Sample Category Title

Elliott Wave Update: EURUSD Favors Weakness In To Support Zone

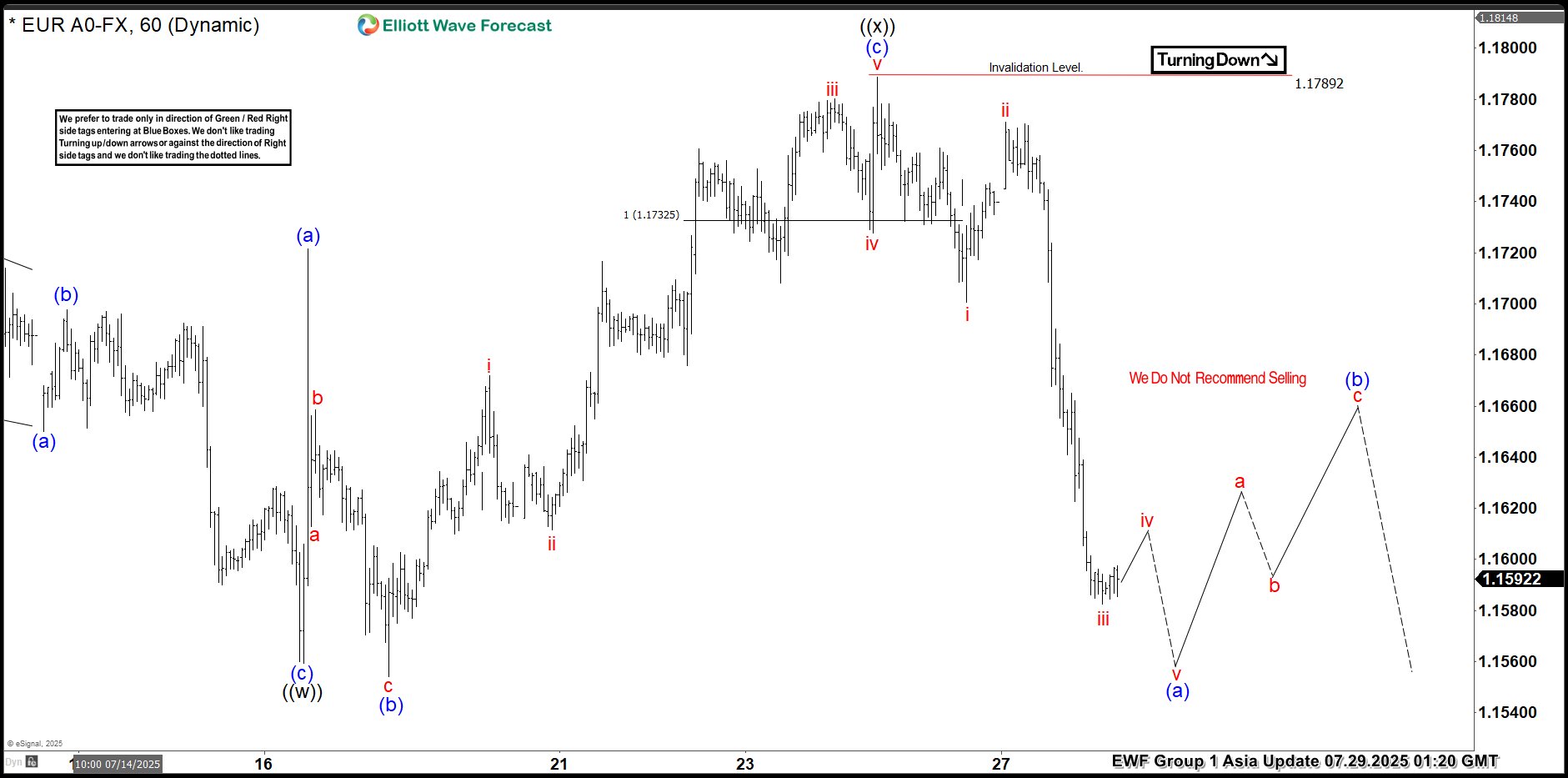

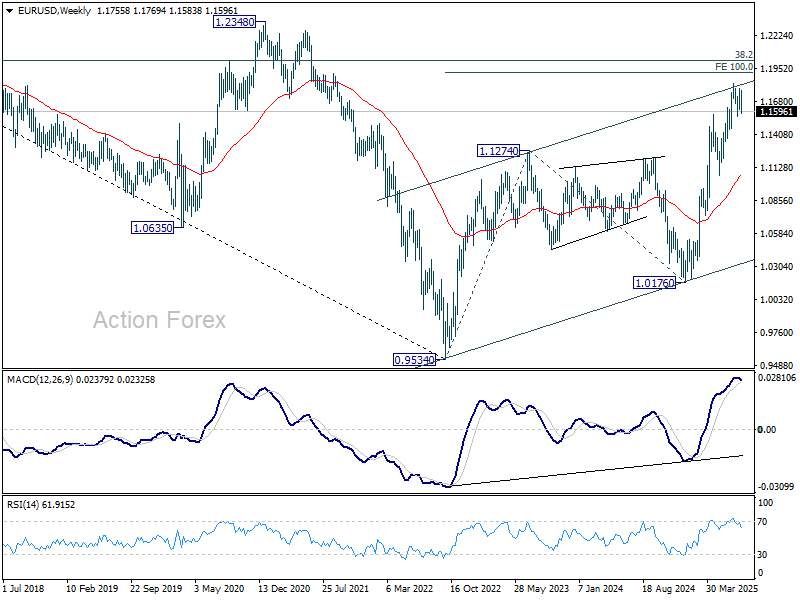

The EURUSD favors upside in 3 swings from September-2022 low & should extend towards 1.1929 or higher against 1.13.2025 low. In 4-hour, it favors double correction lower from 7.01.2025 high to correct 5.12.2025 low. It favors short term pullback in to 1.1512 – 1.1340 area in 7 swing pullback before continue rally in cycle from 1.13.2025 low. Above January-2025 low, it ended (1) at 1.0533 high, (2) at 1.0210 low, (3) at 1.1573 high, (4) at 1.1065 low & favors higher in (5). Within 4-hour, it placed 1 at 1.1830 high & correcting in 2 as double three correction before two more highs. It placed ((w)) at 1.1559 low in 3 swings zigzag correction. In ((w)), it ended (a) at 1.1659 low, (b) at 1.1714 high & (c) at 1.1559 low of 7.16.2025. Later, it unfolded expanded flat correction in ((x)) that ended at 1.1788 high of 7.24.2025. Within ((x)), it placed (a) at 1.1721 high, (b) at 1.1554 low & (c) in 5 swings at 1.1788 high.

Currently, it favors downside in ((y)) of 2 & expect sideways to lower in to support zone. It favors zigzag correction lower in ((y)) to finish 2 in to extreme area before resume rally. Short term, it favors downside in (a) of ((y)) since 7.24.2025 high. In (a), it placed i at 1.1700 low, ii at 1.1771 high & favors downside in iii of (a) towards 1.1576 – 1.1569 area before bounce in iv. It expects a bounce soon in iv followed by one more push lower in v to finish (a) in 5 swings. Wave (a) of ((w)) should end near 1.1578 before bounce in (b) in 3 or 7 swings connector. The bounce in (b) should fail below 1.1788 high to extend lower in (c) in to 1.1512 – 1.1340 area to finish correction. It should find next support in to that area to rally higher as the part of daily sequence targeting 1.1929 or higher. We like to buy in to that area for next leg higher or at least 3 swings bounce. If it breaks above 7.01.2025 high, it expects two more highs to finish cycle from January-2025 before next pullback start.

EURUSD – 60-Minute Elliott Wave Technical Chart:

EURUSD Elliott Wave Technical Video:

https://www.youtube.com/watch?v=pCVQ34fxCHM

EUR/JPY Daily Outlook

Daily Pivots: (S1) 171.52; (P) 172.71; (R1) 173.36; More...

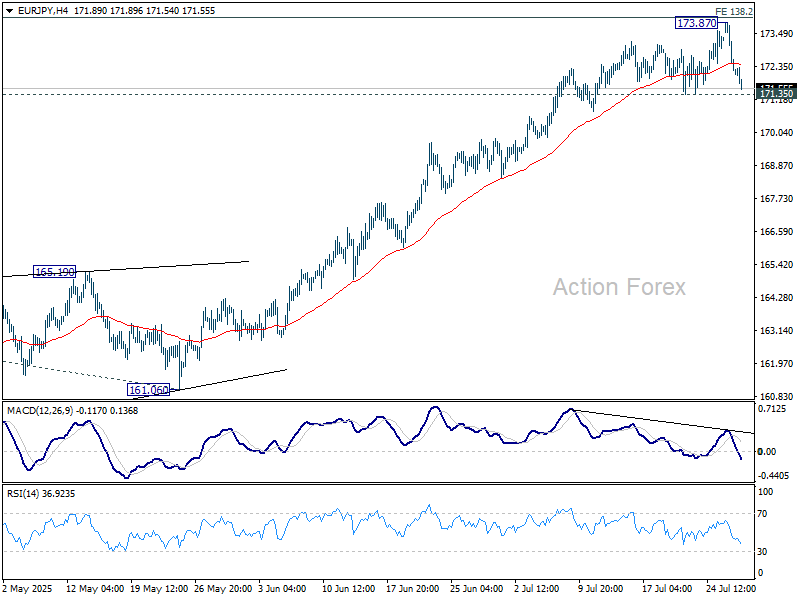

Intraday bias in EUR/JPY is turned neutral first with current steep retreat. Further rise could still be seen as long as 171.35 support holds. Break of 173.87 should pave the way to retest 175.41 high. However, considering bearish divergence condition in 4H MACD, decisive break of 171.35 will confirm short term topping, after rejection by 138.2% projection of 154.77 to 164.16 from 161.06 at 174.03. Deeper pullback should then be seen towards 55 D EMA (now at 168.62).

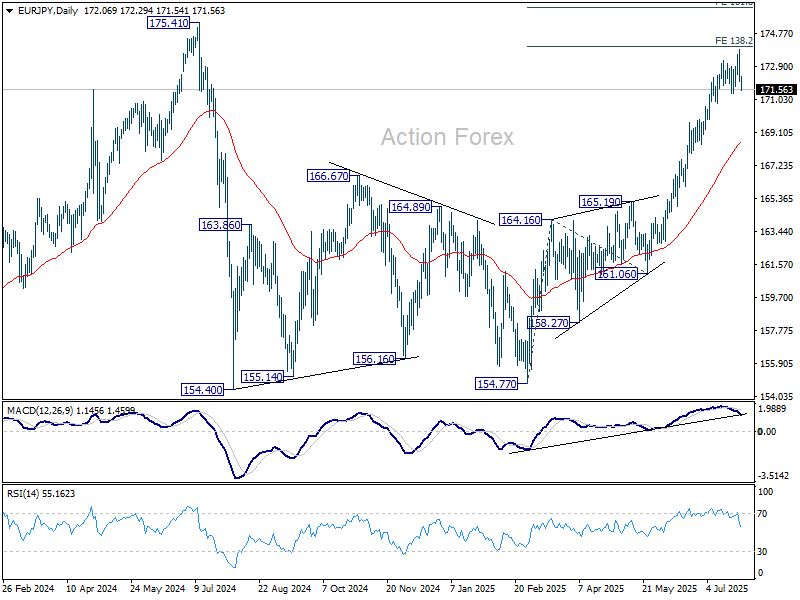

In the bigger picture, considering current strong momentum as seen in the rally from 154.77, corrective pattern from 175.41 could have already completed. Decisive break there will confirm long term up trend resumption. Next target is 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, rejection by 175.41, followed by firm break of 55 D EMA (now at 168.62) will delay this bullish case.

Pre-BoJ Positioning Lifts Yen, Dollar Holds Top Spot

Yen recovered broadly in Asian session, likely helped by short-covering ahead of Thursday’s BoJ policy decision. Traders may be bracing for surprises in the central bank’s updated economic projections, particularly after last week’s US-Japan trade deal lifted some trade-related uncertainty. Although no rate hike is expected, any forward-leaning language suggesting rate hikes in the near term could jolt markets and catch Yen bears off guard.

Across the broader currency markets, Euro remains the worst underperformer for the week after retracing sharply from recent highs. Nevertheless, yesterday’s post-deal drop was not a collapse but rather a technical correction of gains built over the past month. Swiss Franc and Kiwi are also soft, while Dollar continues to lead the majors. Loonie and Yen are gaining ground, while Sterling and Aussie hover in the middle.

On the trade front, US President Donald Trump announced on Monday that countries lacking bilateral deals will soon face a flat tariff of 15–20% when exporting to the US The move aims to simplify trade enforcement and boost U.S. leverage in negotiations. “We’re going to be setting a tariff for essentially the rest of the world,” Trump declared, making clear the US won’t wait on a patchwork of slow-moving talks.

South Korea, meanwhile, is still rushing to avoid the looming 25% tariff threat. Finance Minister Koo Yun-cheol said today he will travel to Washington to pursue a mutually beneficial trade agreement. Koo joins a delegation of senior officials in last-ditch talks with UScounterparts, including Treasury Secretary Bessent and Commerce Secretary Lutnick.

Meanwhile, top US and Chinese trade officials met in Stockholm on Monday for more than five hours of negotiations. While no breakthroughs were announced, both sides signaled that talks would continue Tuesday. Expectations are rather low, as US Trade Representative Jamieson Greer said the goal was to ensure proper implementation of existing deals and improve access to key materials.

Technically, Gold weakened this week following Dollar's rally. Immediate focus is now on 3039.64 support. Firm break there will suggest that rebound from 3248.21 has completed at 3438.89. Deeper decline should then be seen to 3248.21 and possibly below. After all, Gold is extending the corrective pattern from 3499.79 high, which would likely continue for a while.

In Asia, at the time of writing, Nikkei is down -1.04%. Hong Kong HSI is down -1.02%. China Shanghai SSE is flat. Singapore Strait Times is down -0.59%. Japan 10-year JGB yield is down -0.004 at 1.566. Overnight, DOW fell -0.14%. S&P 500 rose 0.02%. NASDAQ rose 0.33%. 10-year yield rose 0.034 to 4.420.

Ranges hold in EUR/USD and stocks even as US-EU deal slammed

Investor sentiment cooled overnight as markets reassessed the US–EU trade agreement more critically. While initially welcomed for averting harsher tariff scenarios, the deal is now being viewed by many as a near-term drag on European growth. What once seemed like a "good deal" in absolute terms is now being interpreted as a relative setback for the EU economy.

Political backlash within Europe has intensified. French Prime Minister Francois Bayrou called the framework a "dark day" for Europe, accusing the bloc of capitulating to US demands. German Chancellor Friedrich Merz also warned that the tariffs embedded in the deal would inflict “significant” damage on Germany’s export-driven economy.

Despite the rhetoric, equity market reactions remained contained. Germany’s DAX lost -1.02% and France’s CAC fell -0.43%, but both indexes remain within tight sideways trading ranges. In the US, DOW dipped slightly by -0.14% while S&P 500 eked out a small gain of 0.02%, signaling that investors don’t see the agreement as overwhelmingly skewed toward American interests either.

EUR/USD came under strong selling pressure yesterday. However, the move is seen as part of the corrective pattern from 1.1829 short term top. Larger up trend is still expected to resume later. This view will hold as long as 55 D EMA (now at 1.1538) holds.

That said, technical headwinds are clearly building. The pair already touching the long term rising channel resistance, and nearing a long-term Fibonacci projection level at 1.1916, 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Bearish divergence on D MACD suggests fading momentum, recent up trend is clearly running out of steam. Sustained break of 55 D EMA will argue that it's already in a larger scale correction after rejection by 1.1916.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 171.52; (P) 172.71; (R1) 173.36; More...

Intraday bias in EUR/JPY is turned neutral first with current steep retreat. Further rise could still be seen as long as 171.35 support holds. Break of 173.87 should pave the way to retest 175.41 high. However, considering bearish divergence condition in 4H MACD, decisive break of 171.35 will confirm short term topping, after rejection by 138.2% projection of 154.77 to 164.16 from 161.06 at 174.03. Deeper pullback should then be seen towards 55 D EMA (now at 168.62).

In the bigger picture, considering current strong momentum as seen in the rally from 154.77, corrective pattern from 175.41 could have already completed. Decisive break there will confirm long term up trend resumption. Next target is 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, rejection by 175.41, followed by firm break of 55 D EMA (now at 168.62) will delay this bullish case.

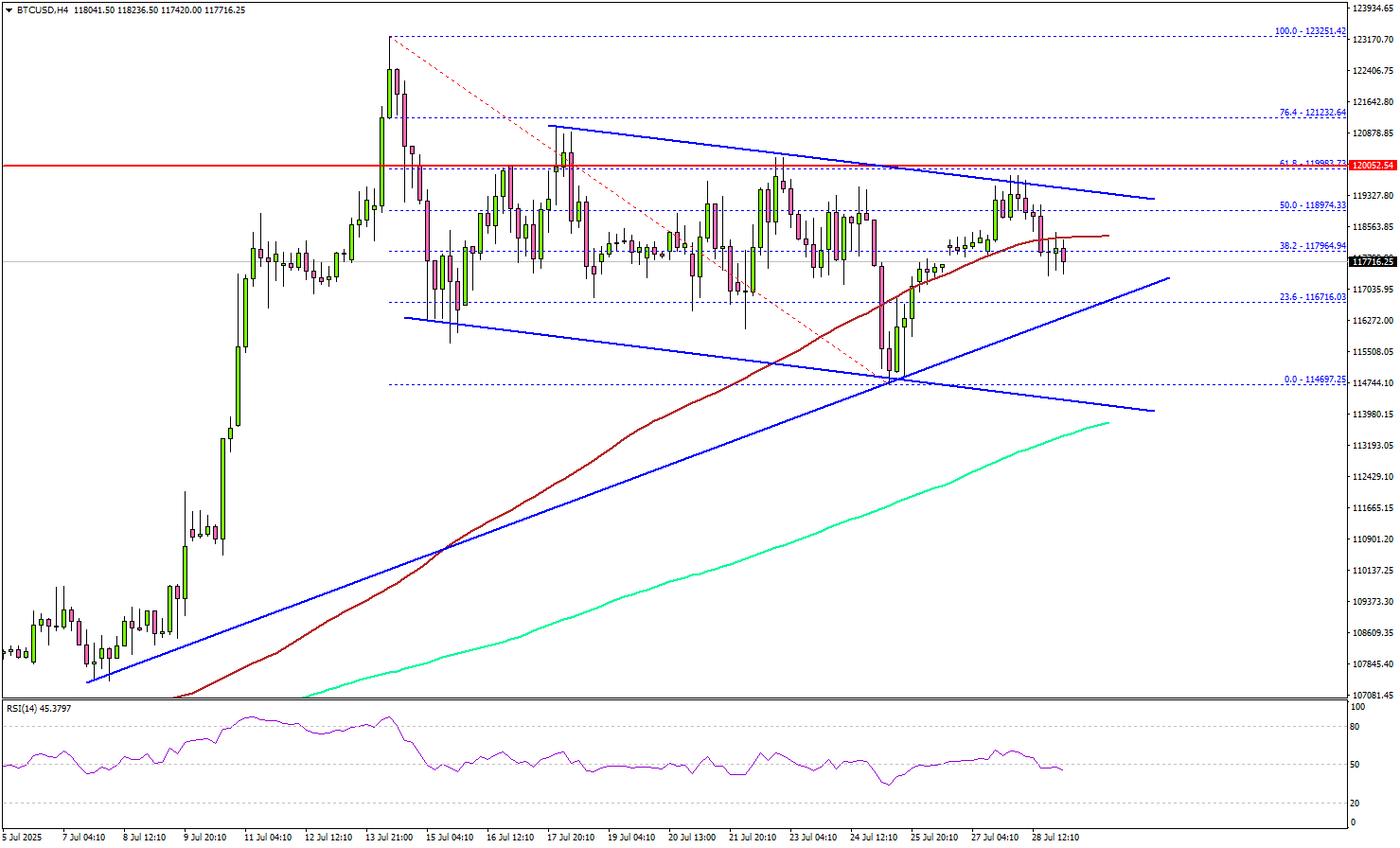

Bitcoin Consolidates Gains, But Bulls Remain In Control

Key Highlights

- Bitcoin rallied above the $115,000 resistance zone before a consolidation phase.

- BTC/USD is following a declining channel with support at $113,500 on the 4-hour chart.

- Ethereum climbed higher above $3,800 resistance.

- XRP price rallied above the $3.20 level and recently corrected gains.

Bitcoin Price Technical Analysis

Bitcoin price started a fresh increase above the $115,000 zone against the US Dollar. BTC was able to climb above the $118,000 and $120,000 resistance levels.

Looking at the 4-hour chart, the price settled above the $115,000 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The bulls even pumped the price above the $122,000 resistance.

A new all-time high was formed near $123,200 and the price is now correcting gains. Immediate support is near $116,700 and a connecting bullish trend line on the same chart.

A downside break below $116,700 might send BTC toward the $115,000 support. Any more losses might send the price toward the $113,500 support zone. There is also a declining channel in place with support at $113,500.

On the upside, the price could face resistance near the $119,500 level. The next key resistance is $120,500. A successful close above $120,500 might start another steady increase.

In the stated case, the price may perhaps rise toward the $122,500 level. Any more gains might call for a test of $123,200.

Looking at Ethereum, the bulls seem to be in control, and they were able to push the price above the $3,800 resistance zone.

Today’s Economic Releases

- US Housing Price Index for May 2025 (MoM) - Forecast -0.2%, versus -0.4% previous.

Ranges hold in EUR/USD and stocks even as US-EU deal slammed

Investor sentiment cooled overnight as markets reassessed the US–EU trade agreement more critically. While initially welcomed for averting harsher tariff scenarios, the deal is now being viewed by many as a near-term drag on European growth. What once seemed like a "good deal" in absolute terms is now being interpreted as a relative setback for the EU economy.

Political backlash within Europe has intensified. French Prime Minister Francois Bayrou called the framework a "dark day" for Europe, accusing the bloc of capitulating to US demands. German Chancellor Friedrich Merz also warned that the tariffs embedded in the deal would inflict “significant” damage on Germany’s export-driven economy.

Despite the rhetoric, equity market reactions remained contained. Germany’s DAX lost -1.02% and France’s CAC fell -0.43%, but both indexes remain within tight sideways trading ranges. In the US, DOW dipped slightly by -0.14% while S&P 500 eked out a small gain of 0.02%, signaling that investors don’t see the agreement as overwhelmingly skewed toward American interests either.

EUR/USD came under strong selling pressure yesterday. However, the move is seen as part of the corrective pattern from 1.1829 short term top. Larger up trend is still expected to resume later. This view will hold as long as 55 D EMA (now at 1.1538) holds.

That said, technical headwinds are clearly building. The pair already touching the long term rising channel resistance, and nearing a long-term Fibonacci projection level at 1.1916, 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Bearish divergence on D MACD suggests fading momentum, recent up trend is clearly running out of steam. Sustained break of 55 D EMA will argue that it's already in a larger scale correction after rejection by 1.1916.

Gold Shows Signs of Fatigue Inside Established Range

Gold has been in a $250 range since hitting new all-time highs after Liberation Day in April 2025.

Despite many signs of new trends very close to beginning, the only true thing is that Gold has not been able to find a trend.

The question that may arise, particularly after last week's rebound on the 2025 upward trendline, which failed to even touch the All-time high record, is: Do Gold bulls have enough fundamental resources to push the metal to new highs?

The weekly session has started with some great volatility, particularly as the US Dollar is breaking higher in a strong manner and with the EU-US Trade Deal being close to concluded.

This volatility has been negative for Gold which had been going up on more tense global trade outlooks. As a matter of fact, global trade is felt to be looking better as more Deals are reached.

Before taking a look at the technicals, let's see if positioning helps us to get a good idea of what is going on.

Client positioning in Gold

Client Positioning for Gold, July 28, 2025 – Source: OANDA Labs

Client positioning in Gold is overweight long. Positioning tends to typically be an inversely correlated tool to imminent Market moves – If players are long, an inability to add to positions emphasis further reversals, in this case it gives a bearish tilt.

Now turning to Technicals for the precious metal

Gold Daily Chart

Gold Daily Chart, July 28, 2025 – Source: TradingView

Gold was on a strong move towards that previously pointed to potentially hitting the all-time highs – A spike at the $3,439 highs got met with an Engulfing bearish candle after the reaching of the US-Japan Trade deal.

Since, an over-$100 correction has brought the precious metal below the 2025 upwards trendline, particularly after opening down on the weekly open, just below its key 50-Day Moving average ($3,342).

Buyers having failed to hold the rally above it gives more emphasis to the ongoing selling – However the action is still rangebound with the prices entering the $3,300 to $3,320 Support Zone.

Any close below would look at the end-June $3,250 level that served as key support, with no other major support until $3,120 May lows

Gold 4H Chart

Gold 4H Chart, July 28, 2025 – Source: TradingView

The weekly open has quickly built towards the Key support mentioned on the Daily timeframe, which leaves a last hurdle for the bulls to support the range before a potential $50 breakdown.

$3,300 is not a pivot point to underestimate, and retracements in Gold tend to be short – Therefore even if the level breaks, it will be essential to see where other buyers step in ($3,250 is the next key support).

There has been a long-tailed wick at the morning session selling candle leading to a small rebound – Any rebound from here will have to be strong enough to bring prices above the $3,350 Pivot Zone in confluence with the 4H MA 200.

Any selloff from there would open the door for a more concrete downwards reversal in a break-retest fashion which would infer a need for further analysis.

Reactions from here are a major key for the action to come.

Gold 30m Chart

Gold 30M Chart, July 28, 2025 – Source: TradingView

Looking even closer, the battle is nnot won yet for the Bears.

The formation of a intermediate-downwards channel shows a potential test of its higher bound which coincides with the 30m 50-period MA ($3,330); a first hurdle to break for the range to hold and to give a chance to regain higher levels.

That MA is actually a key to intraday momentum, having served as resistance for sellers to step in so keep that one closely in check.

Safe Trades!

AUDUSD Weakens as Markets Brace for a Pivotal Week

A fundamental overview of the AUD to prepare for a key week

This week is promised to be a major mover for the Forex market, and the AUD is far from being excluded from potential movement.

Between Central Bank meetings, including Wednesday’s FOMC and Australia’s Quarterly Inflation data, AUD Traders must stay prepared for the upcoming action.

The Royal Bank of Australia held its Main Rate at 3.85% at the beginning of July, citing higher inflation and more than decent employment figures. However, the week after, the figures were not as good.

The initial reaction was stronger for the AUD, but the motion is starting to show some change right after the pair hit some 8-month highs.

Some headwinds are in the longer-term outlook for the Currency pair. Australian funds are increasingly hedging their foreign investments (particularly with the US), which would typically increase fundamental demand for the currency.

This is already taking place, as evidenced by the consistent and stable uptrend formed after the Liberation Day troughs. But markets are forward-looking, and traders need to adapt fast.

The upcoming Wednesday FOMC meeting will be a major key to the pair's dynamics, with a focus on the FED's communication.

The RBA still has about 60 bps of cuts priced in for the rest of the year (with a cut largely priced in for the next meeting), and this pricing is subject to much change, particularly with the inflation data coming up. FYI, the upcoming RBA meeting will be taking place on August 12.

AUDUSD Technical Analysis

AUDUSD Daily Chart

AUDUSD Daily Chart, July 28, 2025 – Source: TradingView

The Aussie had invalidated a double top formation as the US Dollar saw some newfound weakness in the first trading days of the past week, taking the pair to some 8-month highs (0.66250) – failed continuation downwards brought some strong buying in the pair (failed patterns tend to be good signs of strong reversals).

However, the action has reversed again as the Greenback saw a reversal higher after Wednesday trading and this has marked another, more concrete top in AUDUSD with the forming of a bearish divergence.

Daily momentum is neutral but now tilting downwards. With the 50-Day MA acting as immediate support (0.6510), sellers will want to get a stronger push to regain longer-term control of the action.

AUDUSD 4H Chart

AUDUSD 4H Chart, July 28, 2025 – Source: TradingView

Markets have retracted sharply from the last highs and actually passing below the tighter channel lower bound (dotted blue line).

This itself will be attracting some trend-reversal traders but the action has to break conclusively below the Immediate Pivot Zone (level detailed below) before the downwards reversal shows an even higher probability of continuation.

Nevertheless, a failure to continue the selling momentum will point to rangebound action due to the 3 tops and 2 bottoms formed through the past two weeks of trading.

Levels to place on your charts:

Support Levels:

- Immediate Pivot Zone (0.65150 to 0.65350) - above + bullish, below + bearish

- 0.6485 mini support

- 0.6450 intermediate lows

- 0.63 to 0.64 Main Daily Support

Resistance Levels:

- Swing Resistance 0.6570 to 0.6590

- Wednesday Highs 0.66250

- Daily resistance 0.6670 to 0.6740 and high of upwards Channel

AUDUSD 1H Chart

AUDUSD 1H Chart, July 28, 2025 – Source: TradingView

The week has started with some steep correction in the pair as markets are selling the Trade Deal news, with the Greenback seeing some newfound demand.

The selling has found a lower bound after marking oversold levels (0.65160 current session lows), forming the Immediate Pivot. The action still is more bearish than neutral with the ongoing lower consolidation.

The current lows allow for the formation of a downwards hourly channel where reactions to the lower bound will be key to watch for momentum decision – keep this one closely on your charts.

Get ready for the upcoming Australian Inflation data on Tuesday 21:30 (QoQ Inflation consensus at 0.8%, any beat will continue to diminish rate cut expectations, upward demand for the AUD and vice versa)

Safe Trades and successful week!

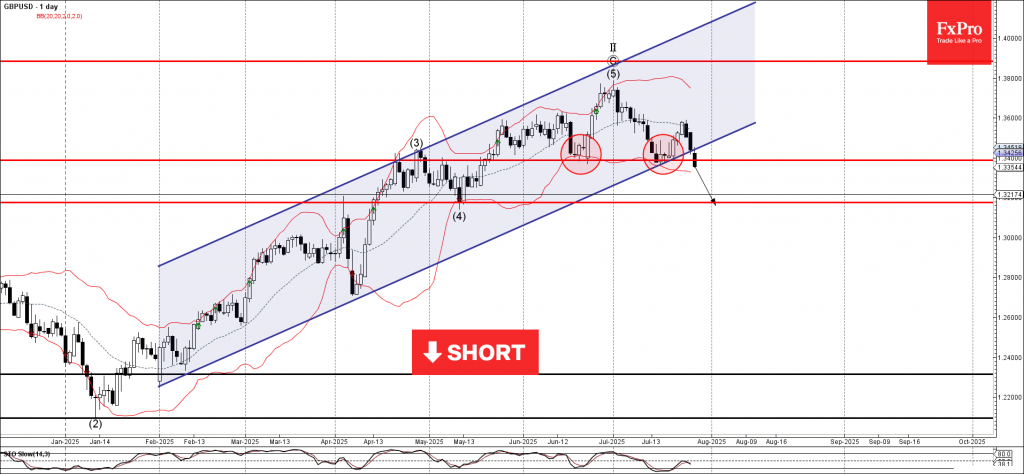

GBPUSD Wave Analysis

GBPUSD: ⬇️ Sell

- GBPUSD broke support zone

- Likely fall to support level 1.3175

GBPUSD currency pair recently broke the support zone between the support level 1.3385 (which has been reversing the price from June) and the support trendline of the daily up channel from January.

The breakout of this support zone should accelerate the active intermediate impulse wave (1) from the start of July.

GBPUSD currency pair can be expected to fall to the next support level 1.3175 (former multi-month low from May, low of the earlier correction (4)).

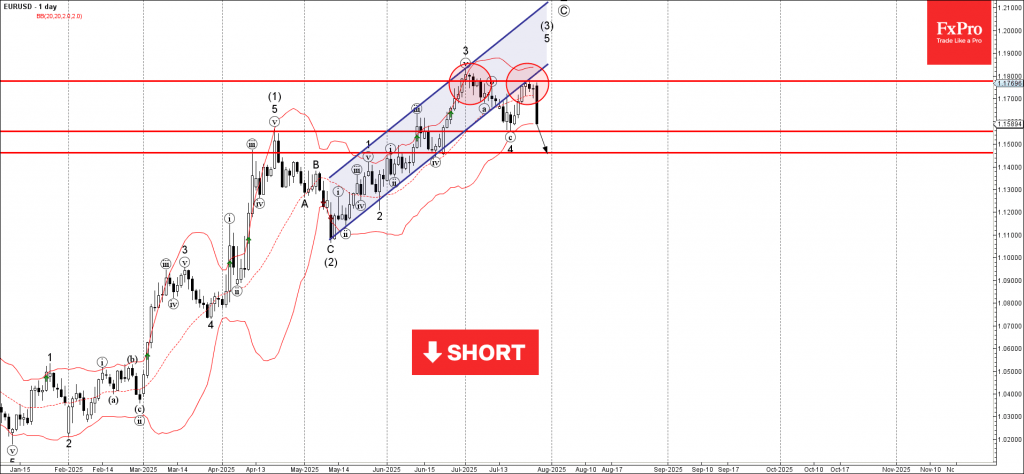

EURUSD Wave Analysis

EURUSD: ⬇️ Sell

- EURUSD reversed from the resistance level 1.1775

- Likely to fall to support levels 1.1555 and 1.1460

EURUSD recently reversed down from the resistance zone between the resistance level 1.1775 (which stopped the previous impulse wave 3 at the start of July, as can be seen below) and the upper daily Bollinger Band.

This resistance zone was further strengthened by the lower trendline of the recently broken up channel from May (acting as resistance after it was broken earlier).

Given the strongly bullish US dollar sentiment, EURUSD can be expected to fall to the next support levels 1.1555 and 1.1460 – the low of waves 4 and iv.