Sample Category Title

EU and US Reach a Deal, Euro Slips

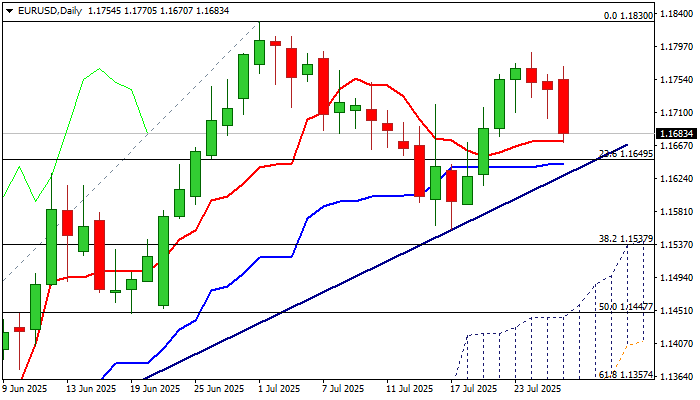

The euro is busy on Monday morning. EUR/USD started the week in positive territory and rose as much as 0.30%, but has reversed directions in the European session and is trading at 1.1677, down 0.54% on the day.

EU and the US reach a trade deal

US President Trump can add another feather to his MAGA cap, with news that the European Union and the United States reached a trade agreement over the weekend. President Trump had threatened to hit the EU with 30% tariffs if a deal wasn't reached by Aug. 1 and the specter of a nasty trade war between the largest two economies in the world has been averted.

A deal is of course good news but it's important to keep in mind that the sides have agreed to a framework agreement, which is thin on details. Some contentious issues remain, such as the US tariff of 50% on steel and aluminum.

The deal mirrors the US-Japan agreement which was announced last week. The US will eliminate some tariffs, such as on aircraft parts and generic drugs, but most European products will face a tariff of 15%, which will make European imports more expensive for US consumers. The EU has also agreed to increase investment in the US by $600 billion and purchase $750 billion in US energy products.

The German auto industry is one of the deal's big winners, as the 15% tariff will be easier to swallow than the current rate of 27.5%. The US-Japan deal puts a 15% tariff on Japanese motor vehicles, which would have put European automakers at a major disadvantage without a EU-US deal.

Trump is moving ahead and reaching deals with major trade partners, which is removing uncertainty and raising risk appetite. Investors are hoping that other key nations, such as Canada and South Korea, will follow soon with trade agreements with the US.

EUR/USD Technical

- EUR/USD has pushed below support at 1.1735 and 1.1710 and is testing 1.1677. Below, there is support at 1.1652

- There is resistance at 1.1768 and 1.1793

EURUSD 1-Day Chart, July 28, 2025

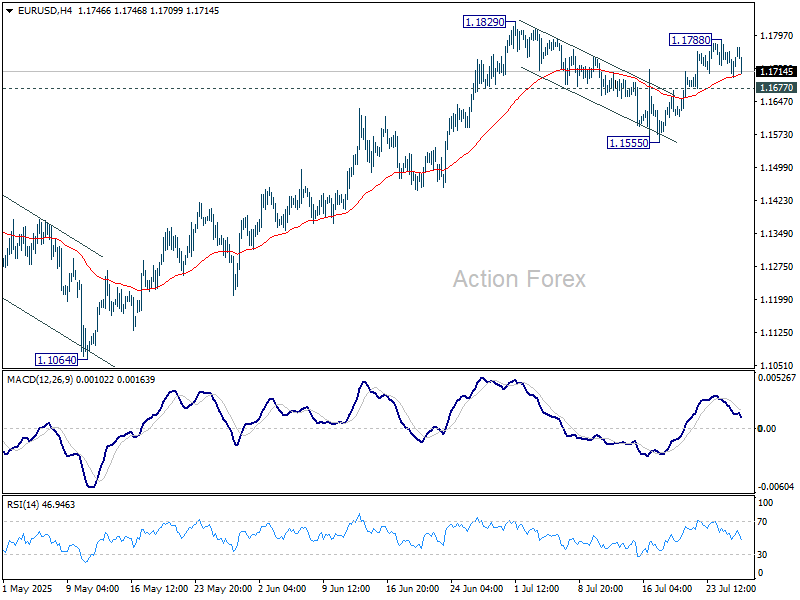

EUR/USD: Tests Strong Support Zone After a Sharp Drop

EURUSD lost ground on Monday after a gap-higher opening and short-lived gains, losing nearly 0.7% in late-Asian / early European trading.

Positive impact from US-EU trade deal was so far very limited, probably that markets have already positively reacted on anticipation that agreement will be reached before the deadline and after digesting the news about the whole package, signed in Scotland, which may not be in favor of the EU bloc.

Technical picture on daily chart weakened as 14-d momentum crossed in the negative territory, after bears cracked initial support at 1.1672 (daily Tenkan-sen) and eye more significant supports at 1.1650/30 zone (Fibo 23.6% of 1.1065/1.1830 uptrend / daily Kijun-sen / trendline support.

Violation of these levels would further weaken near-term structure and unmask key supports at 1.1556/37 (July 17 higher low / Fibo 38.2%), loss of which to complete bearish failure swing pattern and generate reversal signal.

Conversely, ability to hold above the trendline (ideally) would generate initial signal about a healthy correction before larger bulls return to play.

Res: 1.1703; 1.1770; 1.1789; 1.1830.

Sup: 1.1650; 1.1630; 1.1589; 1.1556.

Gold Declines as EU Strikes Trade Deal

Gold held steady at $3,330 per troy ounce on Monday following three consecutive days of declines. The metal faced downward pressure after news emerged of a trade agreement between the US and the EU, dampening investor interest in safe-haven assets.

On Sunday, the US and EU reached a broad trade deal, which includes a 15% tariff on most European goods, alongside commitments to invest hundreds of billions of dollars in American industry. This agreement mirrors last week’s US–Japan trade pact in structure.

Traders are now bracing for a busy week of economic events, with the Federal Reserve meeting at the centre of attention. While interest rates are expected to remain unchanged, markets will scrutinise any signals about a potential rate cut in September.

Key US labour market data will also be in focus, including JOLTS reports, ADP employment figures, and the crucial nonfarm payrolls release. Equally significant will be the PCE price index – the Fed’s preferred inflation gauge – which will indicate whether price pressures are intensifying amid new tariffs.

Technical Analysis: XAU/USD

H4 Chart:

The H4 chart shows XAU/USD forming a broad consolidation range around 3,375. After breaking downward today, the market reached its local downside target at 3,318. Following this, we anticipate a possible upward correction towards 3,375 (testing from below), before a renewed decline towards 3,312. This scenario is supported by the MACD indicator, with its signal line below zero and pointing sharply downward.

H1 Chart:

On the H1 chart, the market has achieved its local decline target at 3,318. Currently, an upward impulse is forming towards 3,349. A consolidation range near 3,346 may develop, with an upside breakout potentially extending gains to 3,375. Thereafter, a new downward wave towards 3,312 could emerge. The Stochastic oscillator aligns with this outlook, as its signal line is above 50 and rising sharply towards 80.

Conclusion

Gold remains under pressure amid shifting global trade dynamics, with technical indicators suggesting further volatility ahead. Traders should monitor key US data releases and signals from the Fed for directional cues.

Global Markets Mixed as US-EU Trade Deal Lifts Wall Street, JPY Slides Further, CHF/JPY (Chart of the Day)

In today’s Asia session, the S&P 500 and Nasdaq 100 E-mini futures recorded intraday rallies of 0.5% and 0.6%, respectively, extending gains from Friday, 25 July’s record-high closes. The rally was driven by optimism following reports of a US-EU trade agreement that has eased global market tensions.

US-EU avoid trade war with new tariff agreement

Late Sunday, media reports confirmed that the European Union and the United States have reached a breakthrough trade agreement after months of strained negotiations. The deal, announced by President Trump and European Commission President Ursula von der Leyen, sets a 15% tariff on EU exports to the US that includes automobiles, down from the previously threatened 30%. Full details are still pending release.

Nikkei slides amid political uncertainty in Japan

Asia-Pacific markets showed mixed performances. Japan’s Nikkei 225 dropped 0.9% intraday for a second consecutive loss, weighed down by domestic political instability. Local reports suggest the Liberal Democratic Party is moving to initiate a parliamentary vote to replace Prime Minister Ishiba.

US-China trade talks resume in Stockholm

The third round of US-China trade negotiations begins today in Stockholm. According to the South China Morning Post, both nations are expected to agree on extending the current tariff pause by 90 days, pushing the deadline beyond 12 August and signaling ongoing diplomatic engagement.

Hang Seng rebounds while Singapore market consolidates

Hong Kong’s Hang Seng Index gained 0.5%, recovering from Friday’s losses. Meanwhile, Singapore’s Straits Times Index declined 0.3% for a second straight session as investors paused after an 11% rally since 23 June.

Dollar recovers as euro reverses gains

The US dollar regained earlier intraday losses triggered by the US-EU trade news. The euro erased a 0.2% gain and now trades flat, while the Japanese yen and Swiss franc declined 0.2% and 0.3% respectively, with yen weakness tied to local political developments.

Gold rebounds slightly ahead of FOMC

Gold (XAU/USD) edged up 0.1% intraday after a three-day slide. Traders remain cautious as they weigh trade deal optimism against anticipation of the upcoming FOMC meeting on 30 July. Market participants are watching for signs that Fed Chair Powell may pivot toward a more dovish stance, potentially setting up a rate cut at the September meeting.

Economic data releases

Fig 1: Key data for today’s Asia mid-session (Source: MarketPulse)

Chart of the day – Bullish flag breakout for CHF/JPY

Fig 2: CHF/JPY minor & medium-term trends as of 28 July 2025 (Source: TradingView)

The CHF/JPY cross pair staged a minor bullish flag breakout last Friday, 25 July, with a positive follow-through in today’s Asia session.

In addition, the hourly RSI momentum indicator has continued to hover above its 50 level and parallel ascending trendline support without hitting its overbought region (above 70) at this juncture.

These observations suggest that minor corrective consolidation in place since 16 July is likely to have ended, and the CHF/JPY may be in the process of staging a potential fresh bullish impulsive up move sequence within its medium-term uptrend phase (see Fig 2).

Watch the 185.10 short-term pivotal support for the next intermediate resistances to come in at 186.70, 187.30/187.70, and 188.80.

On the flip side, a break below 185.10 negates the bullish tone for a slide to expose the next intermediate support at 183.90/183.45 (also the 20-day moving average).

Europe and the US Sign Trade Agreement, EUR/USD Declines

The past weekend was marked by the official signing of a trade agreement between the United States and Europe, as announced by US President Donald Trump and President of the European Commission Ursula von der Leyen following their meeting in Scotland.

According to reports, the agreement is based on a 15% baseline tariff on goods exported from Europe to the United States, with certain exemptions. As previously reported, a trade agreement with a 15% baseline tariff had earlier been concluded between the US and Japan.

According to President Trump:

→ under no circumstances did he allow the baseline tariff for Europe to fall below 15%;

→ the European Union committed to investing in the US economy, purchasing weapons, and importing energy resources.

The financial markets’ reaction to this news is noteworthy:

→ European stock indices opened the week with a bullish gap, reflecting relief that previously feared tariffs of up to 30% did not materialise;

→ the EUR/USD pair is exhibiting bearish momentum this morning.

Technical Analysis of the EUR/USD Chart

As indicated by the black arrow, bearish sentiment intensified on Monday morning, pushing the pair towards the 1.1700 level, which had previously acted as resistance in mid-July.

From the perspective of the ascending channel (shown in blue), its median line is currently acting as a resistance level – following contact with it, a short-term rally was broken (highlighted in purple). This reinforces the notion that bears are currently in control.

Given the above, we could suggest that, should bearish sentiment persist on the EUR/USD chart, we may soon witness an attempt to break through the 1.1700 support level. A successful breach could open the path for further downside movement of the euro against the dollar, towards the lower boundary of the channel.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Gold and Oil Prices Ease – Market Awaits Fresh Catalysts

Gold price started a fresh decline below $3,380. WTI crude oil is also down and remains at risk of more losses below $64.60.

Important Takeaways for Gold and WTI Crude Oil Prices Analysis Today

- Gold price climbed higher toward the $3,430 zone before there was a sharp decline against the US Dollar.

- A key bearish trend line is forming with resistance near $3,350 on the hourly chart of gold at FXOpen.

- WTI crude oil price continued to decline below the $66.00 support zone.

- It traded below a connecting bullish trend line with support at $65.60 on the hourly chart of XTI/USD at FXOpen.

Gold Price Technical Analysis

On the hourly chart of gold at FXOpen, the price climbed above the $3,380 resistance. The price even spiked above $3,400 before the bears appeared.

A high was formed near $3,432 before there was a fresh decline. There was a move below the $3,380 support level. The bears even pushed the price below the $3,350 support and the 50-hour simple moving average.

It tested the $3,325 zone. A low was formed near $3,325 and the price is now showing bearish signs. There was a minor recovery wave towards the 23.6% Fib retracement level of the downward move from the $3,433 swing high to the $3,325 low.

However, the bears are active below $3,342. Immediate resistance is near $3,350. There is also a key bearish trend line forming with resistance near $3,350.

The next major resistance is near the $3,380 zone. It is close to the 50% Fib retracement level of the downward move from the $3,433 swing high to the $3,325 low. The main resistance could be $3,410, above which the price could test $3,432. The next major resistance is $3,450.

An upside break above $3,450 could send the gold price towards $3,465. Any more gains may perhaps set the pace for an increase toward the $3,480 level.

Initial support on the downside is near the $3,325 level. The first major support is near the $3,310 level. If there is a downside break below it, the price might decline further. In the stated case, the price might drop towards the $3,265 support.

WTI Crude Oil Price Technical Analysis

On the hourly chart of WTI crude oil at FXOpen, the price struggled to continue higher above $67.50. The price formed a short-term top and started a fresh decline below $66.00.

There was a steady decline below the $65.80 pivot level. The bears even pushed the price below $65.00 and the 50-hour simple moving average. The price traded below a connecting bullish trend line with support at $65.60.

Finally, the price tested the $64.75 zone. The recent swing low was formed near $64.73, and the price is now consolidating losses. On the upside, immediate resistance is near the $65.60 zone. It is close to the 50% Fib retracement level of the downward move from the $66.42 swing high to the $64.73 low.

The main resistance is $65.80. A clear move above it could send the price towards $66.40. The next key resistance is near $67.50. If the price climbs further higher, it could face resistance near $70.00. Any more gains might send the price towards the $72.00 level.

Immediate support is near the $64.60 level. The next major support on the WTI crude oil chart is near $63.20. If there is a downside break, the price might decline towards $60.00. Any more losses may perhaps open the doors for a move toward the $55.00 support zone.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

US and European Union Struck a Trade Agreement

Markets

And it’s a deal. The US and European Union struck a trade agreement yesterday, concluding months of back and forth negotiations. Both parties agreed an across-the-board 15% US import levy, covering all goods. That includes cars (which are currently struck by a 27.5% tariff) and according to EC president von der Leyen and senior US officials also semiconductors and pharmaceuticals. US president Trump recently said global tariffs on the latter could be as high as 200% over time after a so-called Section 232 probe comes due over the next three weeks. The 15% does not cover EU’s steel and aluminum, which remain subject to a 50% duty. Securing the 15% instead of the 30% that was set to kick in if no deal was found by August 1 required a buy-in though. The EU agreed to buy $750bn in American energy products over the next three years, to invest $600bn in the US and purchase “a vast amount” of US military equipment. Buying off a lower tariff is also what Japan did with a $550bn investment fund. For now, though, it appears that stocks are the only category actually enjoying the good news. European futures point to a higher open of around 1%+. Bund futures trade weaker (ie. yields to open higher) but are off the intraday lows. We nevertheless believe the weekend breakthrough further strengthened the bottom below European yields, but at the front and the long end of the curve. The euro gapped higher at the Asian open this morning to EUR/USD 1.178 but immediately fell prey to some modest profit-taking. The currency pair is currently back at Friday’s (which, by the way, was an uneventful session) closing level of 1.174. These market moves have an aura of buy the rumour, sell the fact. Speculation was already lingering by end last week of the US and EU nearing an agreement in which the latter was willing to accept a 15% rate. But that doesn’t make it less disappointing that EUR/USD not even came close to the July high of 1.1829. We’ll need confirmation in European and US dealings but it suggests the euro is taking a short-term breather. That also means any potential next upleg in EUR/USD would have to come from dollar weakness. A heavy eco calendar this week at least provides plenty of opportunities. The US update includes JOLTS job openings and consumer confidence tomorrow, Q2 GDP figures and the FOMC decision on Wednesday and the payrolls report on Friday. Several EA member states print growth and inflation numbers over the next days. Trade will remain a critical topic this week, even as the US having secured deals with major trading partners Japan and EU ahead of August 1. Talks with China continue today with a.o. the aim of extending the trade truce beyond the August 12 deadline. Meanwhile, the earnings season rolls into its busiest week (Microsoft, Apple, Amazon and Meta Platforms …).

News & Views

Rating agency Moody’s upgraded Turkey’s credit rating to Ba3 from B1 with a stable outlook. Turkey’s rating is now three notches below investment grade and on par with the ones assigned by Fitch and S&P (both BB-). The upgrade reflects strengthening track record of effective policy making, more specifically in the central bank’s adherence to monetary policy, Moody’s said. That should durably ease inflationary pressures, reduces economic imbalances, and gradually restores local depositor and foreign investor confidence in the Turkish lira. The agency noted a reduced yet still-present risk of policy reversal in the coming years. On a macro level, Moody’s foresees annual inflation to drop to 30% by year’s end and to around 20% by end 2026. GDP growth is expected at 2.2% for this year, below potential growth estimates ranging between 3.5% and 4.5%.

Japan’s top chief negotiator Akazawa said he expects only 1-2% of the recently agreed upon $550bn US fund to be in the form of actual investment, Bloomberg reported. It is on this percentage that investment profits would be split at a 90-10 ratio with the US collecting the larger part. This investment fund was a key pillar in the US-Japanese trade deal concluded last week with which Japan bought off a lower import tariff of 15% (instead of 25%). But being conceptually new, its details remain vague. Akazawa said the bulk of the funds would be dispersed via loans, on which Japan will be earning interest payments, and through loan guarantees, on which – if nothing happens – it will be collecting fees.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1710; (P) 1.1735; (R1) 1.1768; More...

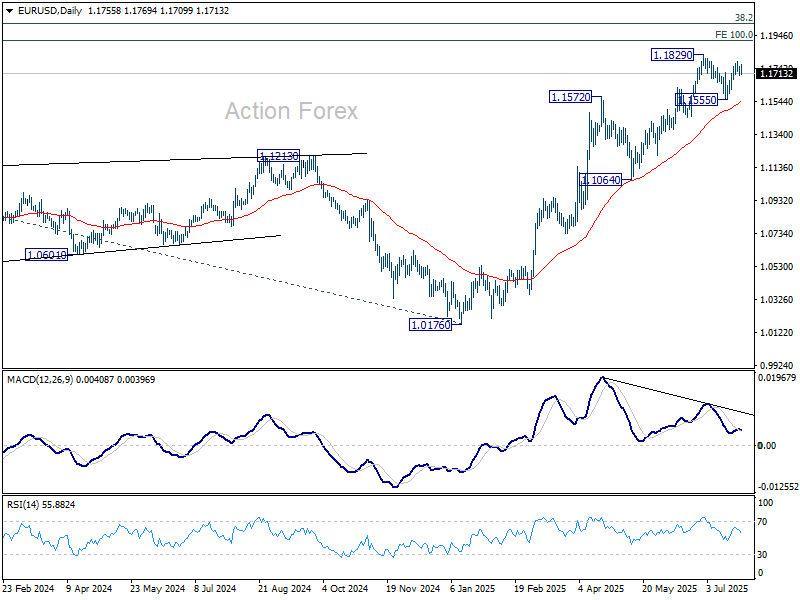

Intraday bias in EUR/USD remains neutral for the moment. On the upside, above 1.1788 will bring retest of 1.1829. Firm break there will will resume whole rally from 1.0176, and target 1.1916 projection level. However, break of 1.1677 will turn bias to the downside, and extend the corrective pattern from 1.1829 with another falling leg.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

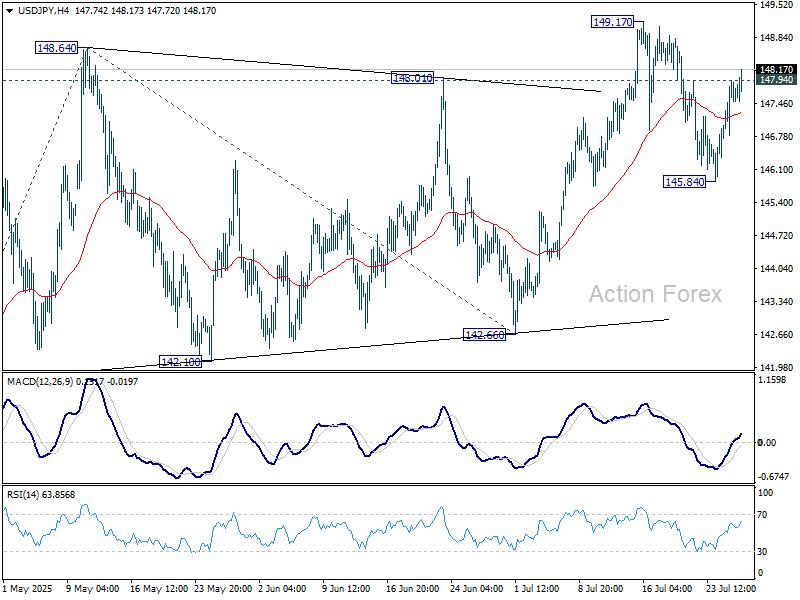

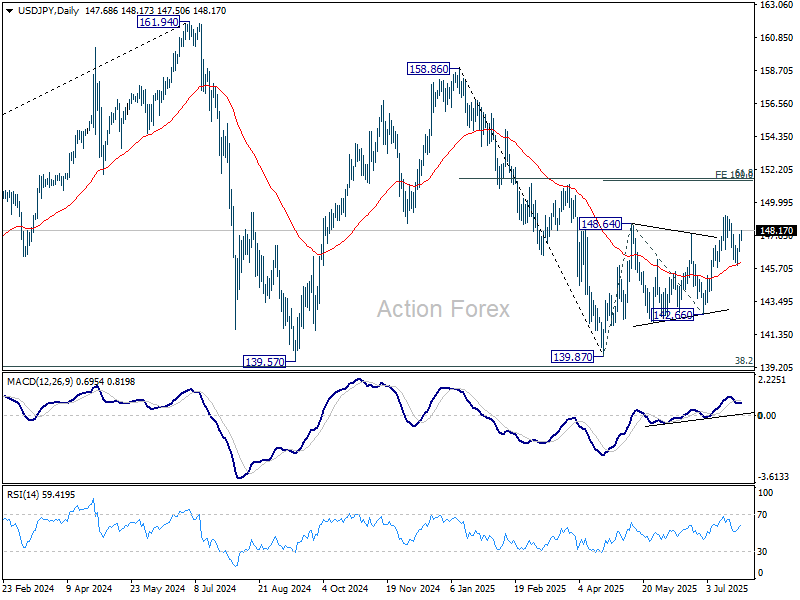

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.03; (P) 147.48; (R1) 148.13; More...

USD/JPY's break of 147.94 resistance suggests that pullback from 149.17 has already completed at 145.84. Intraday bias is back on the upside for retesting 147.94 first. Firm break there will resume whole rise from 139.87. Next target is 100% projection of 139.87 to 148.64 from 142.66 at 151.43, which is close to 151.22 fibonacci level. For now, risk will stay on the upside as long as 145.84 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3395; (P) 1.3458; (R1) 1.3500; More...

Intraday bias in GBP/USD stays neutral for the moment. On the upside, break of 1.3587 will target a retest on 1.3787 high. However, sustained break of 1.3363 support will argue that it's already correcting the whole rally from 1.2099, and target 1.3206 resistance turned support.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3045) holds, even in case of deep pullback.