Sample Category Title

GBP/USD Edges Higher as EUR/GBP Loses Ground

GBP/USD is attempting a fresh increase above the 1.3270 resistance. EUR/GBP declined steadily below the 0.8460 and 0.8440 support levels.

Important Takeaways for GBP/USD and EUR/GBP Analysis Today

- The British Pound is attempting a fresh increase above 1.3250.

- There was a break above a key bearish trend line with resistance at 1.3270 on the hourly chart of GBP/USD at FXOpen.

- EUR/GBP is trading in a bearish zone below the 0.8460 pivot level.

- There was a break above a connecting bearish trend line with resistance near 0.8410 on the hourly chart at FXOpen.

GBP/USD Technical Analysis

On the hourly chart of GBP/USD at FXOpen, the pair declined after it failed to clear the 1.3440 resistance. As mentioned in the previous analysis, the British Pound traded below the 1.3200 support against the US Dollar.

Finally, the pair tested the 1.3140 zone and is currently attempting a fresh increase. The bulls were able to push the pair above the 50-hour simple moving average and 1.3215.

There was a break above a key bearish trend line with resistance at 1.3270. The pair surpassed the 50% Fib retracement level of the downward move from the 1.3402 swing high to the 1.3139 low. It is now showing positive signs above 1.3300.

On the upside, the GBP/USD chart indicates that the pair is facing resistance near 1.3340 and the 76.4% Fib retracement level of the downward move from the 1.3402 swing high to the 1.3139 low.

The next major resistance is near 1.3400. A close above the 1.3400 resistance zone could open the doors for a move toward 1.3440. Any more gains might send GBP/USD toward 1.3500.

On the downside, immediate support is near 1.3270. If there is a downside break below 1.3270, the pair could accelerate lower. The first major support is near the 1.3215 level and the 50-hour simple moving average.

The next key support is seen near 1.3140, below which the pair could test 1.3080. Any more losses could lead the pair toward the 1.3000 support.

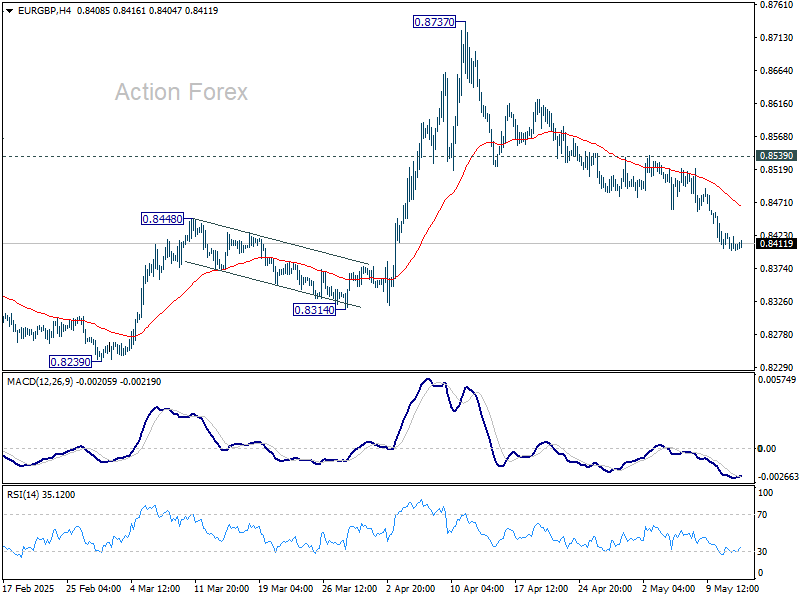

EUR/GBP Technical Analysis

On the hourly chart of EUR/GBP at FXOpen, the pair started a fresh decline from well above 0.8500. The Euro traded below the 0.8430 level and tested 0.8400. It is now consolidating losses and trading below the 50-hour simple moving average. However, there was a break above a connecting bearish trend line with resistance near 0.8410.

The pair is now facing resistance near the 23.6% Fib retracement level of the downward move from the 0.8522 swing high to the 0.8399 low at 0.8430.

The next major resistance could be 0.8460. It coincides with the 50% Fib retracement level of the downward move from the 0.8522 swing high to the 0.8399 low. The main resistance is near the 0.8495 zone. A close above the 0.8495 level might accelerate gains. In the stated case, the bulls may perhaps aim for a test of 0.8520. Any more gains might send the pair toward the 0.8550 level.

Immediate support sits near 0.8400. The next major support is near 0.8365. A downside break below the 0.8365 support might call for more downsides. In the stated case, the pair could drop toward the 0.8300 support level.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

BoE hawk Mann: Labor market resilient, and firms yet to lose pricing power

BoE MPC member Catherine Mann explained her notable policy shift during an interview with CNBC, revealing why she moved from backing a 50bps rate cut in February to voting for a hold at last week’s meeting.

Mann cited the UK labor market’s resilience as a key factor in her reassessment. While recent data suggest some moderation "a slowing labor market", she argued that "it is not a non-linear adjustment."

Mann also flagged a new risk emerging from tariffs. She warned that rising US tariffs on countries like China could lead to an influx of diverted exports into markets such as the UK. While this could temporarily ease goods prices at the border, she cautioned that domestic retailers may use the opportunity to rebuild profit margins, keeping upward pressure on consumer price inflation rather than alleviating it.

Crucially, Mann emphasized the need to see a broad-based "loss of pricing power" in firms. "I need to see that firms are starting to be much more moderate in setting their prices across a broad range of products," she added. "Goods price inflation is actually going up, not down."

Markets Ponder Scope (and Timing) of Additional ECB Rate Cuts

Markets

The market rebound after the weekend US-China trade truce was confronted the with yesterday’s US April inflation data. The potentially less negative impact of the trade war on the US (and global) economy also changed the market assessment on inflation. Especially the combination of resilient activity data and ongoing high inflation data would solidify Powell’s reactive wait-and-see bias. At 0.2% M/M and 2.3% Y/Y for headline CPI (from 2.4%) and 0.2% M/M and 2.8% Y/Y for core (unchanged from March), US inflation was marginally softer than expected. The details showed that some goods prices already tentatively rose as was the case for energy prices (electricity) but this was compensated for by lower food prices and some services prices. Shelter prices still rose 0.3% M/M. Overall the report didn’t bring any decisive guidance on the potential impact of the tariffs going forward. A modest dip in yields immediately after the release was very short-lived. President Trump again used the report to call Fed Chair Powell to cut interest rate immediately. However, markets understood that this report is no reason for the Fed Chair to leave the current approach anytime soon. At the end of the day US yields hardly changed (after the recent rebound) with the 2 and the 5-y down 1.0 bp and the 30-y unchanged. German Bunds still underperformed Treasuries with yields rising between 2.3 bps (2-y) and 4.5 bps (30-y) as markets ponder the scope (and timing) of additional ECB rate cuts in the wake of recent trade developments. A June rate cut is no longer 100% discounted. ECB’s Villeroy indicated that another rate cut is likely by summer. That of course gives some room of maneuver on the timing. In the meantime, US equities remained well supported (S&P 500 +72%). Modest inflation is a supportive. The Nasdaq even outperformed as Trump deals negotiated during his trip in the Middle East supported US tech stocks. The combination of moderate inflation and a continuation of the risk rally this time caused a correction on recent USD gains. DXY eased from 101.7 to close near the 101 big figure. EUR/USD rebounded from the 1.109 area to close near 1.1185. The recent rebound in sterling (against the euro) gradually eased despite in line unemployment date and still solid wage March wage growth (EUR/GBP close 0.841).

Today’s eco data calendar is extremely thin, except for some Fed (Waller, Jefferson) and ECB (Nagel, Holzmann) speakers. Yesterday’s price action at least suggests that the downside in US and probably even more in European yields is well protected. With respect to the latter we also look out to the announced meeting between Ukrainian President Zelensky and (maybe) Vladimir Putin that might take place in Turkey tomorrow. Expectations probably are low. Any positive outcome might further support some kind of European reflation trade. Of course, this remains highly conditional for now. Today we expect more technical consolidation on the risk rally. Even despite yesterday’s correction, we’re not sure that that the dollar rebound has already fully run its course. Some further comeback might still be on the cards.

News & Views

Australian wage growth accelerated from 0.7% Q/Q in Q4 2024 to 0.9% Q/Q in Q1 2025 (vs 0.8% expected), the fastest pace since Q4 2023. Jobs covered by enterprise agreements contributed to over half of all quarterly wage growth. The larger than usual March quarter contribution from enterprise agreement-covered jobs was mainly driven by the new state-based enterprise agreements in the public sector. Annual wage pay picked up from 3.2% to 3.4%. Details showed private sector annual wage growth unchanged at 3.3% while public sector salaries rose by 3.6% Y/Y (up from 2.9%). The Australian Bureau of Statistics publishes its monthly labour market report tomorrow.

Bulgarian parliament speaker Kiselova rejected President Radev’s request for a referendum on euro adaptation saying that it violated Bulgaria’s constitution as well as a range of EU treaties. The politically loaded push came as the country waits the June 4 publication of convergence reports by the EC and the ECB and against the background of a divided political and societal landscape. Interior minister Mitov yesterday labelled the referendum request as “a clear act of sabotage against the introduction of the euro in Bulgaria”.

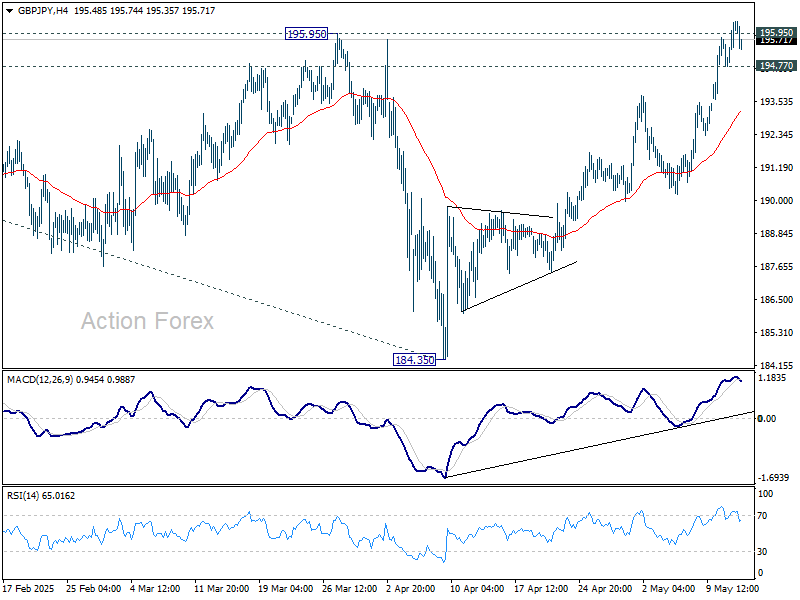

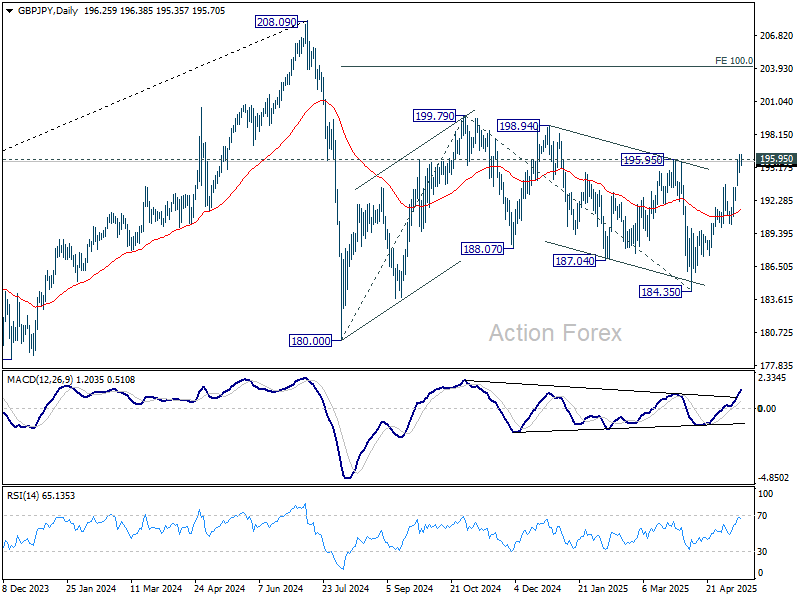

GBP/JPY Daily Outlook

Daily Pivots: (S1) 195.20; (P) 195.79; (R1) 196.81; More...

Intraday bias in GBP/JPY stays on the upside at this point. Decisive break of 195.95 resistance will suggest that whole choppy decline from 199.79 has completed, and target this resistance next. On the downside, below 194.77 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

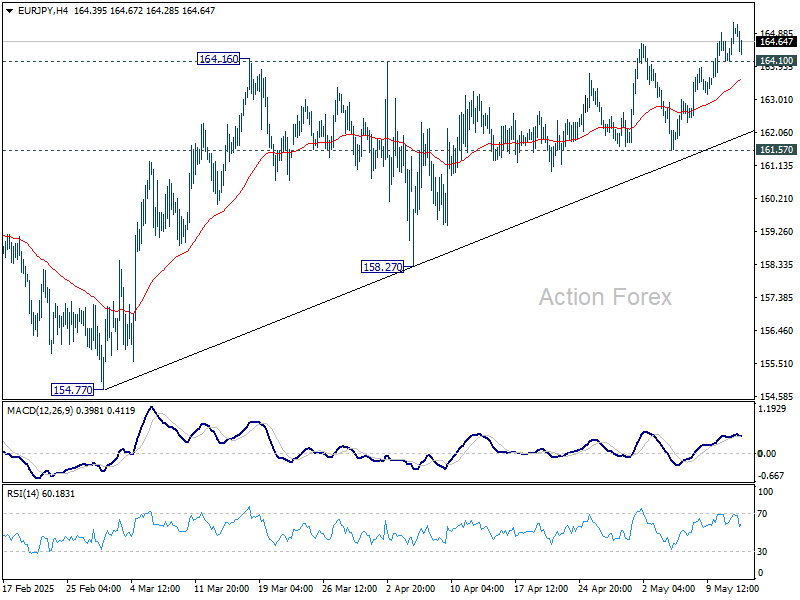

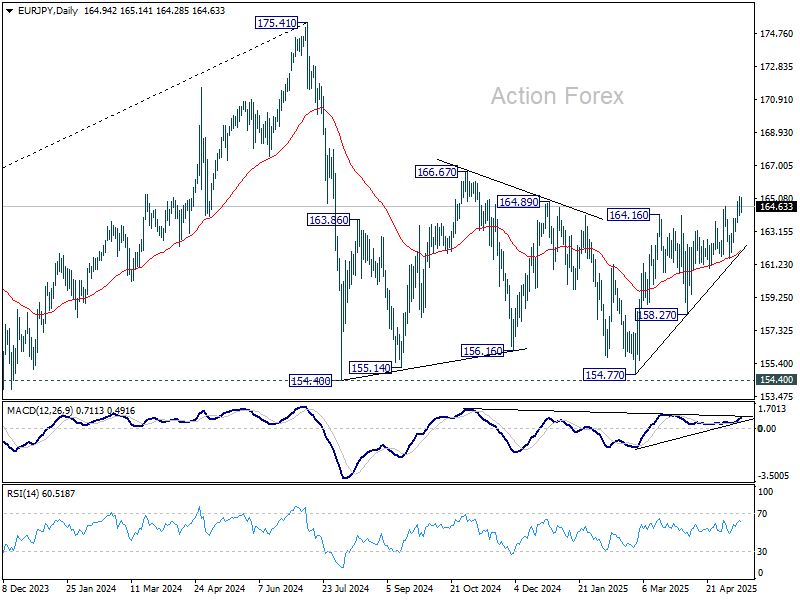

EUR/JPY Daily Outlook

Daily Pivots: (S1) 164.32; (P) 164.77; (R1) 165.41; More...

Intraday bias in EUR/JPY stays mildly on the upside at this point. Current rise from 154.77 should extend to 166.67 resistance. On the downside, below 164.10 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 161.57 support holds, in case of retreat.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

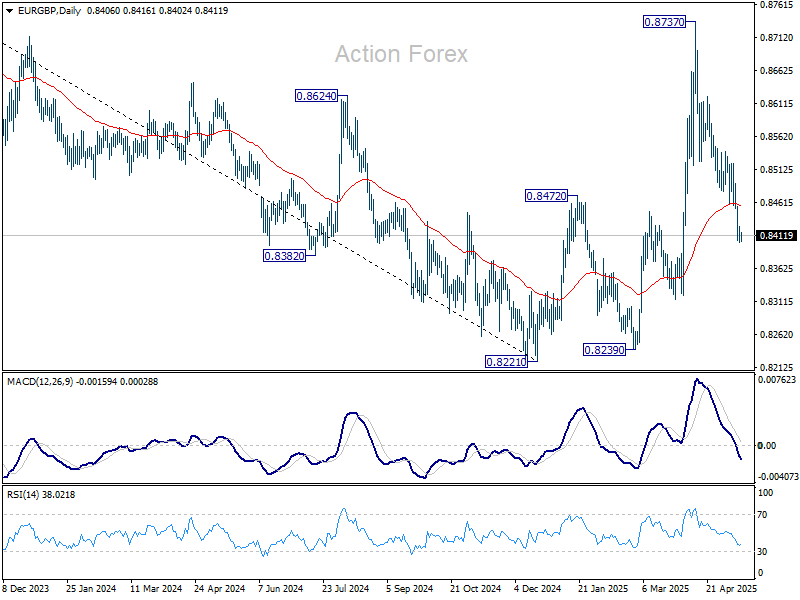

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8398; (P) 0.8413; (R1) 0.8422; More...

EUR/GBP's fall from 0.8737 is in progress and intraday bias stays on the downside. Current development suggests that whole rebound from 0.8221 has completed as a corrective move. Further decline should be seen back to 0.8221/8239 support zone. For now, risk will stay on the downside as long as 0.8539 resistance holds, in case of recovery.

In the bigger picture, the extended decline from 0.8737 dampened the original bullish view. While a medium term bottom was in place at 0.8221, price actions from there could be a corrective pattern only. Larger down trend from 0.9267 (2022 high) might still be in progress. Sustained trading below 55 W EMA (now at 0.8438) will turn favor to this bearish case.

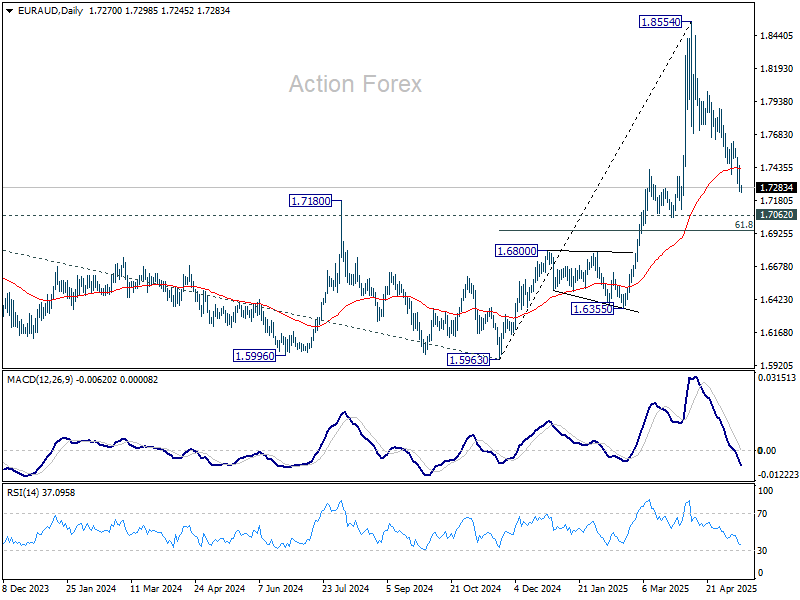

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7209; (P) 1.7331; (R1) 1.7409; More...

Intraday bias in EUR/AUD remains on the downside, as fall from 1.8554 is in progress. Next target is 61.8% retracement of 1.5963 to 1.8554 at 1.6953. On the upside, break of 1.7628 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, as long as 1.7062 resistance turned support (2023 high) holds, up trend from up trend from 1.4281 (2022 low) should still be in progress. However, sustained break of 1.7062 will confirm medium term topping and bring deeper fall back to 1.5963 support.

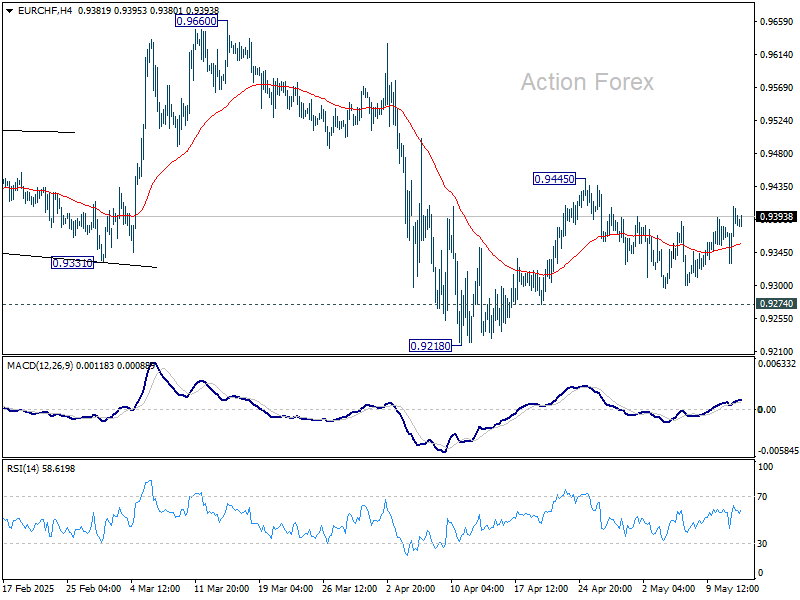

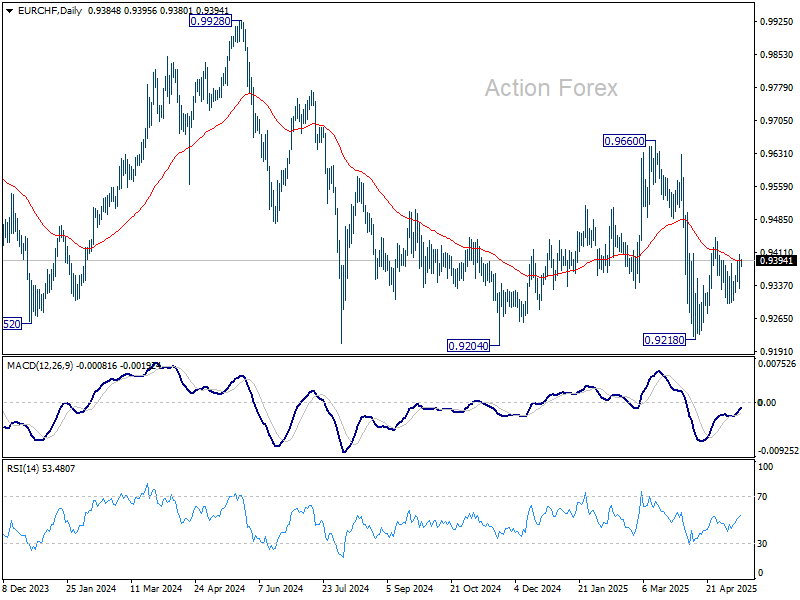

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9345; (P) 0.9377; (R1) 0.9422; More....

Sideway trading continues in EUR/CHF and intraday bias stays neutral. On the upside, above 0.9445 will resume the rebound from 0.9218, either as a corrective move or the third leg of the pattern from 0.9204. However, break of 0.9274 will suggest that that recovery has completed, and bring retest of 0.9204/18 support zone.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9548) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

Trade Winds Shift in Favour of US Indices

Trade news keeps getting better. Yesterday, it was the chipmakers’ turn to lead the rally, as Saudi Crown Prince Mohammad bin Salman pledged to spend as much as $1 trillion in commercial deals with the US, while Jensen Huang announced in Riyadh that the company will be selling chips to the Saudi Arabian AI company Humain for a massive data center project.

Now, remember: the US had been restricting chip sales to Saudi Arabia and the United Arab Emirates for national security reasons. So, this news came as a major relief for US chip companies, especially at a time when concerns about slowing demand from Big Tech have been mounting. Budgets from companies like Google and Meta are hard to match and even harder to replace — so the prospect of fresh orders from Saudi Arabia (and potentially the UAE) is excellent news for US chipmakers.

The market reaction was immediate. Nvidia jumped at the open, pushing above its 200-day moving average and gaining more than 5.5%. The stock is now up nearly 50% since the April dip. AMD extended gains above its 100-day moving average, breaking out of a six-month descending channel and topping the minor 23.6% Fibonacci retracement of last year’s decline.

Broadly speaking, AI demand remains strong, as more industries look to integrate AI into their operations. But recent trade uncertainty had forced some investment plans to pause — a dynamic that could have led to a temporary slowdown in AI-related activity. So the idea that Middle Eastern demand could offset that trend is excellent news on its own and should offer solid support for US chip stocks.

On the macro side, investors also digested the latest US inflation report — which showed prices rising last month, but less than expected on a monthly basis. On a yearly basis, the headline rate eased to 2.3% — the lowest since spring 2021 — marking the third straight month of a softer-than-expected print.

That’s good news for the Federal Reserve (Fed), but the reaction was muted. As the chief economist at Fitch warned, ‘core goods prices have yet to reflect the impact of the tariff hikes that have taken place since February,’ suggesting that many retailers are still selling from pre-tariff inventories. The added costs of new imports may only show up in data in the coming months.

As a result, expectations around the Fed didn’t shift much. The US 2-year yield hovered around the 4% mark, and markets continue to price in two rate cuts this year — with the first not expected before the September meeting.

Interestingly, even as easing trade tensions helped boost equity markets, the US dollar lagged. The dollar index gave back gains despite improving trade sentiment, while both the S&P 500 and Nasdaq extended their rebounds. The S&P 500 has now erased its year-to-date losses and is within 4% of its all-time high, while the Nasdaq has rallied more than 4,600 points since the April dip and sits just 1,000 points shy of its own record — reached in February. The rally is prompting analysts to improve their outlooks for US indices. Note that, the Dow Jones lagged due to an 18% slump in UnitedHealth Group after its CEO stepped down — a move that’s not reflective of the broader index.

Overall, US equity gains are accelerating on improved trade sentiment and a significantly better-than-expected earnings season. So far, S&P 500 companies have posted Q1 earnings growth of 13.1%, compared to just 6.6% expected before the season began. Gloomy earnings forecasts are being overlooked as better trade prospects and upside surprises continue to dominate investor focus. Citigroup’s earnings revision index even turned positive for the first time this year — another boost for sentiment despite hawkish Fed signals and rising yields.

Meanwhile, across the Atlantic, European indices are struggling to keep up — narrowing the performance gap between US and European markets.

April’s surprise jump in eurozone inflation has weakened the hands of European Central Bank (ECB) doves in recent weeks. At the same time, stalled trade negotiations with the US are weighing on sentiment — even more so as European leaders watch the US strike deals elsewhere. Scott Bessent warned this week that negotiations with the EU will likely take time, as European countries must agree internally before engaging with the US. The perception is that Europe is slipping back into its usual pattern: too cautious, too slow — and potentially risking the gains seen in the first four months of the year.

The EURUSD rebounded after touching its 50-day moving average, but sentiment on the euro has been downgraded from positive to neutral. A softer euro combined with rebounding energy prices could further soften expectations for ECB easing and keep a lid on European equity gains.

In the UK, some analysts reacted sharply to rising unemployment and softening wage growth, arguing that the Bank of England (BoE) is asleep at the wheel. Critics say the BoE should have acted more pre-emptively, especially in light of the tax hikes announced last October and ongoing trade tensions. Whether the BoE responds remains to be seen, but the softer data gave doves a boost — and helped sterling rebound past the 1.33 mark against a broadly weaker US dollar.

The euro, meanwhile, gave back all of its gains against the pound since early April, as hopes rise for new UK trade deals with big partners like India and the US — in contrast to the EU, where no new deals have yet been announced.

Final Inflation Figures in the Spotlight

In focus today

In Germany, we await the final April inflation data, which includes all the sub-categories of the CPI index. These will be particularly interesting as core services inflation rose much more than expected in April and will allow us to see if it was mainly due to the timing of Easter or a reflection of a broader pic- up in services momentum. We expect it was mainly due to Easter and the price pressures should remain well-behaved as wage growth is declining.

In Sweden, we receive important economic data, starting with inflation figures. Core inflation came in a tenth lower than expected according to the preliminary figures last week. Today's details provide important clues about how widespread price pressure is, which is important considering high price plans and high inflation expectations. Next is the Riksbank's minutes, where we get a better picture of the discussions when the Riksbank made a small opening towards easier monetary policy last week. The market is pricing 50/50 for a June cut, which means the minutes are unusually interesting. According to our assessment, neither the press release nor Thedéen, Governor of the Riksbank, sent any signals that align with a cut in June. Today, we will see how the rest of the board reasons.

Fed's Waller and Daly are also set to speak during the day.

Economic and market news

What happened overnight

In Japan, wholesale inflation for April came in at 0.2% m/m and 4.0% y/y, as widely expected. Firms continue to raise prices for food and beverages as well as agricultural goods. The figures present a mixed picture for the Bank of Japan, which faces ongoing domestic price pressures while reporting minimal impact seen from the US 'Liberation Day' tariffs, aided by a 90-day pause, as many firms still need to finalise a pricing strategy.

In the trade war, the UK-US trade deal has been criticised by China for potentially excluding Chinese products from British supply chains. The agreement, which includes security requirements for steel and pharmaceuticals, complicates London's efforts to rebuild relations with Beijing, as reported by the Financial Times. China's foreign ministry has emphasised that international cooperation should not harm third-party interests.

What happened yesterday

In the US, April CPI data surprised modestly to the downside, with headline inflation at 0.22 m/m SA (prior: -0.1%) and core terms at 0.24% m/m SA (prior: 0.1%). There was little evidence of tariff-driven price pressures, with slow core goods inflation and a slight decline in food prices. Energy and shelter inflation exceeded expectations, while core services inflation, excluding shelter and healthcare, stayed negative, indicating subdued price pressures despite the trade war. This environment supports the Fed's wait-and-see stance, and EUR/USD reversed course modestly higher. Read more in Global Inflation Watch - Realized price pressures remained under control in April, 13 May.

Ahead of the CPI release, the April NFIB small business optimism survey continued to show weakening sentiment. Firms' real sales growth expectations declined, and capex plans fell to the lowest level since April 2020. The price plans index, often a reliable CPI leading indicator, fell modestly to 28 from 30, nearing pre-Covid levels. Overall hiring plans remained weak. While this soft data paints a gloomy picture, it is somewhat outdated due to recent tariff changes.

In the UK, March labour market data came in a mixed bag, resulting in a muted market reaction. The unemployment rate increased as expected to 4.5% from 4.4%, while regular wage growth slightly underperformed expectations at 5.6% 3m y/y. Notably, private sector wage growth also fell short of expectations at 5.6%, which is also below the Bank of England's forecast. We will closely monitor the April labour market data where a large amount of the wage negotiations take place and next week's, with focus on service inflation.

In Germany, the ZEW showed a continued weak assessment of the current economic situation and a partial rebound in the future expectations index. Following a large decline in expectations to -14 in April, expectations partially rebounded to 25 in May, influenced by less negative US trade signals. The rebound may strengthen further due to the recent US-China trade agreement, as some responses might not fully reflect the deal, given the submission deadline. The assessment of the current situation was broadly stable, slightly declining to -82. Despite this, the data indicates a modest improvement in German activity compared to the past six months, though a clear rebound is not evident. This aligns with recent production and PMI data, pointing to subdued growth in the German economy.

In geopolitics, President Trump announced the lifting of US sanctions on Syria, following encouragement from allies in the Middle East. The policy shift aims to support the new Syrian government and facilitate its economic recovery, aligning with broader efforts to strengthen diplomatic and economic ties in the Middle East. As part of his four-day Gulf tour Trump, is set to visit Syria's new leader, Sharaa, today.

We will also continue to keep an eye out for the tentative Russia-Ukraine talks in Istanbul scheduled for tomorrow. Reuters sources suggested yesterday that from the US side at least Secretary of State Marco Rubio as well as special envoys Steve Witkoff and Keith Kellogg would join the talks. Ukraine has communicated that Zelenskiy would only attend if Putin is also present, which the Russian side has not yet confirmed.

Equities: Yesterday saw a continuation of Monday's big rally. US outperformed Europe, with S&P 500 up 0.7% and Nasdaq 1.4% compared to a modest 0.1% rise for Stoxx 600. S&P 500 is now less than 4% off its all-time high. Risk-on evident in both regions though, with investors showing a big preference for cyclical stocks vs defensives. US tech and overall retail was in favour, in particular helped by positive AI headlines and cooler inflation. Mostly buoyant mood in Asia as well, with Chinese equities outperforming on solid earnings reports.

FI&FX: Despite risk-appetite remaining solid during yesterday's session we saw the USD trade on the back-foot while AUD and NZD continued Monday's rally. In the Scandies neither EUR/NOK nor EUR/SEK did much. In rates space yields edged marginally higher across currencies - but overnight we have seen Majors FI catch a slight bid. BTP-Bund spreads continue to tighten while treasuries have given up slight performance vs the swap.