Sample Category Title

Markets Scaled Back Expectations on Fed Easing This Year

Markets

Substantial progress in the trade negotiations with China this weekend in Switzerland as touted by the US administration triggered an impressive reflationary move of global markets. Both US and most other core bond yields jumped sharply higher in an impressive bear steepening move. US yields rose between 11.9 bps (2-y) and 7.1 bps (30-y). Markets scaled back expectations on Fed easing this year from 75 bps last week tot about to 50 bps eoy. A first rate cut also is pushed to the September meeting rather than July as expected before last week’s Fed meeting. Fed Chair Powell at least can consider his reactive rather than a proactive approach fully validated by the administration U-turn on tariffs. With the Trump administration still working on deregulation and tax cuts, the case for a higher-for-long approach is strengthened even further. Of course, further down the road, the Fed still might come in a position to ease policy as the impact of current uncertainty on growth at some point still might filter through. However, the timing probably will be later rather than sooner and isn’t the focus of the market momentum at this stage. European/German bonds even slightly underperformed especially at the short end of the curve, with German yields adding between 12.8 bps (2-y) and 6.2 bps (30-y), safe haven bunds understandably underperforming swaps. Of late, the impact of the trade war on Europe was assessed as outright deflationary by at least part the ECB MPC members. In case of a further de-escalation and/or progress in EU-US trade talks, this argument might lose some weight, too. ECB hawks recently at least become a bit more vocal with Isabel Schnabel this weekend and Buba president Nagel but also Spanish Member Escriva to some extent joining the idea that current volatile environment might be a good reason not to overreact to short term developments. European markets reversed recent bets for the ECB to cut rates below 1.75%. Especially US equity markets reacted euphorically with the Nasdaq (+4.35%) more than reversing the post-Liberation Day sell-off. The Eurostoxx 50 even is nearing the cycle top reached early March. On FX markets, the dollar now is the preferred risk currency. DXY came with reach of the 102 barrier. EUR/USD briefly dropped below 1.11 (close 1.1086). USD/JPY (164.6 close) is nearing the 164.9/166.7 range top).

Markets today might gradually look for a new equilibrium after yesterday’s sharp repositioning. US equity futures, US yields and the dollar this morning are ceding marginal ground. Regarding the data, ZEW economic sentiment deserves some attention. In the US, we look for the NFIB small business sentiment and even more for the US April CPI. Markets will look whether some tariffs related prices rises already are filtering through. Consensus expects 0.3% M/M both for headline (2.4%Y/Y ) and core inflation (2.8% Y/Y). An upward surprise might only reinforce Powell’s reactive approach. Such a scenario might support the rise in yields, but probably won’t be good news for the risk rally. The impact on the dollar also might be more mixed. However, it’s too early to anticipate on a genuine trend reversal on yesterday’s repositioning.

News & Views

UK retail sales rose by 6.8% Y/Y in April, rising from 0.9% in March and beating consensus estimates (2.3%). The British Retail Consortium pointed out that Easter falling in April rather than March artificially lifted sales (and weighed on growth in March). The sunniest April on record also provided a boost to sales. Food sales increased 8.2% Y/Y while non-food revenues rose by 6.1% Y/Y. BRC CEO Dickinson nevertheless warned for clouds on the horizon as “new costs begin to bite”. She refers to an estimated £7bn of costs to the industry coming from higher Employer National Insurance Contributions, the higher National Living Wage and a new packaging tax.

Bulgarian President Radev filed a request to parliament to organize a referendum on euro adoption. The proposed referendum question "Do you agree to have Bulgaria adopt the single European currency euro in 2026?" will test the democracy and provide an opportunity to hear all the arguments for and against the monetary policy move. The politically loaded push comes as the country waits the June 4 publication of convergence reports by the EC and the ECB and against the background of a divided political and societal landscape. A similar request for euro referendum was filed by the far-right pro-Russian Revival party and eventually rejected by the country’s constitutional court. Interior minister Mitov called the referendum “a clear act of sabotage against the introduction of the euro in Bulgaria” with PM Zhelyazkov urging lawmakers to ignore the President’s request.

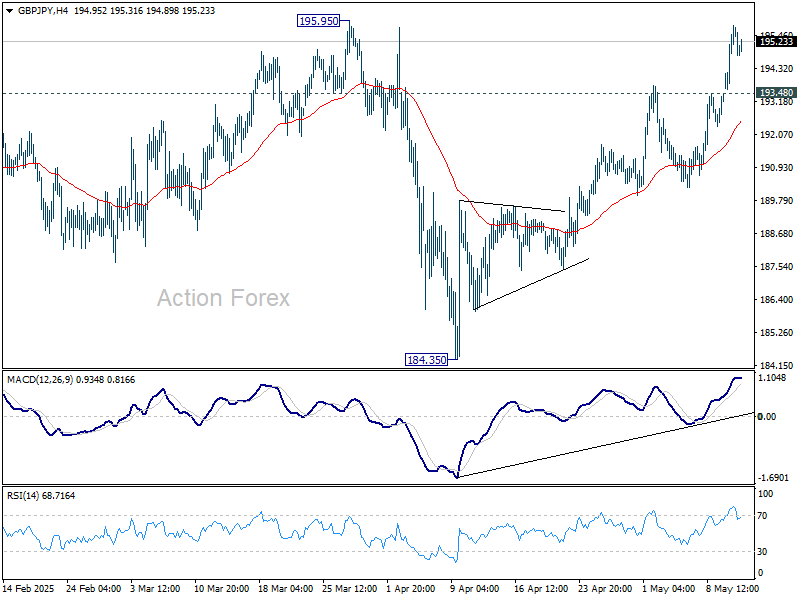

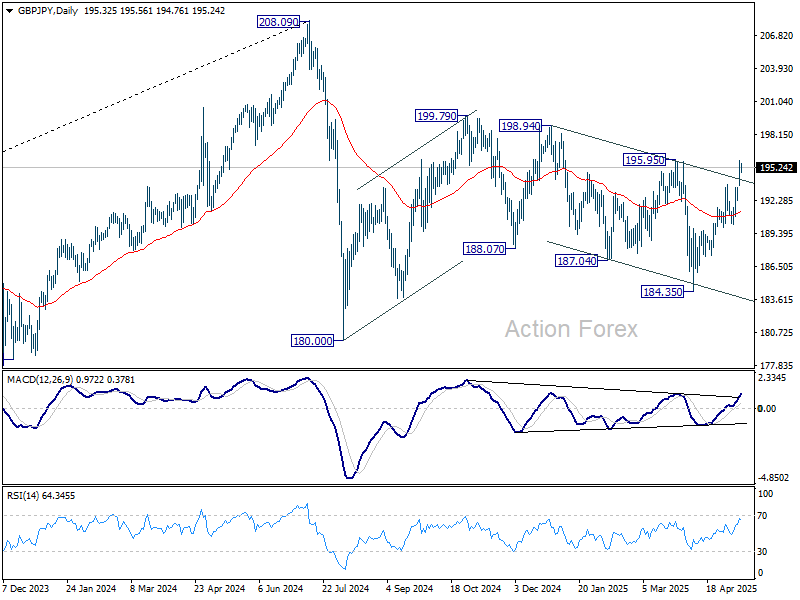

GBP/JPY Daily Outlook

Daily Pivots: (S1) 194.22; (P) 195.02; (R1) 196.40; More...

Intraday bias in GBP/JPY remains on the upside for the moment. Current rise from 184.35 is in progress and break of 195.95 resistance will suggest that whole choppy decline from 199.79 has completed. On the downside, below 193.48 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

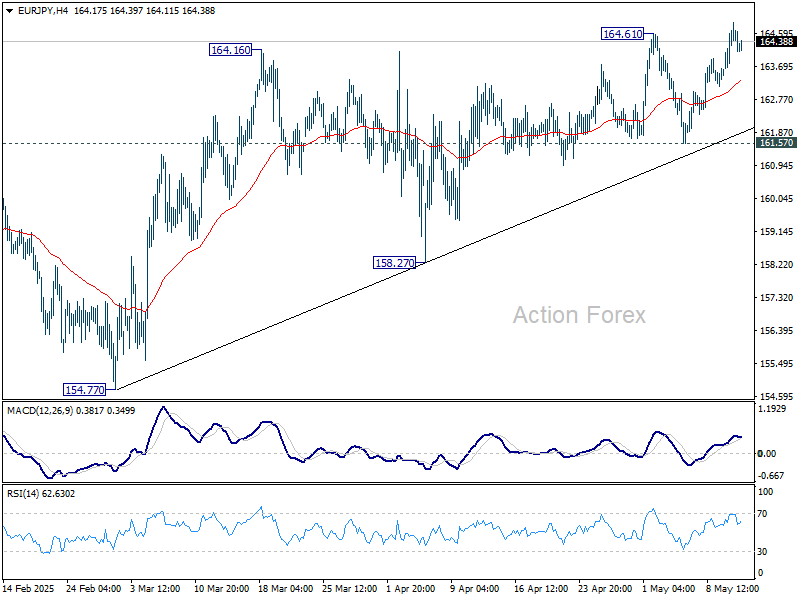

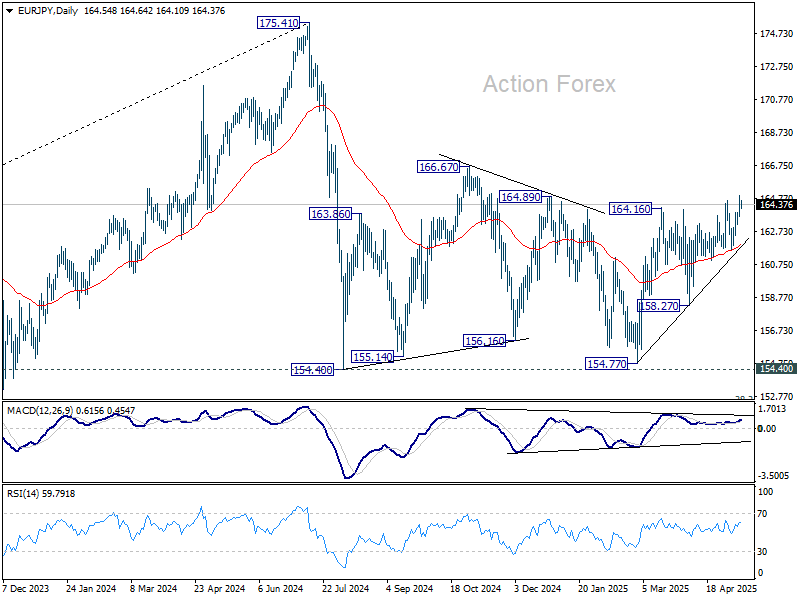

EUR/JPY Daily Outlook

Daily Pivots: (S1) 163.86; (P) 164.39; (R1) 165.15; More...

EUR/JPY's rally from 154.77 resumed by breaking 164.61 resistance and intraday bias is back on the upside. Further rally should be seen to 166.67 resistance. For now, risk will stay on the upside as long as 161.57 support holds, in case of retreat.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

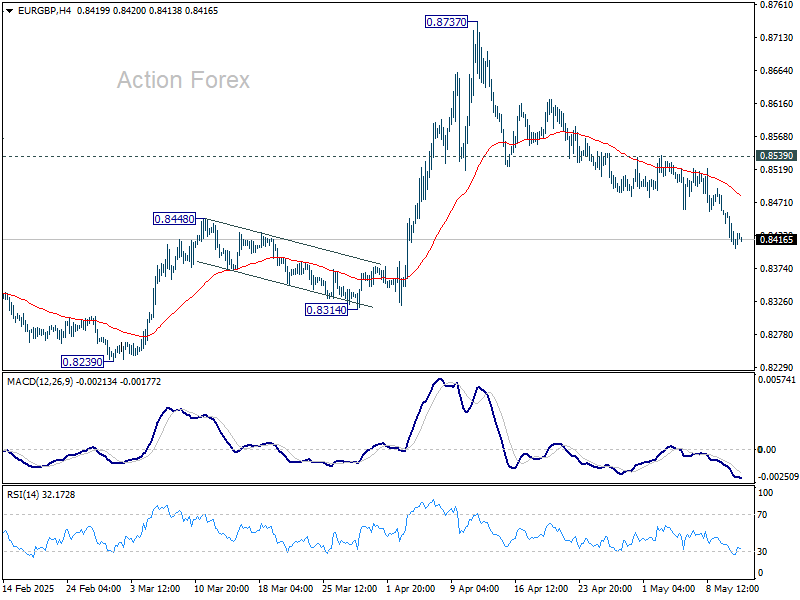

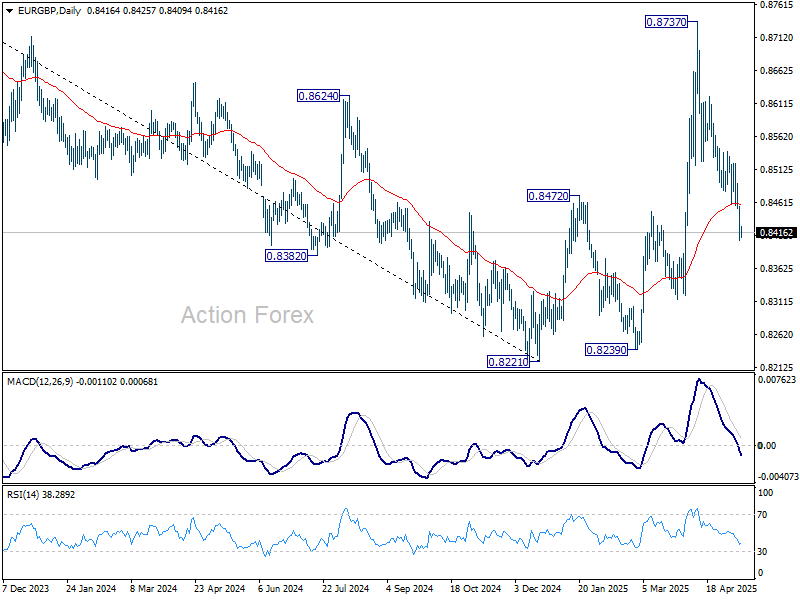

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8394; (P) 0.8426; (R1) 0.8447; More...

Intraday bias in EUR/GBP remains on the downside for the moment. Current development suggests that whole rebound from 0.8221 has completed as a corrective move. Further decline should be seen back to 0.8221/8239 support zone. For now, risk will stay on the downside as long as 0.8539 resistance holds, in case of recovery.

In the bigger picture, the extended decline from 0.8737 dampened the original bullish view. While a medium term bottom was in place at 0.8221, price actions from there could be a corrective pattern only. Larger down trend from 0.9267 (2022 high) might still be in progress. Sustained trading below 55 W EMA (now at 0.8438) will turn favor to this bearish case.

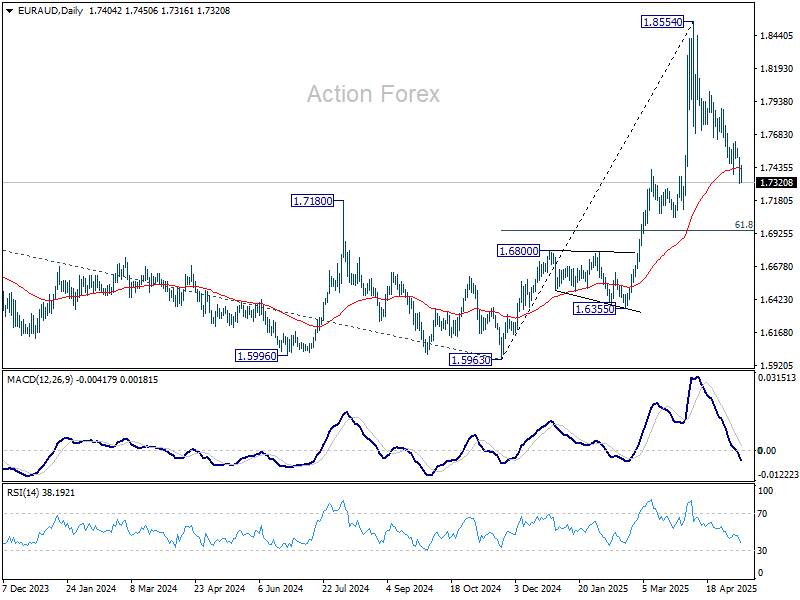

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7303; (P) 1.7409; (R1) 1.7506; More...

EUR/AUD's fall from 1.8554 resumed by breaking through 1.7380 and intraday bias is back on the downside. Sustained trading below 55 D EMA (now at 1.7431) will target 61.8% retracement of 1.5963 to 1.8554 at 1.6953 next. On the upside, break of 1.7628 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, as long as 1.7062 resistance turned support (2023 high) holds, up trend from up trend from 1.4281 (2022 low) should still be in progress. However, sustained break of 1.7062 will confirm medium term topping and bring deeper fall back to 1.5963 support.

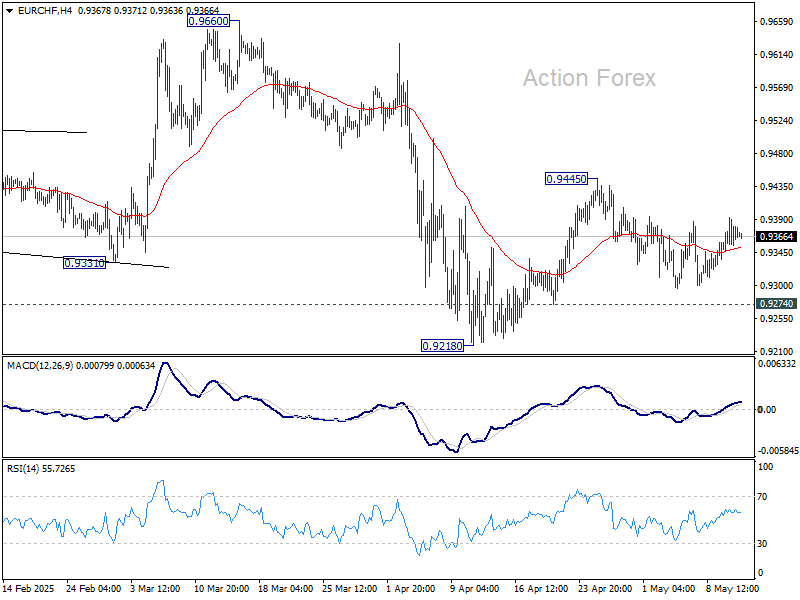

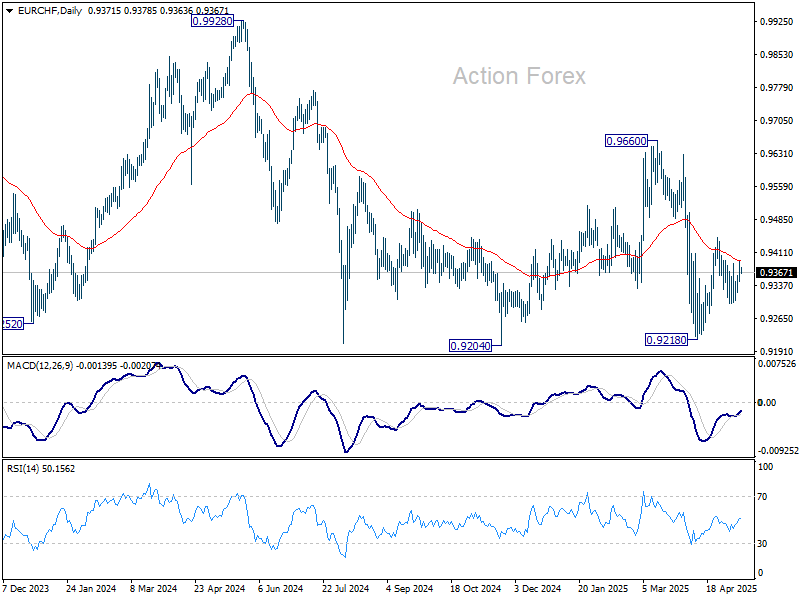

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9346; (P) 0.9370; (R1) 0.9401; More....

Intraday bias remains neutral in EUR/CHF as sideway trading continues. On the upside, above 0.9445 will resume the rebound from 0.9218, either as a corrective move or the third leg of the pattern from 0.9204. However, break of 0.9274 will suggest that that recovery has completed, and bring retest of 0.9204/18 support zone.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9548) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

What an Unexpected Turn of Things

What a blast we had yesterday, didn’t we? The week kicked off with the news that the US and China would announce ‘substantial’ progress in trade negotiations — and the progress was indeed close to substantial. Tariffs were pulled down from 145% to 30% for Chinese exports to the US, and from 125% to 10% for American exports to China.

Yes, the deal is valid for just the next 90 days — similar to the trade relief that the rest of the world currently enjoys from the US administration — but it’s still a big surprise given that we had come to the conclusion the two sides would never talk again. Ever.

So, markets raved with joy. The S&P 500 jumped more than 3%, breaking above both its 100- and 200-day moving averages and adding $1.7 trillion in market value. The Nasdaq 100 surged more than 4%, cleared the 20K offers, and broke its 100- and 200-DMAs. Apple, Tesla, and Nvidia — which had remained in the crossfire — all added between 5–6%, while Amazon rallied more than 8%. The Nasdaq Golden Dragon China Index gained 5.40%. The Dow Jones climbed 2.80%, and US crude rose to $63.60 per barrel.

Small- and mid-cap stocks, however, remained more muted despite the news and even posted slight losses, as the developments dented dovish Federal Reserve (Fed) expectations. The US 2-year yield jumped to 4% on thinking that the tariff pause could support the US economy and reduce the need for Fed support. The probability of a June rate cut fell to below 12%, from nearly 14% before the announcement details came out. The US dollar rebounded sharply, gold tanked 2.73%, and the USD/CHF jumped 1.73% — excellent news for the Swiss National Bank (SNB).

In Europe, the Stoxx 600 rose 1.21%, on the realisation that the US administration isn’t as sanguine as it sounds when fundamentals are shaken. The SMI and FTSE 100 lagged behind other major indices, as heavyweight pharmaceutical stocks came under pressure from Donald Trump’s push to reduce prescription drug prices to the lowest global levels. But even that worry faded, as the fine print suggested that companies will be given a chance to lower prices voluntarily before any action is taken.

So yes — it could hardly have been better.

In Asia, the CSI 300 rose more than 1% and the Nikkei surged 3.40%, though gains are being given back today. European and US futures are also down — a bit of a hangover after yesterday’s party, a moment to question how good the news really is, and how long the truce might last.

Because while recent days have brought major progress to the table, this isn’t the end. Talks could be interrupted at any point, as strategic decoupling between the US and China will continue for national security reasons — keeping pressure on key sectors, including semiconductors.

Also worth noting: the so-called de minimis exemption that allows cheap Chinese products into the US remains at 120% — meaning Shein and PDD won’t massively benefit from the tariff relief.

And of course, uncertainty over what happens after the 90-day pause will keep many companies in wait-and-see mode, delaying investment decisions until a more durable truce emerges.

In the best-case scenario, the damage will be contained. In the worst-case, we start all over again.

One certainty: shipments to the US will continue at full speed in fear of another breakdown and frontloading will likely continue to pressure the US Q2 GDP reading.

Today, investors are walking into the US CPI update with a lighter heart. There’s a chance that the 90-day tariff pause — along with the latest dip in consumer sentiment — could help temper inflationary pressures in the US and give the Fed more room to act, if needed.

Bloomberg’s analyst survey suggests that both headline and core inflation likely jumped in April (m-o-m) due to the tariff situation. If the data comes in line or ideally softer-than-expected, it would reinforce the bullish mood — taming selling pressure on US Treasuries, boosting equities and the dollar. A stronger-than-expected read wouldn’t echo well, but might still be partly overlooked, given the dramatic shift in trade expectations.

Speaking of inflation, eurozone countries will also be updating their April inflation figures this week. Early April data had surprised to the upside, denting dovish European Central Bank (ECB) expectations. While the ECB is still expected to continue cutting rates, the expected pace is now slower. The EURUSD is giving back early-year gains as tariff de-escalation improves US growth prospects. But euro bulls see beyond the ECB/data narrative: many believe the ongoing trade war will help cement the euro’s position as a global reserve currency. Currently, the euro makes up about 20% of central bank reserves — versus 60% for the USD — and there’s room for more.

The EURUSD fell to its 50-DMA yesterday on broad-based dollar strength. For those betting on the euro’s long-term fortunes, current levels could present interesting dip-buying opportunities.

US CPI in the Limelight

In focus today

In the US, the most important data release for today will be the April CPI. We expect the tariffs to start putting gradual upward pressure on especially core goods prices and look for both headline and core inflation to accelerate to +0.3% m/m SA. NFIB's Small Business Confidence index is also due for release ahead of the CPI.

In Germany, focus turns to the ZEW index for May. The estimate of the current economic situation has shown a bottom in German activity like hard data on industrial production. It has yet to show a clear rebound, and expectations for future growth declined greatly in April following 'Liberation Day'. Expectations will likely rebound partly due to the less negative signals on trade barriers from the Trump administration like we saw in the Sentix indicator. Focus will thus centre on whether the current situation has deteriorated due to the tariff uncertainty.

Economic and market news

What happened yesterday

In the trade war, the joint statement from the US-China trade talks announced a successful de-escalation, with tariff reductions exceeding expectations. The US will lower tariffs on Chinese imports from 145% to 30%, while China will reduce duties on US goods from 125% to 10% for an initial 90-day period. Later, news reports added that the agreement does not include reinstating "de minimis" exemptions for low-value e-commerce shipments, and President Trump noted that it does not cover the possible separate tariffs on cars, steel, aluminium, or pharmaceuticals. The cuts will take effect on 14 May, with both nations committed to establishing a mechanism for ongoing discussions on trade relations. The agreement has led to a rally in global stocks, higher yields, and declines in EUR/USD and USD/CNY, indicating risk-on and reduced concerns over a US-driven growth slowdown. Markets now predict only a 10% chance of a Fed rate cut in June, with a 25bp cut expected by September. Read more in US-China Flash: Trade talks succeed in de-escalation, 12 May.

In the US, President Trump signed an executive order aimed at setting price targets for pharmaceutical manufacturers, with provisions for direct consumer purchases, eliminating intermediaries. Should pharmaceutical companies fail to meet government pricing expectations, the administration intends to implement rulemaking to align drug prices with international levels. Potential measures include importing medicines from other developed nations and imposing export restrictions. The President is targeting price reductions of 59% to 90%. That said, the exact details on the planned implementation and whether the measures needed congressional approval remained unclear.

In Denmark, Statistics Denmark reported inflation at 1.5% for April, with lower energy prices and increased travel costs due to Easter timing. Food prices decreased slightly but remain 3.7% higher than last year. Core inflation rose to 1.7%, still below the ECB target, indicating controlled price pressures in Denmark. Despite elevated concerns from Trump's trade war, these fears may be overstated, as the trade conflict could ultimately lead to lower inflation through decreased global demand and cheaper imports driven by a stronger euro. Although EU tariffs on US goods might counteract these effects, they are unlikely to significantly affect Danish consumers.

Equities: You could almost hear the unwinding off puts and shorts squeezing yesterday, as equities rallied on tariff relief. S&P 500 added 3.3% and Nasdaq a full 4.4%, with indexes rallying into the close. As such, US recovered much of its underperformance, with European equities "only" gaining 1% yesterday and Chinese equities even lower this morning. Defence sold off in Europe, suggesting investors shaved off some of their long positions to buy into US. Sector-wise, this was not a "buy everything" rally but believe it or not, a selective one. Defensives and real estate missed out entirely while cyclical sectors added between 2-5%. VIX closed below the important 20-level, which typically resonates with positioning support for risk parity funds. US futures are retreating somewhat this morning and European futures are little changed.

FI&FX: Yesterday's session in FX and FI markets was all about the unwind of the post-Liberation Day trades. Rates curves bearish flattened across currencies amid not least short-ends coming higher on markets pricing in less monetary policy easing this year. Credit spreads tightened, Bund-Periphery spreads performed and US Treasury ASW spreads tightened (richer bonds). In FX space the CNY and USD strengthened considerably with EUR/USD falling back to the 1.11 level. Also, CAD and AUD did well while the CEEs, the EUR and JPY where all underperforming. Interestingly, the SEK was caught between opposing forces leaving the trade weighted Krona little changed on the day.

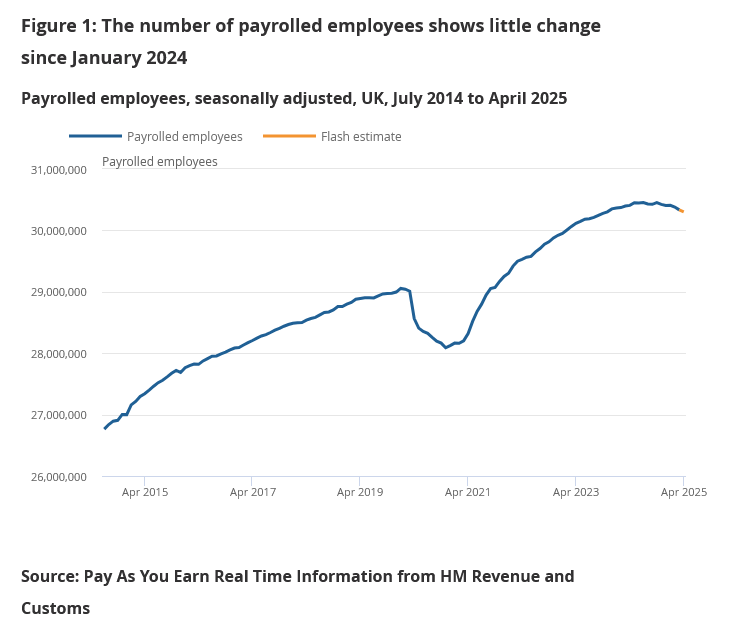

UK payrolled employment falls -33k, wage growth remains elevated

UK labor market data for April showed signs of softening in employment but continued strength in wage growth. Payrolled employment fell by -33k (-0.1% mom), while the claimant count rose by 5.2k. Median monthly pay rose by 6.4% yoy in April, accelerating from 5.9% yoy in the previous month.

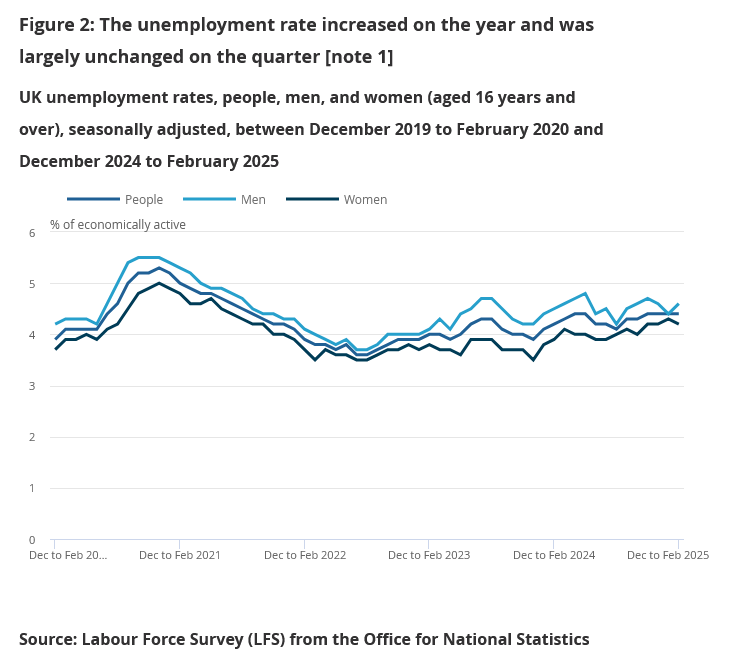

In the three months to March, unemployment rate in the three months to March edged up from 4.4% to 4.5%, in line with expectations and marking the highest level since late 2021.

Average earnings including bonuses rose 5.5% yoy, beating expectations of 5.2% yoy. Earnings excluding bonuses rose 5.6% yoy, slightly below forecast of 5.7% yoy.

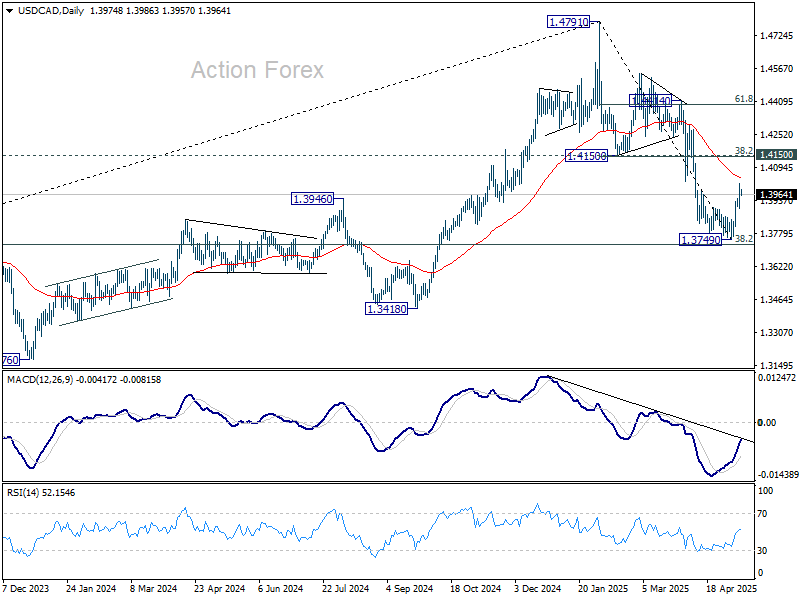

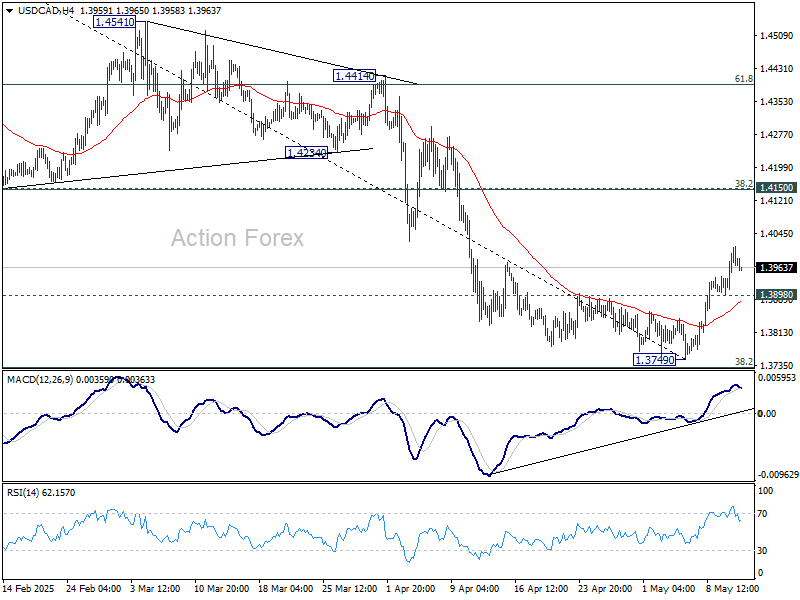

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3910; (P) 1.3963; (R1) 1.4028; More...

Intraday bias in USD/CAD remains on the upside as rebound from 1.3749 short term bottom is in progress. Break of 55 D EMA (now at 1.4043) will target 1.4150 cluster resistance (38.2% retracement of 1.4791 to 1.3749 at 1.4147). On the downside, below 1.3898 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4150 resistance turned support holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.