Sample Category Title

Sunset Market Commentary

Markets

Asian currencies remained among the best performers today. They still thrive on yesterday’s rumours of the US and South Korean having talked about FX policy even though sources later denied the news. Similar speculation of local governments ready and willing to beef up their currency as a bargaining chip in trade talks with the US was the reason Asian currencies in early May ripped higher as well. The story back then centered around the Taiwan dollar though. The SK won strengthens sub USD/KRW 1400 while the Japanese yen moves from USD/JPY 146.75 to 146.1 in a three-day winning streak. Moves in other USD pairs remain very limited and insignificant from a technical point of view. EUR/USD oscillated in a tight sideways trading range around 1.12, the trade-weighted index treaded water just north of 100. Core bonds gain ground with the front outperforming the long end of the curve. German yields drop 4 (30-yr) to 6 bps (2-yr) in a consistent move lower throughout the day. US yields lose up to 6 bps in the 2-yr yield, triggering a test and break of the recently conquered 4% barrier again. The long end of the curve, the 30-yr in particular, suddenly spiked towards the symbolically important 5% before attracting buyers and paring gains again as a result. The moves both at the front and long end coincided with the publication of some US economic data but we wouldn’t draw too many conclusions from them. Especially with respect for long-term bond yields, which we think are more driven by the comeback of fiscal sustainability as a market theme, heralded by Monday’s release of the House reconciliation bill details and yesterday’s dire CRFB deficit-impact calculations. US April retail sales came in to the low end of expectations but saw the March reading revised higher across all gauges. Headline sales last month rose by 0.1% m/m as 5 rising categories made up for the 8 categories printing a drop. A core measure excluding car and gas printed 0.2% growth. The control group series used in GDP calculations unexpectedly declined by 0.2%. PPI numbers for April were a similar story: a sub-consensus outcome offset by upward adjustments for March. Weekly jobless claims remained low (229k) and some confidence indicators for May, including the Empire Manufacturing (-9.2 from -8.1) and Philly Fed Business Outlook (-4 from -26.4) were a mixed bag. The US equity market rally, supported a.o. by Trump’s deal-making tour in the Middle East, is catching a breather with a slightly lower open. Oil in commodity markets faced some selling pressure after the US president said the US and Iran were getting closer to a nuclear deal which could pave the way for a (partial) return of Iranian oil on broader global markets.

News & Views

The International Energy Agency projects global oil demand to slow for the remainder of the year as economic headwinds and record EV sales curb use. In their monthly oil market report, they forecast demand growth averages of 740k b/d in 2025 and 750k b/d in 2026. Those estimates nevertheless are an upward revision from respectively 726k and 692k b/d. World oil supply looks on track to rise by 1.6m b/d on average this year and by an additional 970k b/d in 2026 (from 1.2m & 960k estimates previously). Amid the weaker outlook for the world economy and global oil demand, OPEC+ surprised the market in early May by announcing a second consecutive monthly increase of 411k b/d for June. With the rises in global supply expected to considerably outpace demand growth, oil inventories are forecast to jump by an average of 720k b/d this year and 930k b/d next year, compared with a decline of 140k b/d in 2024. Oil prices are under downward pressure since early “Liberation Day” (April 2) on supply/demand dynamics. One of the most immediate impacts of the recent slump in oil prices is expected to fall on US shale output with independent producers opting to trim rig counts end lower capex plans.

Flash Q1 GDP estimates in Poland and in Switzerland both beat consensus. Polish economic growth slowed from 1.4% Q/Q in Q4 to 0.7% while markets feared a slowdown to just 0.1%. Y/Y broadly stabilized at 3.2% (from 3.4%). Details will follow on June 2nd. Preliminary Swiss (sport event adjuster) Q1 GDP accelerated from 0.5% Q/Q to 0.7% (vs 0.4% expected). The State Secretariat for Economic Affairs that growth was driven significantly by the services sector with industry also showing overall expansion. Detailed numbers for both countries will be available on June 2nd.

UK GDP Stronger Than Expected, US Retail Sales Post Small Gain, Pound Posts Gains

The British pound is in positive territory on Thursday. In European session, GBP/USD is trading at 1.3287, up 0.23% on the day.

UK GDP gives the pound a boost

The British economy expanded 0.7% q/q in the first quarter, below the 1% gain in Q4 2024 but just above the market estimate of 0.6%. This marked the strongest growth in three quarters, driven by stronger activity in services and manufacturing. Annually, growth rose 1.3% in Q1, below the 1.5% gain in Q4 2024 but higher than the market estimate of 1.2%.

The Bank of England lowered the cash rate to 4.25% from 4.5% last week and signaled that further cuts were coming. However, the stronger-than-expected GDP reports has lowered the markets' rate expectations.

The US tariffs have created a lot of uncertainty over global trade. President Trump's unexpected trade deal with the UK and the deal with China to slash tariffs for 90 days are welcome steps but have reinforced Trump's unpredictability. This has made it difficult for the BoE to make growth and inflation projections, as the tariff factor remains a huge question mark.

US retail sales ease, PPI declines

US retail sales in April posted a weak gain of 0.1% m/m. This was well below the upwardly revised 1.7% gain in March but edged above the market estimate of 0%. There was also soft data from the inflation front. Producer Price inflation declined 0.5% in April, down from the upwardly revised 0% in March and below the market estimate of 0.2%.

The Federal Reserve is widely expected to hold rates at the June 30 meeting, but there is a 36% chance of a rate cut in July and a 50% likelihood in September, according to CME's FedWatch. Fed Chair Powell has adopted a wait-and-see stance, hoping that the uncertainty over US trade policy becomes clearer.

GBP/USD Technical

- GBP/USD is testing resistance at 1.3292. Next, there is resistance at 1.3331

- 1.3225 and 1.3186 are the next support levels

GBPUSD 1-Day Chart, May 15, 2025

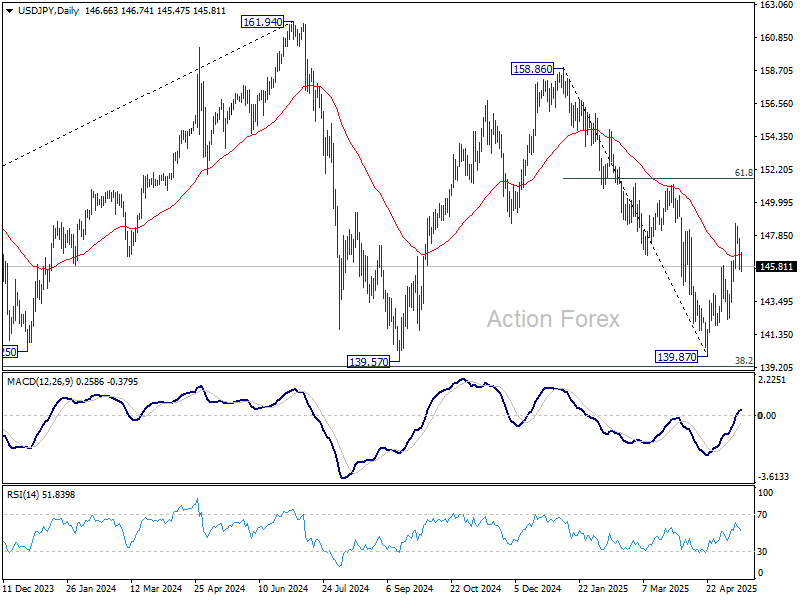

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.68; (P) 146.68; (R1) 147.74; More...

Intraday bias in USD/JPY stays neutral for the moment. Further rally is expected as long as 144.02 resistance turned support holds. As noted before, fall from 158.86 could have completed 139.87 already. Above 148.64 will target 61.8% retracement of 158.86 to 139.87 at 151.60 next. However, firm break of 144.02 will bring retest of 139.87 low instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

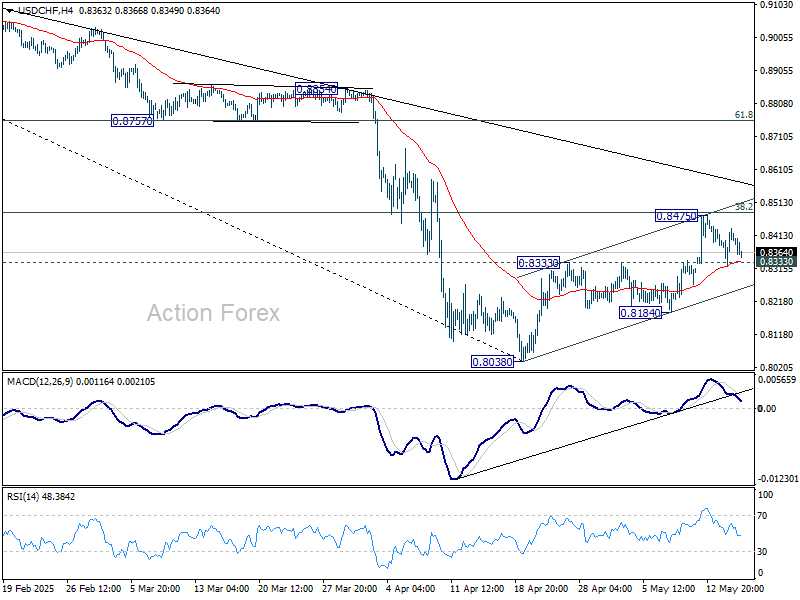

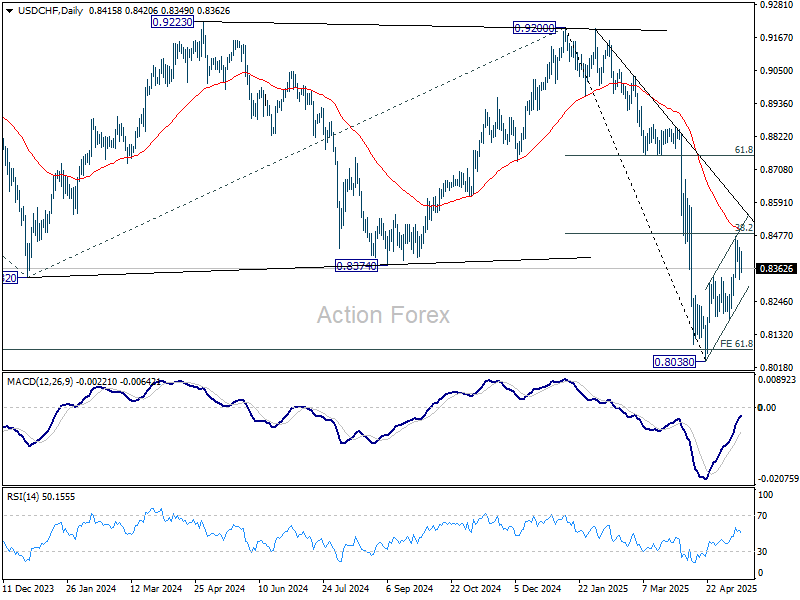

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8352; (P) 0.8394; (R1) 0.8463; More….

Intraday bias in USD/CHF remains neutral for the moment. On the downside, firm break of 0.8333 resistance turned support will argue that corrective rebound from 0.8038 has completed at 0.8475, after rejection by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. Intraday bias will be back on the downside for 0.8184, and then retest of 0.8038 low. However, sustained trading above 0.8482 will dampen this bearish view and target 61.8% retracement at 0.8756 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8750) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

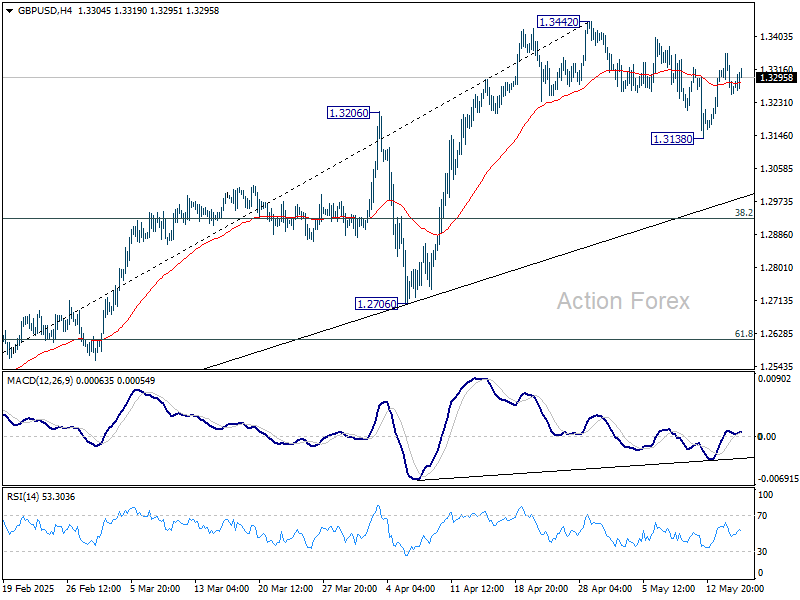

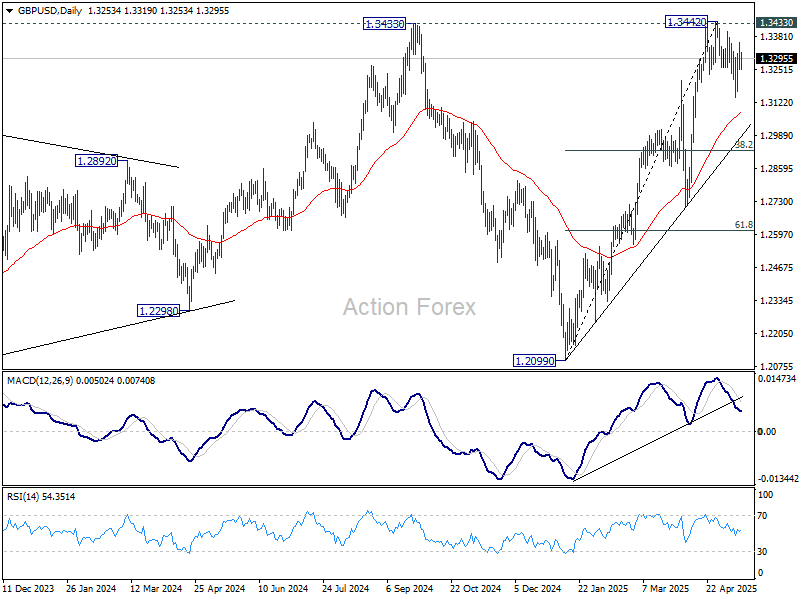

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3225; (P) 1.3292; (R1) 1.3331; More...

Intraday bias in GBP/USD remains neutral first. On the upside, decisive break of 1.3433/42 key resistance zone will confirm larger up trend resumption. Nevertheless, below 1.3138 will resume the correction from 1.3442. But downside should be contained by 38.2% retracement of 1.2099 to 1.3442 at 1.2929 to bring rebound.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could either be resuming the up trend, or the second leg of a consolidation pattern. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on decisive break of 1.3433 at a later stage.

US: Retail Sales Take a Breather in April

Retail and food services sales were little changed in April, edging up by just 0.1% month-on-month (m/m). The pause in activity in April comes after an outsized gain in March, which was revised higher to 1.7% m/m (previously 1.5% m/m).

Motor vehicle sales and parts edged lower by 0.1% m/m, though that came from very elevated levels as households continued to purchase vehicles ahead of the tariffs. Sales at gasoline stations were also lower, declining for the third consecutive month (-0.5% m/m) due to lower prices at the pump. Meanwhile, building materials and equipment stores had another decent month of growth, with sales rising by 0.8% m/m.

Sales in the "control group", which excludes the volatile components above (i.e., gasoline, autos and building supplies) declined by 0.2% m/m, well below expectations for a 0.3% gain.

Sales pulled back across most of the remaining categories, particularly in areas that saw large gains in March, including sporting goods & hobby stores (-2.5% m/m) and miscellaneous store retailers (-2.1% m/m). Furniture & home furnishings and electronics & appliance stores bucked the trend, with sales increasing by 0.3% m/m in each category. Online sales also edged modestly higher (+0.2%).

Sales at bars and restaurants remained strong, rising 1.2% m/m. This comes on the heels of an upwardly revised 3% m/m growth in March (previously reported as 1.9%).

Key Implications

Retail sales were little changed in April, but the easing in activity comes on the heels of a surge in March as consumers rushed to front-load purchases ahead of anticipated tariffs. There continued to be some evidence of this front-loading in April, with auto sales remaining at elevated levels, and consumers still purchasing large ticket items like furniture, electronics, and building materials. Households also showed a continued willingness to spend on discretionary items, as evidenced by another month of strong growth in bar and restaurant sales. While increased spending on goods—particularly cars – can be attributed to efforts to get ahead of potential tariff-related price hikes, robust spending on services like dining out suggests that consumer spending remains relatively resilient, despite downbeat sentiment.

The current divergence between forward-looking consumer sentiment and actual spending activity reflects both the front-loading of purchases and the still-resilient underlying economic fundamentals. The labor market continues to show strength, with job growth averaging 155,000 per month over the past three months, and wage growth remains positive. As for inflation, there have been no significant signs of price pressures stemming from tariffs so far. Corporate efforts to stockpile goods and limit the pass-through of costs to consumers appear to be containing price increases, at least in the short term. The temporary truce with China and the reduction in reciprocal tariffs should further ease pricing pressures in the near term. Looking through the recent volatility, we expect consumer spending to advance by around 1% in the second quarter as the boost from pre-emptive shopping fizzles out.

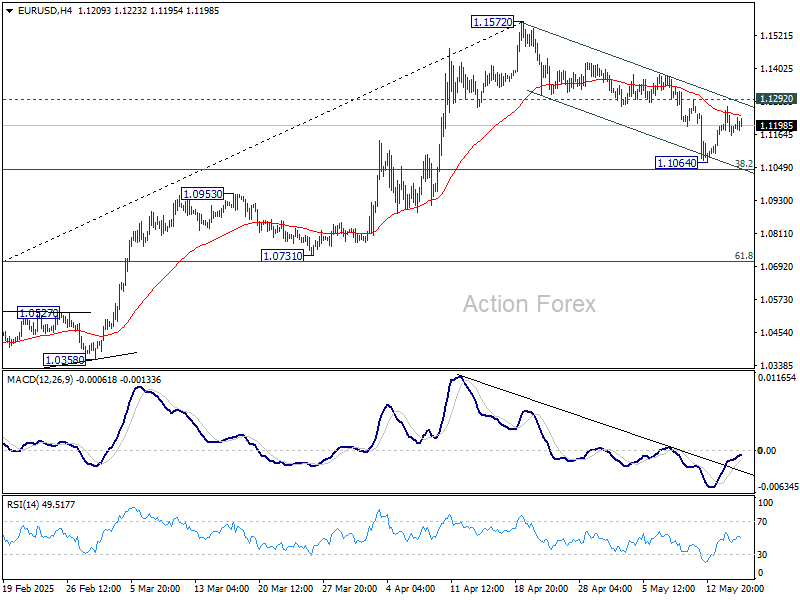

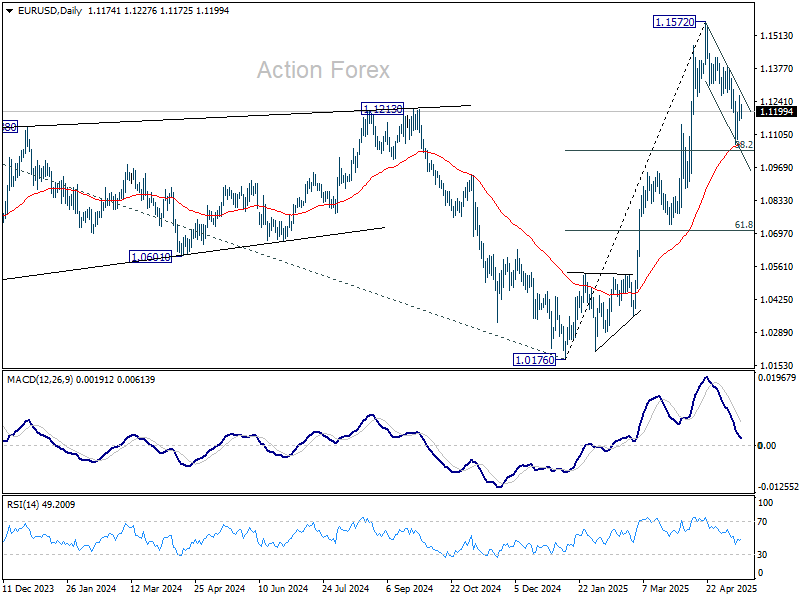

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1136; (P) 1.1201; (R1) 1.1238; More...

Range trading continues in EUR/USD and intraday bias stays neutral. On the upside, break of 1.1292 resistance will argue that correction from 1.1572 has completed after defending 38.2% retracement of 1.0176 to 1.1572 at 1.1039. Intraday bias will be back on the upside for retesting 1.1572. However, sustained break of 1.1039 will dampen this view and target 61.8% retracement at 1.0709 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0789) holds.

Markets Tread Water as Traders Shrug Off US PPI and UK GDP Surprises

Global financial markets are trading in tight ranges today, with little conviction seen across major asset classes. U.S. futures are pointing to a mildly weaker open. Despite a surprise decline in US producer prices in April, suggesting a possible easing of inflation pressures, there was little follow-through in market reaction. Earlier today, stronger-than-expected UK Q1 GDP data also offered limited support to the Pound. Overall sentiment remains contained as traders await further clarity on the trade front.

Much of the current hesitation in markets can be attributed to persisting trade uncertainty. The EU Foreign Affairs Council is holding a key meeting today in Brussels to discuss trade relations with the US and broader economic security. Ahead of the meeting, European trade ministers expressed dissatisfaction with the limited UK-US trade agreement announced last week, which retains a 10% tariff on British exports. EU officials signaled that such a deal would not suffice to deter retaliatory measures.

European Trade Commissioner Maros Sefcovic confirmed a recent conversation with U.S. Commerce Secretary Howard Lutnick and noted that both sides have agreed to step up engagement. Additional meetings are anticipated in Brussels or during upcoming OECD sessions. However, the complexity of negotiations and diverging expectations between the EU and US continue to cast doubt on a swift resolution.

Elsewhere, trade talks between the US and India also show signs of friction. US President Donald Trump claimed that India had offered a trade deal with “no tariffs” on American goods. However, India’s foreign minister Subrahmanyam Jaishankar quickly pushed back, saying that talks remain ongoing and nothing has been finalized. It's believed that India would demand strict reciprocity on tariffs, while it's unlikely to concede easily in politically sensitive sectors such as agriculture, where protectionist pressures remain high.

In the currency markets, Aussie is leading gains for the week, followed by Dollar and then Sterling. On the weaker side, the Swiss Franc is the laggard, with Kiwi and Euro also underperforming. Yen and Canadian Dollar are holding middle positions.

In Europe, at the time of writing, FTSE is up 0.34%. DAX is up 0.10%. CAC is down -0.19%. UK 10-year yield is down -0.042 at 4.674. Germany 10-year yield is down -0.061 at 2.64. Earlier in Asia, Nikkei fell -0.98%. Hong Kong HSI fell -0.79%. China Shanghai SSE fell -0.68%. Singapore Strait Times rose 0.54%. Japan 10-year JGB yield rose 0.022 to 1.479.

US retail sales rises 0.1% mom in Apr, ex-auto sales up 0.1% mom

US retail sales rose 0.1% mom to USD 724.1B in April, matched expectations. Ex-auto sales rose 0.1% mom to USD 582.5B, below expectation of 0.3% mom. Ex-gasoline sales rose 0.1% mom to USD 673.1B. Ex-auto & gasoline sales rose 02% mom to USD 531.5B.

Total sales for the February through April period were up 4.8% from the same period a year ago.

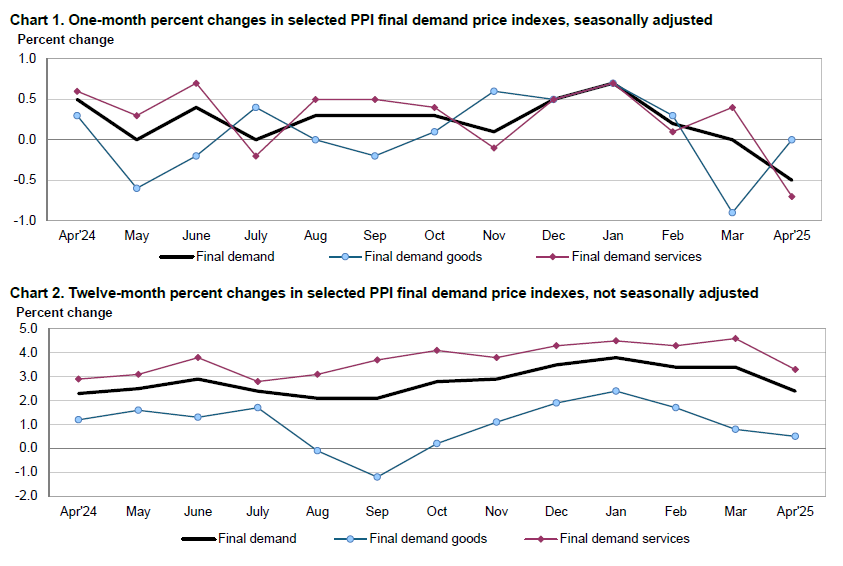

US PPI at -0.5% mom, 2.4% yoy in April, below expectations

US PPI fell -0.5% mom in April, below expectation of 0.2% mom. PPI services fell -0.7% mom while PPI goods was unchanged. PPI less foods, energy and trade services ticked down by -0.1% mom, the first decline since April 2020.

For the 12 months, PPI slowed from 2.7% yoy to 2.4% yoy, below expectation of 2.5% yoy. PPI less foods, energy and trade services rose 2.9% yoy.

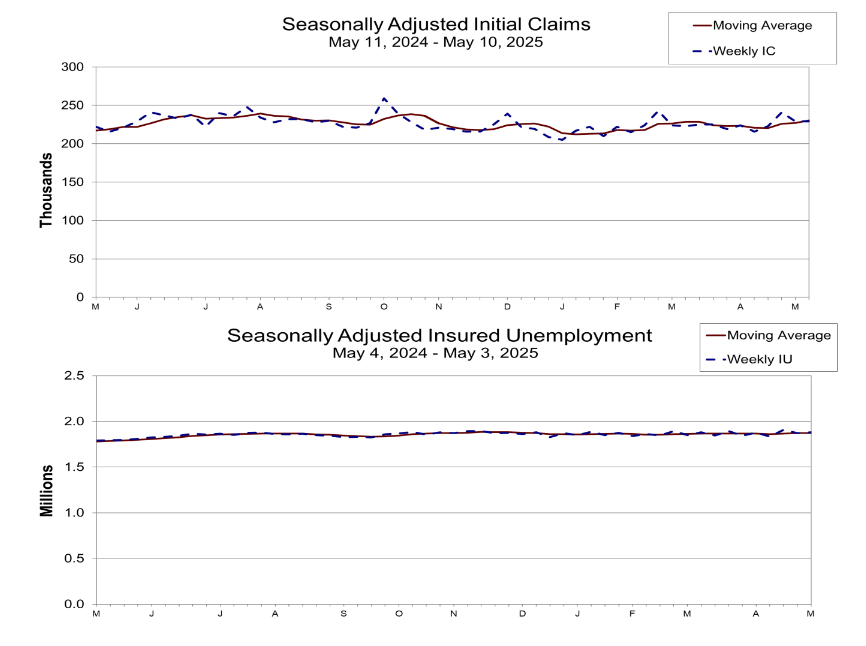

US initial jobless claims unchanged at 229k

US initial jobless claims was unchanged at 229k in the week ending May 10, slightly below expectation of 230k. Four-week moving average of initial claims rose 3k to 230.5k.

Continuing claims rose 9k to 1881k in the week ending May 3. Four-week moving average of continuing claims rose 1k to 1874k.

Eurozone industrial output surges 2.6% mom in March, led by capital goods

Eurozone industrial production jumped 2.6% mom in March, significantly outperforming expectations of 1.7% mom. The surge was driven by strong gains across key categories, including capital goods (+3.2%), durable consumer goods (+3.1%), and non-durable consumer goods (+2.3%). Intermediate goods also posted a modest 0.6% rise, while energy output dipped by -0.5%.

Across the broader EU, industrial production rose by 1.9% mom. Ireland led the gains with a remarkable 14.6% surge, followed by Malta (+4.4%) and Finland (+3.5%). However, there were notable declines in Luxembourg (-6.3%), Denmark, Greece (both -4.6%), and Portugal (-4.0%).

UK economy beats expectations with 0.7% qoq growth in Q1, 0.2% mom in March

The UK economy expanded by 0.7% qoq in Q1, slightly ahead of expectations at 0.6% qoq. Growth was led by a 0.7% qoq rise in the services sector and a robust 1.1% qoq increase in production output, while construction activity was flat. Importantly, real GDP per head also rose by 0.5% qoq, ending two consecutive quarters of contraction.

On the expenditure side, growth was underpinned by a 2.9% qoq rise in gross fixed capital formation, signaling strong business investment. Household consumption also edged up by 0.2% qoq, while net trade contributed positively as exports rose by 3.5% qoq and imports by 2.1% qoq.

Monthly data for March further supported the upbeat quarterly reading, with GDP rising by 0.2% mom, exceeding expectations of flat growth. Services output was the standout, rising 0.4% mom and contributing the most to overall GDP expansion. Meanwhile, construction rose by 0.5% mom, offsetting a -0.7% mom decline in production output.

Australia jobs surge 89k in April, unemployment rate unchanged at 4.1%

Australia’s labor market delivered a strong upside surprise in April, with employment rising by 89k, sharply above expectations of 20.9k. Full-time jobs accounted for 59.5k of the gain, while part-time employment rose by 29.5k.

Unemployment rate held steady at 4.1%, in line with forecasts, as the surge in employment was matched by a jump in labor force participation from 66.8% to 67.1%.

Despite the headline strength, hours worked were largely unchanged on the month. Nonetheless, the employment-to-population ratio rose by 0.3 percentage points to 64.4%, just shy of the record high reached in January.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1136; (P) 1.1201; (R1) 1.1238; More...

Range trading continues in EUR/USD and intraday bias stays neutral. On the upside, break of 1.1292 resistance will argue that correction from 1.1572 has completed after defending 38.2% retracement of 1.0176 to 1.1572 at 1.1039. Intraday bias will be back on the upside for retesting 1.1572. However, sustained break of 1.1039 will dampen this view and target 61.8% retracement at 1.0709 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0789) holds.

US initial jobless claims unchanged at 229k

US initial jobless claims was unchanged at 229k in the week ending May 10, slightly below expectation of 230k. Four-week moving average of initial claims rose 3k to 230.5k.

Continuing claims rose 9k to 1881k in the week ending May 3. Four-week moving average of continuing claims rose 1k to 1874k.

US PPI at -0.5% mom, 2.4% yoy in April, below expectations

US PPI fell -0.5% mom in April, below expectation of 0.2% mom. PPI services fell -0.7% mom while PPI goods was unchanged. PPI less foods, energy and trade services ticked down by -0.1% mom, the first decline since April 2020.

For the 12 months, PPI slowed from 2.7% yoy to 2.4% yoy, below expectation of 2.5% yoy. PPI less foods, energy and trade services rose 2.9% yoy.