Sample Category Title

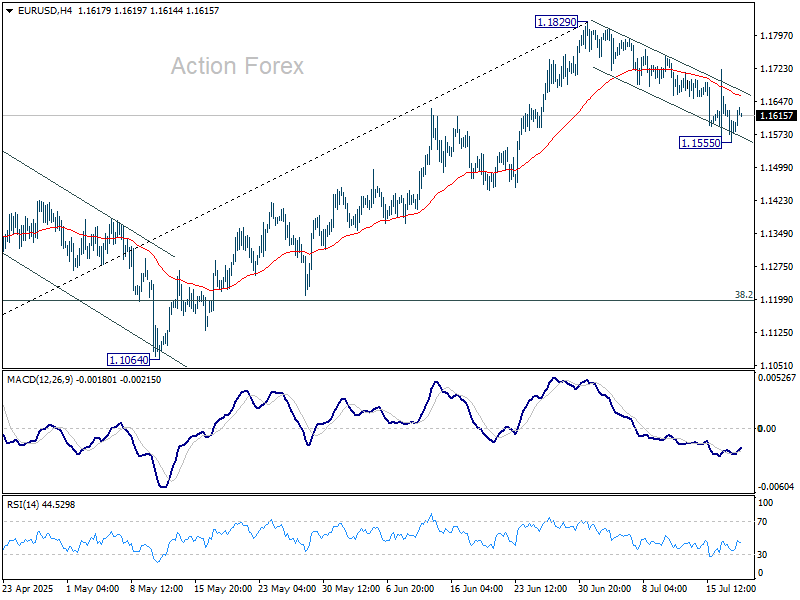

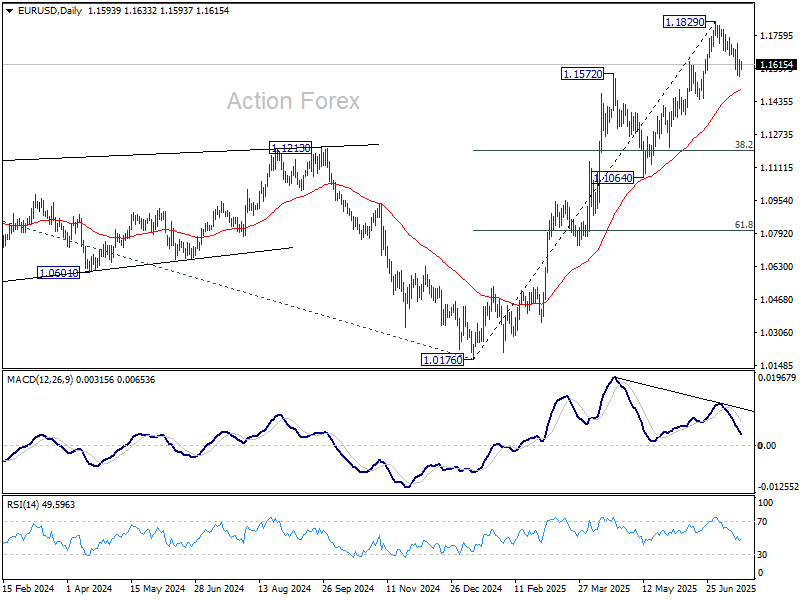

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1555; (P) 1.1600; (R1) 1.1642; More...

Intraday bias in EUR/USD remains neutral at this point. Risk will stay mildly on the downside as long as 1.1829 resistance holds. Fall from there is correcting the rise from 1.1829 or whole rally from 1.0176. Below 1.1555 will target 55 D EMA (now at 1.1493). Sustained break there will target 38.2% retracement of 1.0176 to 1.1829 at 1.1198.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

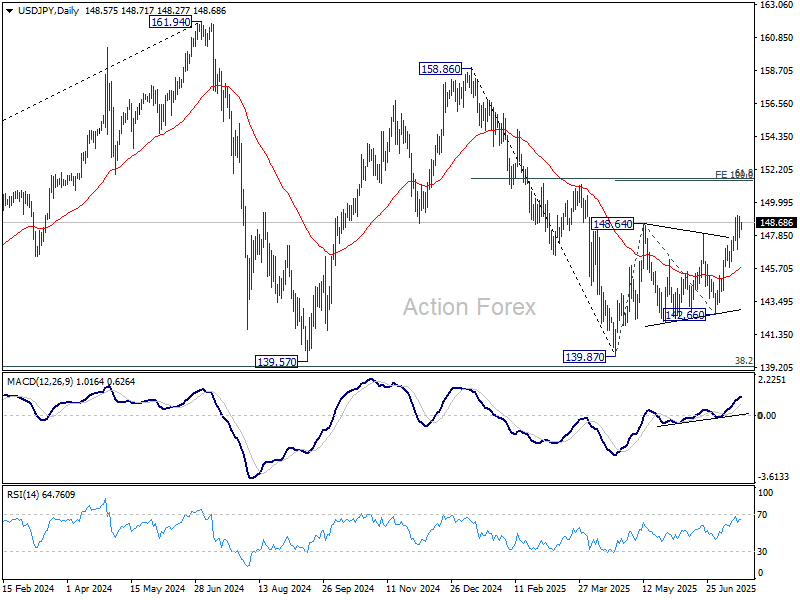

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.86; (P) 148.48; (R1) 149.22; More...

Intraday bias in USD/JPY remains neutral for the moment. More consolidations could be seen below 149.17. Downside should be contained by 55 D EMA (now at 145.77). Break of 149.17 will resume the whole rise from 139.87 to 100% projection of 139.87 to 148.64 from 142.66 at 151.43. That is close to 61.8% retracement of 158.86 to 139.87 at 151.22.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3379; (P) 1.3411; (R1) 1.3447; More...

Intraday bias in GBP/USD remains neutral for the momentum. Focus stays on on 1.3369 support. Decisive break there will suggests that fall from 1.3787 is already correcting the rise from 1.2099. Deeper fall should then be seen to 1.3138 cluster support (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Nevertheless, strong rebound from current level will retain near term bullishness. Break of 1.3561 support turned resistance will bring retest of 1.3787 high first.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3019) holds, even in case of deep pullback.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8011; (P) 0.8037; (R1) 0.8071; More….

Intraday bias in USD/CHF remains neutral at this point. Focus stays on 0.8054 support turned resistance. Decisive break there will suggest that rise from 0.7871 at least correcting the fall from 0.8475. Further rise should then be seen to 55 D EMA (now at 0.8146). Nevertheless, rejection by 0.8054 will retain near term bearishness. Below 0.7946 minor support will bring retest of 0.7871 low.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

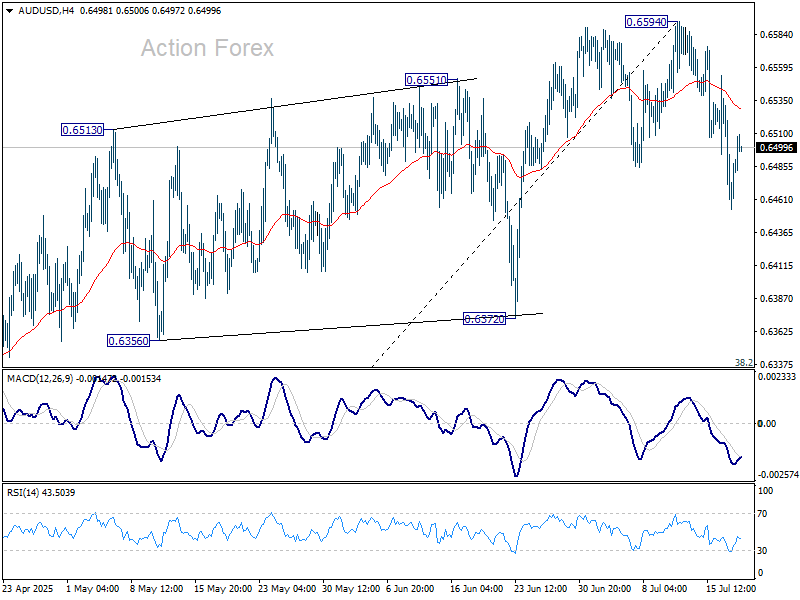

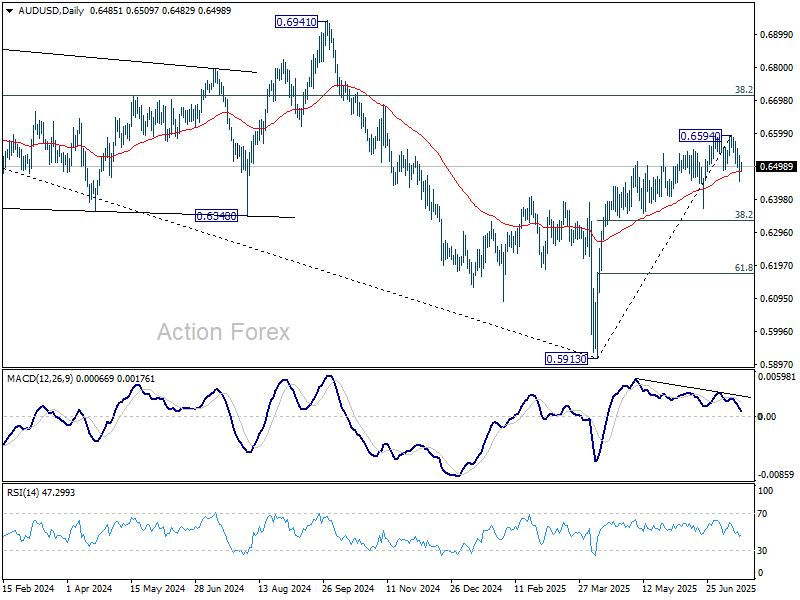

AUD/USD Daily Report

Daily Pivots: (S1) 0.6451; (P) 0.6492; (R1) 0.6530; More...

Intraday bias in AUD/USD stays mildly on the downside at this point. Fall from 0.6594 is tentatively seen as a correction to rise from 0.5913. Deeper fall would be seen to 38.2% retracement of 0.5913 to 0.6594 at 0.6334. Strong support could be seen there to bring rebound. For now, near term outlook is neutral as long as 0.6594 resistance holds, and more consolidations would be seen.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).

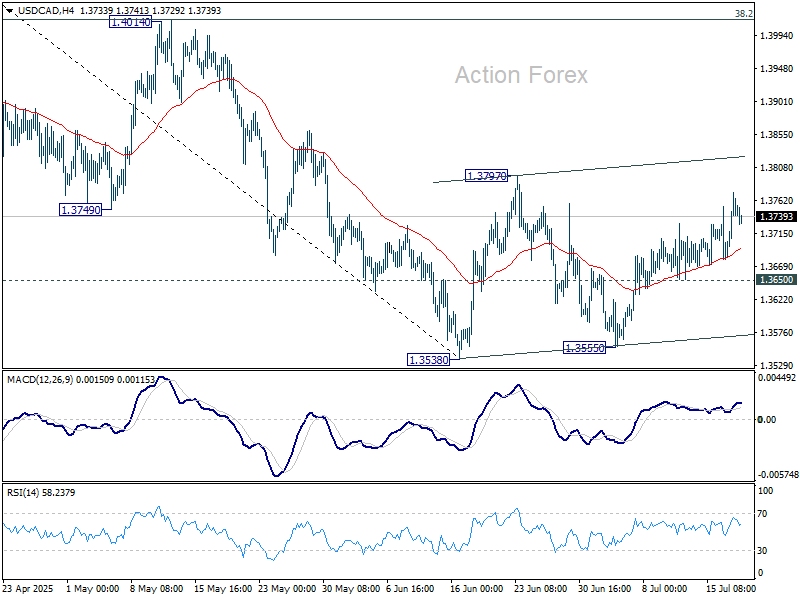

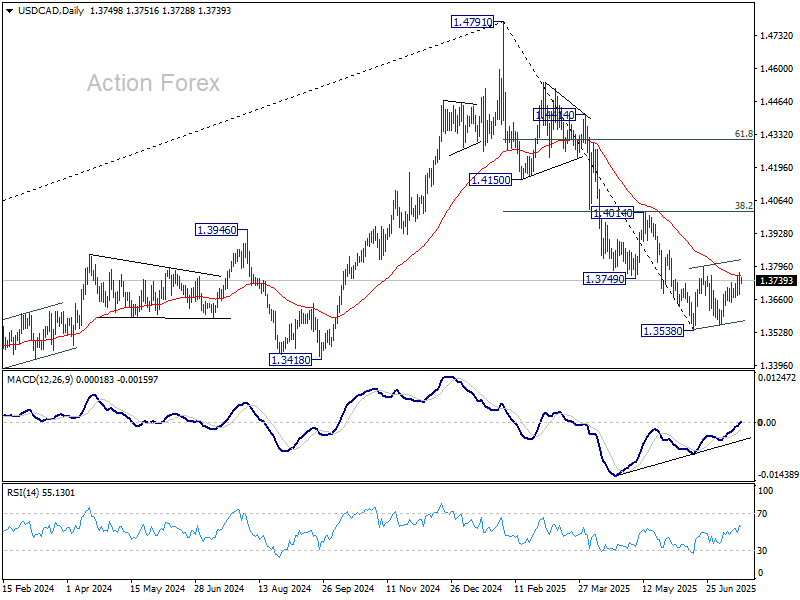

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3698; (P) 1.3736; (R1) 1.3792; More...

Intraday bias in USD/CAD remains mildly on the upside for the moment. Corrective pattern from 1.3538 is extending with the third leg. Further rise would be seen to 1.3797 resistance and possibly above. On the downside, break of 1.3650 minor support will bring retest of 1.3538/55 support zone instead.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

Dollar Holds Weekly as Markets Ignore Fed Waller’s Dovish Push, Ethereum Breaks Higher

Dollar eased slightly in today's Asian session but remains firmly in the lead as the top-performing currency for the week. Fed Governor Christopher Waller reignited the debate over rate cuts, calling for easing as soon as this month. But his comments — timed just ahead of the Fed’s blackout window — failed to shift expectations. Market pricing still implies overwhelming odds of over 97% for no change in July.

The lack of reaction is telling. Waller, though vocal, isn’t seen as representing the majority view, particularly in light of steady inflation and resilient growth. As a voting committee, the FOMC doesn’t take marching orders from a single official — not even the Chair, whose own independence has been under political pressure recently. Markets appear unconvinced that Waller’s remarks signal any imminent pivot. After all, the consensus leans toward staying on hold and watching how tariffs evolve after August 1 tariff truce deadline.

That patience looks justified. US jobless claims fell more than expected and retail sales rebounded, suggesting consumers are recovering from tariff-related uncertainty without a major hit to spending. That resilience is also reflected in risk sentiment, with S&P 500 and NASDAQ both notching fresh record highs overnight.

In FX, Dollar is still the strongest performer this week, trailed by the Loonie and Sterling. At the other end, Aussie has been the weakest following disappointing jobs data, while Kiwi and Yen also struggled. Euro and Swiss Franc are sitting near the middle of the weekly performance table.

Meanwhile, crypto markets are watching Washington closely. The US House passed the long-anticipated Genius Act, establishing a regulatory framework for dollar-pegged stablecoins. The bill received strong bipartisan support and is expected to be signed by US President Donald Trump. It marks a major legislative win for the digital asset industry, which has invested heavily in shaping crypto policy.

While Bitcoin turned sluggish this week, Ethereum is surging. Technically, Ethereum is clearly in upside acceleration as seen in D MACD. Immediate focus is now on 100% projection of 1382.55 to 2879.27 from 2100.58 at 3607.30. Decisive break there will pave the way through 4000 psychological level to 161.8% projection at 4532.23. In any case, near term outlook will now stay bullish as long as 2879.27 resistance turned support holds.

In Asia, at the time of writing, Nikkei is down -0.20%. Hong Kong HSI is up 0.73%. China Shanghai SSE is up 0.34%. Singapore Strait Times is up 0.54%. Japan 10-year JGB yield is down -0.021 at 1.539. Overnight, DOW rose 0.52%. S&P 500 rose 0.54%. NASDAQ rose 0.75%. 10-year yield rose 0.008 to 4.463.

Fed’s Waller sees no reason to wait, backs immediate rate cut

Fed Governor Christopher Waller reinforced his call for a July rate cut, arguing that the policy rate is too restrictive given current economic conditions.

In a speech, Waller emphasized that recent tariffs will only cause a "temporary surge" in prices, not a sustained increase in inflation, and that standard monetary policy practice is to "look through" such one-off price-level shocks as long as expectations remain anchored.

Waller pointed to sluggish growth and moderate inflation as reasons for a cut. He noted that real GDP likely expanded just 1% in the first half of 2025 and is expected to remain soft for the rest of the year—well below FOMC estimates of longer-run growth. With unemployment near 4.1% and inflation close to 2% when tariff effects are stripped out, Waller said policy "policy rate should be around neutral", not nearly 125–150 basis points above the estimated neutral rate of 3%.

Waller also flagged labor market fragility, suggesting that once data revisions are accounted for, private payroll growth is “near stall speed.” With risks to jobs increasing and inflation pressures fading, Waller said, “We should not wait until the labor market deteriorates before we cut the policy rate.”

Fed’s Daly backs two cuts this year, sees tariff impact as muted

San Francisco Fed President Mary Daly said two interest rate cuts this year remain a “reasonable” baseline, as the inflation from tariffs appears less severe than initially feared. Speaking overnight. She projected the policy rate could ultimately stabilize around 3% or slightly above.

Daly downplayed the precise timing of the next move, saying, “Whether it happens in July or September or some other month is really not the most relevant piece.” What matters, she argued, is that the Fed stays on track to avoid overtightening and harming the labor market. “We don’t want to unnecessarily tighten the economy in a way that hurts the labor market or growth,” Daly added.

She also emphasized that bringing inflation down the “last mile” doesn’t require a sharp slowdown. “I wouldn't want to see more weakness in the labor market,” Daly said. “Which is why you can’t wait forever” to cut rates.

Japan CPI core cools to 3.3% on energy, but food and services prices still climb

Japan’s core consumer inflation slowed in June for the first time in four months, driven by easing energy prices. Core CPI, which excludes fresh food, decelerated from 3.7% yoy to 3.3% yoy, in line with expectations. While still above the BoJ’s 2% target — where it's been since April 2022 — the moderation suggests waning energy cost pressures. Headline CPI also dipped to 3.3% from 3.5% in May.

However, underlying price pressures remain sticky. The core-core CPI, which excludes both fresh food and energy, rose from 3.3% yoy to 3.4% yoy, highlighting persistent inflation in services and food. Services inflation ticked up from 1.4% yoy to 1.5% yoy. Food prices excluding fresh items surged 8.2% yoy, up from 7.7% yoy. Rice inflation eased marginally but remains historically elevated at 101.7% yoy.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3698; (P) 1.3736; (R1) 1.3792; More...

Intraday bias in USD/CAD remains mildly on the upside for the moment. Corrective pattern from 1.3538 is extending with the third leg. Further rise would be seen to 1.3797 resistance and possibly above. On the downside, break of 1.3650 minor support will bring retest of 1.3538/55 support zone instead.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

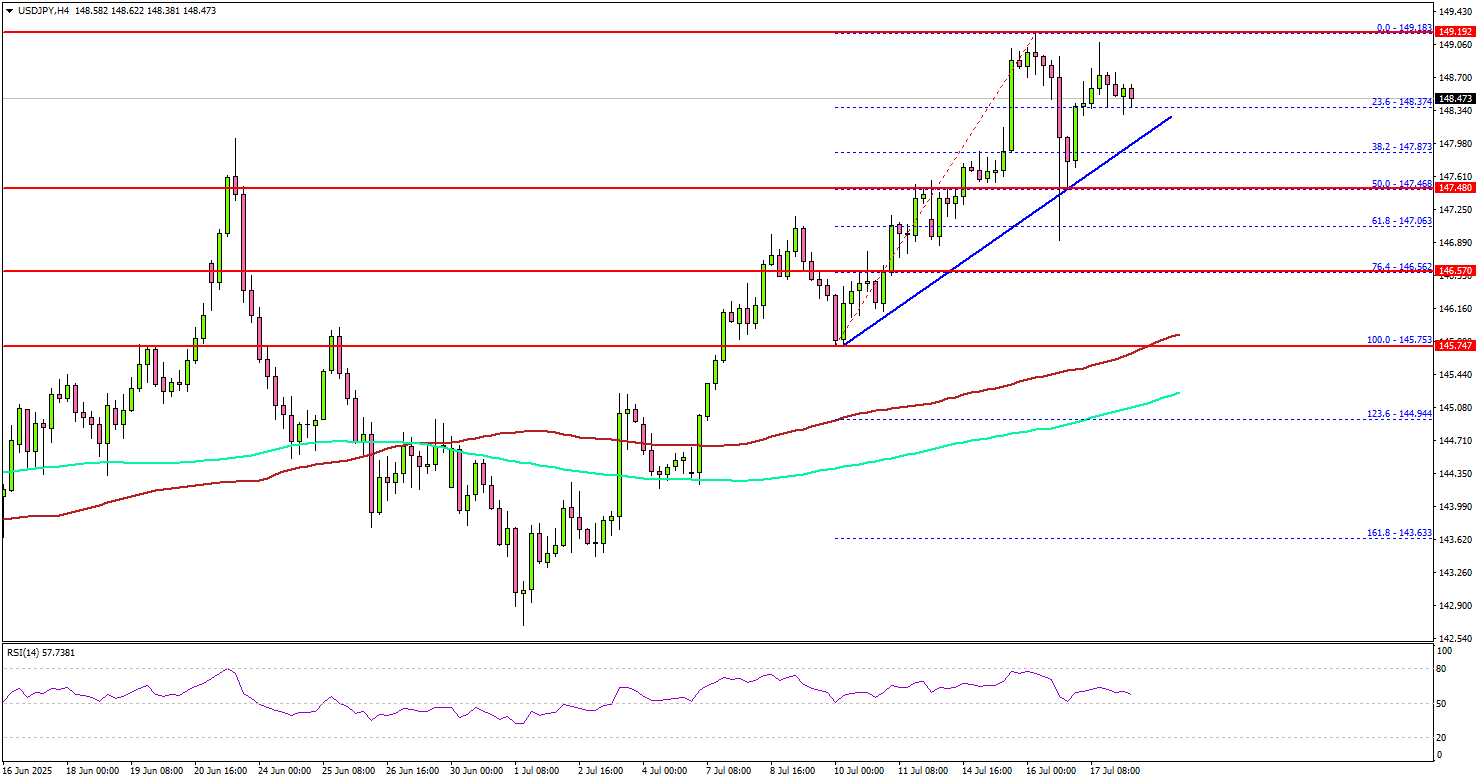

USDJPY Weakens Slightly—Green Light for a Tactical Rebound?

Key Highlights

- USD/JPY gained pace for a move above 148.50 before there was a pullback.

- A connecting bullish trend line is forming with support at 148.00 on the 4-hour chart.

- EUR/USD is showing signs of weakness below the 1.1700 level.

- GBP/USD could gain bearish momentum if there is a close below 1.3350.

USD/JPY Technical Analysis

The US Dollar remained supported above the 146.50 level against the Japanese Yen. USD/JPY broke hurdles near 147.50 and 148.00 to enter a positive zone.

Looking at the 4-hour chart, the pair settled below the 148.00 zone, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). A high was formed near 149.20 before the pair started a consolidation phase.

On the upside, the pair could face resistance near the 149.00 level and the trend line. The next key resistance sits near the 149.20 level. A close above the 149.20 level could set the pace for another increase.

In the stated case, the pair could rise toward the 150.00 resistance. The next major stop for the bulls could be near the 151.20 resistance.

On the downside, immediate support is near the 148.00 level. There is also a connecting bullish trend line forming with support at 148.00 on the same chart. The next key support sits near 147.45. Any more losses could send the pair toward the 146.50 support zone.

Looking at EUR/USD, the pair is struggling to start a fresh increase and might decline further below the 1.1550 level.

Upcoming Economic Events:

- US Housing Starts for June 2025 (MoM) – Forecast 1.30M, versus 1.256M previous.

- US Building Permits for June 2025 (MoM) – Forecast 1.390M, versus 1.394M previous.

- Michigan Consumer Sentiment Index for July 2025 (Prelim) – Forecast 61.5, versus 60.7 previous.

Japan CPI core cools to 3.3% on energy, but food and services prices still climb

Japan’s core consumer inflation slowed in June for the first time in four months, driven by easing energy prices. Core CPI, which excludes fresh food, decelerated from 3.7% yoy to 3.3% yoy, in line with expectations. While still above the BoJ’s 2% target — where it's been since April 2022 — the moderation suggests waning energy cost pressures. Headline CPI also dipped to 3.3% from 3.5% in May.

However, underlying price pressures remain sticky. The core-core CPI, which excludes both fresh food and energy, rose from 3.3% yoy to 3.4% yoy, highlighting persistent inflation in services and food. Services inflation ticked up from 1.4% yoy to 1.5% yoy. Food prices excluding fresh items surged 8.2% yoy, up from 7.7% yoy. Rice inflation eased marginally but remains historically elevated at 101.7% yoy.

Fed’s Waller sees no reason to wait, backs immediate rate cut

Fed Governor Christopher Waller reinforced his call for a July rate cut, arguing that the policy rate is too restrictive given current economic conditions.

In a speech, Waller emphasized that recent tariffs will only cause a "temporary surge" in prices, not a sustained increase in inflation, and that standard monetary policy practice is to "look through" such one-off price-level shocks as long as expectations remain anchored.

Waller pointed to sluggish growth and moderate inflation as reasons for a cut. He noted that real GDP likely expanded just 1% in the first half of 2025 and is expected to remain soft for the rest of the year—well below FOMC estimates of longer-run growth. With unemployment near 4.1% and inflation close to 2% when tariff effects are stripped out, Waller said policy "policy rate should be around neutral", not nearly 125–150 basis points above the estimated neutral rate of 3%.

Waller also flagged labor market fragility, suggesting that once data revisions are accounted for, private payroll growth is “near stall speed.” With risks to jobs increasing and inflation pressures fading, Waller said, “We should not wait until the labor market deteriorates before we cut the policy rate.”