This has been a perfect combination for the RBA as it has softened the short-run trade-off between inflation and unemployment (the ‘sacrifice ratio’) and given the Board scope to focus on its inflation objective, without being constrained by the opposite side of its mandate as the economy slowed.

However, the economy is currently in the midst of a transition. Growth in public demand is expected to slow (but remain elevated), and private demand is staging a fragile recovery. Governments are scaling back cost of living support, the care economy expansion is maturing, and thus slowing, and for the states earlier fiscal largesse is meeting the political realities of higher debt servicing costs. Meanwhile, real household incomes are growing again as inflation has returned to target, stage 3 tax cuts have paid-back some recent bracket-creep and now interest rates are on the way down. This is driving a nascent recovery in household consumption and private demand.

From Boon to Burden

As public demand slows, it could flip the economic calculus presented to the RBA. It will be a significant drag on aggregate economic activity, potentially offsetting the fragile recovery in the private sector (most recently discussed here). For the RBA, there is a related risk the labour market underperforms relative to the real economy as a slowdown in non-market sector job creation packs a bigger punch given its (now) much larger concentration. Additionally, the market sector is less labour intensive so any pick-up in market sector activity will create fewer jobs per dollar of GDP.

Importantly, the slowing in public demand is unlikely to translate into further downward pressure on inflation dynamics, at least not straight away. The earlier point that most of the increase in public demand has been in areas that are not captured in the consumer price index, is one reason for this. Another is that private demand is expected to be in the midst of a gentle recovery and dynamics in the private (market) sector are more consequential for inflation. Finally, the roll-off of government subsidies will actually have the opposite impact, mechanically lifting headline inflation outcomes, though this is likely to be deemed transitory to the extent inflation expectations stay put.

The asymmetric impact of slowing public sector growth is a tricky combination for central bankers. Instead of a world where the RBA has headroom to attend to one side of its mandate, the RBA could be faced with a scenario where they increasingly clash. The magnitude of the slowdown in public demand will ultimately dictate how heavily these objectives jar. A more significant slowing in public demand will exacerbate the trade-off for the RBA.

Monetary Policy as a Tool Might be Even More ‘Blunt’

The challenge imposed on the RBA from a worse trade-off between inflation and labour market outcomes is likely to be compounded by the fact that monetary policy will be working on a smaller share of the economy. In other words, the aggregate economy may have become less sensitive to monetary policy.

Slow moving structural changes often play second fiddle to contemporaneous economic dynamics. Economic composition is a prime example and while ‘growing the pie’ is very important, the relative ‘size of the slices’ mustn’t be ignored.

Over the past decade, Australia’s economy has quietly undergone a monumental structural shift, rivalling that of the mining investment boom. After averaging around 22% of the economy from 1975 to 2015, public demand has since exploded to a record 27% of the economy. A five-percentage point shift may not sound like much, but it’s now worth about $33 billion a quarter in real activity and is equivalent to the increase in the mining sector share of the economy during the mining investment boom.

The pandemic certainly had a role to play in this structural change, but it was by no means the only catalyst. This is a trend that was well underway before the pandemic began and has since continued at pace during the aftermath. As flagged earlier, the forces behind this compositional shift are well known: the massive expansion of the care economy, and more recently, large scale cost of living support for households and businesses. Governments are increasingly delivering support to households by purchasing or subsidising goods and services provided to households, rather than using direct income transfers.

Relatively soggy growth in the private sector over the last decade has also played a role in the rising share of public demand. Household consumption and business investment were anaemic in the lead-up to the pandemic, and outside of lockdown induced volatility, have not impressed since.

The implications of this structural change on aggregate productivity outcomes have been an important topic pioneered by my colleague Pat Bustamante here. But there are broader implications outside of productivity that have so far garnered less attention, one prominent example is what it might mean for setting monetary policy.

The RBA has spilled a lot of ink discussing the different transmission channels through which monetary policy influences the economy. But even more fundamental, is the relative size of the parts of the economy that are sensitive to monetary policy. An increase in the relative size of a less interest rate sensitive component of the economy will, at the margin, reduce the sensitivity of the whole economy to monetary policy.

It would be misleading to suggest that public demand is immune to changes in interest rates in the long run. But it’s less sensitive to monetary policy than the private sector, particularly in the context of a once in a generation terms of trade shock that’s temporarily flattered the health of our fiscal position – as is currently the case. Hence, the huge expansion in public demand has altered the economy’s relative sensitivity to fiscal and monetary policy in favour of fiscal policy decisions. (And while the reduced share of income from transfers might have made households more interest-sensitive at the margin, the expansion in public demand has been large enough to more than offset such an effect.)

Conclusion

The RBA may therefore find itself in a position where it is navigating a more challenging trade-off between its objectives with a less-effective policy tool. A larger adjustment in the labour market from slowing public demand and weaker sensitivity of the aggregate economy to monetary policy supports our view that the RBA will ultimately need to provide the economy with more monetary support.

However, the narrower trade-off with inflation will likely see the RBA remain patient in delivering support, favouring its inflation mandate at least until it no longer sees the labour market as being tighter than full employment. This will see the RBA retain policy flexibility, keep policy guidance to a minimum and continue its non-committal tone. Given this, expect less consensus in short-term meeting outcomes and a less predictable RBA – as was on display earlier this month.

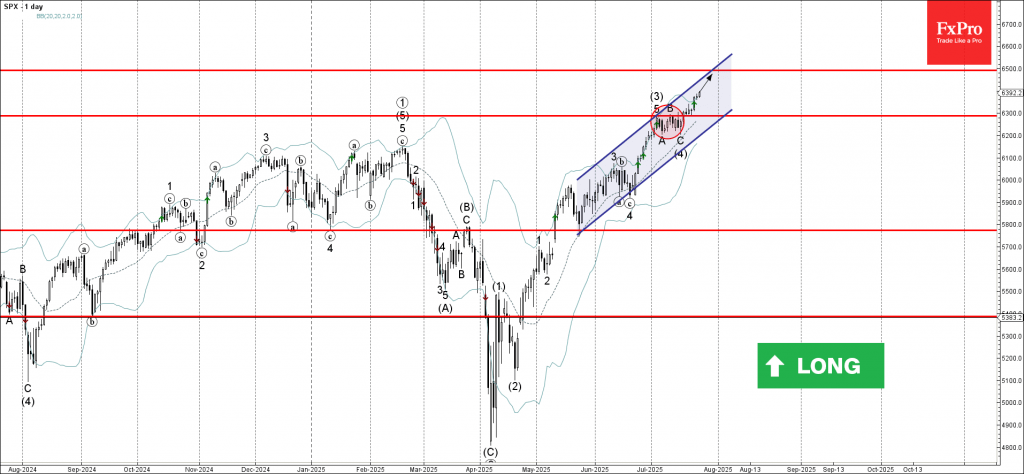

S&P 500 Index Wave Analysis

- S&P 500 Index broke key resistance level 6300.00

- Likely to rise to resistance level 6500.00

S&P 500 Index recently broke the key resistance level 6300.00 (which stopped the previous waves 5 and (B), as can be seen below).

The breakout of the resistance level 6300.00 continues the active intermediate impulse wave (5) from the middle of this month.

Given the strong daily uptrend, S&P 500 Index can be expected to rise to the next resistance level 6500.00 (coinciding with the daily up channel from May).

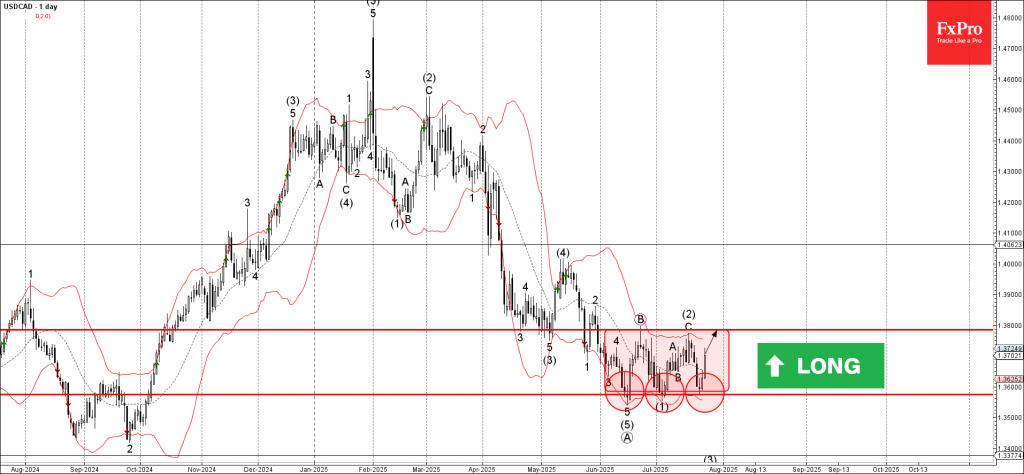

USDCAD Wave Analysis

USDCAD: ⬆️ Buy

- USDCAD rising inside sideways price range inside

- Likely to reach resistance level 1.3800

USDCAD currency pair recently reversed down from the key support level 1.3575 (which is the lower boundary of the sideways price range inside which the price has been trading from June).

The upward reversal from the support level 1.3575 created the daily Japanese candlesticks reversal pattern Morning Star.

USDCAD currency pair can be expected to rise to the next resistance level 1.3800 (upper border of this sideways price range, top of wave (2)).

Risk Appetite Builds After US-Japan Deal, DAX and Euro Awaits Transatlantic Breakthrough

Investor sentiment turned decisively upbeat last week, with global equities rallying on the back of a landmark trade agreement between the US and Japan. The deal was welcomed by markets as a major breakthrough just days ahead of the August 1 tariff deadline.

Japan’s Nikkei surged past 42k mark, with momentum now suggesting a breakout to new record may be imminent. US stocks also extended gains, with the S&P 500 and NASDAQ closing at fresh all-time highs.

In Europe, however, DAX underperformed amid investor caution ahead of pivotal US-EU trade talks. Focus now shifts to Sunday’s high-stakes meeting between US President Donald Trump and European Commission President Ursula von der Leyen in Scotland.

In the currency markets, Euro led weekly gains, supported by fading expectations of a near-term ECB rate cut. The Kiwi and Aussie followed closely, buoyed by strong risk-on flows.

Dollar ended the week as the worst-performing major, despite a late-week rebound. Loonie and Sterling were the next weakest, while the Yen and Swiss Franc held in the middle of the pack.

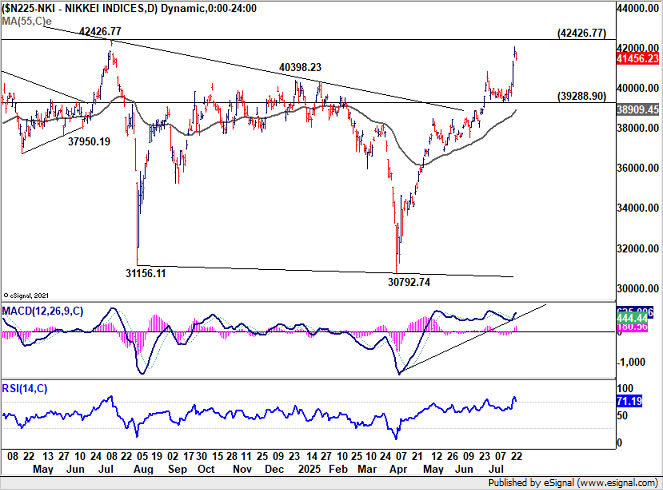

Nikkei Surges Toward Record High on US-Japan Deal

Investor sentiment got a powerful boost last week by the breakthrough in US-Japan trade negotiations, with the two sides agreeing a sweeping deal that includes a 15% blanket tariff on Japanese imports, down from a proposed 25%, and significant Japanese market access for US autos, agriculture, and rice. The agreement also includes private-sector-led projects, with Japan’s top negotiator confirming profit-sharing arrangements will reflect actual capital contributions. Overall, the announcement being made just days ahead of the August 1 global tariff escalation deadline, was seen as a stabilizing force amid rising global trade tensions.

Nikkei surged through 42k for the first time since early 2024, reflecting optimism that the deal will tremendously ease tariff-related uncertainty. Traders booked some profits ahead of the weekend, but market momentum remains strong. With the cloud of trade disruption easing and investors rotating back into Japan, Nikkei should be ready to challenge its 2024 record of 42426.77 in the very near term.

Yet, domestic uncertainties are clouding the outlook. Prime Minister Shigeru Ishiba, whose Liberal Democratic Party suffered a stinging defeat, has yet to confirm a resignation date. Political paralysis could derail fiscal coordination at a time when expansionary policies are being discussed to support the economy.

Besides, the election results raised the risk of deteriorating fiscal discipline. Markets took notice—10-year JGB yields breached 1.6%, a level not seen in over 15 years. A weak 40-year bond auction midweek further signaled investor caution, with the bid-to-cover ratio falling to its lowest since 2011.

Technically, while initial resistance could be seen from 42426.77 record high to limit upside, near term outlook in Nikkei will stay bullish as long as 39288.90 support holds. Firm break of 42426.77 is expected eventually to resume the long term up trend.

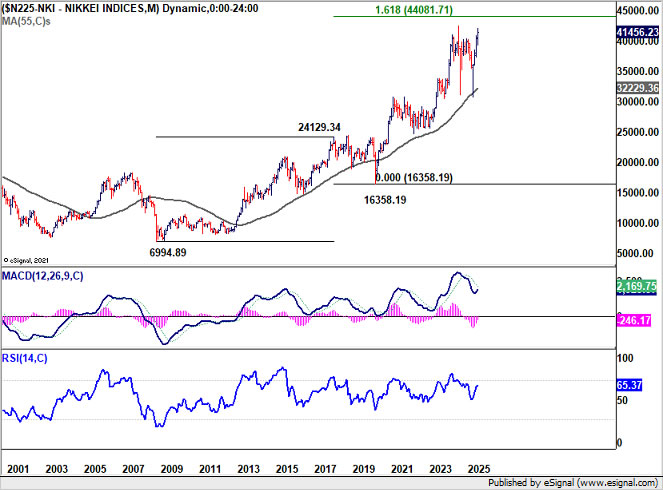

The main hurdle for Nikkei, however, will be on 161.8% projection of 6994.89 to 24129.34 from 16358.19 at 44081.71. Reaction from there will reveal how sustainable Nikkei's up trend would be.

Yen, meanwhile, softened after a brief recovery. The removal of trade risk is arguably a hawkish development for the BoJ, possibly nudging it toward another rate hike later this year. However, that expectation has been eclipsed by resurgent global risk appetite and Japanese equity strength, both weighing on the safe-haven currency.

Technically, the strong support from 55 D EMA in USD/JPY is a clear near term bullish sign. The rebound from 139.87 should be ready to resume soon, to 100% projection of 139.87 to 148.64 from 142.66 at 151.43.

Decisive break of 151.43 will raise the chance that whole medium term corrective pattern from 161.94 (2024 July high) has completed with three waves to 139.87. That would also align with Nikkei's outlook, where medium term consolidation pattern from 42426.77 (2024 July high) has completed with three waves to 30792.44.

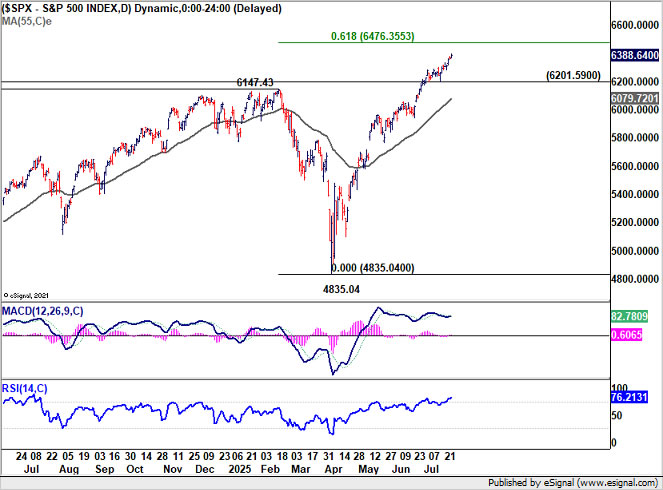

S&P 500 Logs Fifth Record Close, Dollar Still Vulnerable

US equities also closed out the week with strong gains, driven by trade optimism and an impressive earnings season. S&P 500 hit its fifth consecutive record, while the NASDAQ notched four record closes during the week.

The rally was supported by improved risk sentiment following breakthroughs in trade talks and by better-than-expected results from major companies, including Alphabet. The markets were further boosted by signs that companies have weathered tariff-related uncertainty more effectively than expected, with over 82% of S&P 500 firms beating earnings forecasts so far.

Technically, S&P 500 remains on track to 61.8% projection of 3491.58 to 6147.43 from 4835.04 at 6476.35. There might be some resistance between this projection level and long term channel resistance to limit upside on the first attempt. But still, near term outlook will stay bullish as long as 6201.59 support holds, in case of retreat.

Dollar Index dipped to 97.10 midweek before recovering Friday after signs emerged that US President Donald Trump is unlikely to fire Fed Chair Jerome Powell.

Technically, though, prior rejection by falling 55 D EMA (now at 98.67) is a near term bearish sign. Price actions from 96.37 are currently seen as a consolidation pattern only. Further decline is expected as long as 98.91 resistance holds. Break of 96.37 will resume larger fall from 110.17.

However, it should be pointed out again that Dollar Index is close to decade long channel support (now at around 96). With bullish convergence conditio in D MACD too, firm break of 98.91 support will be a strong sign of bottoming. Further rise should then be seen to 101.97 resistance, which is slightly above 38.2% retracement of 110.17 to 96.27 at 101.64, even still as a corrective move.

DAX Awaits Trade Breakthrough, Trump–Von der Leyen Talks Loom

European markets, on the other hand, wrapped the week with mixed sentiment. FTSE 100 notched a fresh record high, benefiting from global risk-on mood. In contrast, Germany’s DAX remained stuck within a near-term range, reflecting broader investor caution as key US-EU trade negotiations approach a potential climax.

Much of the hesitation is tied to uncertainty around the outcome of talks between Washington and Brussels. While reports suggest meaningful progress has been made in discussions, traders are holding back from decisive positioning until there is clear confirmation of a deal—or a breakdown.

Focus now turns to Sunday, when European Commission President Ursula von der Leyen is set to meet US President Donald Trump in Scotland. The high-stakes summit could determine whether a new US-EU trade pact is secured ahead of the August 1 tariff deadline, or if the transatlantic relationship shifts back toward confrontation.

Trump confirmed the meeting on Friday, telling reporters in Glasgow, “Ursula will be here — a highly respected woman. So we look forward to that.” He added that the chances of a deal were “50-50,” with sticking points remaining on “maybe 20 different things.”

Von der Leyen’s spokesperson noted “intensive negotiations” have been taking place across technical and political levels. Her office emphasized that leaders are now weighing a “balanced outcome” that protects cross-border trade and consumer stability.

European diplomats have hinted that the deal on the table could mirror the recent US-Japan pact, featuring a 15% base tariff and possible carve-outs for sensitive sectors like autos and agriculture.

Sunday’s meeting marks the final window for a diplomatic resolution before the US triggers its tariff package. Failure to strike a deal could spark broad retaliation and weigh heavily on sentiment heading into August.

Technically, near term outlook in DAX remains bullish with 23051.55 intact. Breakthrough in US-EU trade negotiations could easily push it through 24639.10 record high.

However, considering bearish divergence condition in W MACD, the real test for DAX would be at 61.8% projection of 11862.84 to 23476.01 from 18489.91 at 25666.77. Strong resistance might emerge there on first attempt to bring deeper correction.

Euro Leads Weekly Gains as Markets Scale Back ECB Cut Bets

Despite lackluster performance in DAX and CAC, Euro stood out as the best-performing major currency, posting solid gains across the board. The reassessment of the ECB’s policy outlook played a key role in driving renewed buying interest.

Markets no longer see a September rate cut as a done deal. While one more move is still possible before the current easing cycle concludes, the odds have shifted toward a later date. October is gaining attention, but December—when the ECB will release updated economic projections—might be even more plausible.

The ECB's decision to keep the deposit rate steady at 2.00% came as no surprise. However, the tone of President Christine Lagarde’s post-meeting remarks reinforced the idea that the ECB is in no rush. Inflation is at target, and growth conditions have turned “relatively favorable,” as she described, dampening the case for immediate action.

Importantly, Lagarde addressed recent strength of Euro, which some fear could undermine inflation. She dismissed those concerns, noting that the ECB’s June forecasts had already factored in slight undershoots in the coming months. For now, she emphasized, it’s the medium-term path that matters most for policy.

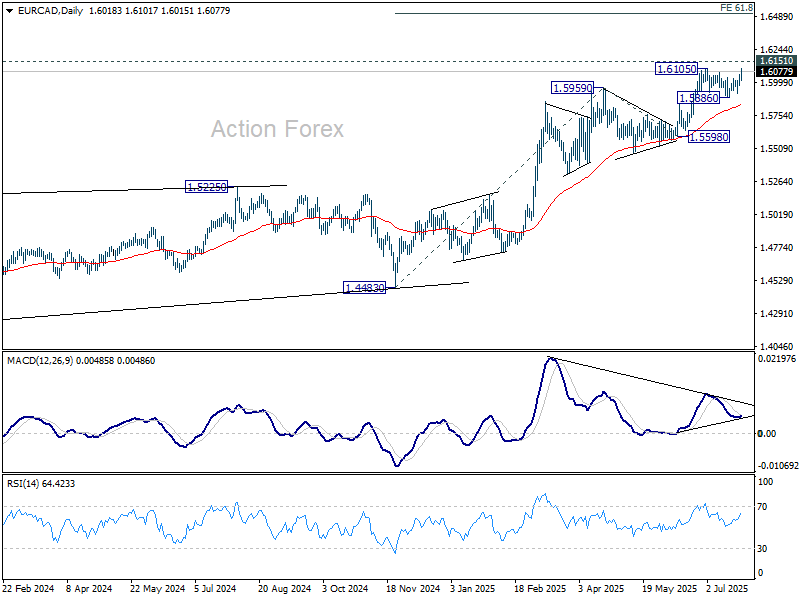

Technically, EUR/CAD's up trend is probably resume to resume through 1.6105 short term top. Firm break there will target 61.8% projection of 1.4483 to 1.5959 from 1.5598 at 1.6510.

More importantly, sustained trading above 1.6151 key resistance (2018 high) will confirm resumption of the whole up trend from01.2127 (2012 low). That would pave the way to 100% projection of 1.2127 to 1.6151 from 1.2867 at 1.6891 in the medium term.

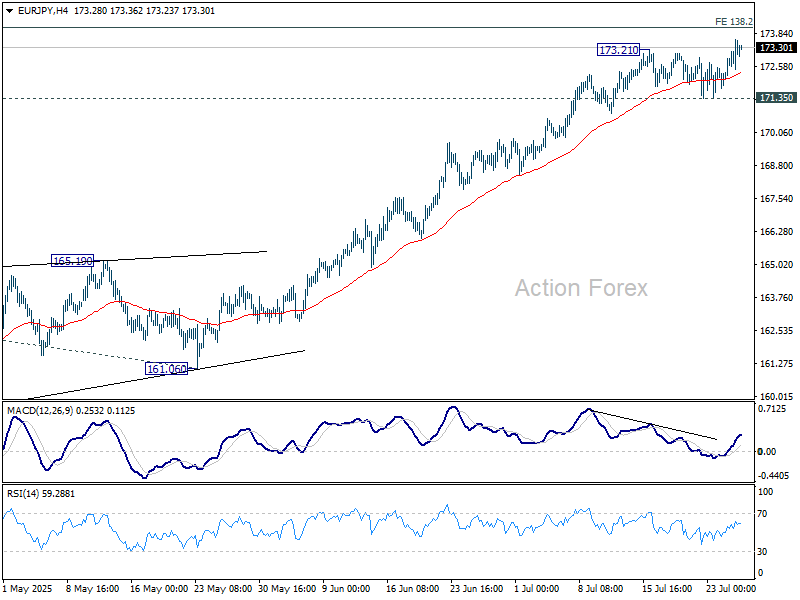

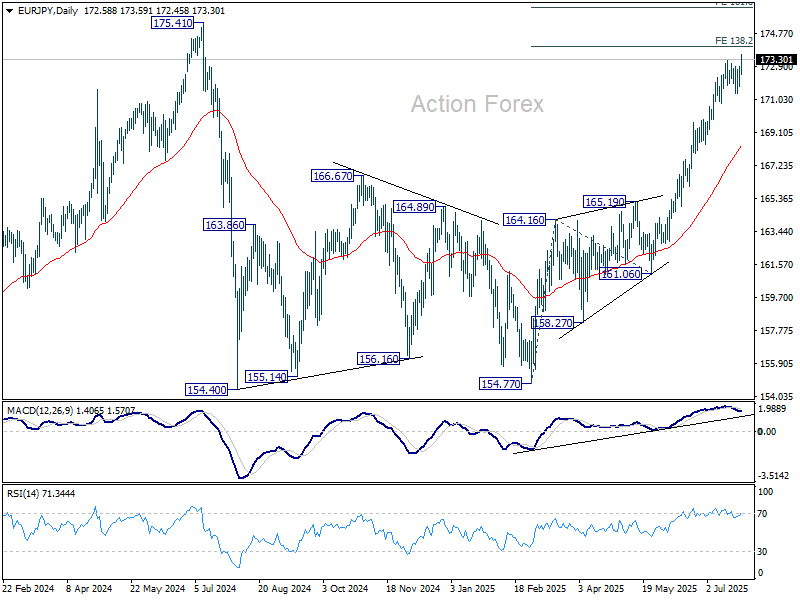

EUR/JPY Weekly Outlook

EUR/JPY's consolidations from 173.21 completed late last week with upside breakout. Initial bias is back on the upside this week for 138.2% projection of 154.77 to 164.16 from 161.06 at 174.03. Break there will bring retest of 175.41 high. For now, near term outlook will remain bullish as long as 171.35 support holds, in case of retreat.

In the bigger picture, considering current strong momentum as seen in the rally from 154.77, corrective pattern from 175.41 could have already completed. Decisive break there will confirm long term up trend resumption. Next target is 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, rejection by 175.41, followed by firm break of 55 D EMA (now at 168.37) will delay this bullish case.

In the long term picture, up trend fro 94.11 (2021 low) is still in progress. On resumption, next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32.

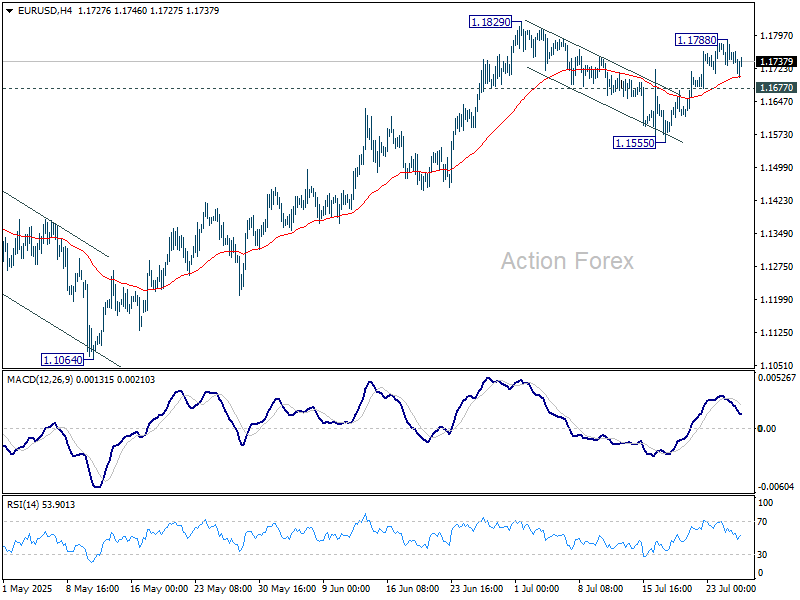

EUR/USD Weekly Outlook

EUR/USD rebounded last week but lost momentum after hitting 1.1788. Initial bias stays neutral this week first. On the upside, above 1.1788 will bring retest of 1.1829. Firm break there will will resume whole rally from 1.0176, and target 1.1916 projection level. However, break of 1.1677 will turn bias to the downside, and extend the corrective pattern from 1.1829 with another falling leg.

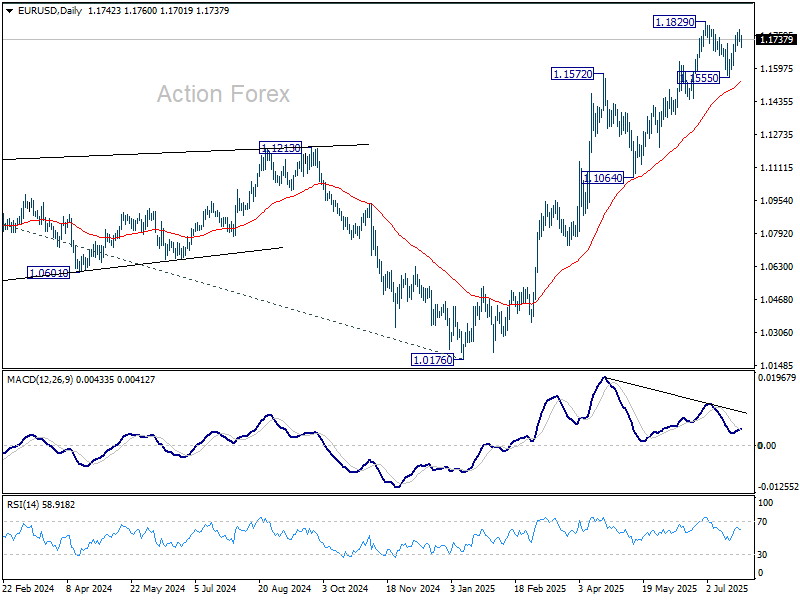

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

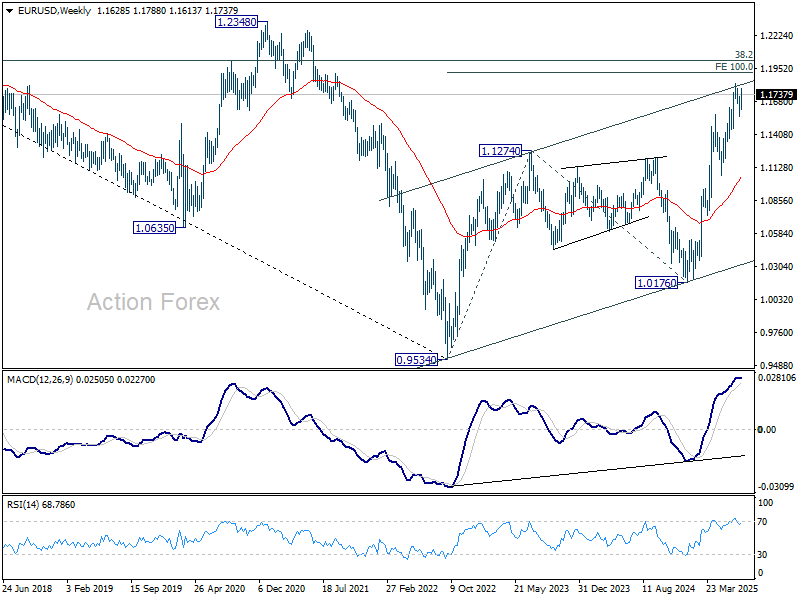

In the long term picture, a long term bottom was in place already at 0.9534, on bullish convergence condition in M MACD. Further rise should be seen to 38.2% retracement of 1.6039 to 0.9534 at 1.2019. Rejection by 1.2019 will keep the price actions from 0.9534 as a corrective pattern. But sustained break of 1.2019 will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.

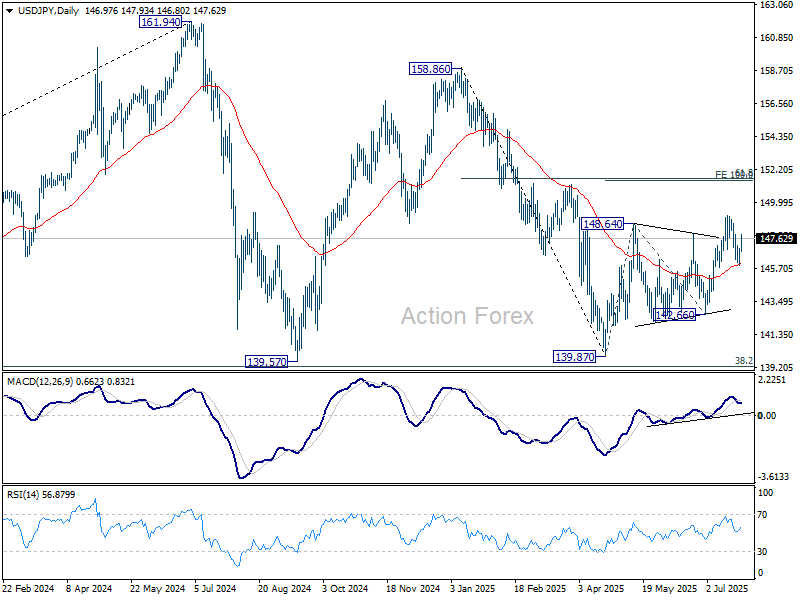

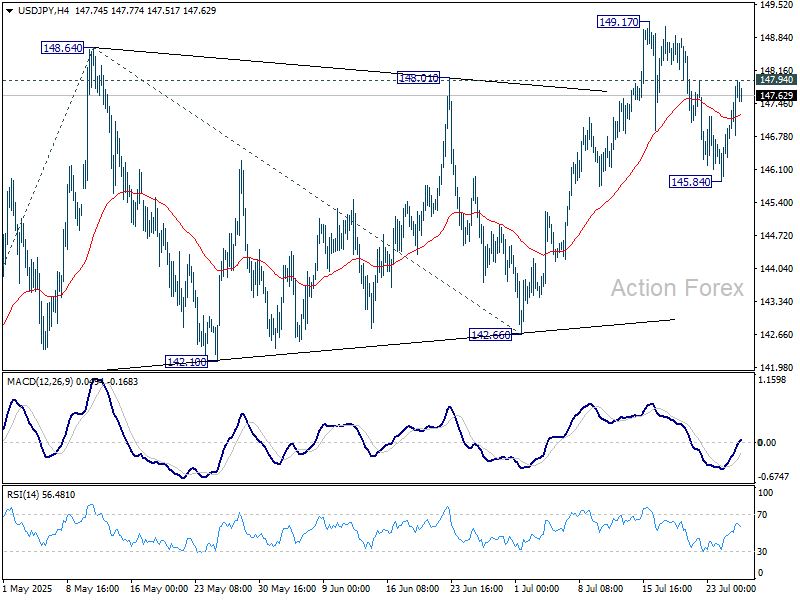

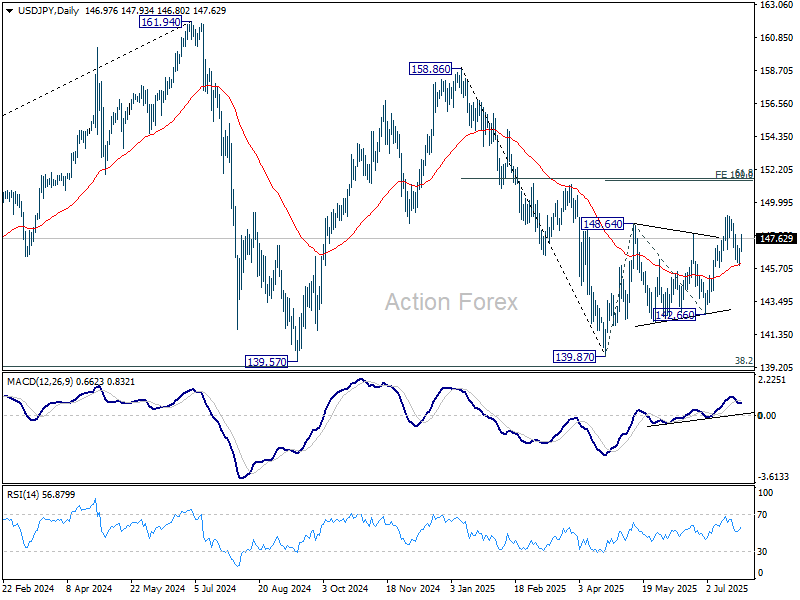

USD/JPY Weekly Outlook

USD/JPY's pullback from 149.17 extended lower last week but recovered after drawing support from 55 D EMA (now at 145.99) and rebounded. Initial bias remains neutral this week and further rise is expected. Above 147.94 minor resistance will bring retest of 149.17 first. Firm break there will target 100% projection of 139.87 to 148.64 from 142.66 at 151.43, which is close to 151.22 fibonacci level.

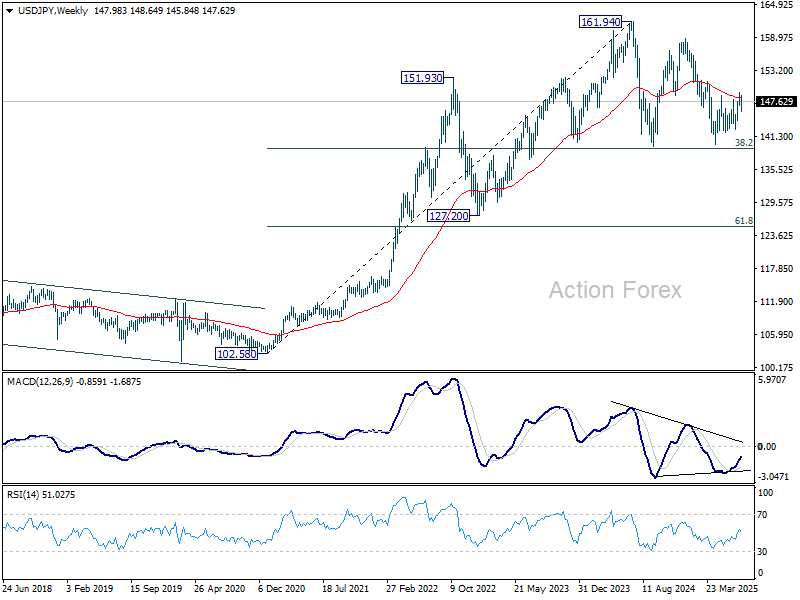

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

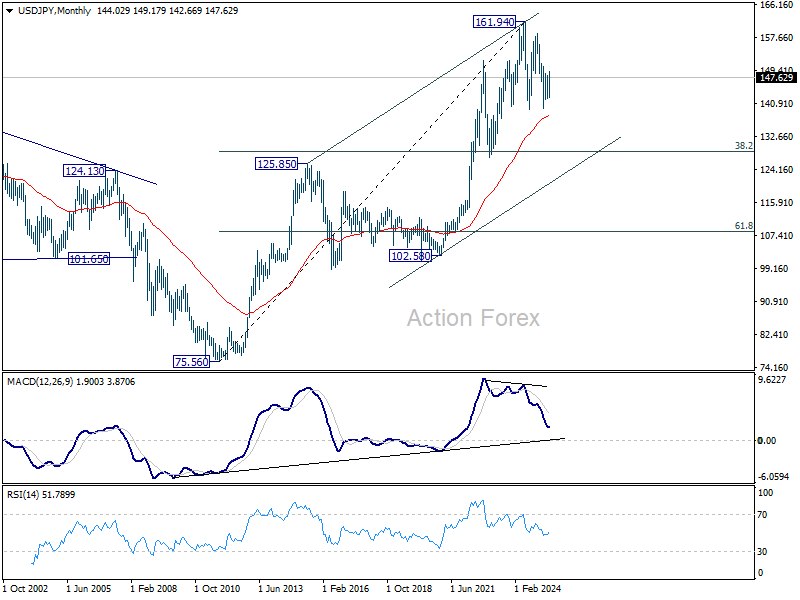

In the long term picture, there is no sign that up trend from 75.56 (2011 low) has completed. But then, firm break of 161.94 is needed to confirm resumption. Otherwise, more medium term range trading could still be seen.

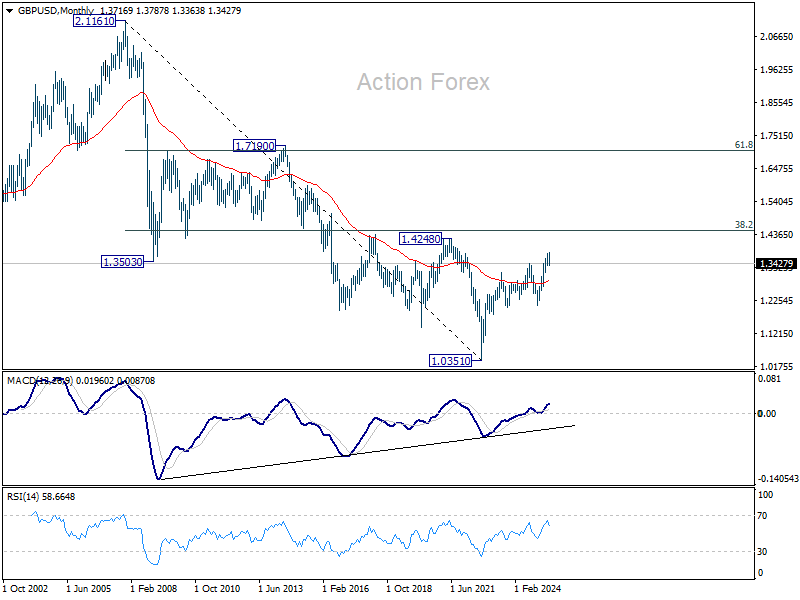

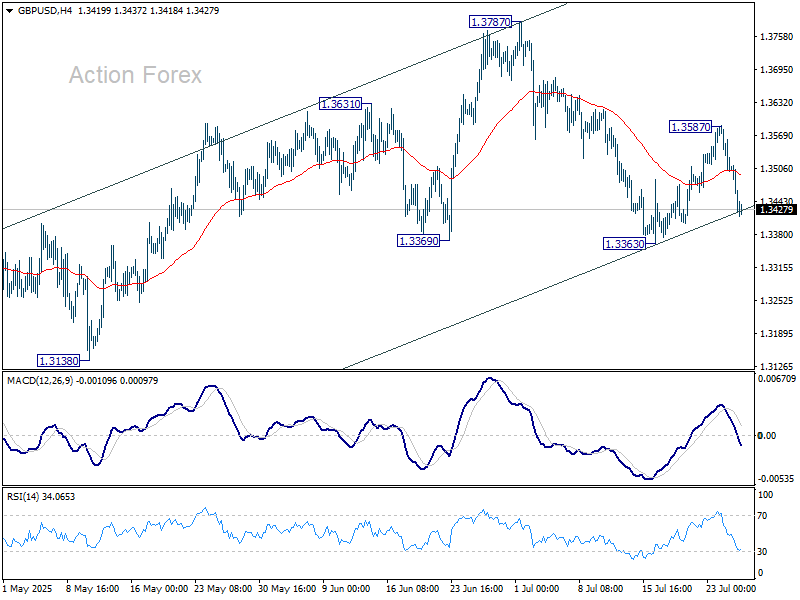

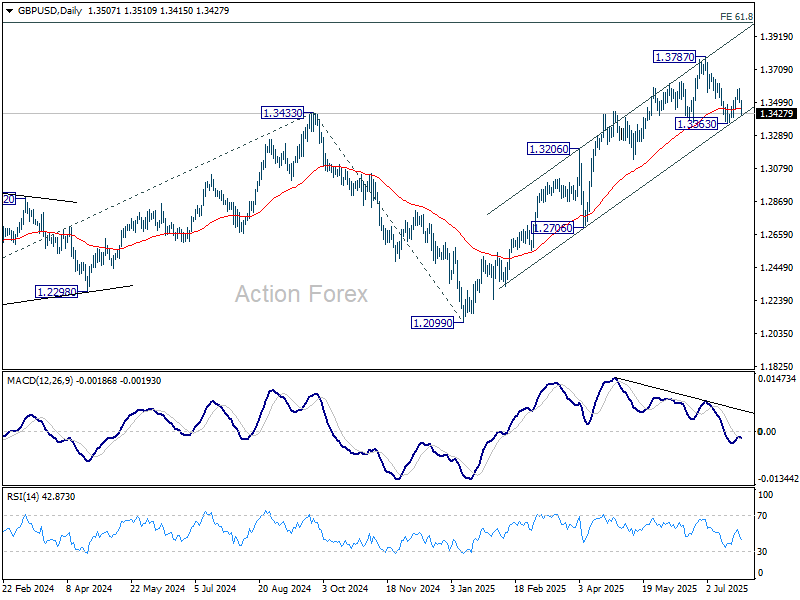

GBP/USD Weekly Outlook

GBP/USD rebounded to 1.3587 last week but reversed from there. Downside is held above 1.3363 support so far. Initial bias stays neutral this week first. On the upside, break of 1.3587 will target a retest on 1.3787 high. However, sustained break of 1.3363 will argue that it's already correcting the whole rally from 1.2099, and target 1.3206 resistance turned support.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3032) holds, even in case of deep pullback.

In the long term picture, for now, price actions from 1.0351 (2022 low) are still seen as a corrective pattern to the long term down trend from 2.1161 (2007 high) only. However, firm break of 1.4248 resistance (38.2% retracement of 2.1161 to 1.0351 at 1.4480) will be a strong sign of long term bullish reversal.