Sample Category Title

BoE’s Greene says trade risks justify rate cut

BoE MPC member Megan Greene said during a panel discussion today that while wages and inflation are moving in the right direction, they remain uncomfortably high. and more concerningly, "medium-term inflation expectations have also started picking up."

Greene, who voted with the majority last week in favor of a 25bps rate cut, the fourth since last August, revealed that she was initially undecided going into the meeting.

She noted being “torn” between holding rates steady and cutting, but ultimately decided to support easing. A key factor in her decision was the rise in global trade tensions, driven by US President Donald Trump’s sharp tariff hikes.

Despite the subsequent temporary trade truce between the US and China announced today, Greene said it would not have changed her vote.

She also flagged continued uncertainty over US-EU trade relations as a key downside risk for the UK economy, noting that any escalation could further dampen external demand.

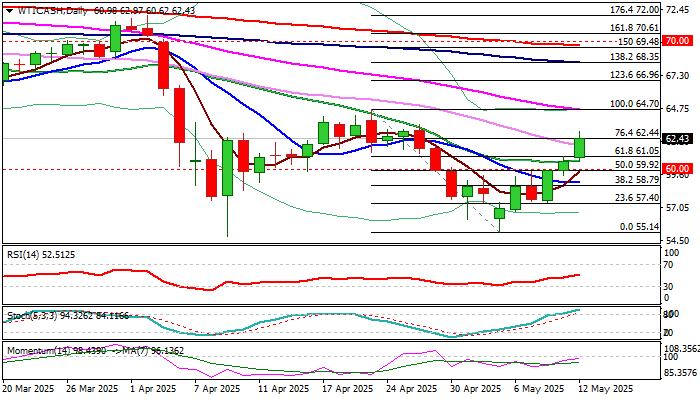

WTI: Oil Price Rises Further as Positive Moves in US-China Trade Talks Improve the sentiment

WTI oil price jumped over $2 on Monday following success of US-China trade talks over the weekend that eased tensions and signaled that world’s two largest oil consumers are on the way to resolve their trade conflict.

The markets welcomed positive move that significantly brightened the demand outlook and further lifted oil price.

The WTI contract resumed strong rally of the last week (up almost 8%) on Monday and hit the highest in two weeks, marking retracement of over 76.4% of $64.70/$55.14 bear leg.

Bulls focus target at $63.55 (Apr 28 high) the last obstacle en-route to $64.70 breakpoint (Apr 24 high), violation of which to generate reversal signal on completion of daily bullish failure swing pattern.

However, a pause in current rally (due to overbought conditions and 14-d momentum indicator being still in negative territory) may precede fresh push higher, with shallow dips to ideally find ground at $61.00 zone and offer better levels to re-enter bullish market.

Only loss $60 pivot, which previously marked strong barrier and now reverted to solid support, would sideline bulls.

Res: 62.97; 63.55; 64.70; 65.00.

Sup: 61.90; 61.05; 60.71; 60.00.

US-China: Trade Talks Succeed in De-escalation

US-China trade talks over the weekend developed more positively than both we and consensus expected. Below we give a short overview of what happened and the implications in US and China, respectively.

What it means for the US

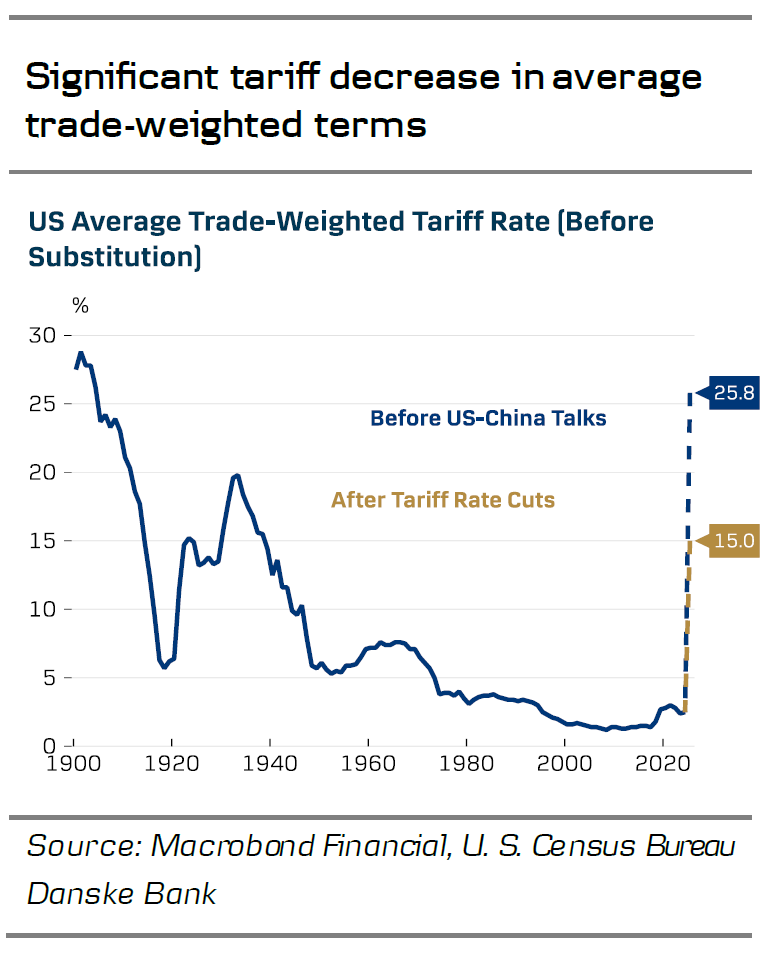

While both US and Chinese officials had signalled a positive outcome from the Geneva negotiations already on Sunday, the cuts to tariff rates were larger than we had anticipated. Treasury Secretary Scott Bessent announced a 115%-point reduction to the previous rate of 145%, which would take the rate close to pre-Liberation Day level of 30%. Previously, our baseline scenario included a cut down to 60%. The cuts are initially in effect for 90 days, as was the case with the delay of other reciprocal tariffs as well.

Before Trump entered the office, the average tariff rate on Chinese goods imports was around 10-12%. And already before the Liberation Day, the rate was increased twice by 10%-points at a time as part of the so-called 'Fentanyl tariffs'.

For estimating the economic impact, we are going to assume a tariff rate of 30%. It is not immediately clear for us if the 10% universal tariff also applies on top of the pre-Trump rates and the Fentanyl tariffs. This means the rate could be slightly higher around 40-42%.

Before today's announcements, the average tariff rate on all US imports was around 25.8%. Cutting the Chinese rate to 30% reduces the average rate by more than 10%-points to around 15%. The Tax Foundation estimated earlier, that without reductions, the tariffs would weigh on US GDP by around 0.8% or 1.0% including retaliation. After today's announcements, the expected negative impact on US GDP could be nearly halved to only around 0.5%.

It is worth noting that consensus forecast for US GDP growth in 2025 had already been downgraded from 2.2% to 1.4% after the Liberation Day, reflecting a negative impact of 0.8%. Hence, if made permanent, today's tariff announcements could pose upside risks to current consensus growth outlook. While the easing does not naturally alleviate all of the negative consequences already seen in international trade and consumer/business sentiment, in our view today's announcement significantly reduces the risk of an outright recession down the line.

What it means for China

From a Chinese perspective the talks were also a success. China had several goals met:

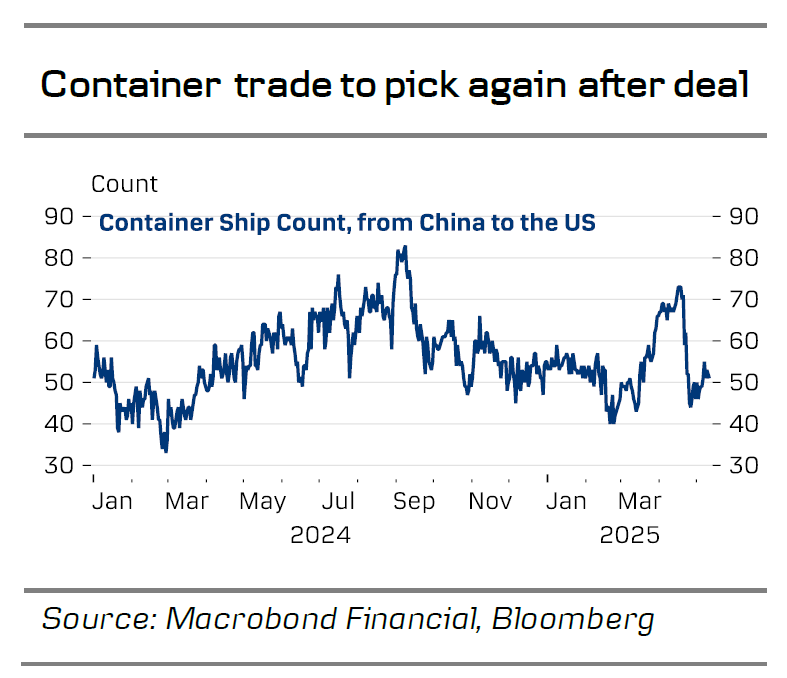

First and foremost, tariff rates have been significantly reduced, which means trade can resume and Chinese companies exporting goods for Halloween, Christmas, Black Friday etc. can ship their goods at tariff rates that are manageable. China could soon see tariff rates reduced by a further 20% if they strike a deal on Fentanyl, which seems likely based on positive comments from Bessent on China's efforts to meet the US on this point.

With tariff rates significantly lower, the Chinese growth outlook for the coming quarters looks a lot better.

Second, negotiations according to the Chinese delegation happened in a good atmosphere with mutual respect, sincerity and understanding for the other side. These are key points for China and often underestimated. And in China it vindicates that the initial strong retaliation has paid off with the US showing more respect now instead of bullying. People matter in diplomacy and Bessent and Greer seem to be the right people at the table. You can disagree and have demands but if you show respect and understanding, it is much easier to get results when dealing with China.

Second, negotiations according to the Chinese delegation happened in a good atmosphere with mutual respect, sincerity and understanding for the other side. These are key points for China and often underestimated. And in China it vindicates that the initial strong retaliation has paid off with the US showing more respect now instead of bullying. People matter in diplomacy and Bessent and Greer seem to be the right people at the table. You can disagree and have demands but if you show respect and understanding, it is much easier to get results when dealing with China.

Where to go from here?

US-China talks are set to continue over the coming months. One of the tracks are related to Fentanyl and could very well lead to a further reduction in US tariffs on China by 20%- points. In the medium to longer term, trade talks will likely take time and could easily face bumps on the road due to disagreements on industrial policy, Chinese purchases of US goods etc.

It is worth keeping in mind that achieving significant reductions in US trade deficit with China, which remains a high priority for the US side according to Greer, appears unlikely without a significant reduction in US demand. During Trump’s 1st term, China failed to reach the levels of US goods purchases outlined in the so-called ‘Phase One’ trade deal agreed in 2019, and achieving a deal that satisfies all demands for both sides will be difficult to reach this time around as well – especially within the timeframe of only 90 days. However, it now seems more likely we could end up close to our original baseline scenario where US tariff rates on China are ultimately around 40%. A headwind but manageable for both sides.

Market implications

The agreement has fuelled a rally in global stocks, higher yields and a decline in EUR/USD and USD/CNY. The move reflects lower perceived risk of a US-driven growth slowdown, and was also evident in oil prices ticking higher. In the short-end of the USD curve, markets now price in only a 10% chance of the Fed cutting rates in June, and the next 25bp rate cut is fully priced in only by the September meeting. With trade talks on a better footing, macro data will likely start to matter more for market developments in the coming months – not least US data.

Gold Drops to 3,273 USD as Markets Await Trade Deal Developments

The price of a troy ounce of gold fell to 3,273 USD on Monday, losing about 1% compared to the previous session’s level.

Key factors driving gold’s movement

The primary reason for the decline is positive signals regarding trade talks between the US and China, which have reduced the demand for safe-haven assets.

Negotiations between representatives of the two countries concluded over the weekend, and the results offer some grounds for optimism. Beijing announced plans to initiate formal talks, while Washington reported progress towards an agreement.

US Treasury Secretary Scott Bessent stated that he could provide further details at a full briefing on Monday. Today's developments are expected to generate significant market reactions.

Geopolitically, the ceasefire between India and Pakistan remained in place until Sunday, despite mutual accusations of violations shortly after its conclusion.

Earlier, additional pressure on gold came from statements made by the Federal Reserve. The regulator warned of rising inflation and risks within the labour market. At the same time, Chairman Jerome Powell ruled out the possibility of a pre-emptive rate cut in response to tariff threats.

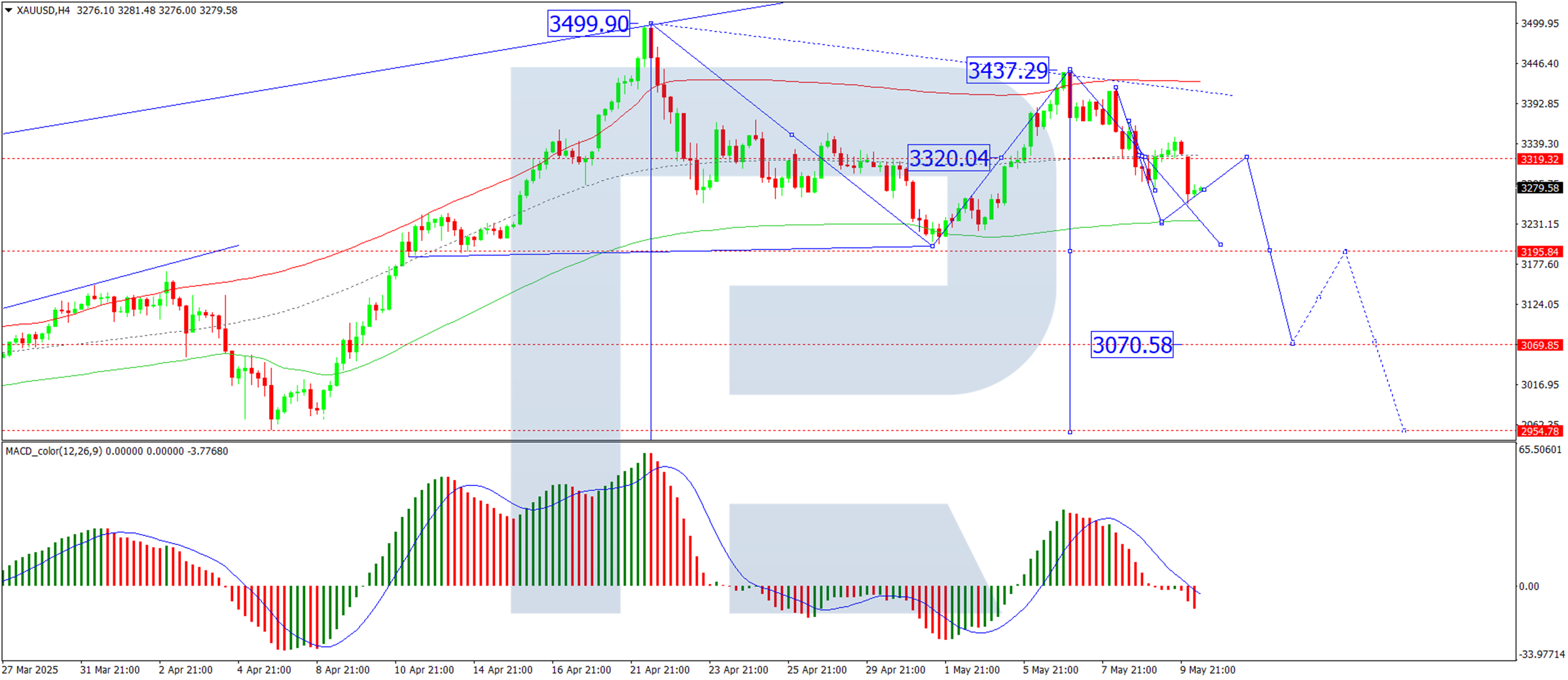

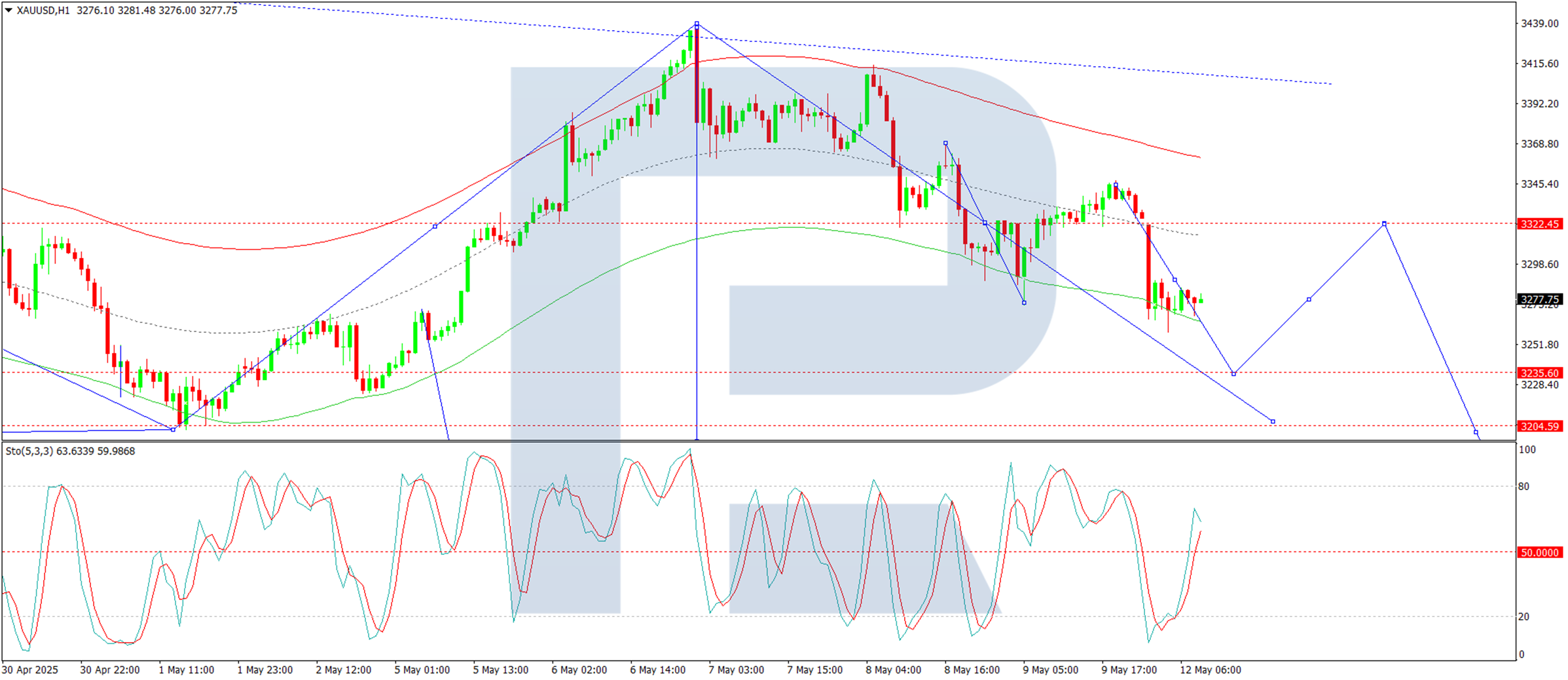

Technical analysis: XAU/USD

On the H4 chart, XAU/USD has formed a consolidation range around the 3,322 level. Today, we expect a possible decline to 3,195. After reaching this target, a correction to the 3,255 level is possible. Upon completing this correction, a new wave of decline to the local target of 3,070 may follow. Technically, this scenario is confirmed by the MACD indicator, as its signal line is below the zero level and is pointed decisively downwards.

On the H1 chart, XAU/USD has broken below the 3,290 level and continues to move towards 3,235. This target level will likely be reached today. A corrective move towards the 3,322 level cannot be ruled out. Subsequently, a decline to at least 3,200 is expected. Technically, this scenario is confirmed by the Stochastic oscillator; its signal line is below the 80 level and is directed steadily downwards towards the 20 level.

Conclusion

Gold remains under pressure amid improving trade sentiment and hawkish commentary from the Fed, with technical indicators pointing to further downside potential. Traders will be closely watching today’s briefing for any new market-moving details.

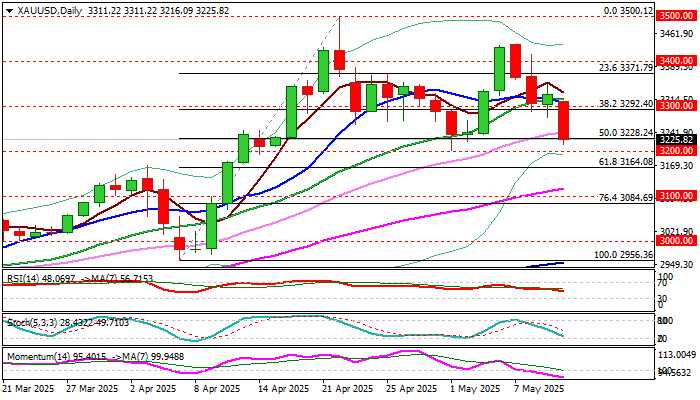

XAU/USD: Gold Price Tumbles as Waves of Fresh Optimism Fade Safe-Haven Demand

Gold price fell around 2.5% at the start of the week, as positive news (US-China trade deal / India – Pakistan ceasefire) dominated in early Monday and strongly contributed to fading safe haven demand.

Fresh optimism that disastrous scenario of escalation of trade war between world’s two largest economies has been avoided, lifted US dollar and pushed metal’s price to the lowest in almost two weeks.

All eyes are now on potential direct peace talks between Russia and Ukraine, with any signs of progress to further deflate gold price.

Positive signal on clear break of pivotal $3300 support zone (psychological / Fibo 38.2% of $2956/3500 upleg) weakened near-term structure, as negative momentum strengthened further and 10/20DMA’s formed bear cross.

Bears cracked next significant support at $3228 (Fibo 50% / daily Kijun-sen) and eye breakpoint at $3200 (floor of consolidation range under new record high), break of which to complete a failure swing pattern on daily chart and generate stronger reversal signal.

However, headwinds at $3200 zone can be expected, due to significance of support, with limited upticks likely to mark positioning for fresh acceleration of pullback from $3500 (new record high), if current factors that drive gold price persist.

Broken $3292/$3300 supports reverted to solid barriers which should cap potential stronger upticks and keep bears in play.

Break of $3200 trigger to unmask targets at $3164 (Fibo 61.8%), $3100 (round-figure) and $3084 (Fibo 76.4% of $2956/$3500).

Res: 3242; 3265; 3292; 3310.

Sup: 3200; 3164; 3116; 3100.

Risk Assets Rise Following US-China Talks, Gold Slides, DAX Fresh Highs

US stock futures climbed, and the dollar gained after China and the US made strong progress in trade talks, fueling hope that tensions will ease.

A regional stock index rose 0.7%, with the Hang Seng Index up for the eighth straight day, marking its best streak in a year. S&P 500 futures increased 1.5%, Nasdaq 100 jumped 2%, and European futures rose 0.8%.

Global bonds fell as Treasury yields rose and European debt futures dropped. Stocks in India climbed 3%, while those in Pakistan surged 9% after the two nations agreed to a ceasefire.

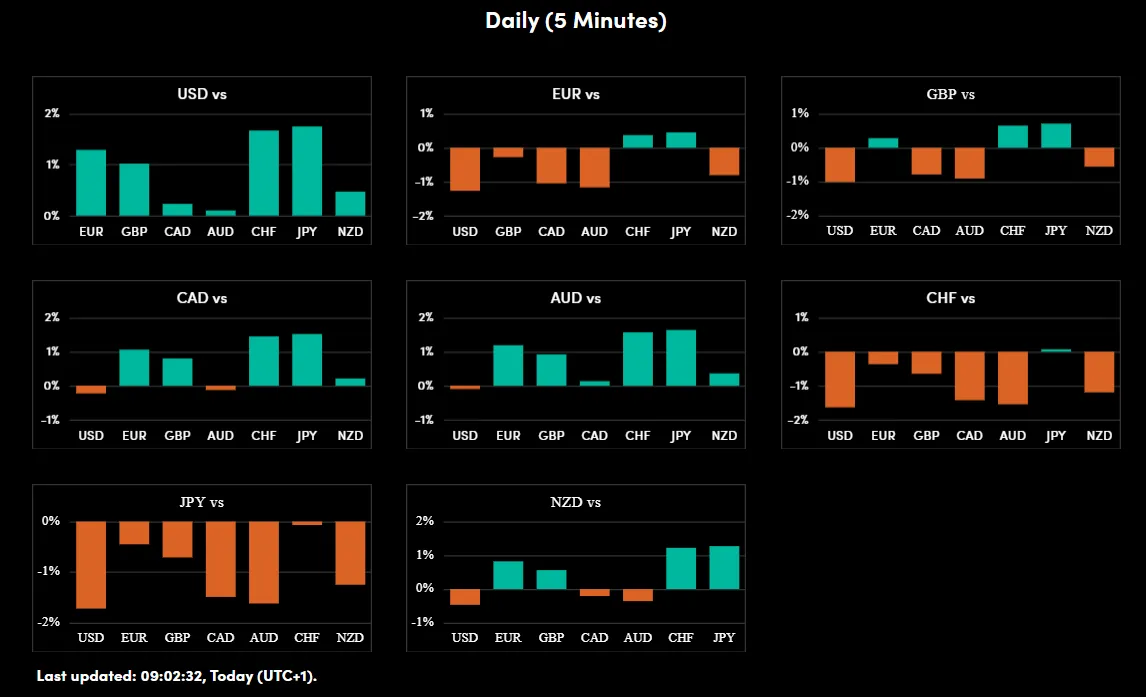

On the FX front, safe havens are struggling this morning as optimism over a trade deal. The dollar rose 0.4% to 145.93 yen and 0.5% to 0.8337 Swiss francs.

The dollar index stayed steady near a one-month high but remained 3.6% lower since the April 2 announcement of Trump’s "Liberation Day" tariffs.

The New Zealand dollar rose 0.3% to 0.5927, and the Australian dollar also gained 0.3% to 0.6432. Meanwhile, the euro dropped 0.2% to 1.1228, and the British pound fell 0.3% to 1.3288.

Currency Strength Chart:

Source: OANDA Labs Blog

US-China trade talks

China's Vice Premier He Lifeng called the weekend talks with US officials “an important first step” toward improving trade relations.

Though no specific actions were announced on Sunday, Lifeng said both sides agreed to set up a system for future discussions, to be led by US Treasury Secretary Scott Bessent and himself. Bessent promised more details and a joint statement on Monday.

Lifeng stressed that China-U.S. trade is about mutual benefits, rejecting the idea that one side must lose for the other to win. He said China is ready to work with the US to handle differences, strengthen collaboration, and “expand shared opportunities.”

Markets are likely to take cues from developments around the US-China talks and any announcements that are forthcoming. US Treasury Secretary Bessent to brief on China talks at 3AM EST, according to US Officials.

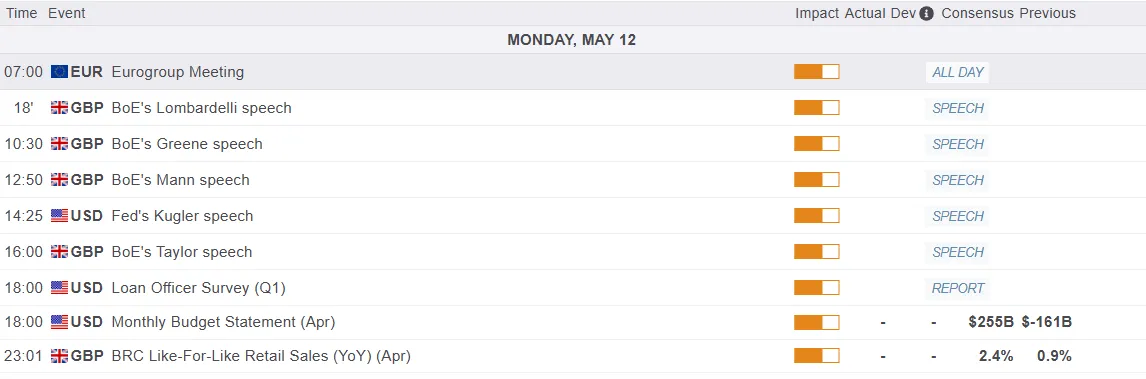

Economic data releases

From a data standpoint, it is a quiet start to the week. The biggest highlights will come from the Bank of England Bank Watchers conference 2025 at King’s Business School.

We will hear from BoE policymakers Lombardelli and Green who are both speaking at the event.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the day - DAX

From a technical standpoint, the DAX has gapped up over the weekend and pushed to within a whisker of the 24000 handle.

The DAX index has now printed all-time highs but with a lack of historical price action, technical analysis remains somewhat of a challenge.

I will be paying attention to psychological level and round numbers which tend to illicit a response.

Resistance ahead may be found at 24250 and 24500.

Immediate support rests at 23471 and 23212 respectively.

DAX Daily Chart, May 12, 2025

Source: TradingView.com (click to enlarge)

BoE’s Lombardelli: Gradual cuts warranted as wage and services inflation stay high

BoE Deputy Governor Clare Lombardelli reinforced the case for a "gradual and careful" approach to policy easing in a speech today. She noted underlying inflation "have continued to fall" despite noises. Monetary policy is still restrictive and will continue to balance the need to lower inflation with the risk of undermining already soft demand.

Lombardelli highlighted wage growth as a central focus in the disinflation process, particularly given its outsized influence on domestic services pricing. She noted that private sector regular average weekly earnings rose 5.9% in February, still well above levels consistent with BoE’s inflation target. Services inflation, a key proxy for persistent price pressure, remains elevated at 4.7% as of March. Both indicators suggest that while progress has been made, inflationary momentum in wage-sensitive sectors continues to pose a challenge.

She also addressed the global backdrop, warning that higher US tariffs and increasingly uncertain American trade policy could lower growth and inflation in the short term by dampening global demand and trade volumes. However, over the longer term, if trade fragmentation continues, it could "reduce output and productivity and would raise inflationary pressures."

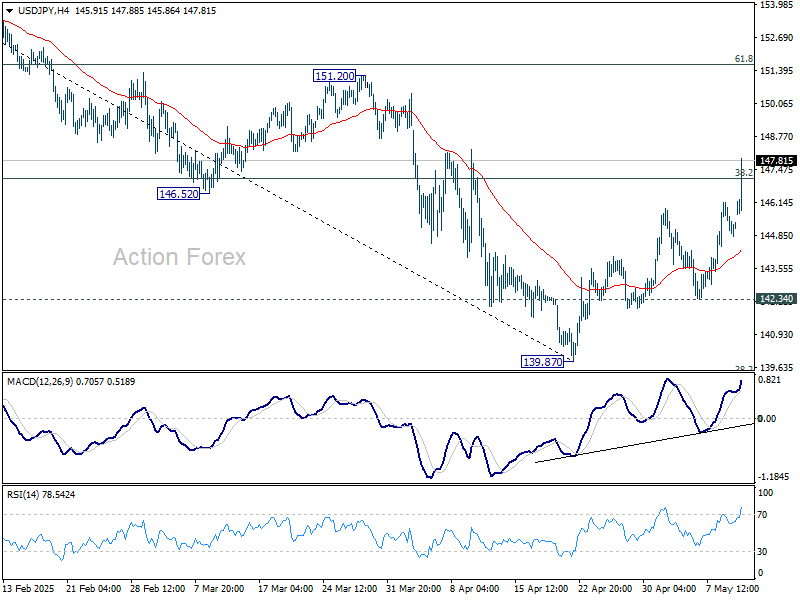

US-China suspend reciprocal tariffs in breakthrough, USD/JPY heading back to 150

Dollar surges sharply alongside strong gains in US equity futures, following the official confirmation of a major breakthrough in trade talks between the US and China. Both sides have agreed to suspend most of the tariffs imposed on each other’s goods, cutting “reciprocal” duties from 125% to just 10%.

However, the US will retain a 20% tariff on Chinese imports related to fentanyl, leaving total effective tariffs on China at 30%. The move marks a significant de-escalation in trade tensions.

The agreement was reached over the weekend during negotiations in Switzerland, and both countries stated they will continue talks on economic and trade matters in the coming weeks.

USD/JPY soars through 38.2% retracement of 158.86 to 139.87 at 147.12. The development now suggests that fall from 158.86 has already completed at 139.87, just ahead of 139.57 (2024 low). Further rally should be seen to 61.8% retracement at 151.60 next.

AUD/USD and NZD/USD Ready to Climb Again

AUD/USD is attempting a fresh increase from the 0.6370 support. NZD/USD is also rising and could aim for a move above the 0.5945 resistance.

Important Takeaways for AUD/USD and NZD/USD Analysis Today

- The Aussie Dollar found support at 0.6370 and recovered higher against the US Dollar.

- There was a break above a key bearish trend line with resistance at 0.6410 on the hourly chart of AUD/USD at FXOpen.

- NZD/USD is consolidating above the 0.5915 support.

- There was a break above a connecting bearish trend line with resistance at 0.5910 on the hourly chart of NZD/USD at FXOpen.

AUD/USD Technical Analysis

On the hourly chart of AUD/USD at FXOpen, the pair formed a base above 0.6420. The Aussie Dollar started a decent increase above the 0.6450 resistance against the US Dollar, as mentioned in the previous analysis.

The pair even cleared 0.6500 before there was a minor pullback. The recent low was formed at 0.6370 and the pair is again rising. The bulls pushed the pair above the 23.6% Fib retracement level of the downward move from the 0.6514 swing high to the 0.6370 low.

Besides, there was a break above a key bearish trend line with resistance at 0.6410. The pair is now consolidating above the 50-hour simple moving average. On the upside, the AUD/USD chart indicates that the pair is now facing resistance near the 0.6440 zone.

The first major resistance might be 0.6460 and the 61.8% Fib retracement level of the downward move from the 0.6514 swing high to the 0.6370 low. An upside break above the 0.6460 resistance might send the pair further higher. The next major resistance is near the 0.6515 level. Any more gains could clear the path for a move toward the 0.6550 resistance zone.

If not, the pair might correct lower. Immediate support sits near the 0.6410 level. The next support could be 0.6370. If there is a downside break below the 0.6370 support, the pair could extend its decline toward the 0.6320 zone. Any more losses might signal a move toward 0.6300.

NZD/USD Technical Analysis

On the hourly chart of NZD/USD on FXOpen, the pair also followed AUD/USD. The New Zealand Dollar formed a base above the 0.5900 level and started a decent increase against the US Dollar.

The pair climbed above the 0.5980 resistance. It tested the 0.6020 resistance before there was a pullback. The recent low was formed at 0.58704 and the pair is again rising above the 50-hour simple moving average.

There was a break above a connecting bearish trend line with resistance at 0.5910. The pair cleared the 0.5915 resistance and the 23.6% Fib retracement level of the downward move from the 0.6022 swing high to the 0.5870 low.

The NZD/USD chart suggests that the RSI is back above 50 signaling a positive bias. On the upside, the pair is facing resistance near the 50% Fib retracement level of the downward move from the 0.6022 swing high to the 0.5870 low at 0.5945.

The next major resistance is near the 0.5985 level. A clear move above the 0.5985 level might even push the pair toward the 0.6020 level. Any more gains might clear the path for a move toward the 0.6050 resistance zone in the coming days.

On the downside, there is a support forming near the 0.5915 zone. If there is a downside break below the 0.5915 support, the pair might slide toward 0.5870. Any more losses could lead NZD/USD in a bearish zone to 0.5810.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Cautiously Positive Momentum Can Be Maintained

Markets

Markets of late gradually faced something what, with some exaggeration, one can label as ‘tentatively reflationary vibes’. For now, hard (US) eco data, despite the post-liberation Day trade escalation held up fairly well (US payrolls, GDP, but also the likes of the EMU Q1 GDP). This allowed central bankers (Fed, BoE and several others) to hold a guarded, gradual approach on further easing. The first US trade agreement with UK last week also reinforced the feeling that US trade policy entered some kind of de-escalation phase, with markets looking forward to first high level talks between US and Chinese officials in Switzerland this weekend. Moves on yield markets on Friday were limited (US yields changed less than 2 bps across the curve), but the broader bottoming pattern was confirmed. ECB policymakers in their communication of late focused more on the potential deflationary impact of the trade conflict, suggesting room for some further easing. However, given markets already discounting an ECB depo rate below 1.75%, there was also room for some bottoming. German yields on Friday added between 1.2 bps (2-y) and 3.0 bps (30-y). The bottoming out narrative from yield markets to some extent spilled over to the dollar. The US currency last month was a major victim of the trade disruption, which was seen as raising the risk of a US recession. Uncertainty on what will happen in H2 remains elevated, but data showing some resilience and the Fed for now in no hurry to remove interest rate support provided some support even as USD momentum remains tepid, to say the least. On Friday, with little high profile data or headline news, the dollar lost marginally (close DXY 100.34, EUR/USD 1.125). Still, the US currency as a trend further left the April lows behind.

At the start of the new trading week, it looks that the cautiously positive momentum can be maintained as China and the US reported ‘substantial progress’ after the talks in Switzerland during the weekend. They provided no concrete details on any reduction in tariffs yet, but negotiators said to have agreed on a mechanism for further talks. Additional communication is said to come later today. Most Asian markets show modest gains of about 0.5% -1.0%. The ceasefire in the conflict between India and Pakistan might be a positive for regional markets, too. US yields are adding 3-4 bps across the curve. US equity futures gain 1.0%-2.0%. The dollar also again shows cautious gains (EUR/USD 1.1215, USD/JPY 146.1). Today’s eco calendar in the US and EMU is almost empty. So the focus will remain on progress in trade talks between the US and China (and/or other trading partners). Later this week, the US April CPI (Tue), retail sales (Thu) and Michigan confidence (Fri) deserves attention. Unless these data show an unexpected substantial setback, the bottoming out process in US yields and the dollar might continue. This might also apply to German yields. In this respect, the concrete implementation of the fiscal plans of the new German government gradually might get some more attention after the risk driven rally of Bunds post Liberation Day.

News & Views

The downturn in UK hiring activity eased in April according to the latest KPMG & REC UK report on jobs. Both permanent placements and temp billings fell at softer rates compared to March amid reports of weak employer confidence and tighter hiring budgets. Recruiters signaled a further marked drop in demand for workers (18th consecutive month) which, alongside redundancies, drove another rapid increase in candidate availability (2nd sharpest pace since December 2020). Turning to pay, stronger than average increases in the national minimum and living wage rates underpinned the quickest temp pay for nearly a year. Starting salaries increases again, but remain below the long term average pace of growth. REC commented that “the biggest single drag factor on activity right now is uncertainty, some of which can’t be helped but payroll tax costs and regulation design is in the Government’s gift”.

Chinese consumer prices rose by 0.1% M/M in April, to be down on an annual basis for a third consecutive month (-0.1% Y/Y). Details showed core inflation rising by 0.5% Y/Y and services prices by 0.3% Y/Y while goods deflation was extended with a 0.3% annual drop. Food prices, which have a heavy weight in the price basket, “only” fell 0.2% Y/Y (down from 1.4% in March). Factory gate deflation persisted for a 31st month with producer prices falling by 2.7% Y/Y. Supply keeps outstripping demand with government and PBOC easing actions in the trade war aimed to at least partly restore the balance. Those effects might only start showing in Summer though.