Sample Category Title

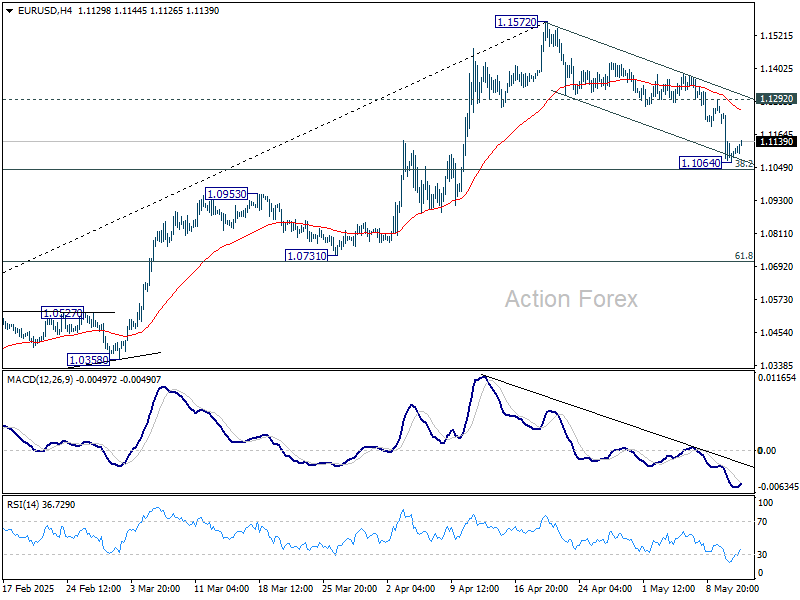

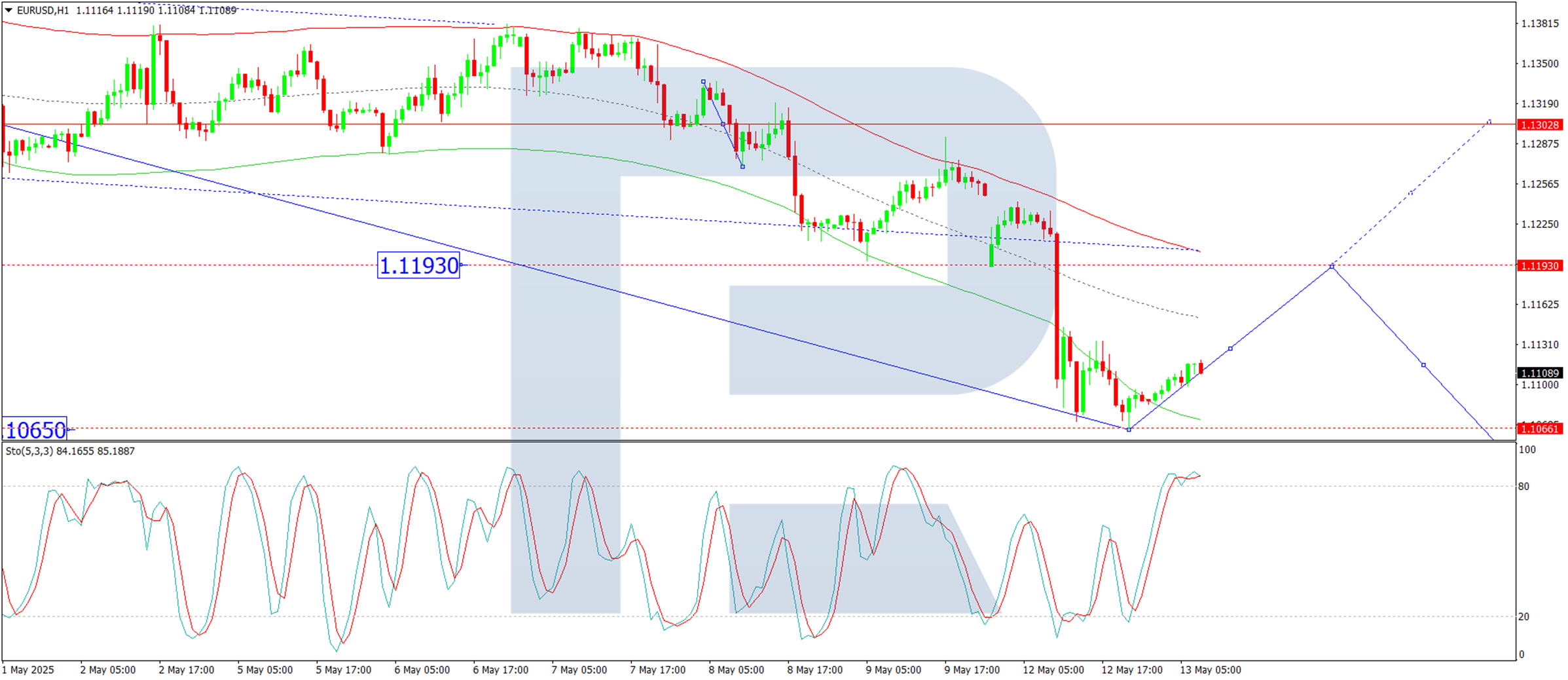

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1022; (P) 1.1132; (R1) 1.1199; More...

Intraday bias in EUR/USD is turned neutral first with current recovery. Overall, strong support should be seen from 38.2% retracement of 1.0176 to 1.1572 at 1.1039 to bring rebound. On the upside, break of 1.1380 will suggest that the correction from 1.1572 has completed, and bring retest of 1.1572. However, sustained break of 1.1039 will dampen this view and target 61.8% retracement at 1.0709 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0789) holds.

Dollar Eases as Trade Boost Fades, Sterling Finds Support on Wages and BoE Rhetoric

Dollar softened slightly in early US trading today, though the move appears more related to a fading post-trade-deal rally than any direct reaction to economic data. While April’s inflation report showed encouraging progress on headline disinflation, the core CPI reading held firm, suggesting underlying price pressures remain sticky. That dynamic should keep Fed cautious, and today's market reaction suggests the data did little to shift expectations meaningfully. The more optimistic takeaway, however, is that recent tariffs have yet to significantly lift inflation.

In contrast, Sterling is gaining some traction, particularly against Euro, following solid UK wage data. Despite signs of softening in overall employment, wage growth remains robust, with average earnings still running well above levels consistent with BoE's 2% inflation target. BoE Chief Economist Huw Pill reinforced that concern by warning that more aggressive or sustained policy action may be needed to bring inflation under control. His remarks have helped underpin Sterling sentiment.

Overall in the currency markets, Aussie has overtaken Dollar to become the week's top performer. Kiwi and Loonie are also firm. At the other end of the spectrum, Yen continues to struggle, while Swiss Franc and Euro are also soft.

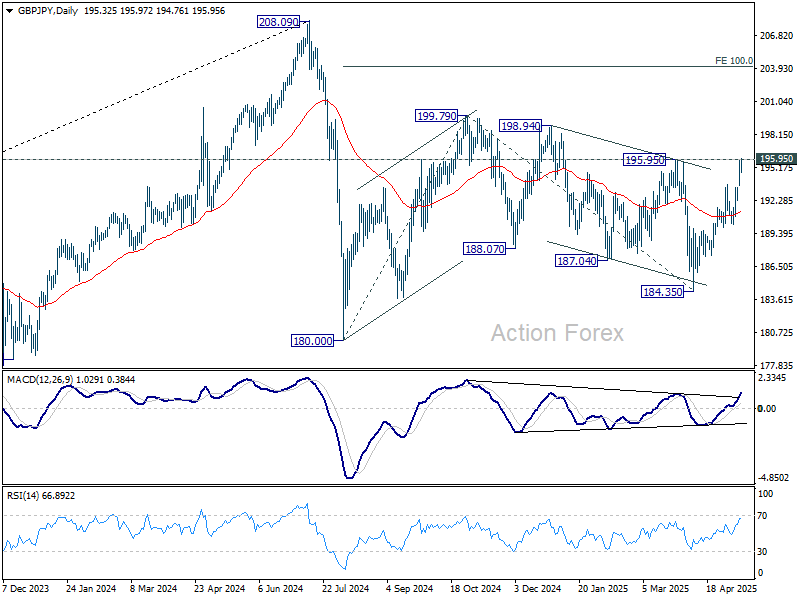

Technically, GBP/JPY is now pressing 195.95 resistance as rise from 184.35 extends. Decisive break of 195.95 will argue that choppy fall from 199.79 has completed at 184.35 already. More importantly, rise from 180.00 might then be ready to resume through 199.79 in this bullish case.

In Europe, at the time of writing, FTSE is up 0.05%. DAX is up 0.17%. CAC is up 0.23%. UK 10-year yield is up 0.021 at 4.671. Germany 10-year yield is up 0.013 at 2.666. Earlier in Asia, Nikkei rose 1.43%. Hong Kong HSI fell -1.87%. China Shanghai SSE rose 0.17%. Singapore Strait Times rose 0.13%. Japan 10-year JGB yield rose 0.06 to 1.449.

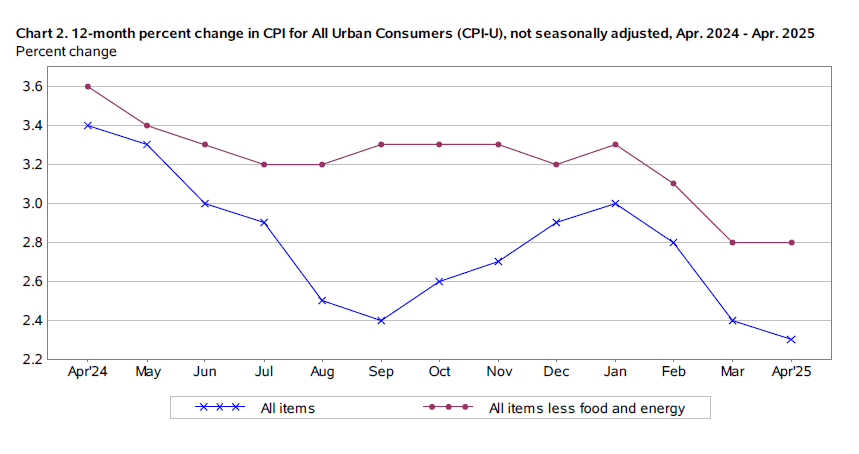

US CPI hits four year low at 2.3%, but core inflation holds steady at 2.8%

US headline CPI rose just 0.2% mom, below the expected 0.3% mom. Core CPI, excluding food and energy, also increased by 0.2%, undershooting forecasts of 0.3% mom.

On an annual basis, headline inflation eased to 2.3% yoy from 2.4% yoy, the lowest rate since April 2021. Core inflation held steady at 2.8% yoy, in line with expectations.

Shelter remained the key driver of monthly inflation, rising 0.3% mom and accounting for over half of the total increase.

Energy prices also ticked higher by 0.7% mom, while food prices declined slightly by -0.1% mom. On a year-over-year basis, energy costs dropped by -3.7%, helping to keep overall inflation in check, while food prices rose 2.8%.

BoE’s Pill: May require more aggressive and persistent effort to bring down inflation

Speaking at a press conference today, BoE Chief Economist Huw Pill warned that returning inflation to the BoE’s 2% target may prove more difficult than anticipated. Hence, Pill said the central bank may need to respond in a “somewhat more aggressive or more persistent” way to ensure inflation is brought under control within a reasonable time frame.

He raised concerns that recent shifts in wage and price-setting behavior might reflect a more "structural change", drawing parallels with inflation dynamics of the 1970s and 1980s.

Pill emphasized that investors should not interpret BoE's latest forecast, showing inflation returning to target by early 2027 based on market-implied rates, as a clear endorsement of future rate cuts.

Instead, he pointed to the Bank’s more inflationary risk scenario, which assumed persistently weak productivity and stronger wage pressures. These conditions, he said, echo past inflation crises, where elevated price levels triggered repeated and entrenched pay demands.

Last week, Pill voted against the BoE's quarter-point rate cut, aligning with fellow hawk Catherine Mann in preferring to keep rates unchanged.

UK payrolled employment falls -33k, wage growth remains elevated

UK labor market data for April showed signs of softening in employment but continued strength in wage growth. Payrolled employment fell by -33k (-0.1% mom), while the claimant count rose by 5.2k. Median monthly pay rose by 6.4% yoy in April, accelerating from 5.9% yoy in the previous month.

In the three months to March, unemployment rate in the three months to March edged up from 4.4% to 4.5%, in line with expectations and marking the highest level since late 2021.

Average earnings including bonuses rose 5.5% yoy, beating expectations of 5.2% yoy. Earnings excluding bonuses rose 5.6% yoy, slightly below forecast of 5.7% yoy.

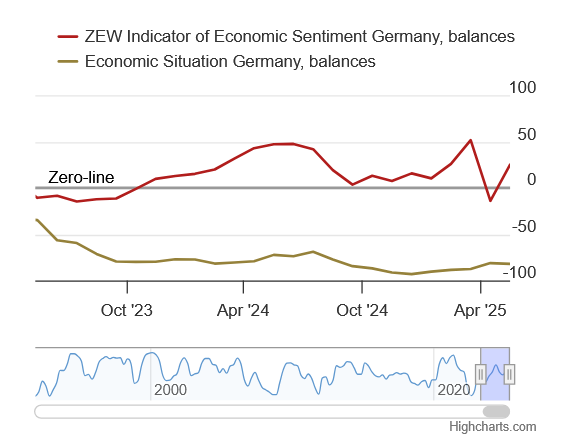

German ZEW economic sentiment surges on stabilizing domestic politics and trade progress

Investor sentiment in Germany and the wider Eurozone improved sharply in May, with ZEW Economic Sentiment Index for Germany jumping from -14.0 to 25.2, well above the expected 9.8. Eurozone sentiment followed suit, rising from -18.5 to 11.6, also beating expectations.

According to ZEW President Achim Wambach, the rebound reflects growing optimism tied to easing trade tensions, a new German government, and stabilizing inflation, helping to offset last month’s sharp deterioration.

However, views on current conditions remain deeply negative. Germany’s Current Situation Index edged down further from -81.2 to -82.0, missing forecasts. Eurozone’s improved modestly but still stood at -42.2. This divergence suggests that while expectations for the months ahead are improving, near-term economic conditions remain fragile, particularly in Germany.

BoJ’s Uchida sees temporary inflation pause, but wage growth to persist

BoJ Deputy Governor Shinichi Uchida said today that while Japan’s underlying inflation and medium- to long-term inflation expectations may "temporarily stagnate", wage growth is expected to remain firm as "Japan's job market is very tight."

He added that companies are likely to continue "passing on rising labour and transportation costs by increasing prices".

Uchida also stressed that BoJ will assess the economic impact of US trade policy “without pre-conception,” acknowledging the high degree of uncertainty surrounding the global outlook.

BoJ opinions: Sees tariff risks but maintains flexible rate-hike stance

BoJ’s Summary of Opinions from its April 30–May 1 meeting revealed a generally cautious view on the impact of US tariffs, with board members acknowledging the potential economic damage but not seeing it as enough to derail the pursuit of the 2% inflation target.

One member noted that BoJ may enter a "temporary pause" in rate hikes due to weaker US growth. But it's emphasized that "it shouldn't be too pessimistic".

The member emphasized that rate hikes could resume if conditions improve or US policy shifts.

Other opinions highlighted the high level of uncertainty facing Japan’s economic and price outlook, driven largely by global trade tensions. One board member noted the policy path “may change at any time.”

Another reaffirmed that there has been "no change to the BoJ's rate-hike stance", as projections continue to show inflation reaching the 2% target and real interest rates remain deeply negative.

Australian Westpac consumer sentiment rises to 92.1, weak confidence supports RBA cut

Australia’s Westpac Consumer Sentiment Index rose 2.2% to 92.1 in May, partially recovering from April’s sharp decline triggered by trade-related uncertainty.

Westpac attributed the modest rebound to stronger financial markets and a decisive outcome in the Federal election. However, sentiment remains subdued, with the index still 3.9% below its March level and firmly in pessimistic territory.

With all key inflation measures now back within the 2–3% target range, Westpac expects RBA to cut the cash rate by another 25bps to 3.85%. The combination of soft domestic sentiment and a more "unsettled and threatening global backdrop" strengthens the case for further easing.

Australia’s NAB business conditions weaken to 2, profit pressures mount

Australia’s NAB Business Confidence Index edged up from -3 to -1 in April. However, the underlying Business Conditions Index slipped from 3 to 2. Trading conditions eased from 6 to 5, while profitability dropped sharply from 0 to -4, highlighting the ongoing strain on margins.

Purchase cost growth accelerated to 1.7% in quarterly equivalent terms, up from 1.4%. Labor cost growth remained elevated at 1.6%. Rising input costs appear to be eroding profitability, with businesses struggling to pass through the full extent of these increases. This was reflected in modest increases in final product and retail price growth, which rose to 0.8% and 1.4% respectively—still below the pace of input cost growth.

NAB Chief Economist Sally Auld noted that weaker profitability was at the core of the drop in business conditions, aligning with the uptick in purchase costs and softer trading performance.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1022; (P) 1.1132; (R1) 1.1199; More...

Intraday bias in EUR/USD is turned neutral first with current recovery. Overall, strong support should be seen from 38.2% retracement of 1.0176 to 1.1572 at 1.1039 to bring rebound. On the upside, break of 1.1380 will suggest that the correction from 1.1572 has completed, and bring retest of 1.1572. However, sustained break of 1.1039 will dampen this view and target 61.8% retracement at 1.0709 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0789) holds.

US CPI hits four year low at 2.3%, but core inflation holds steady at 2.8%

US headline CPI rose just 0.2% mom, below the expected 0.3% mom. Core CPI, excluding food and energy, also increased by 0.2%, undershooting forecasts of 0.3% mom.

On an annual basis, headline inflation eased to 2.3% yoy from 2.4% yoy, the lowest rate since April 2021. Core inflation held steady at 2.8% yoy, in line with expectations.

Shelter remained the key driver of monthly inflation, rising 0.3% mom and accounting for over half of the total increase.

Energy prices also ticked higher by 0.7% mom, while food prices declined slightly by -0.1% mom. On a year-over-year basis, energy costs dropped by -3.7%, helping to keep overall inflation in check, while food prices rose 2.8%.

US Dollar Roars Back in a Blaze of Glory as Market Shrugs Off Recession Fears

EUR/USD dropped to 1.1110 on Tuesday, with the US dollar surging by over 1% in the previous trading session. The rally was driven by market reactions to news of a provisional agreement between China and the US to reduce tariffs, which helped alleviate global recession fears.

Key factors driving EUR/USD movement

Washington and Beijing have agreed to cut tariffs to 30% and 10%, respectively, for 90 days.

Meanwhile, US Treasury Secretary Scott Bessent confirmed plans to meet with Chinese representatives again in the coming weeks to begin negotiations on a broader trade deal.

The tariff reductions boosted market sentiment towards the dollar, which had previously faced pressure over concerns that President Donald Trump’s trade policies were diminishing the appeal of US assets. However, market nervousness is likely to persist until the White House establishes stable trade terms with all key partners.

Attention now turns to the latest US inflation report, which may show how the new tariff policy affects prices.

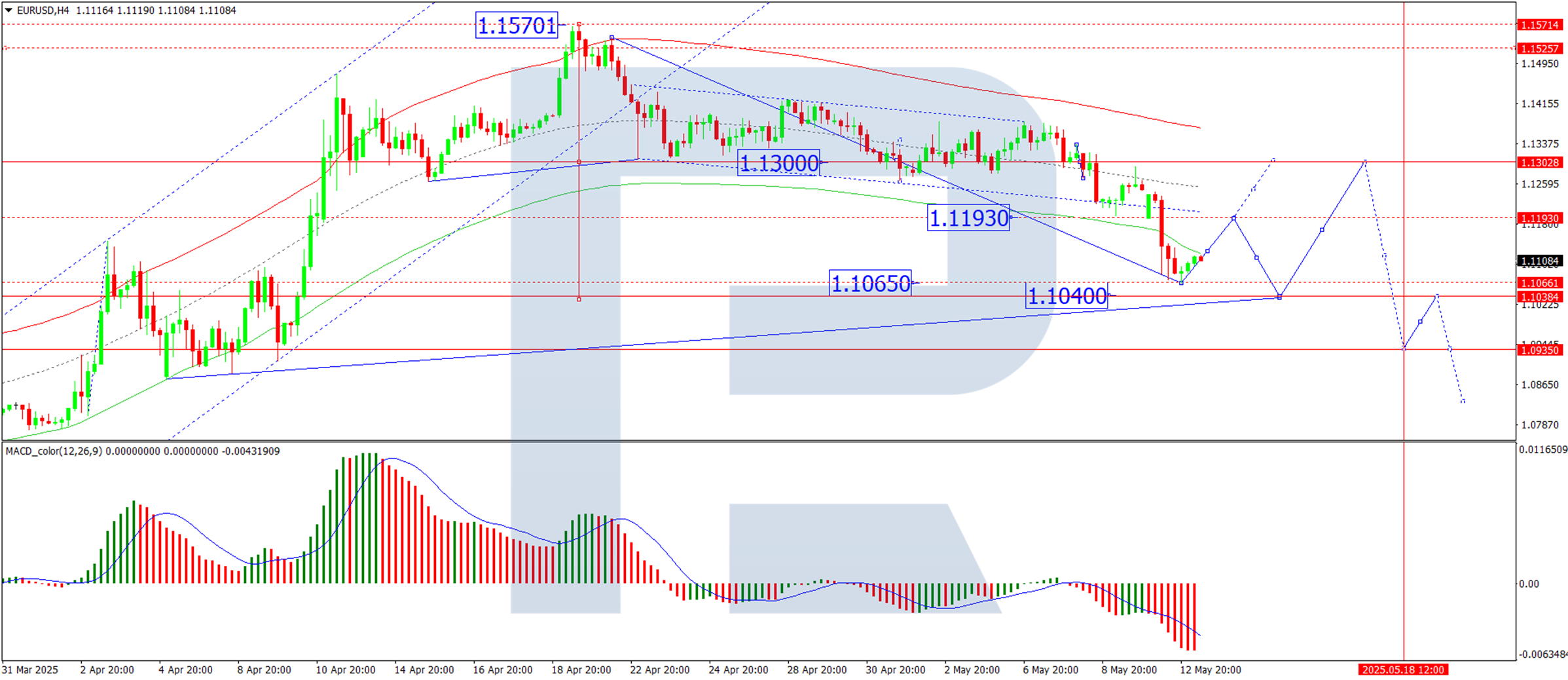

Technical analysis: EUR/USD

On the H4 chart, EUR/USD broke below 1.1190, completing the third wave of decline towards 1.1065. Today, we anticipate a corrective wave retesting 1.1190 (from below). Once this correction concludes, a new downward wave towards 1.1040 is expected. This scenario is technically confirmed by the MACD indicator, with its signal line below zero and pointing decisively downward.

On the H1 chart, the market has achieved the local downside target at 1.1065. Today, a potential rebound to 1.1126 is in focus. If this level is breached upwards, a further correction towards 1.1190 may follow. Subsequently, the downward trend could resume, targeting 1.1040. This outlook is supported by the Stochastic oscillator, whose signal line is above 80 but poised to decline towards 20.

Conclusion

The US dollar’s resurgence reflects improved risk sentiment following the US-China tariff truce, though uncertainty lingers over long-term trade relations. Technically, EUR/USD remains under pressure, with further downside likely after a brief correction.

BoE’s Pill: May require more aggressive and persistent effort to bring down inflation

Speaking at a press conference today, BoE Chief Economist Huw Pill warned that returning inflation to the 2% target may prove more difficult than anticipated. Hence, Pill said the central bank may need to respond in a “somewhat more aggressive or more persistent” way to ensure inflation is brought under control within a reasonable time frame.

He raised concerns that recent shifts in wage and price-setting behavior might reflect a more "structural change", drawing parallels with inflation dynamics of the 1970s and 1980s.

Pill emphasized that investors should not interpret BoE's latest forecast, showing inflation returning to target by early 2027 based on market-implied rates, as a clear endorsement of future rate cuts.

Instead, he pointed to the Bank’s more inflationary risk scenario, which assumed persistently weak productivity and stronger wage pressures. These conditions, he said, echo past inflation crises, where elevated price levels triggered repeated and entrenched pay demands.

Last week, Pill voted against the BoE's quarter-point rate cut, aligning with fellow hawk Catherine Mann in preferring to keep rates unchanged.

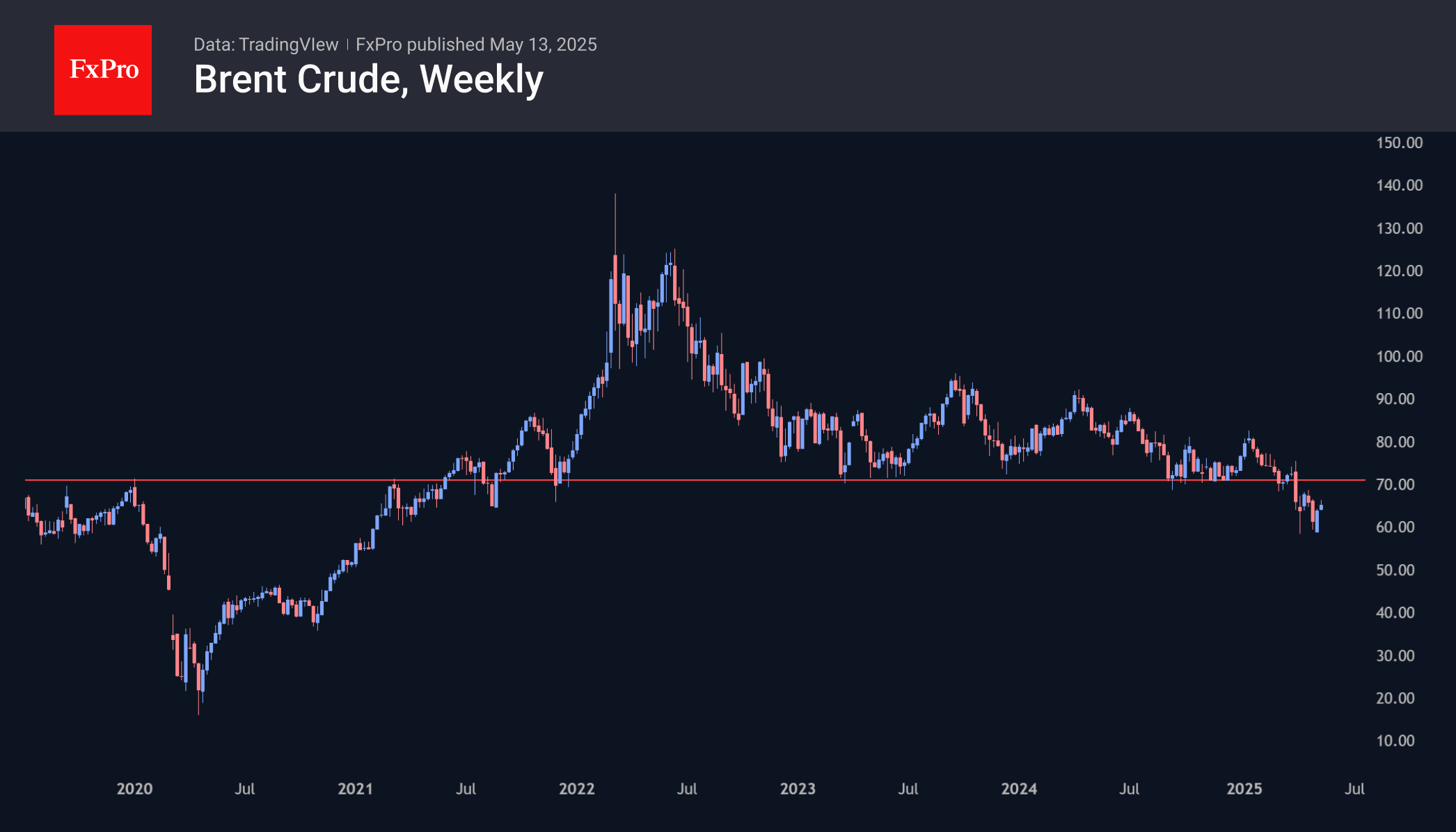

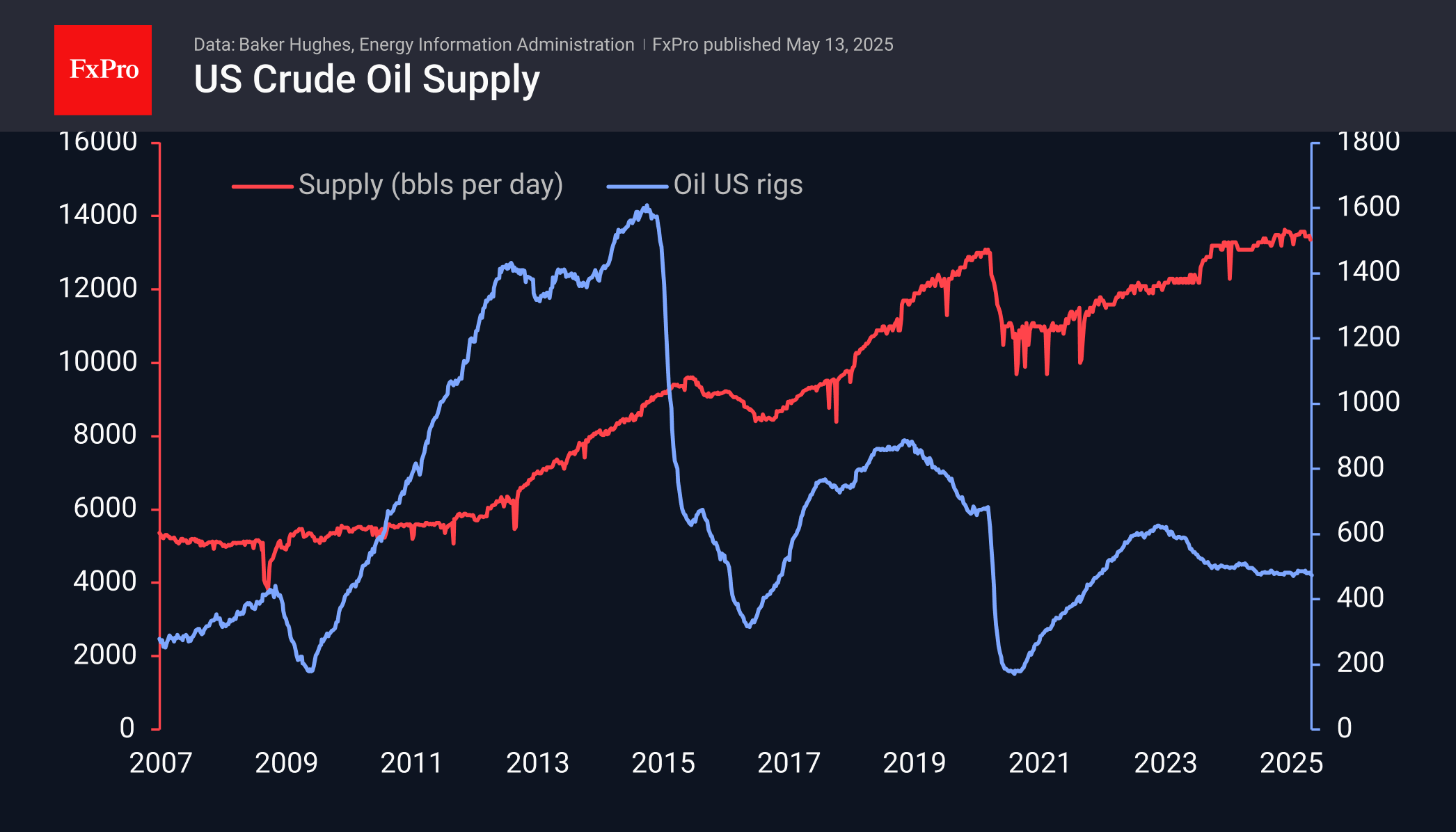

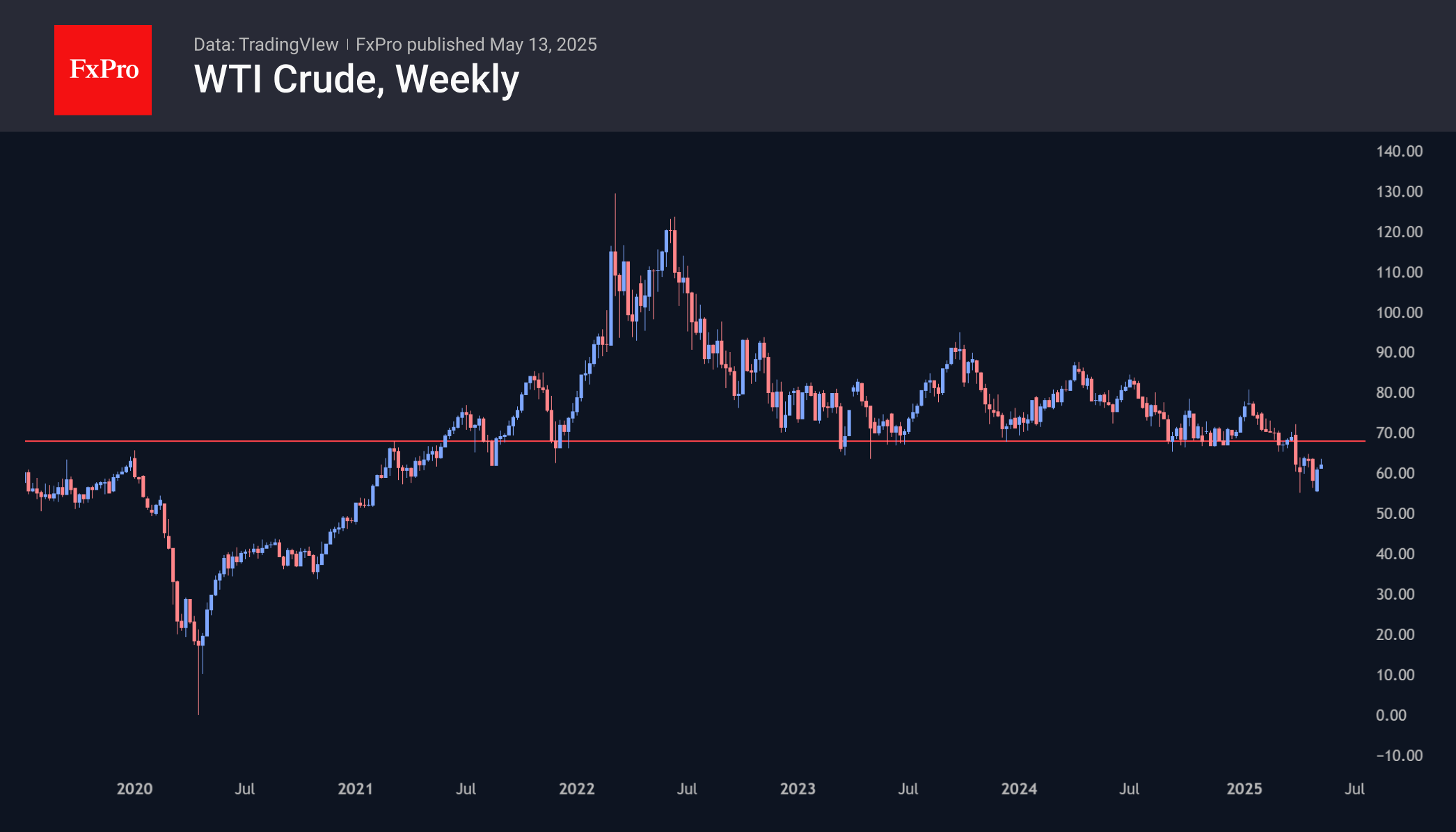

Oil Gains on Production Lull, Trade Optimism

Oil prices have been rising since the start of last week, up more than 12%. The growth comes on the back of positive news on China-US tariff negotiations. The decrease in geopolitical tensions in Russia-Ukraine and India-Pakistan relations in recent days has not had a significant impact on quotations. This may be due to a lack of confidence in progress in these areas or the concentration of market participants on positive news.

Weekly data from the US supports the optimistic approach. Over the past fortnight, the number of active oil drilling rigs has fallen to 474 from 483. This decline is due to oil producers reacting to the decline in oil prices to 4-year lows. This was also evidenced by a slight decline in production to 13.37 million bpd from 13.46 million bpd previously.

Meanwhile, commercial oil inventories have been falling by 2mbpd and 2.7mbpd in the last couple of weeks, which is the opposite of the seasonal trend of rising inventories. As a result, commercial inventory levels are now 4.6% lower than a year earlier.

Although daily timeframes show a bullish divergence (new price lows correspond to a higher RSI value), more emphasis is placed on the weekly charts. There is no similar divergence between them, and the price has yet to be tested for the April reversal area.

Only exceeding $67 per barrel of Brent and $64 for WTI will attempt to turn the rebound into growth. The final confirmation will be a strengthening of another $4 to $71 and $68, respectively. In this case, the price will recover above the former support level, which has become resistance. In addition, a recovery in this area would indicate a rise of more than 20% from the May lows, signalling the start of a bull market.

UK Labor Market Cools, US CPI Next, Pound Steady

The British pound has edged higher on Tuesday. In the European session, GBP/USD is trading at 1.3218, up 0.34% on the day.

UK employment, wages cool

Uncertainty over the global economy, particularly US tariff policy, weighed on the UK employment report. The economy added 112 thousand jobs in the three months ending in March, down sharply from 206 thousand a month earlier and shy of the market estimate of 120 thousand. It was the weakest job growth in three months.

The unemployment rate inched up to 4.5% from 4.4%, in line with expectations and its highest level since August 2021. Wage growth including bonuses eased to 5.5% from a revised 5.7%, above the market estimate of 5.2%.

The Bank of England cut rates by a quarter-point to 4.25% last week but remains in a bind. The cooling job market should push inflation lower but wage growth remains stubbornly high and is an upside risk to inflation. The BoE will have to carve out a rate path that balances a weaker labor market with high wage growth - this could mean a delay in further rate cuts until late in the year. The BoE meets next on June 19.

US CPI expected to rise in April

The US releases the April inflation report later today. Headline CPI is expected to rise to 0.3% m/m, up from -0.1% in March, which marked the first decline since June 2024. Annually, headline CPI is expected to remain unchanged at 2.4%. Core CPI is also expected to climb to 0.3% from 0.1%. Annually, core CPI is projected to remain at 2.8%.

The escalating trade tensions due to US tariffs have raised concerns that US growth will fall and inflation will decline, even resulting in a recession in the US. The US-China agreement to slash tariffs, which will be in effect for 90 days, is an important de-escalation in the trade war and should curtail inflation and reduce the risk of a recession.

GBP/USD Technical

- GBP/USD is testing resistance at 1.3205. Above, there is resistance at 1.3271

- 1.3112 and 1.3046 are the next support levels

GBPUSD 1-Day Chart, May 13, 2025

German ZEW economic sentiment surges on stabilizing domestic politics and trade progress

Investor sentiment in Germany and the wider Eurozone improved sharply in May, with ZEW Economic Sentiment Index for Germany jumping from -14.0 to 25.2, well above the expected 9.8. Eurozone sentiment followed suit, rising from -18.5 to 11.6, also beating expectations.

According to ZEW President Achim Wambach, the rebound reflects growing optimism tied to easing trade tensions, a new German government, and stabilizing inflation, helping to offset last month’s sharp deterioration.

However, views on current conditions remain deeply negative. Germany’s Current Situation Index edged down further from -81.2 to -82.0, missing forecasts. Eurozone’s improved modestly but still stood at -42.2. This divergence suggests that while expectations for the months ahead are improving, near-term economic conditions remain fragile, particularly in Germany.

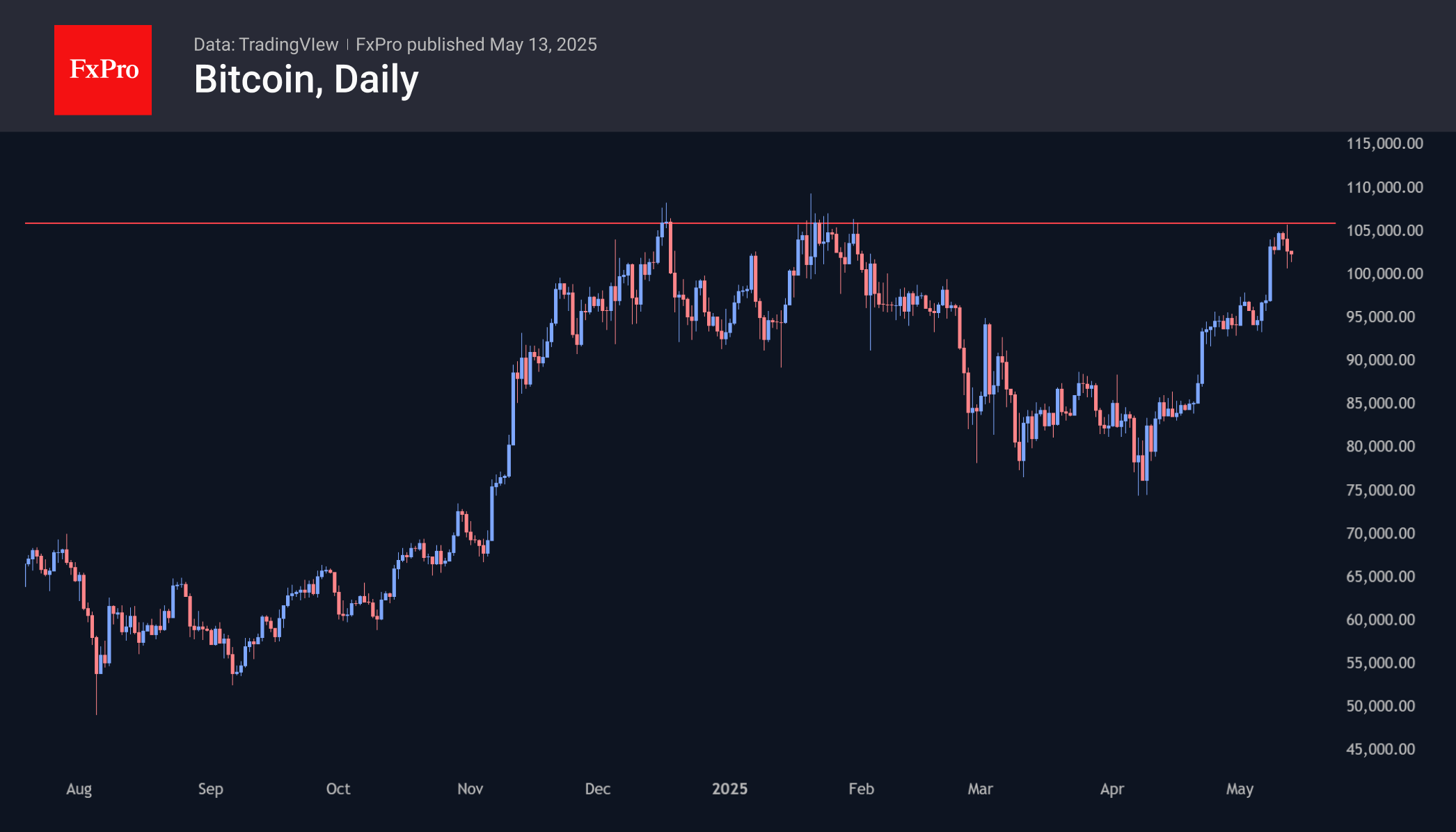

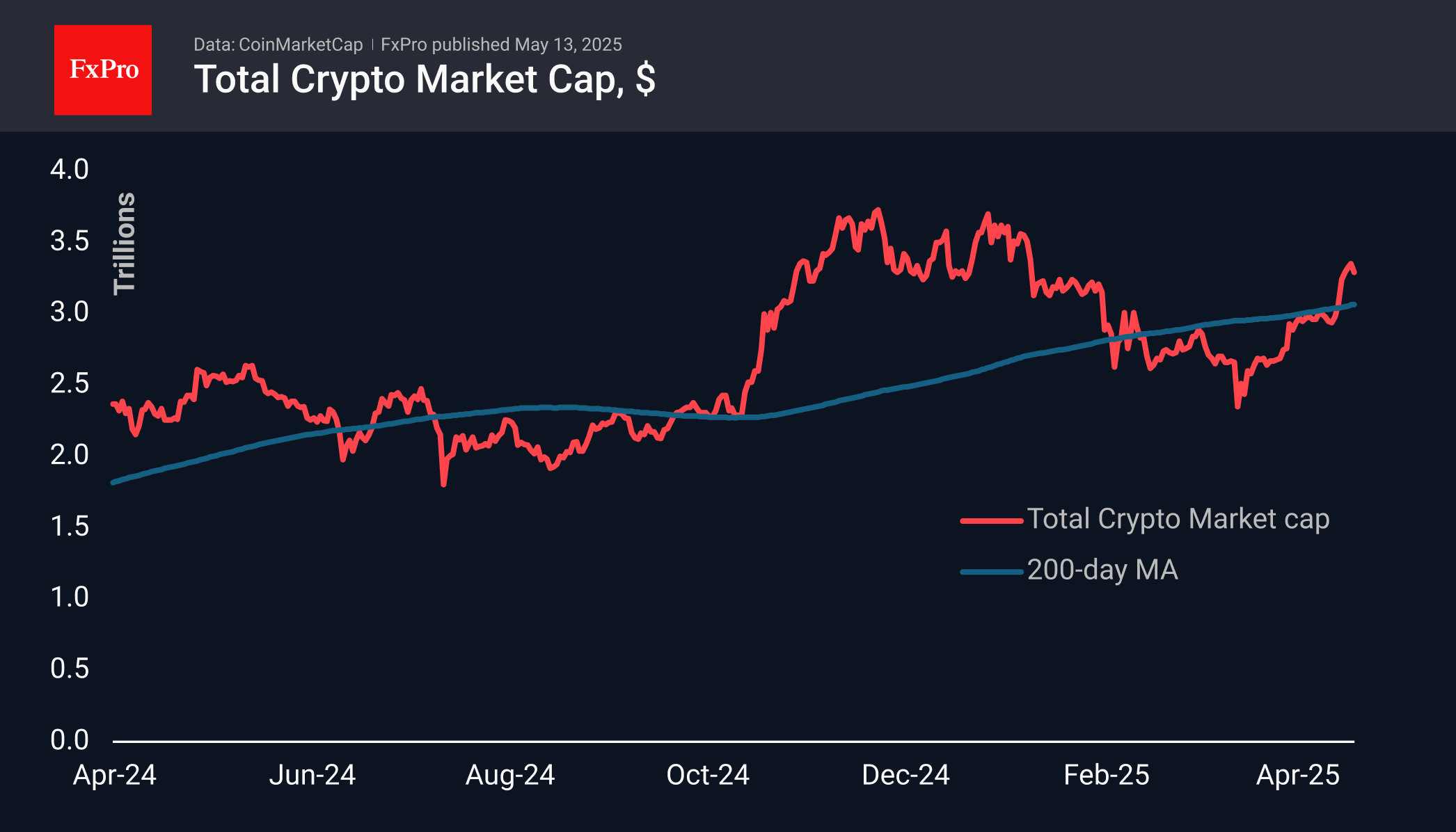

Crypto Booked Profits Amid General Euphoria

Market Picture

The Crypto market cap has fallen 1.7% in the last 24 hours to $3.29 trillion, despite continued positive traction in the equity market. The strengthening dollar on news of tariffs has been a natural drag on cryptos. This is doubly true due to Bitcoin’s proximity to the highs, reinforcing the pull for short-term profit taking after rallying in just over a month.

The sentiment index is stuck at 70 for a fourth day, indicating investors continued healthy greed despite the intraday pullback.

Bitcoin showed its unpredictable nature on Monday, dropping to $100.5k at one point, contrary to the impressive rally in other markets. But it was clearly profit taking followed by buying that brought the price back to $102.7k. With the positivity remaining, it is worth paying attention to the price dynamics near $105k. Will we see an acceleration or a new failure? The answer will allow for the prediction of the dynamics of the next days.

News Background

According to CoinShares, global investments in crypto funds rose by $882 million last week, with significant inflows for the third week in a row. Bitcoin investments increased by $867 million, Ethereum by $1.5 million, XRP by $1.4 million, and Sui by $12 million. Investments in Solana decreased by $3.4 million.

Coinshares suggests that the growth of investments was due to a combination of factors: the global growth of the M2 money supply, risks of stagflation in the US, and the approval of bitcoin as a strategic reserve asset by several US states.

HTX Research believes that Bitcoin’s current growth is being fuelled by institutional investors, including Abu Dhabi’s sovereign wealth fund and BlackRock’s increasing position in the BTC-ETF.

Presto Research noted that Bitcoin’s dominance has reached levels last seen before the 2021 bull market, and capital is starting to flow into altcoins.

Nakamoto Holdings will be the first publicly traded conglomerate to integrate cryptocurrency into traditional financial structures. It aims to raise $710 million to create a Bitcoin reserve.

Options on Solana (SOL) recorded large call option purchases with a 27 June maturity and a $200 strike, Amberdata notes. If SOL crosses the $200 mark, volatility may increase sharply.

Hang Seng Index Pulls Back as Trade Deal Optimism Fades

Yesterday, Hong Kong’s Hang Seng Index (Hong Kong 50 on FXOpen) climbed above the 23,600 mark, supported by progress made during US–China tariff negotiations.

However, today the Hang Seng Index (HSI) has dropped towards the 23,100 level, which may be explained by fading optimism that dominated the market a day earlier.

According to Reuters, Christopher Hodge, Chief Economist at investment bank Natixis, stated that “these talks will yield nothing of long-term value. Ultimately, tariffs will still be significantly higher and will weigh on US economic growth.”

Technical Analysis of the Hang Seng Index (HSI) Chart

Price movements are forming an upward trend channel (marked in blue), with the following features:

→ The price is situated in the upper half of the channel (a sign of demand), and the upper boundary appears to act clearly as resistance;

→ Yesterday’s reversal suggests that bears became active above the former support area near the 23,385 level.

In this context, it is reasonable to assume that the Hang Seng Index (Hong Kong 50 on FXOpen) may test the support zone formed by the psychological level of 23,000 and the median line of the ascending channel. If the fundamental backdrop gives markets more reasons for caution, a deeper correction towards the lower boundary of the blue channel cannot be ruled out.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.