Sample Category Title

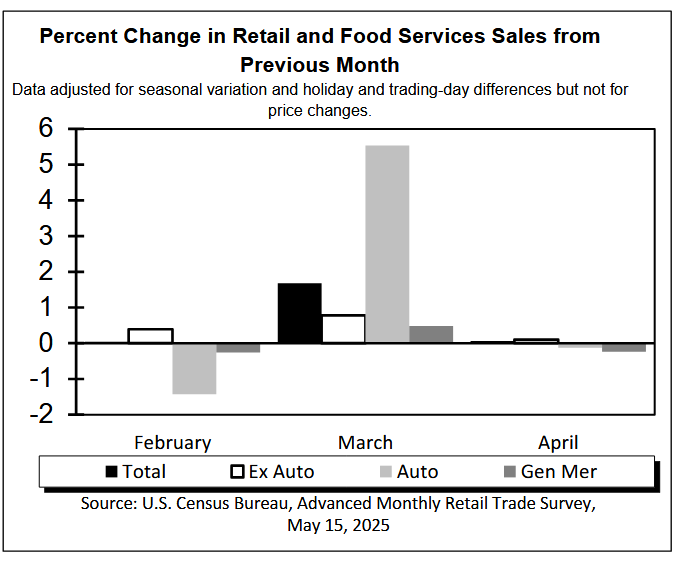

US retail sales rises 0.1% mom in Apr, ex-auto sales up 0.1% mom

US retail sales rose 0.1% mom to USD 724.1B in April, matched expectations. Ex-auto sales rose 0.1% mom to USD 582.5B, below expectation of 0.3% mom. Ex-gasoline sales rose 0.1% mom to USD 673.1B. Ex-auto & gasoline sales rose 02% mom to USD 531.5B.

Total sales for the February through April period were up 4.8% from the same period a year ago.

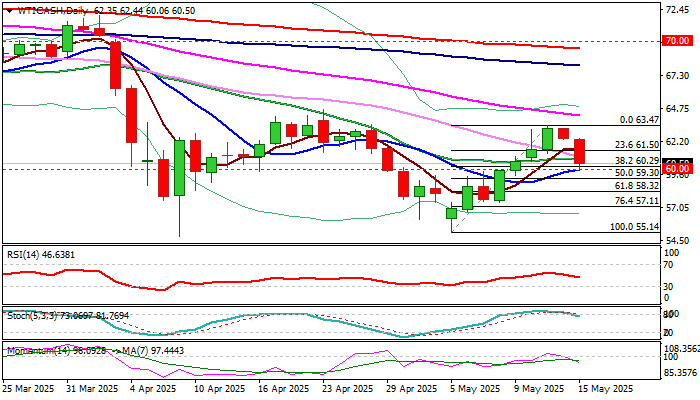

WTI: Oil Prices Drop on Oversupply Concerns as US and Iran Close to Reach a Deal

WTI oil price fell over 3% on Thursday morning, as positive sentiment was soured by the latest encouraging news about US-Iran nuclear talks which may result in easing of sanctions on Iranian oil export and unexpected strong build in US crude stocks that added to growing concerns about oversupply.

Thursday’s strong acceleration extends pullback from recovery top ($63.47) after repeated failure at important Fibo barrier at $63.38 (50% of $71.98/$54.77) and just under the base of falling daily cloud.

Fresh weakness cracked strong supports at $60.29/00 zone (Fibo 38.2% of $55.14/$63.47 recovery leg / psychological, reinforced by 10DMA).

Clear break here to generate fresh bearish signal for deeper drop.

The notion is supported by strengthening negative momentum and stochastic emerging from overbought zone, however bears may face increased headwinds due to significance of supports.

Consolidation above $60 zone may precede fresh push lower, but caution on bounce above $61.50 (broken Fibo 23.6%) which may sideline bears and generate initial signal of an end of corrective phase.

News about progress in US-Iran talks will be closely watched for further direction signals.

Res: 61.00; 61.50; 62.44; 63.00

Sup: 60.00; 59.30; 59.00; 58.32

Australia Employment Soars, Australian Dollar Calm

The Australian dollar is showing limited movement on Thursday. In the European session, AUD/USD is trading at 0.6412, down 0.12% on the day.

Australia job growth surges

Australia's economy added 89 thousand jobs in April, blowing past the market estimate of 20 thousand and above the upwardly revised gain of 36.4 thousand in March. Full-time employment was up an impressive 59.5 thousand. The unemployment rate was unchanged at 4.1%.

Today's jobs report indicates that the labor market remains strong, but that is not expected to change minds at the Reserve Bank of Australia. The money markets have priced in a quarter-point cut at next week's meeting, which would lower the cash rate to 3.85%.

RBA widely expected to lower rates next week

The central bank is expected to cut rates in response to weakening inflation and the uncertainty over US tariffs. Australia's reliant economy could take a significant hit if the US and China trade war continues, which makes the recent tariff deal between the two countries a welcome first step. The agreement, which slashes tariff rates between the US and China, is valid for 90 days and negotiations will continue during that time. Only a few weeks ago, escalating trade tensions threatened to spill into a global trade war but the US has taken a step backwards, reaching a trade deal with the UK and a truce with China.

President Trump's erratic trade policy has roiled the financial markets and made it difficult for the RBA to make inflation and growth forecasts. Still, the RBA appears ready to lower rates next week, which will boost domestic growth. The central bank is expected to remain cautious in its rate policy in the turbulent global economic environment. At home, the labor market has been resilient, inflation is generally under control but consumer spending has been weaker than expected.

AUD/USD Technical

- AUD/USD has pushed below support at 0.6426 and is testing support at 0.6410. Below, there is support at 0.6398

- There is resistance at 0.6438 and 0.6454

AUD/USD 4-Hour Chart, May 15, 2025

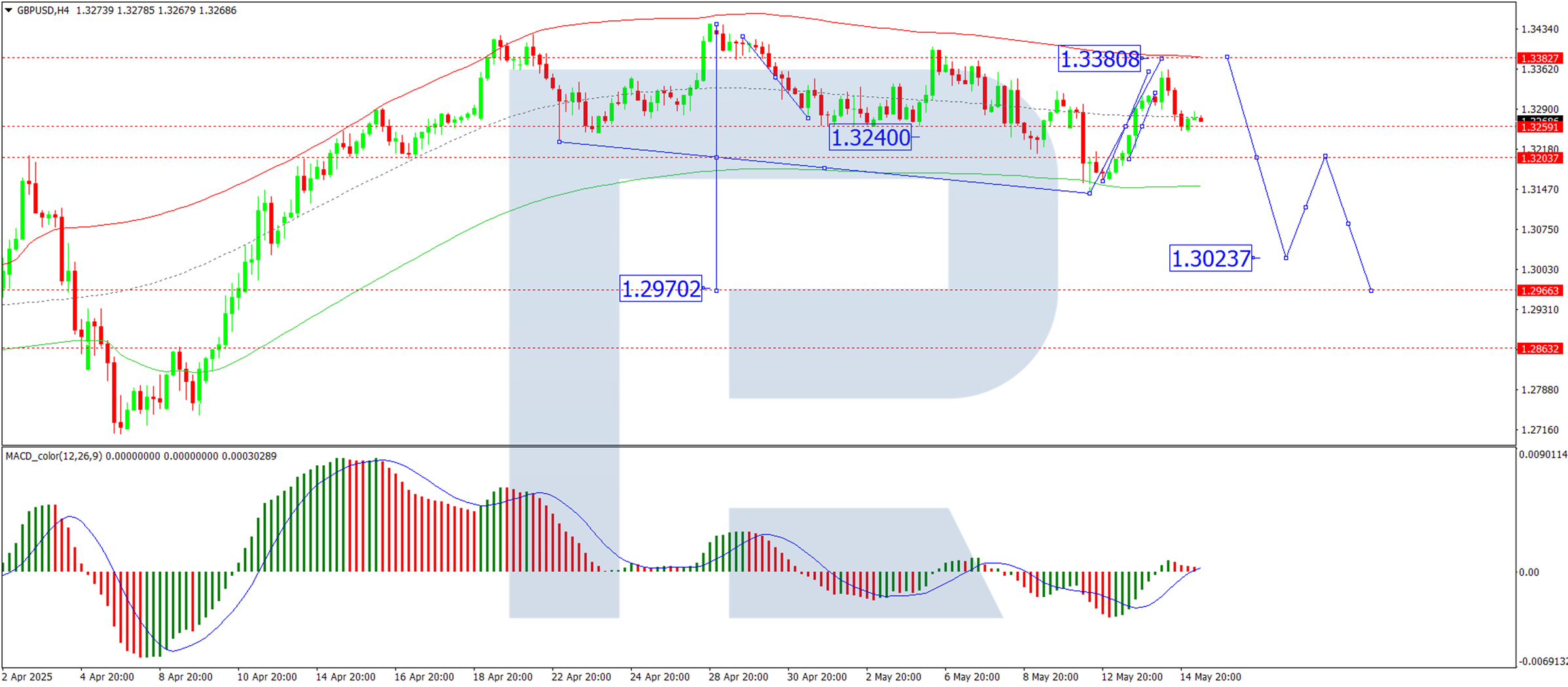

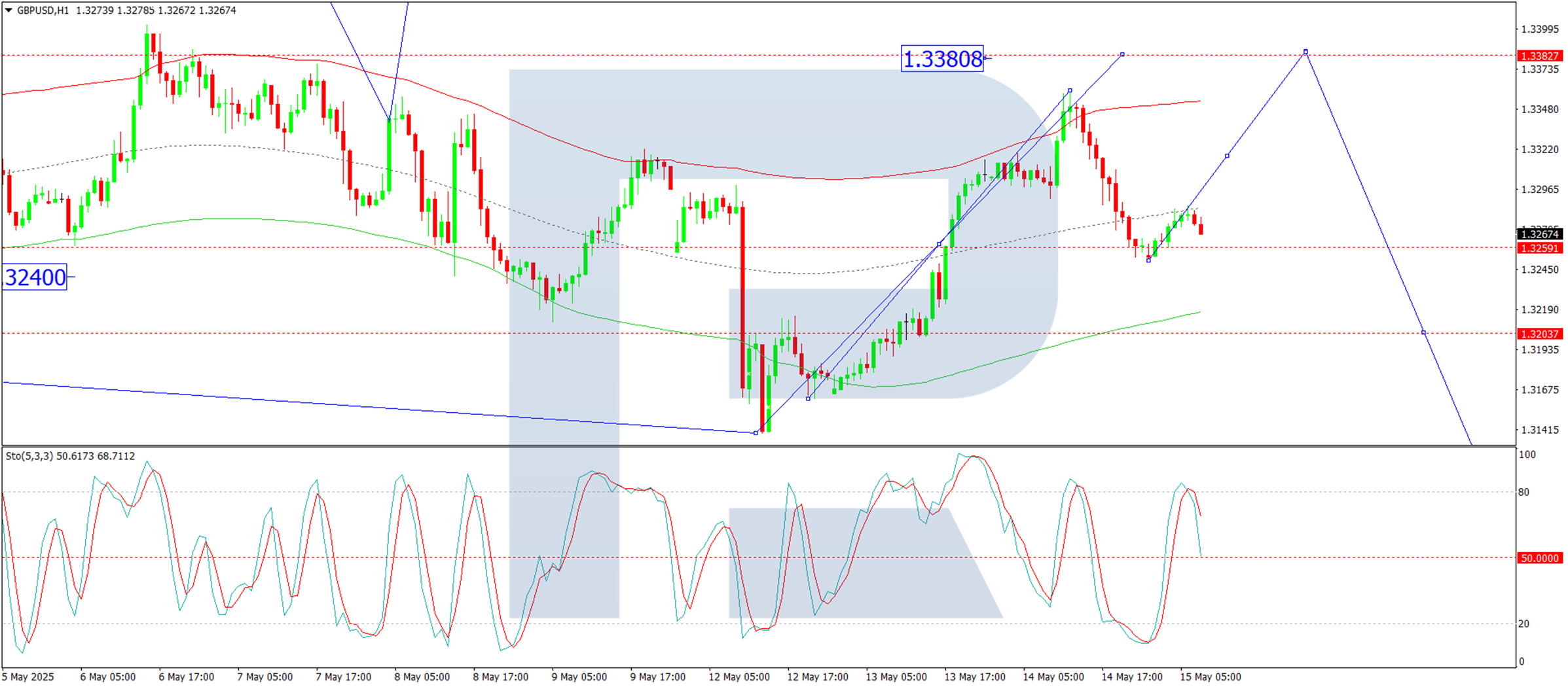

GBP/USD at a Crossroads: Momentum Needed for New Buying Opportunities

The GBP/USD pair has again lost direction, hovering around 1.3283 on Thursday after hitting a seven-day high mid-week.

Key drivers influencing GBP/USD movement

The US dollar weakened on Wednesday, allowing the pound to regain ground. This shift followed ongoing currency negotiations between the US and South Korea, where both parties agreed to continue discussions on exchange rate policies. The reduced demand for the greenback lent support to most major currencies, including sterling.

Domestically, the market focus shifted to the Bank of England (BoE) commentary. Deputy Governor Sarah Breeden emphasised the necessity of long-term reforms in the bond market. At the same time, Monetary Policy Committee (MPC) member Catherine Mann noted that further rate cuts would require more evident signs of easing price pressures – essentially, a sustained drop in inflation.

Meanwhile, the latest UK labour market data revealed an increase in the unemployment rate to 4.5%, the highest since 2021, accompanied by a slowdown in wage growth.

These factors have collectively reinforced expectations of further monetary policy easing by the BoE. Despite internal MPC dissent, last week’s 25bps rate cut caught markets off guard, as many expected a pause in the easing cycle.

Technical analysis: GBP/USD

H4 Chart:

- The pair continues to trade within a broad consolidation range around 1.3260

- The current range extends to 1.3360, with a technical pullback to 1.3260 (testing from above) now underway

- A drop towards 1.3200 is anticipated. A break below this level could extend the downtrend to 1.3100, potentially stretching further to 1.3030

- This bearish outlook is supported by the MACD indicator, whose signal line remains above zero but is trending sharply upward

H1 Chart:

- The pair broke above 1.3260, reaching the local upside target of 1.3360

- Today’s corrective decline is testing 1.3260 again

- A renewed upward move towards 1.3380 is possible if support holds

- The Stochastic oscillator aligns with this scenario, with its signal line above 50 and rising towards 80

Conclusion

The GBP/USD remains in a holding pattern, awaiting fresh catalysts for a decisive move. While technical indicators suggest near-term volatility, the broader trend hinges on BoE policy signals and global risk sentiment. Traders should watch for a breakout beyond 1.3360 or a drop below 1.3200 for clearer directional bias.

DAX Consolidates After All-Time Highs

Asian Session Market Wrap

Asian stocks dropped on Thursday after rising for four straight days, as the boost from US-China trade talks started to fade.

Stocks in Japan, China, and US futures all fell, showing a more cautious mood after a week of strong gains driven by trade progress and steady economic performance. Investors are concerned that stocks have risen so much they could be easily affected by unexpected events. European stock futures also dipped slightly.

The European Open

Heading into the European open, European shares were being weighed down by energy stocks which saw big losses due to falling oil prices, while investors looked ahead to important U.S. economic data and comments from Federal Reserve Chair Jerome Powell.

Oil prices fell over 3% due to the possibility of a U.S.-Iran nuclear deal, which could lift sanctions and increase supply. Big oil companies like BP and Shell saw their shares drop by 5% and 3%, pulling down the main stock index.

Gold prices faltered once more with the precious metal printing an Asian session low of around the $3125/oz handle before recovering to trade around $3158/oz at the time of writing.

Looking at US equities, the mood remained positive in the Asian session as markets still digest a US-China trade truce, a UK agreement, and major Gulf deals which have boosted investor confidence.

The S&P 500 went up by 0.1% overnight, and the Nasdaq 100 rose 0.5%, driven by Nvidia's gains, which erased its 2025 losses.

Following the European open however, both the S&P 500 and Nasdaq have turned red for the day, trading 0.57% and 0.85% lower respectively.

On the FX front, safe-haven currencies like the Japanese yen and Swiss franc strengthened, with the yen rising 0.6% to 145.88/USD after hitting a one-month low of 148.65 earlier this week. The Swiss franc also gained 0.6%, reaching 0.8376/USD.

The euro increased by 0.2% to 1.12. A Bloomberg report on Wednesday mentioned that the US is not pushing for a weaker dollar in tariff talks, which helped ease market worries.

The dollar index, which tracks the dollar against six other currencies, fell 0.2% to 100.81 but is still set to gain 0.4% for the week. However, the index is down nearly 7% for 2025.

Currency Power Balance

Source: OANDA Labs

Economic Data Releases and Overall Sentiment

Looking at market sentiment, it remains largely positive. The main focus will be U.S. retail sales data, and investors will also watch for updates on potential trade deals following the U.S.-China tariff truce.

There will also be a speech by Fed Chair Jerome Powell and earnings from Walmart which could rattle markets ahead of the US Open.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the day - DAX

From a technical standpoint, the DAX index has been consolidating above a key support area having printed fresh all-time highs on Monday.

The support area between 23212 and 23471 continues to hold firm underpinning the index and providing bulls with optimism that another bullish leg may be in offing.

A move higher still needs a clear break and acceptance above the 24000 handle which could lead to a bigger move to the upside.

On the downside, a break of support at 23212 could open up a retest of the 20 and 50-day MAs which rest at 22704 and 22460 respectively.

DAX Daily Chart, May 15, 2025

Source: TradingView.com (click to enlarge)

Gold Price Drops to Lowest Level in Over a Month

As shown on the XAU/USD chart, the price of gold fell below $3,130 this morning – its lowest level since 10 April.

Since its peak in May, gold has lost more than 8% in value per ounce.

Why Is Gold Falling?

Bearish sentiment in the gold market may be fuelled by easing geopolitical tensions. According to media reports:

→ China and the US have already reported progress in reaching a trade agreement, while details of potential deals with India, Japan, and South Korea are currently being developed.

→ Iran is reportedly willing to sign a nuclear deal in exchange for the lifting of sanctions. In addition, Donald Trump may lift sanctions on Syria during his visit to the Middle East.

→ The situation between India and Pakistan has stabilised, and today, talks between Russia and Ukraine are expected to take place in Istanbul, with a potential ceasefire on the agenda.

These developments could be seen as reducing the appeal of gold as a safe-haven asset.

Technical Analysis of the XAU/USD Chart

In our 7 May gold price analysis, we:

→ outlined a descending channel (marked in red);

→ noted that bearish pressure persisted above $3,400.

Since then, the gold (XAU/USD) price has continued to move within this channel, breaking support around the $3,200 level and approaching a key support zone formed by:

→ the lower boundary of the red channel;

→ a long-term trendline (marked in blue);

→ a former resistance level (highlighted with arrows) at $3,140.

Given these conditions, traders should consider a scenario in which a minor rebound may occur – for instance, towards the median line of the red channel.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

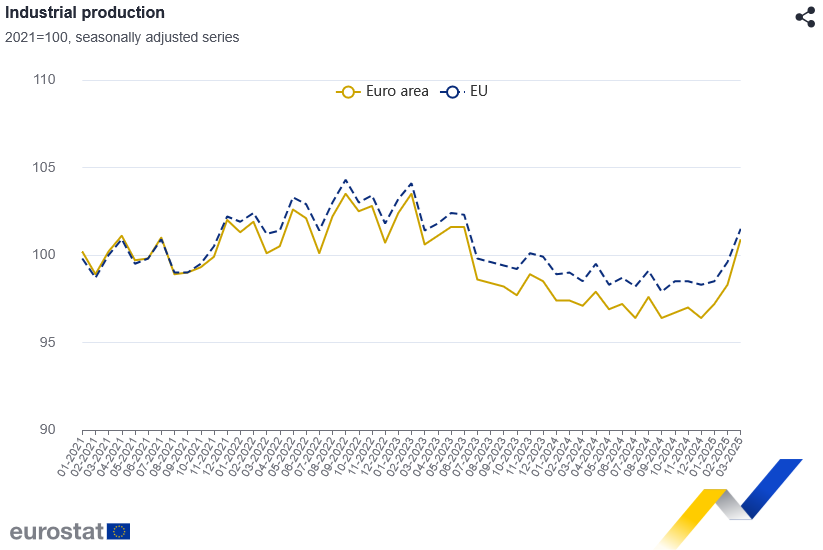

Eurozone industrial output surges 2.6% mom in March, led by capital goods

Eurozone industrial production jumped 2.6% mom in March, significantly outperforming expectations of 1.7% mom. The surge was driven by strong gains across key categories, including capital goods (+3.2%), durable consumer goods (+3.1%), and non-durable consumer goods (+2.3%). Intermediate goods also posted a modest 0.6% rise, while energy output dipped by -0.5%.

Across the broader EU, industrial production rose by 1.9% mom. Ireland led the gains with a remarkable 14.6% surge, followed by Malta (+4.4%) and Finland (+3.5%). However, there were notable declines in Luxembourg (-6.3%), Denmark, Greece (both -4.6%), and Portugal (-4.0%).

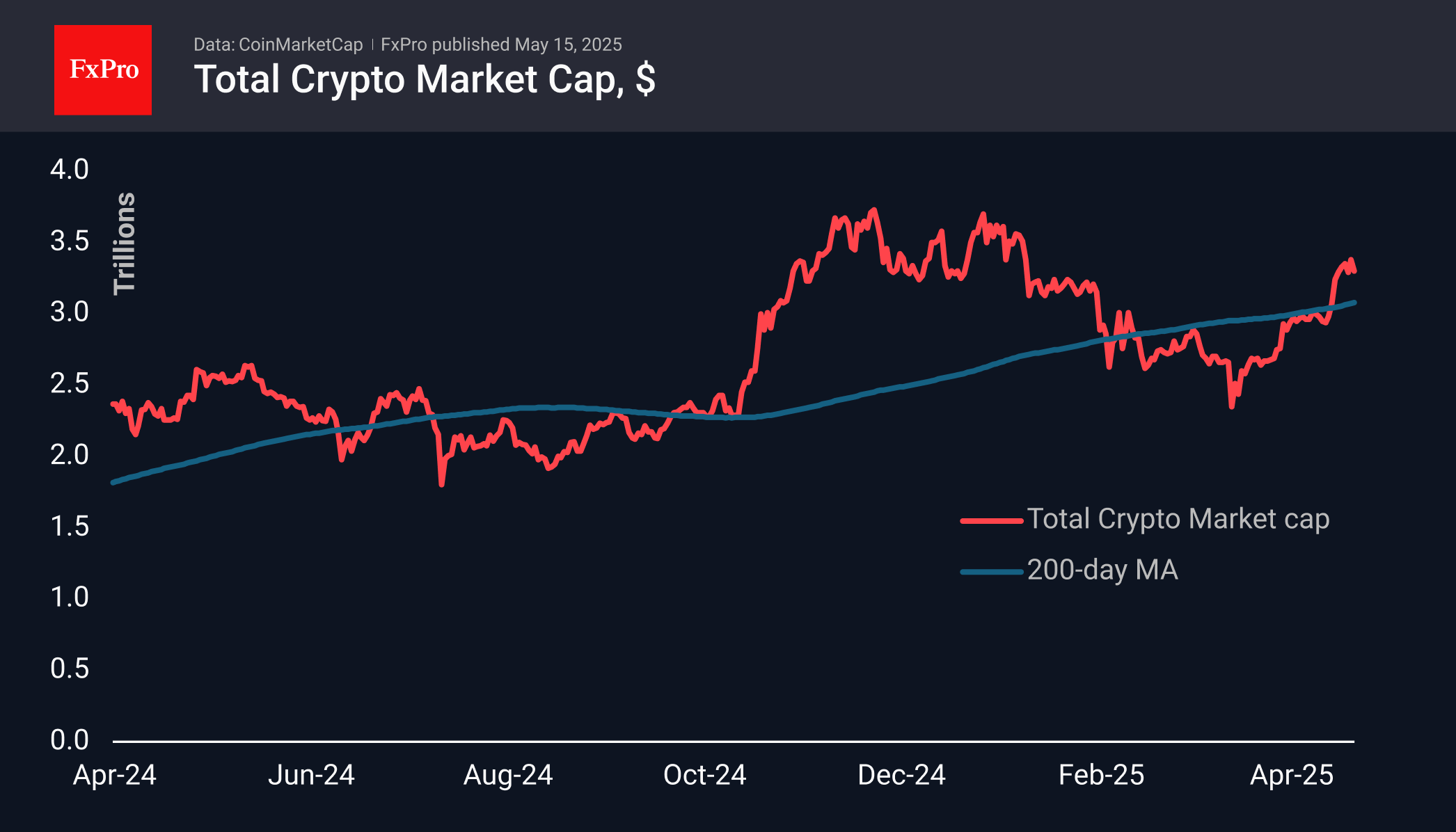

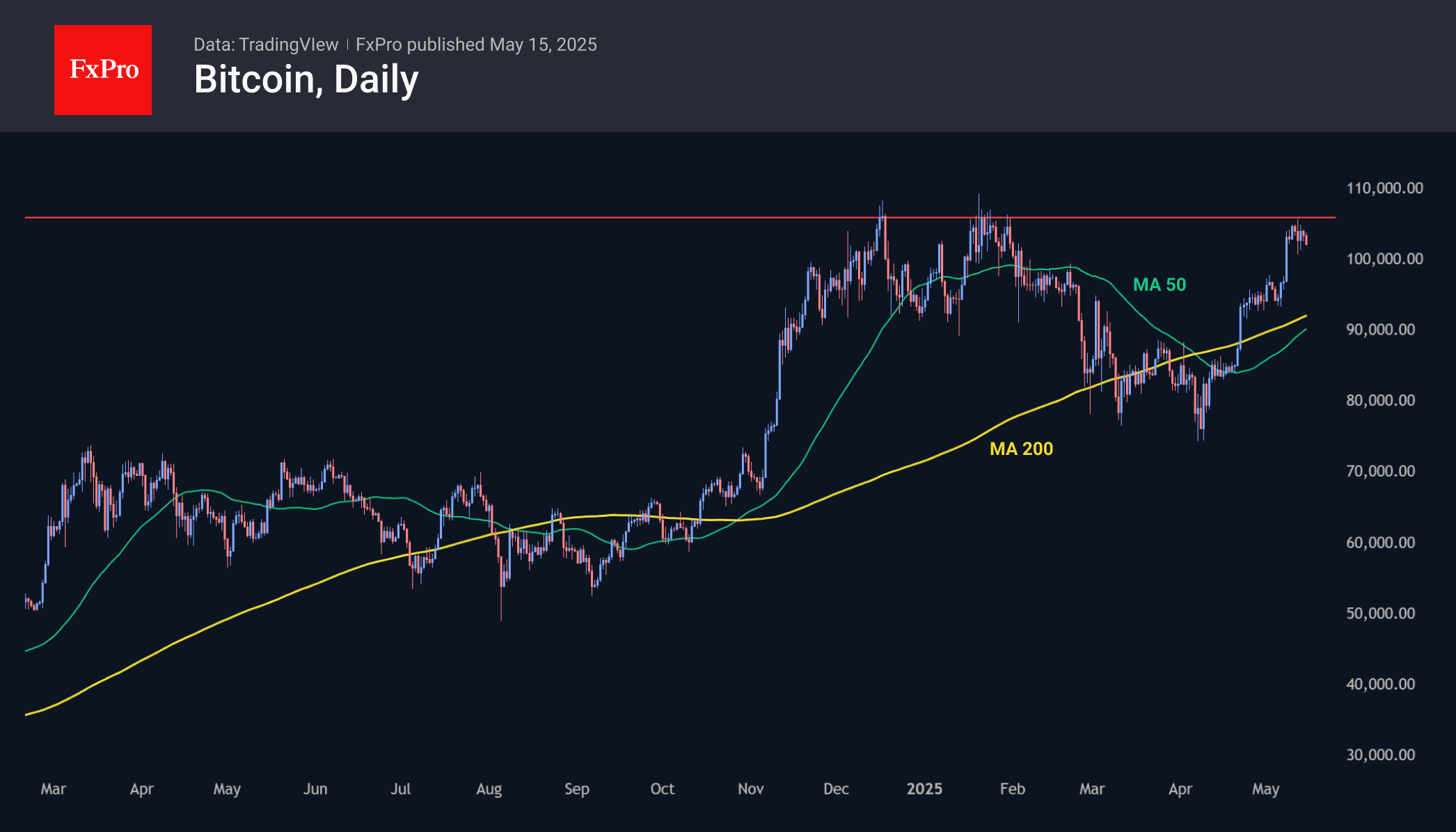

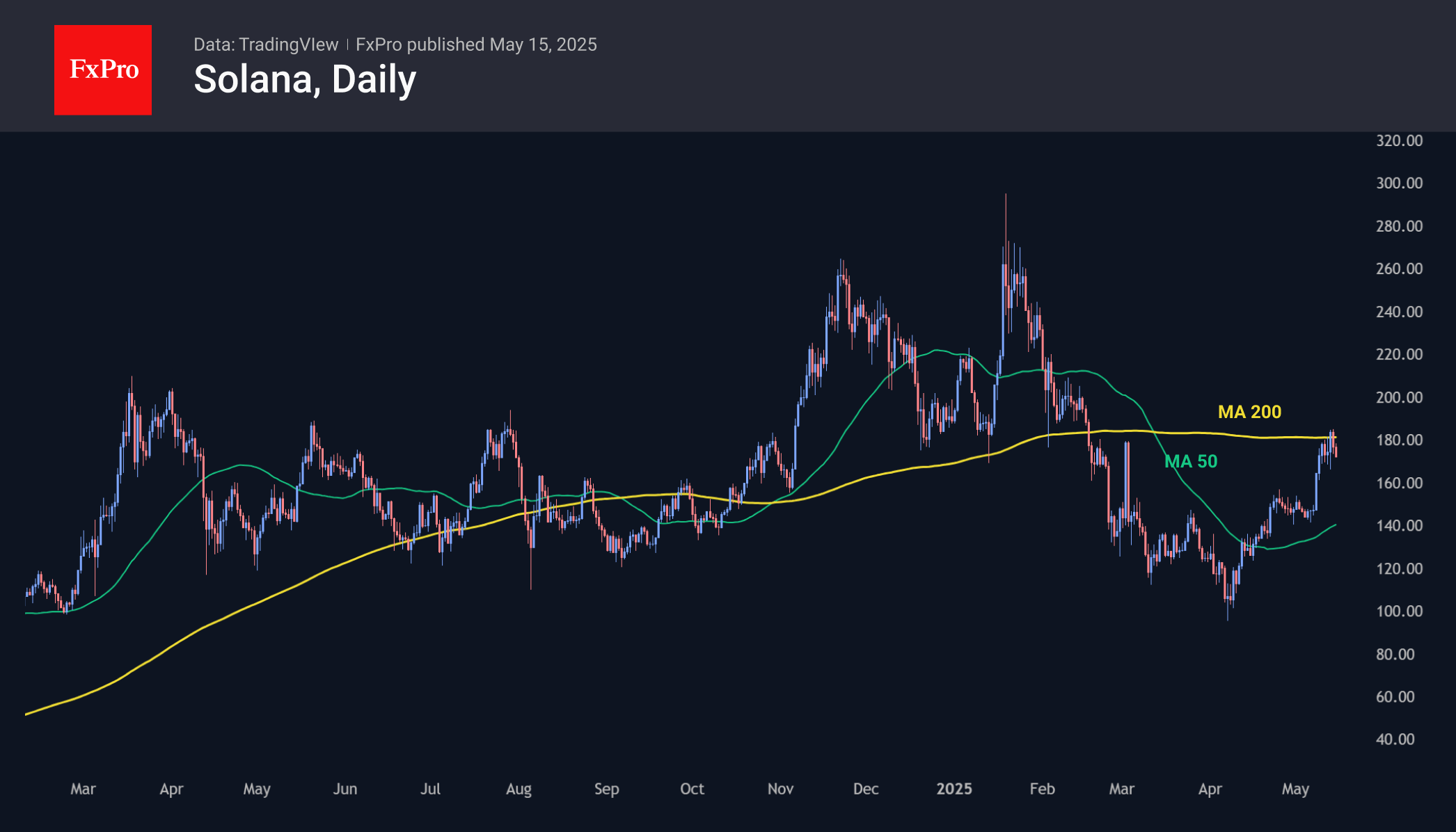

Altcoins Consolidating Their Strength by Joining Bitcoin

Market Picture

Market capitalisation has fallen 2% in the last 24 hours to $3.30 trillion. Bitcoin, stuck near past highs, quickly spoiled the market’s mood, triggering a local profit correction after the rally. An active correction in gold may also be playing a role.

The crypto market sentiment index rolled back from 73 to 70, while remaining at an ‘elevated level’, implying positive sentiment and sufficient risk appetite.

Bitcoin retreated 1.5% to $102.0k, having been smoothly forming a top for the past seven days. This is a signal of an impending correction, which is reasonable near previous peaks and against the backdrop of slippage in the equity market.

Ethereum and Solana have stalled near their 200-day moving averages. Optimists may look at this as a stop to gain strength before a further hike upwards. Pessimists, on the other hand, may point out that BTCUSD took its 200-day MA last month in a strong move, with confidence that the leading altcoins are lacking right now.

News Background

Bitcoin’s current growth, unlike previous ones, is driven by strong demand on the spot market rather than leveraged speculation, according to K33 Research. This sets the stage for a renewal of historical highs. Experts do not expect unpleasant surprises from May, which is a weak month.

CryptoQuant noted that retail investors are increasingly active despite Bitcoin’s consolidation above $100,000. Such a resurgence is often a sign of renewed confidence and could be an additional catalyst for the next price move.

Wealthy UBS clients in Asia are shifting their focus from dollar assets to gold, cryptocurrencies and Chinese markets. Switzerland’s largest bank cites growing geopolitical uncertainty and persistent volatility as the main reasons.

Tether reported to the SEC that it bought 4,812 BTC worth more than $458 million for Twenty One Capital’s pending SPAC merger with Cantor Equity Partners.

US Retail Sales on Today’s Menu

In focus today

In the US, a range of data is due for release in the afternoon. April retail sales will provide the first hard data evidence on how consumer behaviour has reacted to higher tariffs. April PPI will provide further sense of the cost pressures that US firms are facing after the tariffs took effect. First regional manufacturing indices from the NY Fed and Philly Fed will provide a more forward-looking sense of the business cycle.

In the euro area, we receive the second estimate of GDP growth in Q1 2025. The first estimate showed larger than expected growth at 0.35% q/q. Focus in the second estimate will thus mainly be on the employment data that we also receive. Employment growth slowed down in the final quarter of 2024 but remained positive at 0.1% q/q. Soft indicators point to broadly the same growth rate in Q1 2025 or slightly lower, overall indicating a stagnating labour market, but with record-high employment despite the weak growth.

Also in the euro area, we keep an eye on industrial production data for March, which likely increased further, in a sign that activity has bottomed out, but also with potential front-loading distortions from the US trade policy.

In Norway, we expect that mainland GDP rose by 1.0 % in Q1, marking the strongest quarterly growth in close to three years. This would surpass Norges Bank's March forecast of 0.6%, suggesting the potential need for rate cuts may be lower than expected. The big question is whether the Q1 recovery was influenced by unfulfilled rate cut expectations in March.

Also, the government will publish the Revised Budget 2025, with no significant changes expected in the fiscal policy framework. The withdrawal from the State Petroleum Fund will probably increase to around 3%, driven by lower fund values and increased support for Ukraine, with minimal impact on Norway's activity level.

In Sweden, we receive inflation expectations from Origo (Prospera). It will be interesting to see if there are any signs of rising expectations, as we saw among firms in the NIER survey.

In Japan, Q1 national account data will be released overnight. Even if Q1 is a long time ago, it is not irrelevant for the picture of the fragile economic recovery and the prospects for further rate hikes from the BoJ. Data out so far suggests close to a standstill in GDP, as import growth will likely constitute a drag following a comeback from Q4. Also, particularly a surge in food prices weighs on private spending. Wage increases will compensate for it once implemented over the summer.

Economic and market news

What happened overnight

In geopolitics, Thursday's peace talks in Turkey, focused on the Russia-Ukraine conflict, will unfold without the presence of President Putin and Trump, lowering expectations for significant progress. President Zelenskyy has earlier stated that he will attend only if Putin is present.

What happened yesterday

In the US, The Fed's Daly said late yesterday that the strength of US economy allows policymakers to be patient, which is well in line with comments heard from other FOMC participants since the May meeting.

In Germany, the final inflation print for April confirmed the flash release of 2.1% y/y in CPI and 2.8% y/y in core CPI. Core inflation was higher than expected in the flash release and the final estimate allows us to digest which categories contributed to this. The move higher was especially due to Easter being in April this year compared to March last year. This is visible as prices on package holidays rose 9.2% y/y, passenger transport 11.3% y/y, and air tickets 19.1% y/y. It suggests that the increase in April should be seen more as a one-off rather than a resurgence of price pressures in core services.

In Sweden, inflation figures have been released with CPI at 0.3% y/y, CPIF at 2.3% y/y, and CPIF excl. energy at 3.1% y/y, aligning with flash estimates. Core inflation was driven by international flight costs, while food prices rose 0.2%, slightly below the forecast. Energy prices and mortgage costs were in line with our forecast. Core inflation's surprise led to a 0.15 percentage point forecast error across all inflation measures. We expect inflation to remain slightly above target this year and return to target next year, anticipating the Riksbank will uphold its stance given the enhanced risk environment.

We also received minutes from the Riksbank, revealing board consensus on higher-than-usual uncertainty. While elevated core inflation is expected to soften, the tariff impact is deemed marginal. The board views the economy as weaker than March forecasts, suggesting easing inflationary pressures and a potential rate cut as a next step. We consider a rate cut becoming more likely, but June is premature, with timing uncertain thereafter.

In China, April's credit data revealed a sharper-than-expected decline in new loans to CNY 280bn (cons: CNY 700bn), amid ongoing trade tensions with the US that have further dampened market appetite during a typically slow month for loan demand. The M2 money supply surprised to the topside, rising by 8.0% y/y, reflecting the government's stimulus efforts.

Equities: Equities lost steam on Wednesday. Most regions were lower, including Stoxx 600 -0.5%, Nordic -0.4% but S&P 500 up 0.1% (but equal weighted -0.6%). So, the US outperformance continues, although it is entirely subscribed to the MAG 7 stocks. S&P 500 is now up 9% over the last month, a few decimals ahead of Stoxx 600. Although indexes took a breather yesterday, risk-on remains with a clear cyclical preference. Futures are a notch lower this morning together with Asian markets.

FI&FX: The post trade-deal risk rally is losing steam with notably the JPY marking a comeback over the last 24 hours with USD/JPY moving back to 146. In the Scandies, EUR/NOK has rebounded back above 11.60 while EUR/SEK is back close to the 10.90 mark. Despite a temporary spike higher EUR/USD is close to unchanged since Tuesday evening. Overnight, USD rates have rallied somewhat driven by the short end resulting in a slight steepening pressure. This has reversed the USD flattening/rise in USD rates from yesterday's session where NOK rates notably underperformed European peers.

Dollar Hit by Headlines that US Seeking Engagements on a Weaker Dollar at Trade Negotiations

Markets

There were very few eco data to guide global trading yesterday. (US) equities took a breather. Details on US trade agreements with the likes China and the UK still have to be hammered out. This is also the case for (framework) deals with other trading partners. For now, equity investors felt enough trade de-escalation might have been discounted. The S&P closed little changed (+0.1%). Headlines on commercial deals during Trump’s Middle East trip still triggered some Nasdaq outperformance, but also here the risk momentum appears to be slowing. Core yields markets didn’t find a clear direction in European trading, but again took the path north in US dealings. At the short end of the curve, better/less negative economic prospects only reinforced the case of Powell’s reactive policy approach. The 2-y yield regained the 4.0% mark (+5.1 bps). LT yields also continued their recent assent. Here, probably it’s not only better economic prospects at work. As the Trump fiscal package is moving its way through the committees of Congress, the theme of fiscal sustainability is also again looming (cf infra). The US 10-y added 7.1 bps. The 30-y is coming ever closer to the 5.0% psychological barrier (4.96%, + 6.3 bps). German yields also again gained a few bps (0.5 bp to 2.5 bps across the curve). UK gilt yields in a similar way added 4-5 bps. Higher (less low) for longer is again becoming mainstream on core yields markets. On FX, the dollar was hit by headlines that the US was seeking ‘engagements’ on a weaker dollar at trade negotiations with trading partners, e.g. South Korea. The rumours evidently weren’t confirmed by any of the parties involved, but markets picked up the message. After gaining on recent US reflationary spirits, the dollar rally was blocked. After spiking lower intraday, DXY closed the session little changed at 100.03. Idem for EUR/USD (close 1.1175). The yen outperformed (USD/JPY close 146.75).

This morning, Asian equities are facing some profit taking after recent rally. US yields are holding little changed. The dollar is losing further ground, especially against the likes of the yen (USD/JPY 146.05). EUR/USD is again nearing the 1.12 big figure. Later today, the eco calendar is better filled with the EMU Q1 GDP, the US empire manufacturing survey, the Philly Fed business outlook, US April retail sales, PPI & jobless claims. Most of these releases probably mirror the brisk swings in expectations post the Libation Day announcements. In this respect, it won’t be easy for markets to draw any conclusions on what to expect going forward. If anything, good/better than expected data still might solidify the bottom for core real yields. At the same time, after yesterday’s price action, it’s doubtful this will be much of a help for the dollar. The US currency is at risk being captured again in a sell-on-upticks pattern. This morning, UK Q1 GDP surprise on the upside (0.7% Q/Q and 1.3% Y/Y), but details were a bit mixed (poor consumption, solid capital formation). In a first reaction, sterling is gaining a few ticks (0.843).

News & Views

The US Committee for a Responsible Federal Budget estimates that the developing House reconciliation bill will add roughly $3.3tn to US debt through the fiscal year 2034 as written or $5.2tn if made permanent. Under current law, debt is projected to rise from nearly 100% of GDP today to 117% by 2034. Adding the impact of the reconciliation bill, this would be 125% or even 129% of GDP. Total yearly deficits would rise dramatically – from $1.8tn in 2024 to $2.9tn by 2034 under the bill and $3.3tn under a permanent version of the bill. As a share of GDP, yearly deficits would rise to 6.9% – or 7.8% if the bill were extended permanently. Interest costs alone would make up a large share of that borrowing, doubling from nearly $900bn in 2024 to $1.8tn (4.2% of GDP) by 2034 as written, or to $1.9tn (4.4% GDP) if permanent. This excludes dynamic effects where higher debt boost interest rates.

Australian employment increased by 89k in April, up from 36.4 in March and significantly beating the consensus estimate (+22.5k). Details showed the lion share of occupations coming from full time jobs (+59.5k). Employment has grown by 390k people, or 2.7%, over the year. This annual growth rate is higher than the population growth rate for people aged 15 years and over, which was 2.1% over the same period. The unemployment rate stabilized at 4.1%, but the labour force participation rate increased from 66.8% to 67.1%. Yesterday, the Australian Bureau of Statistics released wage growth numbers. Those showed an acceleration from 0.7% Q/Q in Q4 2024 to 0.9% in Q1 2025 (+3.4% Y/Y). Despite labour market strength and slightly higher than expected Q1 CPI numbers, money markets stick to the view that the Reserve Bank of Australia will lower its policy rate by 25 bps to 3.85% when it meet next week. The RBA implemented a first cautious rate cut in February this year followed by a status quo in April.