Sample Category Title

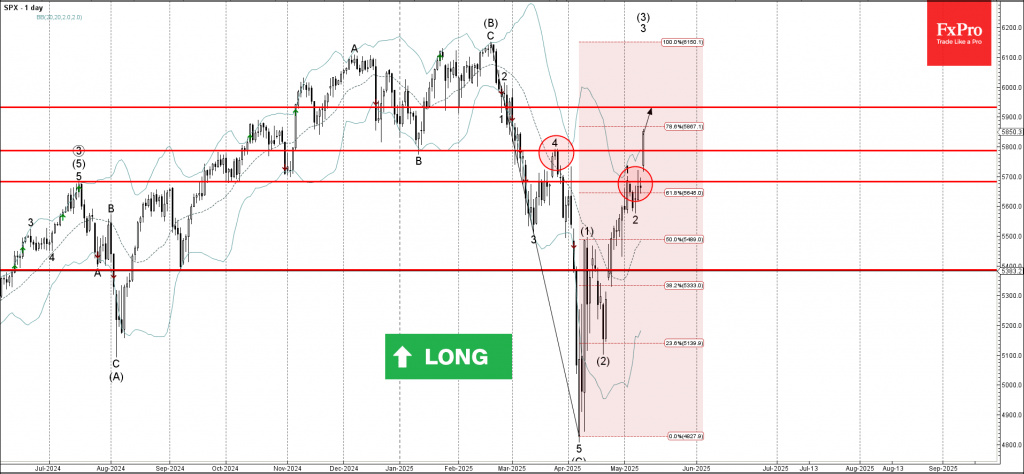

S&P 500 index Wave Analysis

S&P 500 index: ⬆️ Buy

- S&P 500 index broke resistance area

- Likely to rise to resistance level 5930.00

S&P 500 index recently broke the resistance area between the resistance levels 5800.00 (top of wave 4 from March), 5700.00 (which stopped wave 1 at the start of May) and the 61.8% Fibonacci correction of the downward impulse from February.

The breakout of this resistance area is aligned with the short-term impulse wave 3 of the intermediate impulse wave (3) from April.

S&P 500 index can be expected to rise to the next resistance level 5930.00, former support from January and February.

Sunset Market Commentary

Markets

Markets are flying high following the “substantial progress” made during the first high-level US-Sino trade talks over the weekend. US Treasury Secretary Bessent, one of the attendees, shortly before the European open briefed what this meant in practice: a sharp reduction on both sides in import tariffs for 90 days. The US cut tariffs on Chinese goods from 145% to 30%. This level consists of the 10% base rate currently in place for all other countries and the 20% levy related to the separate issue of fentanyl. China in return lowered the rate to 10% from 125%. Risky assets shifted into an even higher gear after seeing the details, not least because US President Trump ahead of the talks suggested a much higher 80% tariff “seems right”. Bessent in an interview with Bloomberg a couple of hours later added a few more details to it. He said the 10% is a floor and it’s “implausible” the US would go below that level. The 34% announced on Liberation Day in turn is a ceiling. Adding the 20% fentanyl levy, which Bessent said could also be lowered if China takes action, brings that to a max tariff of 54%. Stock markets are on a tear, surging 1.7% in Europe and opening almost 4% higher in the US (Nasdaq). Pharmaceuticals do weigh on the performance with the sector underperforming on Trump’s aim to slash US drug prices. Core bond yields shoot up dramatically with curves bear flattening. Yields in the US rise between 5.2 (30-yr) and 11.1 bps (2-yr). And that’s only the beginning if Bessent’s “victory is a three-legged stool” view for year’s end comes true when the three parts of the US administration’s programme will be kicking in: a settlement to (most of) the trade disputes, having the tax bill done and deregulation across all industries. German rates add 5.4 bps to 13.6 bps in a similar shift. The 10-yr yield (2.64%) is returning to the gap opening levels (2.65%) in the wake Merz’ defense spending announcement early March. Bunds underperform vs. swap as well as European countries, pushing spreads lower both in semi-core and peripheral member states. It reflects a reversal of haven flows and possibly hopes for a similar quick breakthrough in US-European trade talks. It would reduce uncertainty materially and help avoid a sharp growth slowdown. Combined with the now-reduced disinflationary risk of cheap redirected Chinese goods flooding the European market, investors pare ECB rate cut bets materially. Money markets now assume the rate to be closer around 1.75% by year’s end than the 1.5% last Friday. This repositioning has some more room to go. The US dollar is the star performer in currency markets. EUR/USD at some point fell below 1.11 before paring losses to 1.112 currently, down from 1.1244 at the open. After losing the 1.1235 support, 1.1026 is the next reference to look at. USD/JPY surges to 148, the highest since the April 2 mayhem. The trade-weighted DXY came close to but never really tested 102. Other typical risk-on beneficiaries include the AUD and NZD as well as the Scandinavian currencies. The Swiss franc slips to EUR/CHF 0.937.

News & Views

According to a survey of published by the German Ifo Institute, companies in the German Industry are assessing that they are drastically losing competitiveness. 24% of companies rated their competitiveness compared to countries outside the EU as low. Competition within the EU is also becoming tougher, according to 21%. Hardly any company saw its position improve against global competition. “We have never seen a slump like this in international competition in such a short space of time” Klaus Wohlrabe, Head of Surveys at Ifo was quoted. The automotive industry, which has been losing ground for around two years, is particularly hard hit. The situation also remains tense in the metal and chemical industries. Beverage manufacturers are comparatively stable – their position in international competition has hardly changed recently. Ifo in this respect urges the new government to take decisive action to prevent the German industry from even further falling behind in international competition.

The unemployment rate in the Czech Republic in April remained stable at 4.3%. While still historically low, it compares to a level of 3.7% in April last year. The number of people looking for a job declined by 3.6k to 318.5 k. The number of vacancies rose by 4k to 95.8 k. The tight labour market and above average wage growth are mentioned as a factor of importance in the monetary policy assessment of the Czech central bank (CNB) as it is seen as contributing to services inflation. The CNB last week cut its policy rate by 25 bps to 3.5%, but indicated that any such easing steps have to be cautious and that monetary policy will remain tight with distinctively positive rates.

Japanese Yen Tumbles to Five-Week Low on US-China Tariff Deal

The Japanese yen has started the week with sharp losses. USD/JPY is trading at 148.18, up 1.9% on the day. Earlier, the yen strengthened to 148.59, its strongest level since April 3.

US and China agree to temporary cut in tariffs

The US and China have reached an agreement to slash tariffs on each other's products for 90 days. This would be a major de-escalation in the bruising tariff war between the world's two largest economies. Under the agreement, the US and China will slash tariffs by 115%, leaving US tariffs on China at 30% and China's tariffs on the US at 10%.

The tariff agreement has boosted risk appetite, sending global stock markets higher. The deal has weighed on safe-haven assets like the yen, which is sharply lower on Monday. Gold, another safe-haven, has plunged 3.1% today.

Japan's household spending, wages decelerate

In Japan, household spending and wage growth were down in March. Household spending decelerated to 0.4% m/m, down sharply from 3.5% in February. Average Cash Earnings declined to 2.1% y/y, down from a downwardly revised 2.7% a month earlier. There was more bad news as service-sentiment for April eased, reflecting concern over US tariffs.

These numbers support the case for the Bank of Japan to continue its wait-and-see stance before raising interest rates. The BoJ wants to see inflation remain sustainable at 2%, which will require higher wage growth and stronger consumer spending.

Fed members support Powell's wait-and-see stance

Over the weekend, a host of Fed members made public statements. New York Fed President John Williams and Fed Governor Adriana Kugler both noted that current rate policy was in an appropriate place and suggested patience was needed. This message echoed Fed Chair Powell's remarks at last week's FOMC meeting, when he said the Fed would take a wait-and-see attitude due to the uncertainty over US tariffs.

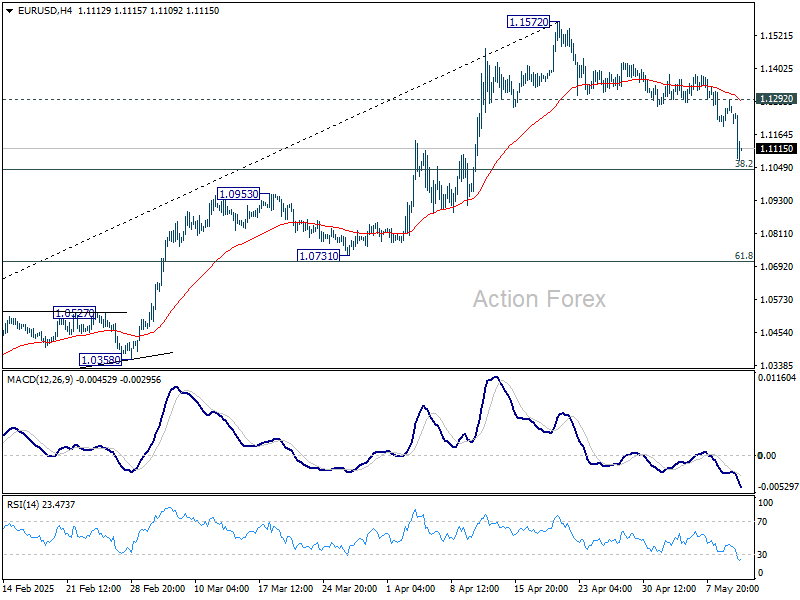

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1200; (P) 1.1246; (R1) 1.1296; More...

Intraday bias in EUR/USD's remains mildly on the downside for 55 D EMA (now at 1.1053) and possibly below. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039 to bring rebound. On the upside, break of 1.1380 will suggest that the correction from 1.1572 short term top has completed, and bring retest of 1.1572.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0789) holds.

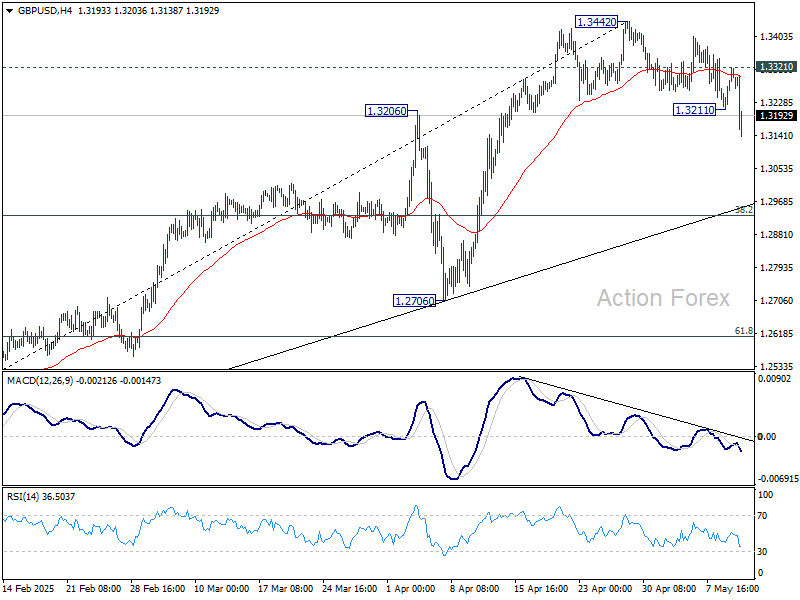

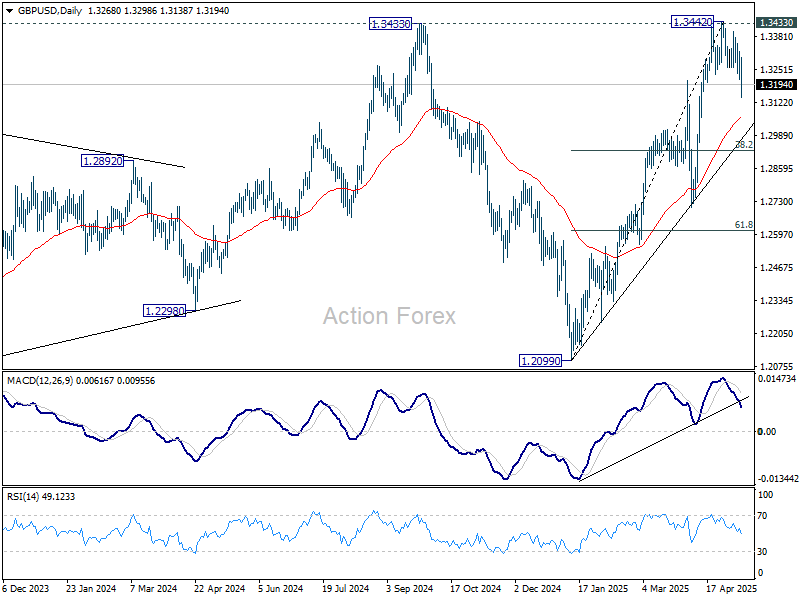

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3236; (P) 1.3279; (R1) 1.3347; More...

GBP/USD's fall from 1.3442 short term top resumed after brief recovery and intraday bias is back on the downside. Deeper fall should be seen to 55 D EMA (now at 1.3063) and below. But downside should be contained by 38.2% retracement of 1.2099 to 1.3442 at 1.2929 to bring rebound. On the upside, above 1.3321 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could either be resuming the up trend, or the second leg of a consolidation pattern. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on decisive break of 1.3433 at a later stage.

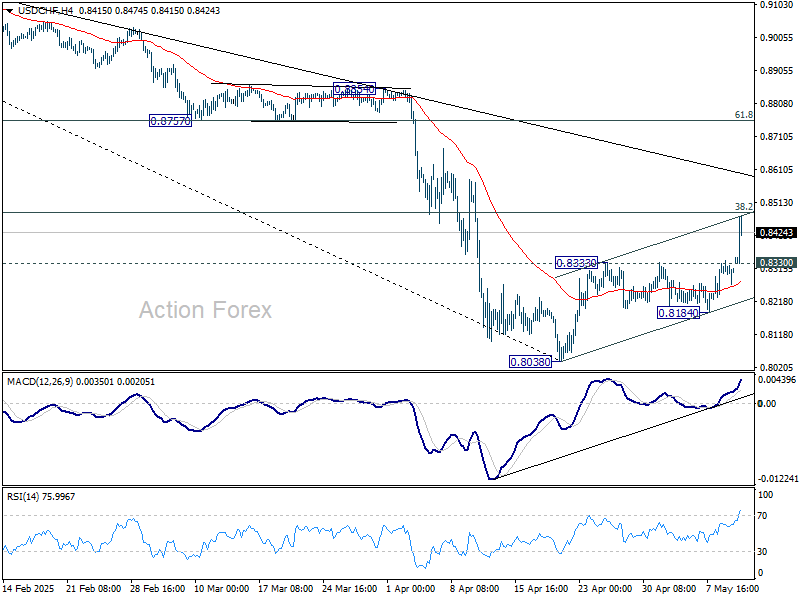

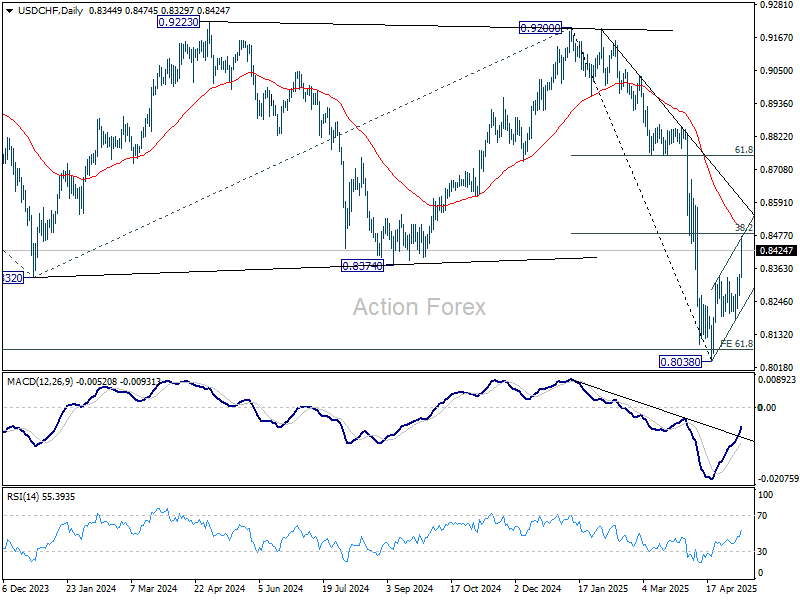

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8192; (P) 0.8232; (R1) 0.8278; More….

While USD/CHF's rebound from 0.8038 extended higher today, strong resistance is still expected from 38.2% retracement of 0.9200 to 0.8038 at 0.8482 to limit upside. Break of 0.8330 resistance turned support will turn intraday bias neutral first. Further break of 0.8184 will bring retest of 0.8038 low. However, sustained trading above 0.8482 will dampen this bearish view and target 61.8% retracement at 0.8756 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8750) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

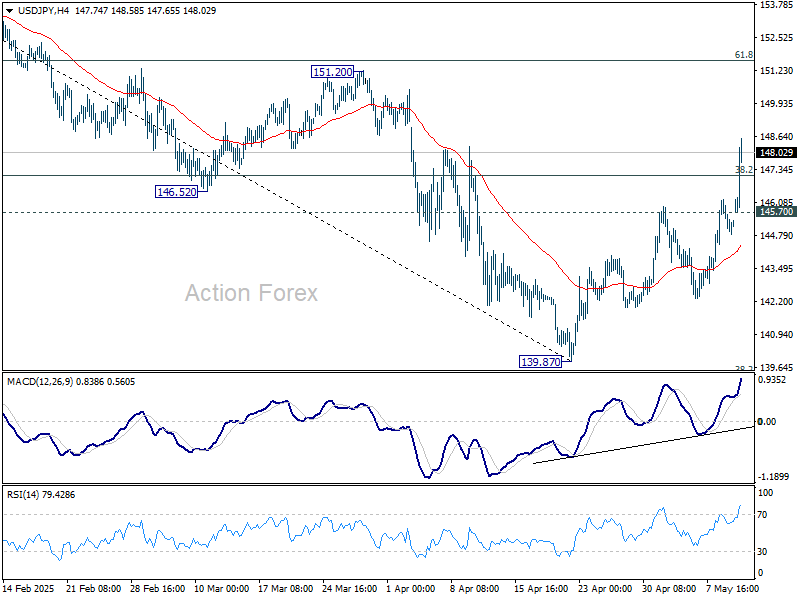

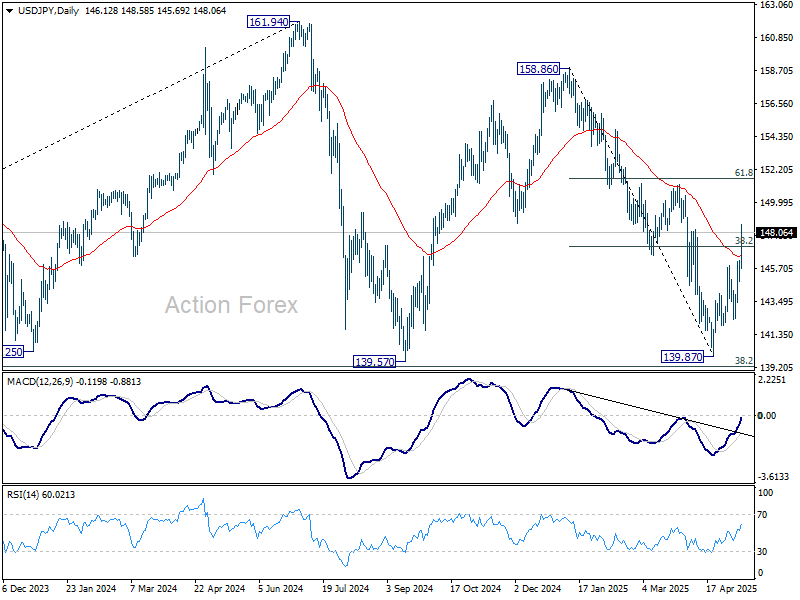

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.74; (P) 145.46; (R1) 146.11; More...

USD/JPY's rise from 139.87 accelerates higher today Break of 38.2% retracement of 158.86 to 139.87 at 147.12 suggests that whole fall from 158.86 has completed at 139.87, after defending 139.57 support and 139.26 fibonacci level. Intraday bias stays on the upside for 61.8% retracement at 151.60 next. On the downside, below 145.70 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Risk Assets Soar as US-China Tariff Rollback Surpasses Expectations

Global risk markets surged after the surprising breakthrough in US-China trade negotiations delivered results far beyond market expectations. Just days ago, hopes were low, with even the mere continuation of talks seen as a positive development. Investors had braced for a possible breakdown or at best, a symbolic gesture of engagement. Instead, both countries announced a major easing of tariffs, offering a rare dose of optimism to fragile global sentiment.

The agreement will see tariffs lowered on both sides for a 90-day period. Specifically, the US will cut its tariffs on Chinese goods from 125% to 30%, while China will reduce its duties on US goods from 125% to just 10%. The gap reflects the US’s decision to maintain a 20% base tariff linked to concerns about fentanyl imports. Still, the rollback represents a major de-escalation.

In a joint statement, both governments emphasized the intention to continue discussions in a “spirit of mutual openness” and “cooperation,” with follow-up meetings already being planned. US Treasury Secretary Scott Bessent confirmed he expects to meet Chinese officials again in the coming weeks to build on the momentum.

In the currency markets, Dollar is the strongest performer of the day. Commodity-linked currencies including the Aussie, Kiwi and Loonie are also advancing. In contrast, Yen is under significant pressure while. European majors are also lagging.

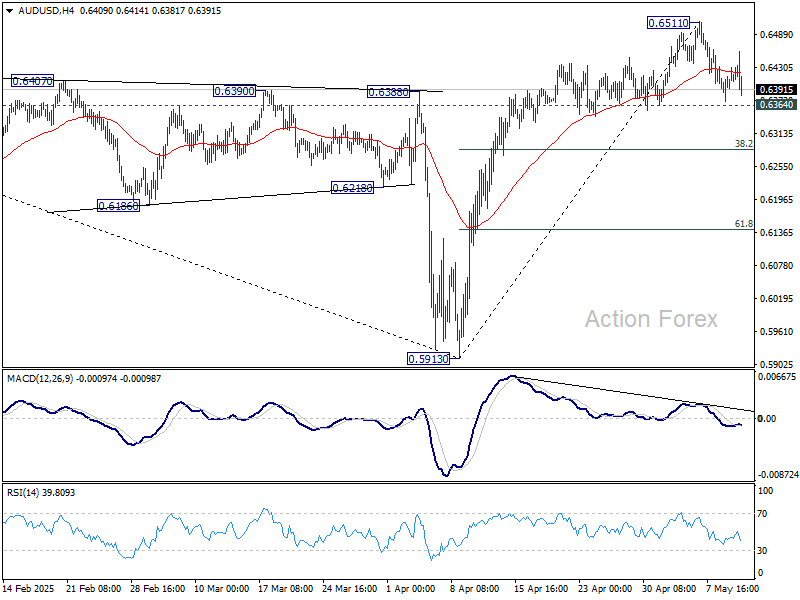

AUD/USD would now provide an important gauge to Dollar's underlying strength in this risk-on sentiment. Technically, break of 0.6364 support will confirm short term topping at 0.6511. Deeper decline would then be seen to 38.2% retracement of 0.5913 to 0.6511 at 0.6283. Firm break there will argue that whole rise from 0.5913 has already completed.

In Europe, at the time of writing, FTSE is up 0.64%. DAX is up 0.67%. CAC is up 1.46%. UK 10-year yield is up 0.089%. Germany 10-year yield is up 0.085 at 2.646. Earlier in Asia, Nikkei rose 0.38%. Hong Kong HSI rose 2.98% China Shanghai SSE rose 0.82%. Singapore was on holiday. Japan 10-year JGB yield rose 0.035 to 1.389.

BoE’s Lombardelli: Gradual cuts warranted as wage and services inflation stay high

BoE Deputy Governor Clare Lombardelli reinforced the case for a "gradual and careful" approach to policy easing in a speech today. She noted underlying inflation "have continued to fall" despite noises. Monetary policy is still restrictive and will continue to balance the need to lower inflation with the risk of undermining already soft demand.

Lombardelli highlighted wage growth as a central focus in the disinflation process, particularly given its outsized influence on domestic services pricing. She noted that private sector regular average weekly earnings rose 5.9% in February, still well above levels consistent with BoE’s inflation target. Services inflation, a key proxy for persistent price pressure, remains elevated at 4.7% as of March. Both indicators suggest that while progress has been made, inflationary momentum in wage-sensitive sectors continues to pose a challenge.

She also addressed the global backdrop, warning that higher US tariffs and increasingly uncertain American trade policy could lower growth and inflation in the short term by dampening global demand and trade volumes. However, over the longer term, if trade fragmentation continues, it could "reduce output and productivity and would raise inflationary pressures."

BoE’s Greene says trade risks justify rate cut

BoE MPC member Megan Greene said during a panel discussion today that while wages and inflation are moving in the right direction, they remain uncomfortably high. And more concerningly, "medium-term inflation expectations have also started picking up."

Greene, who voted with the majority last week in favor of a 25bps rate cut, the fourth since last August, revealed that she was initially undecided going into the meeting.

She noted being “torn” between holding rates steady and cutting, but ultimately decided to support easing. A key factor in her decision was the rise in global trade tensions, driven by US President Donald Trump’s sharp tariff hikes.

Despite the subsequent temporary trade truce between the US and China announced today, Greene said it would not have changed her vote.

She also flagged continued uncertainty over US-EU trade relations as a key downside risk for the UK economy, noting that any escalation could further dampen external demand.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.74; (P) 145.46; (R1) 146.11; More...

USD/JPY's rise from 139.87 accelerates higher today Break of 38.2% retracement of 158.86 to 139.87 at 147.12 suggests that whole fall from 158.86 has completed at 139.87, after defending 139.57 support and 139.26 fibonacci level. Intraday bias stays on the upside for 61.8% retracement at 151.60 next. On the downside, below 145.70 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Crypto Market Slows Down, Nearing a Top

Market Picture

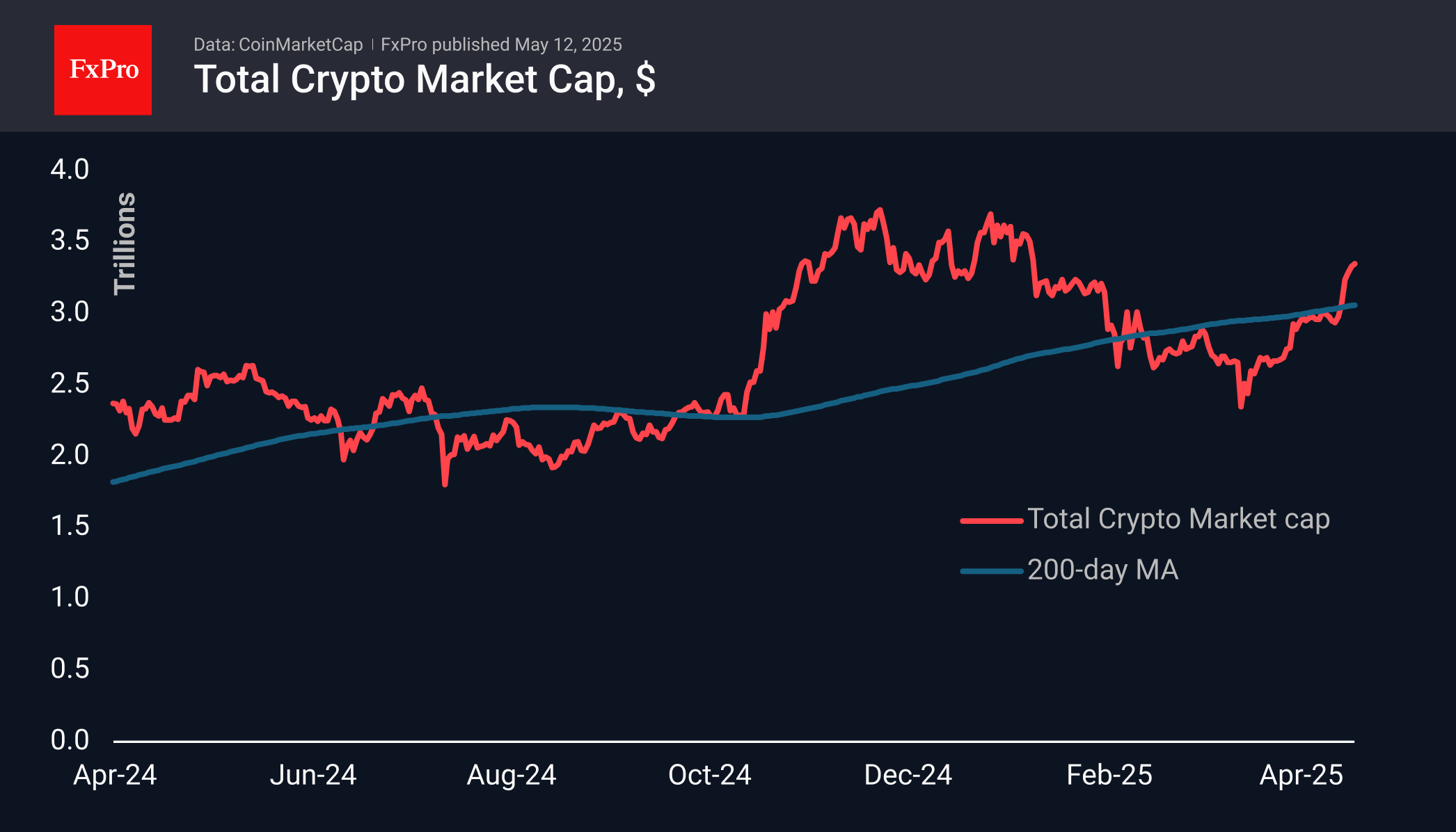

The crypto market slowed down but continued to move upwards over the weekend, reaching $3.35 trillion. For the past few days, it has been trading in the region of the highs since early February. Ethereum and Dogecoin have been the stars of this movement, adding around 40% in seven days, although the former’s contribution is certainly more significant.

The crypto market’s sentiment is consolidating in the greed zone, leaving the corresponding index at 70 for the last three days. This is a good basis for continued gains: not too hot to take profits and not too cold to leave traders on the sidelines.

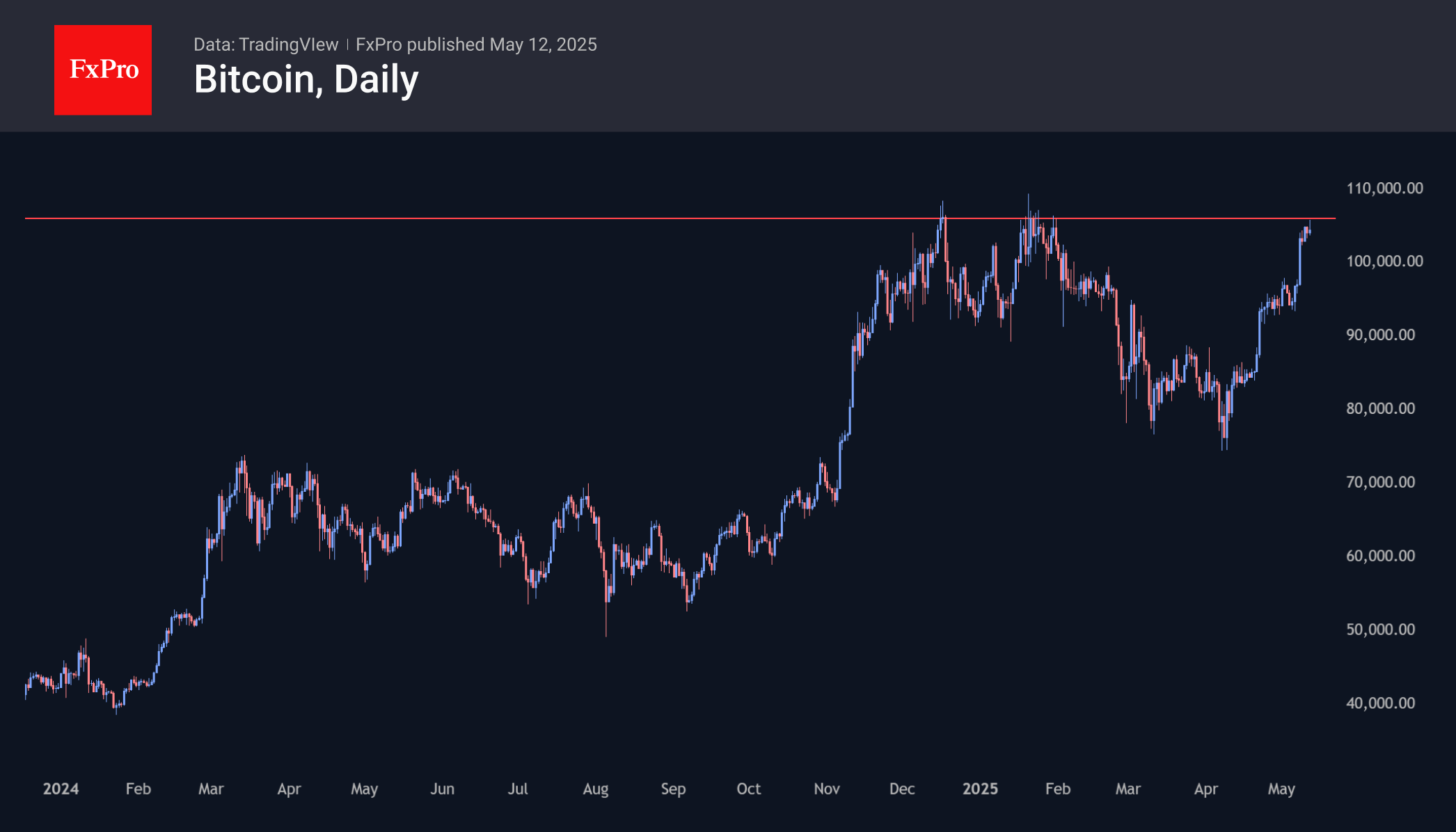

Bitcoin rallied above $105.5k on Monday morning, entering the area of highs where it has twice failed to hold over the past six months. The impressive corrective pullback from late January to early April, in our opinion, created substantial margin for a new wave of growth. Therefore, we will not be surprised if, along with the positive dynamics of stocks, BTCUSD will move to the renewal of historical highs already this week.

News Background

On the weekly bitcoin chart, after the upward breakout of the ‘bull flag’ pattern, a further rise to $182,000 is possible, given the growth before the downward consolidation. Cointelegraph presented such a scenario.

Significant inflows into spot bitcoin ETFS in the US continued for the third week in a row. According to SoSoValue data, weekly net inflows into spot BTC-ETFS totalled $921 million, bringing the total to $41.16 billion since bitcoin-ETFS were approved in January 2024.

Inflows into spot Ethereum-ETFS in the US broke after two weeks, recording a small net outflow of $38.2 million to $2.47 billion since last July.

Cryptoquant noted that the strategy firm’s pace of bitcoin purchases exceeds the rate at which miners are issuing new coins. The firm’s holdings alone imply an annual deflation of the asset of 2.23%.

Public mining companies sold about 70% of mined Bitcoins in April against a falling mining profitability, TheMinerMag calculated. Since March, miners seemed to be moving away from the HOLDing strategy that had prevailed last year.

Over the years, Coinbase has considered investing a significant portion of its savings in bitcoin, following the example of Strategy, but abandoned the idea because of the risks, said Brian Armstrong, head of the exchange.