Sample Category Title

Sunset Market Commentary

Markets

All eyes were on Japan. A flopped 20-yr bond auction pushed long-term Japanese bond yields through the roof and immediately raised the stakes for next week’s 40-yr sale. Japan’s fiscal position is a very weak one with its prime minister yesterday calling it even worse than Greece’s. Its huge debt pile is already around 250% of GDP. A lot of debt is owned domestically, of which >45% by the Bank of Japan. However, the Bank of Japan has been slowing down bond purchases as part of its policy normalization and it appears that other domestic bond holders (>40% of outstanding JGBs) do not jump in to fill the gap. Debt and fiscal unsustainability concerns lie at the heart of the matter and the auction was merely a trigger. The Japanese 30-yr hit an intraday record high (3.15%) while the 40-yr tenor closed at one (3.59%). Spillovers to core bond markets were limited at first but shortly after the European opening bell yields headed north nonetheless. That didn’t stop at the US open. Net daily changes currently vary between +1.7 bps (2-yr) to +8.7 bps (30-yr) in the US and up to 6.7 bps (30-yr) in Germany. UK gilt yields staged a sharp intraday U-turns, erasing a 6 bps opening drop to trade 4.5-5.4 bps higher, not in a bear steepener though, but in a flattener. Bank of England chief economist Pill was remarkably vocal in pushing back against rates being cut too quickly. Pill wanted to keep the policy rate steady at this month’s meeting, worrying that rates are coming down too fast in the face of still elevated pay increase and robust services inflation. His fears stem from the fact that the UK may have entered a new regime where price shocks no longer fade “quickly and painlessly” as behaviour of firms and households fundamentally changed. The chief economist said rates have plateaued too low in 2023 (5.25%) and therefore argues for cautious cuts only. In practice that means an even slower pace than the current quarterly one.

Pill’s comments barely support sterling, though. EUR/GBP continues to trade in an extremely tight trading range just north of 0.84. Other currencies trade little changed. EUR/USD holdq steady around 1.123, the trade-weighted dollar index kept the 100 lever alive. The Japanese yen does not capitalize on the huge yield jump, most likely because it’s risk premia driving the move higher. It even erased an early Asian gain that rooted from finance minister Kato seeking bilateral FX talks with US Treasury Secretary Bessent. USD/JPY is currently changing hands around 144.88. The Aussie dollar underperforms global peers today in the wake of the RBA’s 25 bps rate cut. While the move was expected, the softish policy statement and press conference was not.

News & Views

Belgian consumer confidence bounced back in May, from the lowest level since December 2022 (-14) to the second best reading since October of last year (-7). More positive expectations for the general economic situation (-30 from -44) and diminishing concerns about unemployment (13 from 21) made a particularly strong contribution to the boost in confidence. The improvement in confidence is also apparent at the personal level. Households report improved expectations for their own financial situation (-3 from -8). Their saving intentions are also up slightly (19 from 17). Belgian consumer confidence is now again at its long-term average (1990-2024). On Thursday, the National Bank of Belgium releases its May update for business confidence. A rebound can be expected as well as on the back of easing global trade tensions which reduce recession risks.

Headline Canadian inflation fell by 0.1% M/M with the annual figure falling back below the Bank of Canada’s 2% inflation target (1.7% from 2.3% vs 1.6% consensus and vs 1.5% expected by the BoC). The slowdown in April was driven by lower energy prices, which fell 12.7% and comes mainly from the removal of a consumer carbon tax. Excluding food and energy, core inflation accelerated by 0.5% M/M or from 2.4% to 2.6% in Y/Y-terms. The Bank of Canada’s preferred gauge (trimmed mean) rose by 0.4% M/M and from 2.9% Y/Y to 3.1% Y/Y, the fastest pace since March of last year. The acceleration in core inflation was more fierce than expected and pushes BoC rate cut bets for the June 4 policy meeting below 50%. The preferred outcome is now a policy rate status quo in line with the April decision. Today’s inflation report was the penultimate major input for the central bank with Q1 GDP numbers still due on May 30. The Canadian Loonie trades slightly stronger after the CPI report around USD/CAD 1.3920.

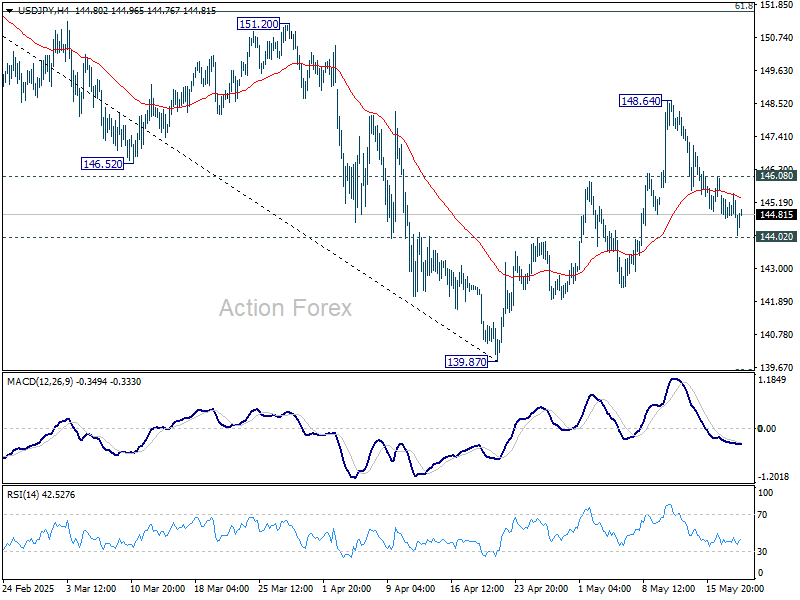

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.52; (P) 145.00; (R1) 145.33; More...

Intraday bias in USD/JPY stays neutral at this point. Further rally is in favor as long as 144.02 support holds. Above 146.08 minor resistance will target 148.64 first. Firm break there will resume the rally from 139.87 to 61.8% retracement of 158.86 to 139.87 at 151.60 next. However, firm break of 144.02 will bring retest of 139.87 low instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

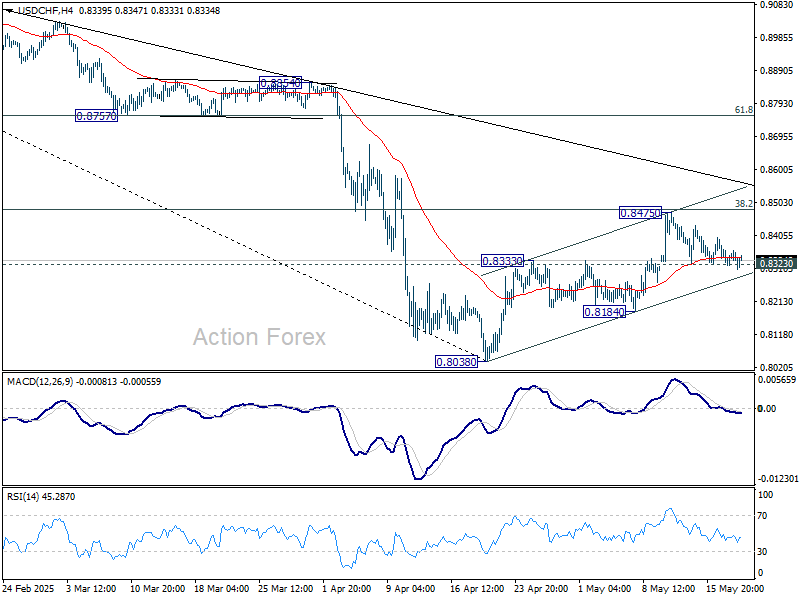

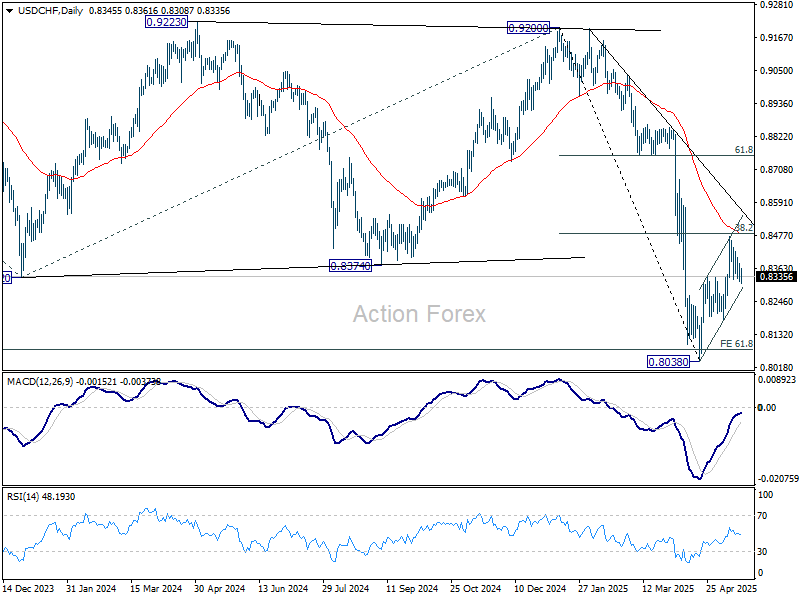

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8318; (P) 0.8349; (R1) 0.8378; More….

USD/CHF breached 0.8323 support but failed to sustain below. Intraday bias stays neutral first. On the downside, firm break of 0.8323 support will argue that corrective rebound from 0.8038 has completed at 0.8475, after rejection by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. Intraday bias will be back on the downside for 0.8184, and then retest of 0.8038 low. However, sustained trading above 0.8482 will dampen this bearish view and target 61.8% retracement at 0.8756 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8765) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

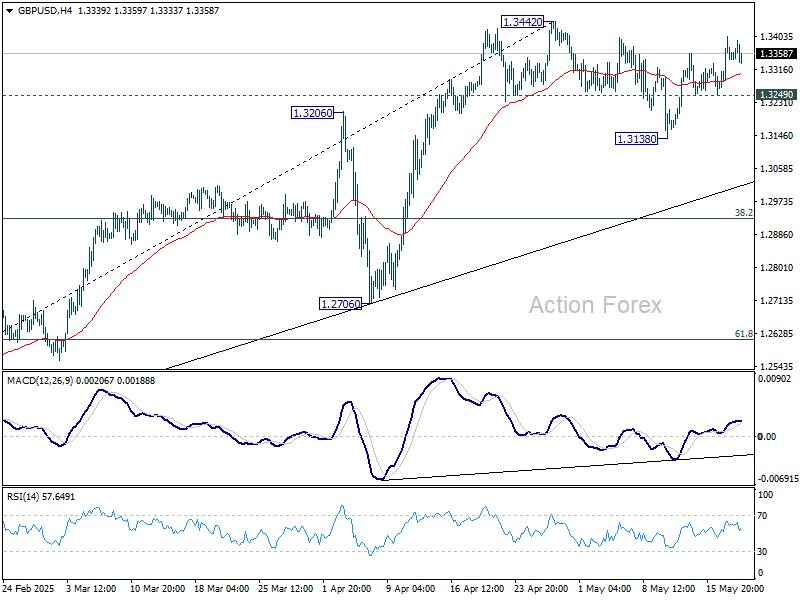

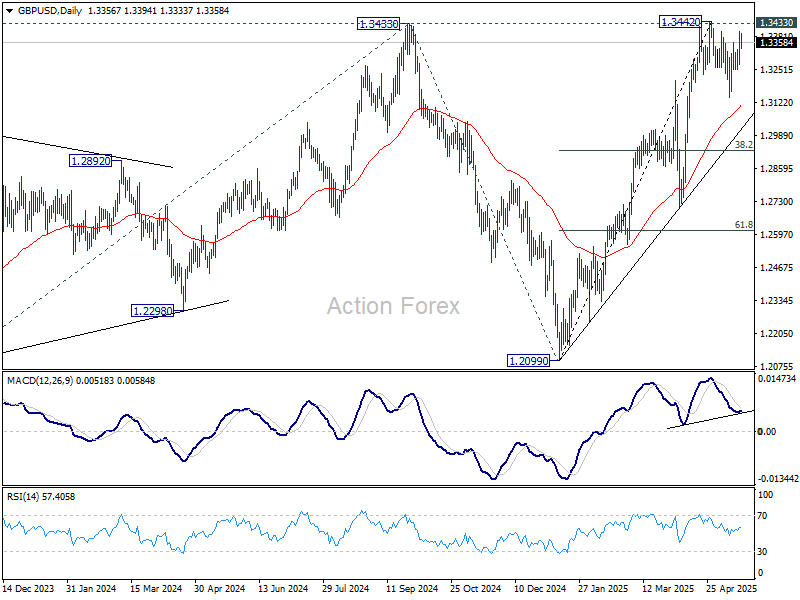

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3283; (P) 1.3344; (R1) 1.3421; More...

Intraday bias in GBP/USD stays mildly on the upside for the moment. Decisive break of 1.3433/42 key resistance zone will confirm larger up trend resumption. On the downside, though, below 1.3249 support will extend the corrective pattern from 1.3442 with another falling leg.

In the bigger picture, up trend from 1.3051 (2022 low) is still in progress. Decisive break of 1.3433 (2024 high) will confirm resumption. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Nevertheless, sustained trading below 55 D EMA (now at 1.3112) will delay the bullish case and bring more consolidations first.

Canada: Falling Gas Prices Mask an Acceleration in Underlying Inflation

Headline CPI inflation for April came in at 1.7% year-on-year (y/y), down from 2.3% y/y in March but above expectations for a 1.6% y/y print.

The deceleration was due to gasoline prices tumbling 18.1% y/y as the consumer carbon price was removed. Also notable was the bounce-back in travel tour prices, which rose 6.7% y/y in April after a 4.7% y/y fall in March.

Prices on food purchased from stores rose 3.8% y/y, also adding to April's inflation.

The Bank of Canada's (BoC) preferred "core" inflation measures both accelerated, with the CPI-Trim rising from 2.9% y/y to 3.1% y/y in April, and the CPI-Median jumping from 2.8% y/y to 3.2% y/y.

Key Implications

Top line inflation seemingly offered a reprieve, but the details of the report show that underlying inflation pressures picked up. Both of the BoC's "core" measures showed a notable uptick in April, rising 0.2 and 0.4 percentage points in the month. Even the traditional "core" measure of CPI (excluding food and energy prices) rose from 2.4% in March to 2.6% in April. As highlighted in our prior commentary, we had expected the inflationary impacts of tariffs to start flowing through later in the second quarter of the year – the jump in April suggests this could be happening sooner than expected.

Today's inflation print is a setback for the BoC and complicates the picture for the path of monetary policy. However, with the government of Canada offering a temporary reprieve on some tariffs, and the labour market slowing rapidly, we believe the central bank will have enough space to deliver two more cuts this year – adding a bit more support to an economy quickly losing momentum.

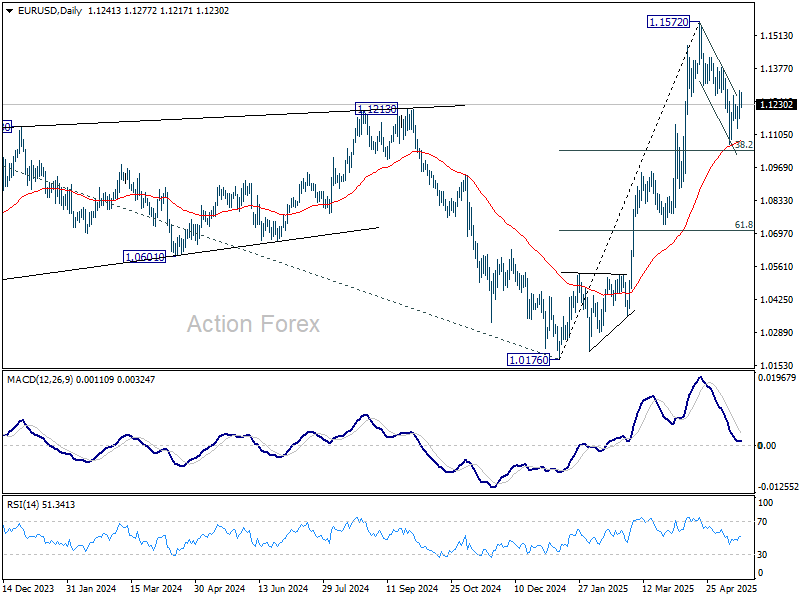

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1180; (P) 1.1234; (R1) 1.1296; More...

Range trading continues in EUR/USD and intraday bias remains neutral. On the upside, decisive break of 1.1292 resistance should indicate that correction from 1.1572 has already completed after defending 38.2% retracement of 1.0176 to 1.1572 at 1.1039. Intraday bias will be turned back to the upside for retesting 1.1572 next. However, sustained break of 1.1039 will bring deeper decline to 61.8% retracement at 1.0709 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0818) holds.

Loonie Lifts on Hot Core Inflation, But BoC Cut Still in Play

Canadian Dollar firmed modestly in early US trading after inflation data showed a sharper-than-expected pickup in core price pressures. While headline CPI slowed to 1.7% in April, the drop was largely due to a steep decline in energy prices. In contrast, underlying inflation picked up pace, with core measures such as CPI-median, trim, and common all rising more than expected, driven in part by higher grocery and travel costs.

The market response was swift. Traders pared back expectations for a BoC rate cut at its June 4 meeting, with swaps now pricing in around a 48% chance, down from 65% prior to the release. Still, attention will now turn to Canada’s Q1 GDP report on May 30, which is likely to be the key data point in determining whether BoC will proceed with a cut or hold off amid resurging inflation pressures.

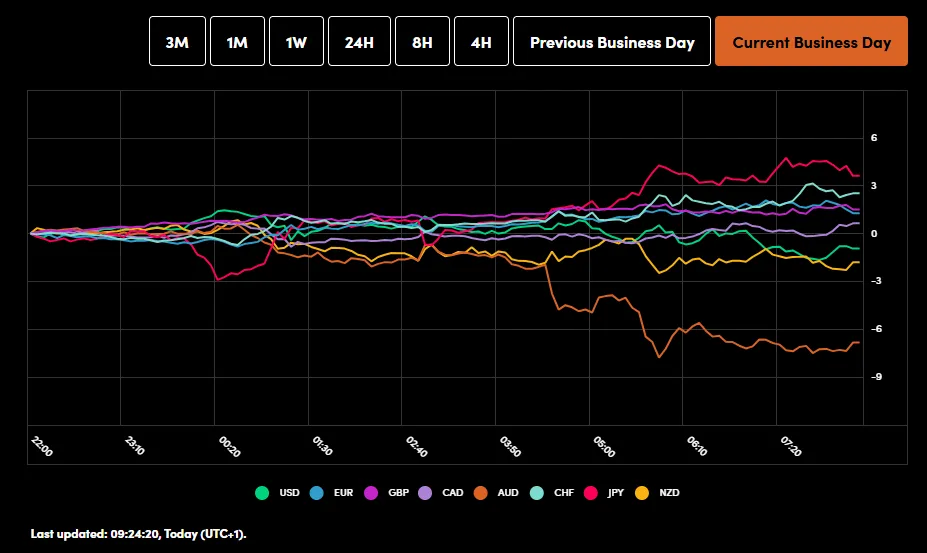

In the currency markets, Loonie is currently leading gains for the day, followed by Swiss Franc and Yen. Meanwhile, Aussie is the day’s worst performer, weighed down by RBA’s dovish rate cut and downgrade in inflation and growth projections. Kiwi is the second weakest, and then Sterling. Euro and Dollar are positioning in the middle.

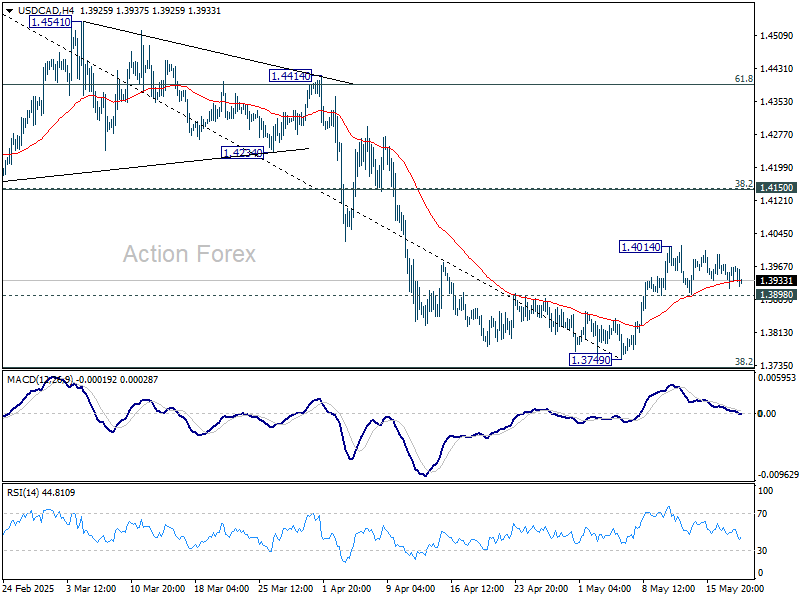

Technically, however, USD/CAD is still bounded firmly inside range of 1.3898/4014. Further rise is still in favor and break of 1.4014 will resume the rebound from 1.3749 short term bottom to 1.4150 cluster resistance (38.2% retracement of 1.4791 to 1.3749 at 1.4147). However, firm break of 1.3898 will bring retest of 1.3749 low instead.

In Europe, at the time of writing, FTSE is up 0.72%. DAX is up 0.46%. CAC is up 0.71%. UK 10-year yield is up 0.039 at 4.704. Germany 10-year yield is up 0.013 at 2.606. Earlier in Asia, Nikkei rose 0.08%. Hong Kong HSI rose 1.49%. China Shanghai SSE rose 0.38%. Singapore Strait Times rose 0.16%. Japan 10-year JGB yield rose 0.035 to 1.523.

Canada's headline CPI slows to 1.7% on energy, but core measures jump

Canada’s headline consumer inflation eased to 1.7% yoy in April, down from 2.3% yoy in March, slightly above the expected 1.6% yoy. The deceleration was primarily due to a steep drop in energy prices by -12.7% yoy, with gasoline down -18.1% yoy and natural gas falling -14.1% yoy. On a monthly basis, overall CPI declined by -0.1% mom.

However, the details beneath the surface were less comforting for policymakers. Excluding energy, inflation actually accelerated, with CPI rising 2.9% yoy compared to 2.5% yoy in March.

Moreover, all three core inflation measures rose notably. CPI-median rose from 2.9% yoy to 3.2%, above expectation of 2.9% yoy. CPI trimmed rose from 2.8% yoy to 3.1% yoy, above expectation of 2.8% yoy. CPI common jumped from 2.3% yoy to 2.5% yoy, above expectation of 2.3% yoy.

BoE’s Pill: Quarterly rate cuts may be too rapid given increasing intrinsic inflation persistence

BoE Chief Economist Huw Pill explained his vote to keep the Bank Rate unchanged at the May MPC meeting as a "skip" rather than a pause in the broader easing cycle.

In speech today, Pill said that while disinflation remains on track, the pace of quarterly 25bps cuts since last summer may be " too rapid" given current inflation dynamics.

He expressed particular concern that structural changes in wage and price-setting behavior have heightened the "intrinsic persistence" of inflation in the UK.

As a result, Pill argued that a more cautious approach to monetary easing is warranted, reinforcing the need to slow the pace of rate reductions while continuing the broader policy normalization.

ECB's Schnabel: Disinflation on track, steady hand needed amid new shocks

ECB Executive Board member Isabel Schnabel said the Eurozone’s disinflation process remains on track, but “new shocks” — particularly from trade tariffs — are presenting emerging risks.

While tariffs may dampen inflation in the short term, Schnabel warned they pose medium-term upside risks, warranting a “steady hand” in monetary policy.

She emphasized the importance of not overlooking "supply-side shocks" if they appear persistent, as doing so could risk "de-anchoring inflation expectations".

Schnabel also highlighted the Eurozone’s relative resilience following the tariff escalation on April 2, noting Euro’s appreciation and a shift in perception toward the region as a "safe haven." She characterized this as a “historical opportunity” to strengthen the international role of Euro.

ECB’s Knot: June rate cut possible, but not confirmed

Dutch ECB Governing Council member Klaas Knot said today that a rate cut at the June meeting remains on the table but is far from a done deal.

“I can't exclude we will decide to have another rate cut in June, but I also can't confirm it,” he told reporters, emphasizing that ECB must remain focused on medium- to long-term inflation risks rather than short-term fluctuations.

Knot said the new staff projections next month will incorporate scenarios reflecting the impact of recent US trade policies and potential EU countermeasures.

While the outlook may show lower inflation in 2025 and 2026, the bigger concern lies beyond that window, given the longer-term effects of tariff-related distortions. “It is more interesting to see what happens after that period,” he noted.

RBA cuts rates to 3.85%, lowers 2025 growth and inflation forecasts

RBA delivered a widely expected 25 bps rate cut, lowering the cash rate to 3.85%. In its statement, RBA said the risks to inflation had become "more balanced," with headline inflation now within the target range and upside pressures "appear to have diminished" amid deteriorating global economic conditions.

Still, the central bank remains cautious, citing significant uncertainty around both demand and supply dynamics, as well as the evolving impact of global trade tensions and geopolitical developments.

The Board acknowledged a "severe downside scenario" and emphasized that monetary policy is "well placed" to respond decisively if global shocks materially affect Australia's outlook. RBA flagged the unpredictability of global tariff policies and noted that households and businesses may hold back on spending amid heightened uncertainty. These concerns have contributed to a weaker outlook across growth, employment, and inflation.

In its revised forecasts, RBA downgraded GDP growth for 2025 to 1.9% (from 2.1%) and for 2026 to 2.2% (from 2.3%). End-2025 headline CPI was revised down to 3.0% from 3.7%, with end-2026 projection lifted from 2.8% to 2.9%. Trimmed mean forecasts for the end-2025 and end 2026 were both cut slightly from 2.7% to 2.6%.

RBA's Bullock: Debated 25 vs 50bps cut debated; trade risks tilt toward disinflation

Following RBA’s decision, Governor Michele Bullock revealed in the post-meeting press conference that the Board briefly considered holding rates but quickly moved to debate between 25 and 50 basis point reductions.

Ultimately, the more measured 25bps cut was preferred, given that inflation is within target and unemployment remains resilient. Bullock emphasized that while easing was justified, "it doesn't rule out that we might need to take action in the future."

Bullock also noted that the Board views recent global trade developments as broadly "disinflationary" for Australia. However, she cautioned that risks remain tilted both ways.

"There is a risk to inflation on the upside, trade policies could lead to supply chain issues, which could raise prices for some imports, much as we saw during the pandemic," she emphasized.

China cuts loan prime rates for first time in seven months

China’s central bank lowered its key lending benchmarks for the first time since October, delivering a long-anticipated move to support the economy.

PBoC lowered the one-year loan prime rate by 10 bps to 3.0%. The five-year LPR, a key reference for mortgages, was also trimmed by 10 bps to 3.5%.

The October 2025 easing was more aggressive at 25 basis points, but today’s cuts still mark a meaningful step in the ongoing monetary support cycle.

The move comes as part of a broader policy package unveiled by PBOC Governor Pan Gongsheng and top financial regulators ahead of high-level trade talks in Geneva that have since led to a temporary truce between China and the US on tariffs.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1180; (P) 1.1234; (R1) 1.1296; More...

Range trading continues in EUR/USD and intraday bias remains neutral. On the upside, decisive break of 1.1292 resistance should indicate that correction from 1.1572 has already completed after defending 38.2% retracement of 1.0176 to 1.1572 at 1.1039. Intraday bias will be turned back to the upside for retesting 1.1572 next. However, sustained break of 1.1039 will bring deeper decline to 61.8% retracement at 1.0709 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0818) holds.

Canada’s headline CPI slows to 1.7% on energy, but core measures jump

Canada’s headline consumer inflation eased to 1.7% yoy in April, down from 2.3% yoy in March, slightly above the expected 1.6% yoy. The deceleration was primarily due to a steep drop in energy prices by -12.7% yoy, with gasoline down -18.1% yoy and natural gas falling -14.1% yoy. On a monthly basis, overall CPI declined by -0.1% mom.

However, the details beneath the surface were less comforting for policymakers. Excluding energy, inflation actually accelerated, with CPI rising 2.9% yoy compared to 2.5% yoy in March.

Moreover, all three core inflation measures rose notably. CPI-median rose from 2.9% yoy to 3.2%, above expectation of 2.9% yoy. CPI trimmed rose from 2.8% yoy to 3.1% yoy, above expectation of 2.8% yoy. CPI common jumped from 2.3% yoy to 2.5% yoy, above expectation of 2.3% yoy.

ECB’s Knot: June rate cut possible, but not confirmed

Dutch ECB Governing Council member Klaas Knot said today that a rate cut at the June meeting remains on the table but is far from a done deal.

“I can't exclude we will decide to have another rate cut in June, but I also can't confirm it,” he told reporters, emphasizing that ECB must remain focused on medium- to long-term inflation risks rather than short-term fluctuations.

Knot said the new staff projections next month will incorporate scenarios reflecting the impact of recent US trade policies and potential EU countermeasures.

While the outlook may show lower inflation in 2025 and 2026, the bigger concern lies beyond that window, given the longer-term effects of tariff-related distortions. “It is more interesting to see what happens after that period,” he noted.

Markets Eye Trade Deals, DAX Breaches 24000

Asian Session Market Wrap

The MSCI Asia Pacific index rose by 0.4% after the S&P 500 nearly entered a bull market on Monday. Hong Kong stocks went up by 1.3%, with Contemporary Amperex Technology surging up to 18% on its first trading day.

Markets shrugged off a Moody’s downgrade with risk assets largely continuing their rally. There was some caution on show as safe havens like Gold did gain a bid yesterday.

Optimism from the US-China 90 day pause may be waning at the moment with market participants looking toward other trade deal announcements to boost sentiment.

Market participants are closely watching US trade talks with India and Japan after a recent tariff-lowering deal with China raised hopes.

India is working on a three-part trade deal with the US and aims to finalize an interim agreement before July, when Trump’s reciprocal tariffs are set to start, according to insiders. Meanwhile, Japan’s top trade negotiator, Ryosei Akazawa, is planning a third round of talks in the US as early as this week.

Japan’s finance minister is also arranging a meeting with US Treasury Secretary Scott Bessent this week to discuss issues like currency, which boosted the yen.

Additionally, Vietnam and the US began their second round of talks on a bilateral tariff agreement in Washington DC on Monday, with discussions continuing until Thursday.

Following on from yesterday's Chinese data, major Chinese banks cut deposit rates again, in the latest efforts to drive consumers to spend more amid a flagging economy. This was evident by the retail sales numbers yesterday.

Developments and announcements on these trade deals could help boost market sentiment and potentially stir another bullish rally in risk assets.

The European Open

Heading into the European open, S&P 500 futures dropped 0.2%, indicating a six-day advance may be poised to end. Contracts for Europe strengthened 0.5%

The pan-European STOXX 600 index rose 0.2%, reaching its highest level in seven weeks. The DAX index printed fresh all-time highs and peaked just above the 24000 handle but trades slightly down on the day.

Utility stocks went up by 1.1%, with Portugal's EDP Renovaveis gaining 3.5% after Deutsche Bank upgraded its rating from "hold" to "buy."

On the FX front, the US dollar stayed steady at 144.75/yen, after hitting 144.66 on Monday, its weakest level since May 8. The dollar index dropped 0.1%, following a 0.6% decline in the previous session.

The Australian dollar fell 0.5% to 0.6423, giving up part of Monday's 0.8% gain. This came after the Reserve Bank of Australia (RBA) lowered its main cash rate to 3.85%, a two-year low, due to a weaker global outlook and slowing inflation at home.

The British pound remained steady at 1.3353, while the euro stayed flat at 1.1249.

Currency Power Balance

Source: OANDA Labs

Economic Data Releases

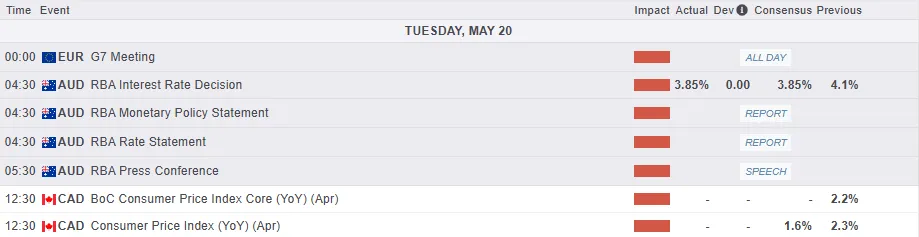

Looking at the economic calendar, it is a quiet one in Europe with a few ECB policymakers being the highlight. Later in the day we have Canadian CPI data and a few Federal Reserve policymakers which could stoke volatility as well.

For now, news and comments on potential trade deals as well as any new information on the Russia-Ukraine truce could have an impact on market moves.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the day - DAX

From a technical standpoint, the DAX index has printed a fresh all-time high just above the 24000 handle.

In early European trade the index is trading slightly down on the day and this could be due to some caution and potential profit taking.

The daily candle did close above the 24000 handle and could help push the Index higher.

However, looking at recent price action and the last time the index printed a fresh all-time high we did see about three days of consolidation before the next push to the upside. Will history repeat itself?

The period-14 RSI remains in overbought territory with immediate support resting at 23750 before the 23471 handle comes back into focus.

A move beyond 24000 and i will be paying attention to whole numbers at 24250 and 24500 respectively.

DAX Index Daily Chart, May 20, 2025

Source: TradingView.com (click to enlarge)