Sample Category Title

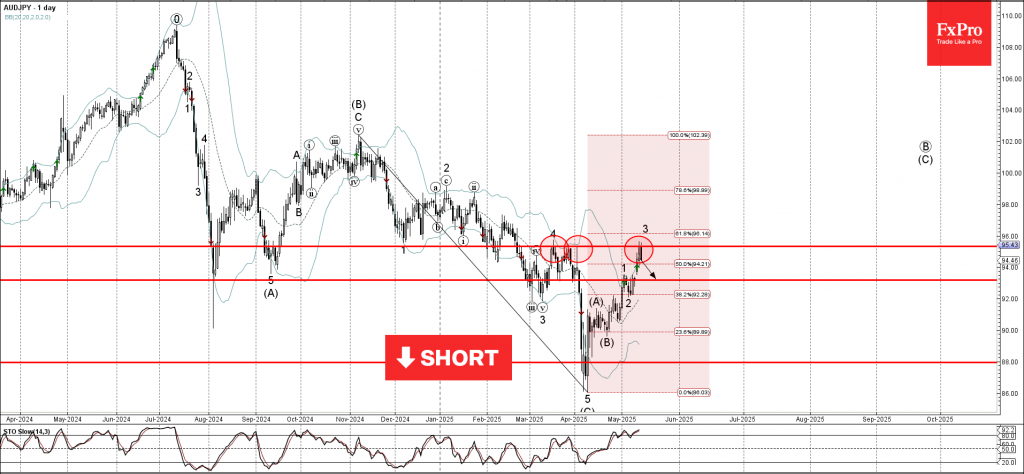

AUDJPY Wave Analysis

AUDJPY: ⬇️ Sell

- AUDJPY reversed from resistance area

- Likely to fall to support level 93.20

AUDJPY currency pair recently reversed from the resistance area between the key resistance level 95.30 (former monthly high from March), upper daily Bollinger Band and the 61.8% Fibonacci correction of the downward impulse wave (C) from November.

The downward reversal from this resistance area stopped the earlier short-term impulse wave 3 from the start of May.

Given the overbought daily Stochastic and strongly bullish yen sentiment, AUDJPY currency pair can be expected to fall to the next support level 93.20.

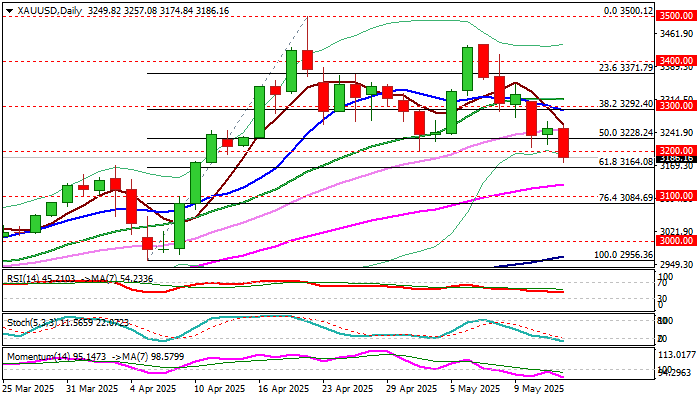

XAU/USD: Gold Price Falls Further as US-China Trade Deal Fuels Risk Appetite

Gold price fell through key supports on Wednesday, deflated by growing optimism on US-China trade deal that cooled fears about deeper economic crisis and offset other factors that boost safe haven demand.

Fresh wave of risk appetite pushed gold through pivots at $3228 (50% retracement of $2956/$3500 upleg) which recently contained several attacks and $3200 (psychological/low of pullback from new record high).

Sustained break of $3200 to complete bearish failure swing pattern and generate signal of potential deeper pullback from $3500 peak.

Daily studies are weakening as 14-d momentum is heading deeper into negative territory and the price fell below 10/20/30 DMA’s which also formed bear-crosses.

However, oversold stochastic warns of possible increased headwinds that may result in hesitation at $3200 zone and keep near term price action in extended consolidation.

The price should stay under broken Fibo 50% ($3228) and extended upticks not to exceed daily highs of Tuesday / today ($3265/57 respectively) to keep bears intact.

Res: 3200; 3228; 3265; 3292.

Sup: 3164; 3126; 3100; 3084.

Fed’s Jefferson: Moderately restrictive policy well positioned as growth and inflation risks rise

Fed Vice Chair Philip Jefferson said in a speech today he supported last week’s decision to keep the federal funds rate unchanged, which he views as “moderately restrictive.” He noted that the current policy setting is “well positioned” to respond to a range of evolving economic conditions.

Jefferson pointed to a sharp decline in consumer and business sentiment this year, saying he is closely monitoring "hard data" for signs of weakening economic activity.

On the inflation front, he acknowledged that higher tariffs could add upward pressure to prices in the months ahead, though it remains uncertain whether such effects would prove “temporary or persistent.”

With elevated risks to both sides of the dual mandate, Jefferson said "the current stance of monetary policy is well positioned to respond in a timely way to potential economic developments."

Sunset Market Commentary

Markets

There were hardly any data with market moving potential and for now no trade-related headlines from US president Trump to guide trading today. European equities are taking a breather after the recent rebound (EuroStoxx 50 -0.1%). US indices open marginally higher after yesterday’s (tech) rebound on president Trump’s announcement of several eye-catching contracts in the Middle East. Core bond markets were mainly mired on technical trading. The US curve steepens slightly with yields adding between 0.5 bps (2-y) and 3.2 bps (30-y). German bunds slightly outperform Treasuries, with yields easing about 1.0 bp across the curve. Fortunately, FX markets at least provided a bit more of animateness. The dollar at the end of the Asian trading dropped in an otherwise calm market. The move was triggered by comments on financial news wires (Bloomberg) referring to people familiar with the trade talks between the US and South Korea earlier this month saying they also discussed FX policies. This caused markets to ponder whether an outright weaker dollar might also get more weight in trade talks with other trading partners. For now there is no official reaction to the reports. Even so, the SK won after tentatively easing this morning currently trades more than 1% stronger in a daily perspective. The move also spilled over the yen. USD/JPY currently trades near 146.25, off the intraday lows, but to be compared with an intraday top of 147.67 early in Asian dealings. The euro is also captured by this overall USD setback, but underperforms the likes of the yen. EUR/USD regained the 1.12 mark but struggles to make further progress (1.1215). EUR/JPY yesterday intraday at 165.1 came with reach of the 166.7 end October top, but today eases to 164.15. Even as US trade negotiations with the EU are rumored to have made little progress for now, the topic of a too weak currency likely is more of an issue for Asian currencies rather than for the EU (only Germany is on the monitoring list of the US Treasury Department). As indicated above, the move today was mainly limited to FX markets and it is not evident for officials from the countries involved in trade talks to openly comment on this topic. Also from a US point of view, there are risks to openly push for a weaker USD as it might revive the sell US trade that was a source of elevated market volatility last month. In this respect, we keep still also keep an eye at the very long end of the US curve. The US 30-y yield is again within reach of the 5.0% barrier (4.94%). The latest rebound in US yields mainly was for a ‘good reason’ (reflation on a de-escalation in trade tensions). However, LT US yields surpassing 5.0% (whether due a risk of USD weakness, due to doubts or fiscal sustainability or whatever other reason) soon might tilt to becoming a renewed source of (global) uncertainty.

News & Views

The Kingdom of Belgium launched a new 5-yr bond via syndication today. OLO 105 (Oct2030) was prices to yield MS +28 bps, compared with guidance in the MS +30 bps area; allowing the debt agency to raise €7bn with books above €72bn. The BDA now raised €27.6bn of its €42bn 2025 OLO funding need (65.5%). The lion share came from syndicated deals following a new long 10-yr (€7bn OLO103 3.1% Jun2035) and a long 15-yr (€5bn OLO 104 3.45% Jun2042) earlier this year. They also raised $1bn via a 10-yr USD benchmark within the framework of the EMTN programme. If the debt agency sticks to its funding plan, this was the final new OLO of the year with the remainder of the funding need to be raised via regular monthly auctions. The May auction is cancelled, leaving five more on the calendar (no planned in August). The means an average of €2.88bn to be raised at each occasion which is in line with traditional targeted amounts (€3bn area).

National Bank of Poland Kochalski sees a pretty good change of a decision on rate cuts in July. His base case is a 25 bps cut, but he doesn’t rule out copying this month’s 50 bps move. Overall, he sees scope for 50-75 bps of easing by end 2025. Yesterday, NBP Janczyk suggested a preference to a 50 bps rate cut somewhere this year if inflation and wage growth stay soft. In the short run, attention shifts to Polish presidential elections. The Polish president is more than a ceremonial function with the current president, linked to the previous Law and Justice party, complicating PM Tusk’s policy making. The latter’s candidate (Trzaskowski) is expected to come out on top in Sunday’s first round of voting with a second round run-off against the PiS-candidate (Nawrocki) expected on June 1st. Polls also favour Trzaskowski over Nawrocki in that tie. EUR/PLN holds steady around 4.24 after the zloty recovered partly from April losses thanks to the risk rebound.

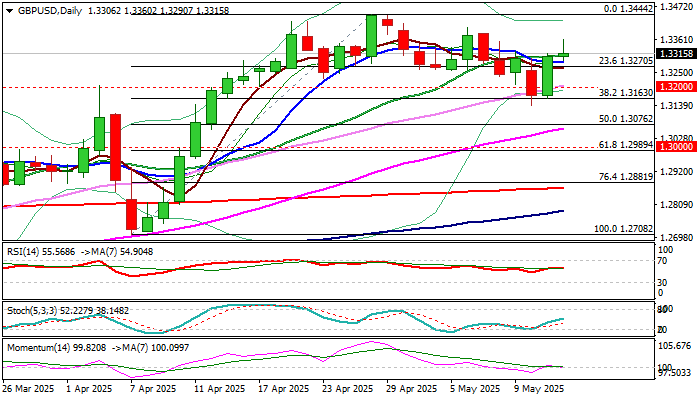

GBP/USD: Bulls Hold Grip Ahead of UK GDP Data

Cable keeps firm near term tone and extends recovery after Tuesday’s 1% rally generated positive signal on over 50% retracement of 1.3444/1.3139 pullback and completion of bullish engulfing pattern on daily chart.

Fresh extension higher on Wednesday rose above Fibo 61.8% retracement that adds to development of reversal signal, after strong bounce on Tuesday signaled that corrective phase from new 2025 high (1.3444) is likely over.

Formation of bear-trap under Fibo 38.2% of 1.3444/1.3139 contributes to positive near-term outlook, along with predominantly bullish daily studies.

Traders focus on tomorrow’s releases of UK GDP data, with expectations for 0.6% growth in Q1 being significantly above 0.1% growth in the first three months of 2024, although economists see flat growth in March compared to 0.5% expansion in the previous month.

Sterling would benefit from better than expected GDP data that would also ease pressure on BOE to cut rates again in June (bets for June cut have dropped significantly after May’s hawkish cut).

Also, a trade deal with the US would ease uncertainty and improve economic situation on removing one of major obstacles for economic growth.

Res: 1.3360; 1.3402; 1.3444; 1.3500.

Sup: 1.3270; 1.3232; 1.3200; 1.3162.

Yen Posts Sharp Gains as PPI Hit 4 Percent

The Japanese yen has posted strong gains for a second straight day. In the North American session, USD/JPY is trading at 146.32, down 0.79% on the day. The yen plunged 2.1% on Monday but has now recovered those losses.

Japan's PPI eases slightly to 4%

Wholesale inflation in Japan remained high, rising 4% y/y in April. This was slightly lower than the revised 4.2% gain in March and was in line with expectations. This is the fourth straight month that PPI has been at 4% or higher, as companies continued to pass on costs to consumers. Food prices have been rising, led by rice prices which have doubled over the past 12 months.

The Bank of Japan has been carefully monitoring inflationary pressures as it looks to continue hiking interest rates on the path to monetary normalization. The BoJ raised rates in January but has stayed on the sidelines since then and is in a wait-and-see mode until there is more clarity about President Trump's tariff policy. The Bank meets next on June 17.

The 90-day tariff deal between the US and China has raised hopes that Trump will reach trade deals with China and other countries. Japan sends 20% of its exports to the US, which is Japan's largest trading partner and trade talks are underway between the two countries.

Fed in a wait-and-see mode

The US inflation report was particularly important as Trump's tariffs took effect on many products in April. Inflation rose in April but was lower than expected. The full impact of the tariffs, which could send inflation lower, may not be seen until June or July.

The Federal Reserve is also in a wait-and-see mode. At last week's Fed meeting, Fed Chair Powell pushed back against Trump, who has called for the Fed to lower rates. The Fed is widely expected to hold rates at the June 18 meeting.

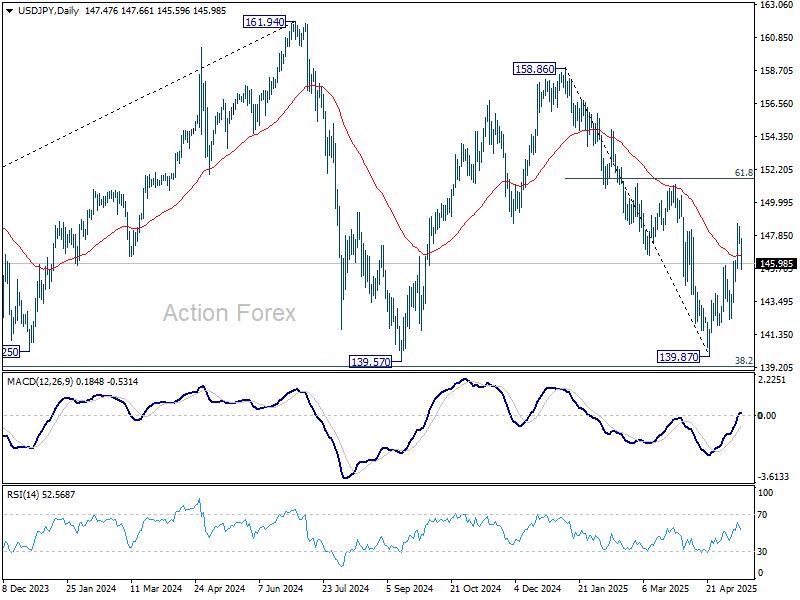

USD/JPY Technical

- USD/JPY has pushed below support at 147.06 and 146.64. The next support level is 145.91

- 147.79 and 148.21 are the next resistance lines

USDJPY 1-Day Chart, May 14, 2025

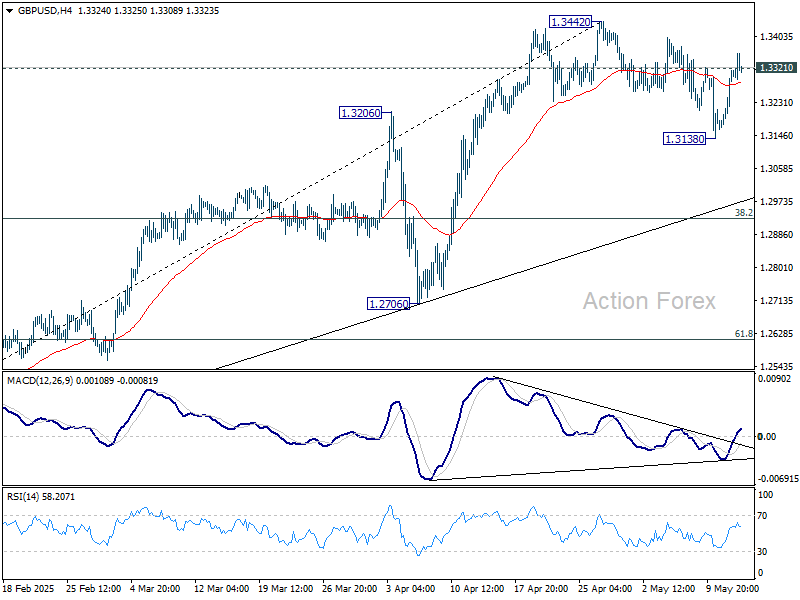

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3202; (P) 1.3259; (R1) 1.3363; More...

GBP/USD's correction from 1.3442 might have completed at 1.3138 already. Intraday bias is back on the upside. Decisive break of 1.3433/42 key resistance zone will confirm larger up trend resumption. Nevertheless, below 1.3138 will resume the correction. But downside should be contained by 38.2% retracement of 1.2099 to 1.3442 at 1.2929 to bring rebound.

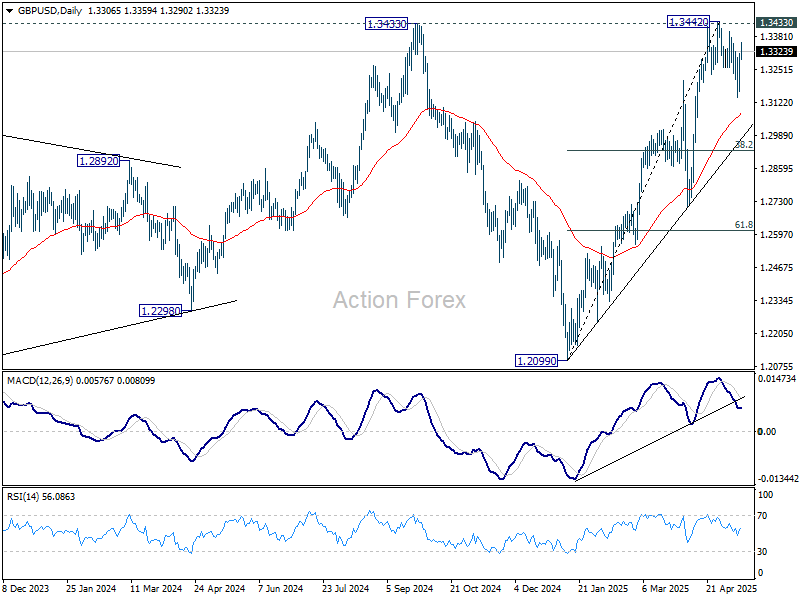

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could either be resuming the up trend, or the second leg of a consolidation pattern. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on decisive break of 1.3433 at a later stage.

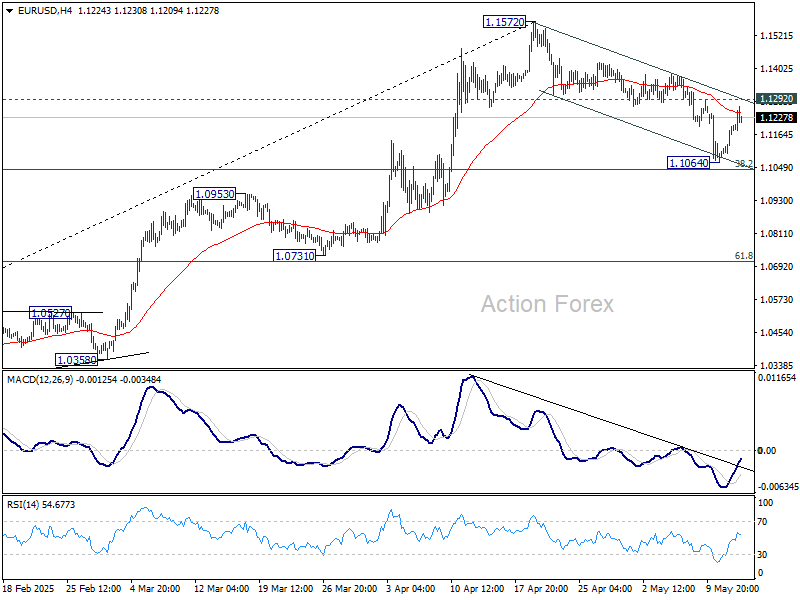

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1114; (P) 1.1155; (R1) 1.1225; More...

Intraday bias in EUR/USD stays neutral at this point. On the upside, break of 1.1292 resistance will argue that correction from 1.1572 has completed after defending 38.2% retracement of 1.0176 to 1.1572 at 1.1039. Intraday bias will be back on the upside for retesting 1.1572. However, sustained break of 1.1039 will dampen this view and target 61.8% retracement at 1.0709 next.

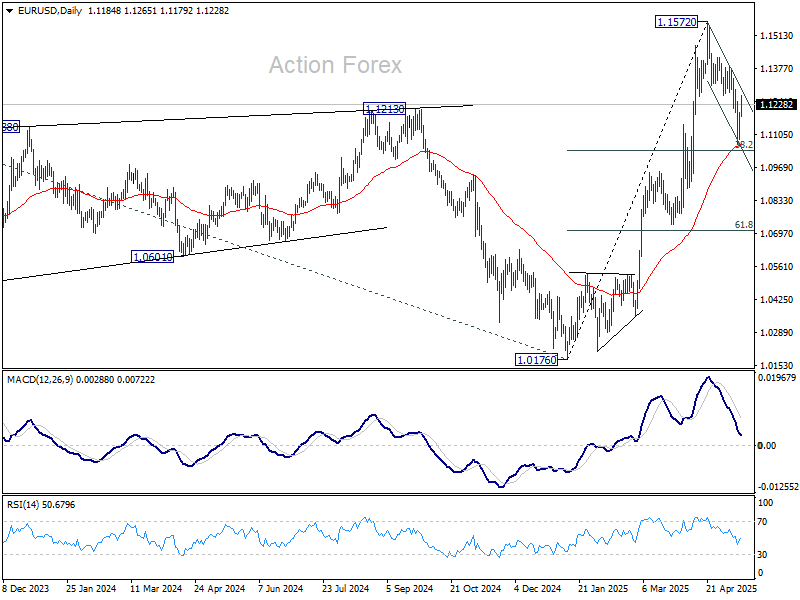

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0789) holds.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.06; (P) 147.79; (R1) 148.21; More...

Intraday bias in USD/JPY remains neutral for the moment. Further rally is expected as long as 142.43 support holds. As noted before, fall from 158.86 could have completed 139.87 already. Above 148.64 will target 61.8% retracement of 158.86 to 139.87 at 151.60 next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.