Sample Category Title

This Week Concludes With US Consumer Sentiment

In focus today

In the US, we await the preliminary May consumer sentiment survey from University of Michigan, which will provide markets with the latest sense of how consumers are feeling after the tariffs took effect. Earlier surveys have shown a sharp deterioration in future expectations and rapid upticks in inflation expectations.

In the euro area, the European Commission had scheduled to publish its spring economic forecast today, but the publication has been rescheduled for Monday following the trade war de-escalation between the US and China.

In China, early Monday, April's monthly data including retail sales, housing data and industrial production will be released. The month marks the trade escalation, making it crucial to observe any impact on consumption etc. Consensus looks for broadly unchanged growth in retail sales around 6% y/y. The housing market shows a decline in home prices but moderate improvement in home sales. These figures are somewhat outdated, as they precede the US-China trade deal on 11-12 May. We look for a decent recovery in China soon, as front-loading by US importers is set to give a big boost to Chinese exports over the next three months.

Have a great Friday and weekend!

Economic and market news

What happened overnight

In Japan, Q1 national account data reveals a sharper-than-expected decline in GDP at -0.2% q/q (cons: -0.1%), with lower external demand at -0.8% and stagnant consumption, which accounts for more than half of Japan's GDP, in the driver's seat. Capital spending rose by 1.4% q/q, surpassing the consensus of 0.8%. The figures mark the economy shrinking for the first time of the year, underscoring the fragile recovery and complicating the BoJ's rate hike path.

What happened yesterday

In the US, yesterday's data revealed m/m declines in core PPI and control group retail sales, with mixed signals from manufacturing data: the Philly Fed rebounded strongly, but the NY Fed's Empire Index continued to decline. Retail sales details were also mixed, suggesting that the weak retail sales may be a reversal of front-loading effects rather than true underlying weakness. The negative core PPI reading was due to weak services price pressures, while core goods inflation modestly accelerated due to tariffs. Overall price pressures thus seem to remain controlled. Markets reacted by sending yields modestly lower.

Moreover, the budget committee of the US House of Representatives is expected to finalize the reconciliation bill today, combining the extensions to Trump's 2017 tax cuts with other budget changes. The first vote on House floor will most likely take place already this month, but passing the bill through House and Senate is expected to be challenging.

Meanwhile, Fed Chair Jerome Powell opened a two-day conference to reassess the Fed's monetary policy framework, acknowledging the need for adaptation due to more frequent supply shocks and inflation trends.

In the euro area, employment continued to grow in the first quarter of the year, rising 0.3% q/q after growing 0.1% q/q in Q4 2024. Hence, the labour market remains on the strong footing it has been on in the past years despite weak economic activity. The strong labour market is a hawkish argument for the ECB.

Alongside the employment data we also got the second estimate of growth in Q1, which showed GDP rising 0.3% q/q compared to the 0.4% q/q in the first estimate. However, the revision was mainly due to rounding when evaluating the second decimal.

In Norway, mainland GDP rose by 1.0% q/q in Q1, surpassing consensus and Norges Bank's forecast in March, both at 0.6%. Private consumption increased by 1.5% q/q, corporate investments by 1.1% q/q, and residential investments by 0.4% q/q. Despite a drop in public investment and oil investments, the strong figures question the necessity for rate cuts. However, improvements in rate-sensitive sectors may reflect expectations of a rate cut in March that was never delivered. Monthly figures reveal a slowdown during Q1, with January at 1.2 % m/m, February 0.1 % m/m, and March at -0.2 % m/m.

The revised fiscal budget figures showed an increase in spending at 2.7% of the oil fund equity, aligning with Norges Bank's estimates. Support packages for Ukraine contribute to lifting spending to NOK 542.2bn, delivering a substantial fiscal impulse of 2.5%. Much of this spending is unlikely to directly impact the mainland economy.

In Sweden, inflation expectations decreased in April, with CPIF projections returning to 2.1% for both the one- and two-year horizons. The crucial five-year expectation, previously at 2.3% last month, has now aligned with the inflation target of 2%. Overall, this is a positive reading for the Riksbank, with inflation expectations presenting no obstacle should they decide to cut rates in the coming months.

In geopolitics, Russian delegation head Vladimir Medinsky announced that talks with Ukraine will start this morning in Istanbul. Zelenskiy criticised Putin's absence, and the US expressed low expectations for the talks until a meeting occurs between Trump and Putin.

Equities: Equities drifted gradually higher, with some interesting dynamics. Major indexes were 0.5-1% higher, but underlying sectors and style preferences flipped around. Equal weighted S&P 500 outperformed S&P 500 and Europe outperformed US. Interestingly, this happened despite yields plunging 5-10bp, which would normally result in US outperformance. Moreover, it was a defensive comeback, with utilities, consumer staples and real estate outperforming the Mag Seven. Some context is warranted: defensive sectors have lower valuation multiples than in April while cyclical sector valuation has fully recovered. This is not very intuitive and speaks for catch-up in those names, just like the session yesterday. Futures are little changed this morning while Asian stocks are retreating after a strong week.

FI&FX: The last 24 hours have been characterised by broad-USD and NOK weakness while the JPY and CHF have enjoyed souring risk appetite. Softer US figures contributed to sending USD rates meaningfully lower for the first time in a week with the US 10Y Treasury yield back close to 4.40. The EUR curve flattened driven by the long end while Scandi rates generally underperformed. BTP-Bund spreads continue to tighten while Treasury ASW spreads have been stable in recent sessions.

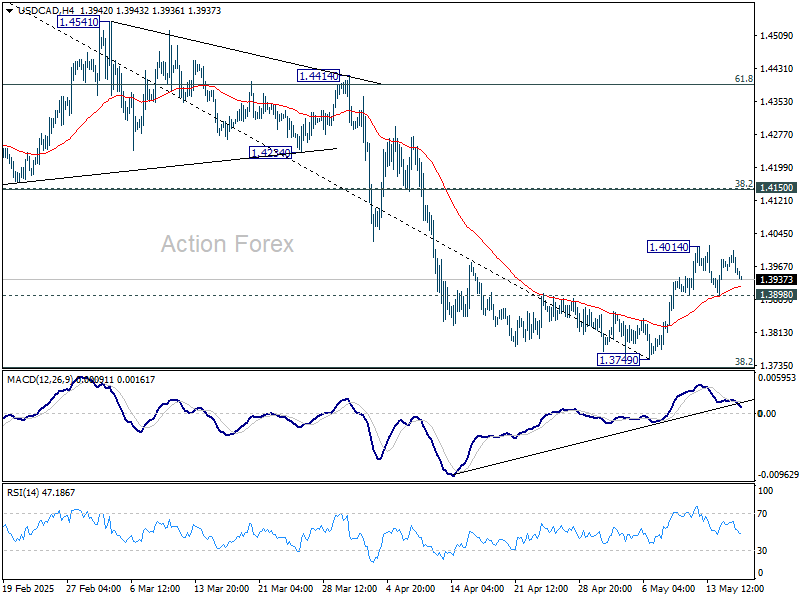

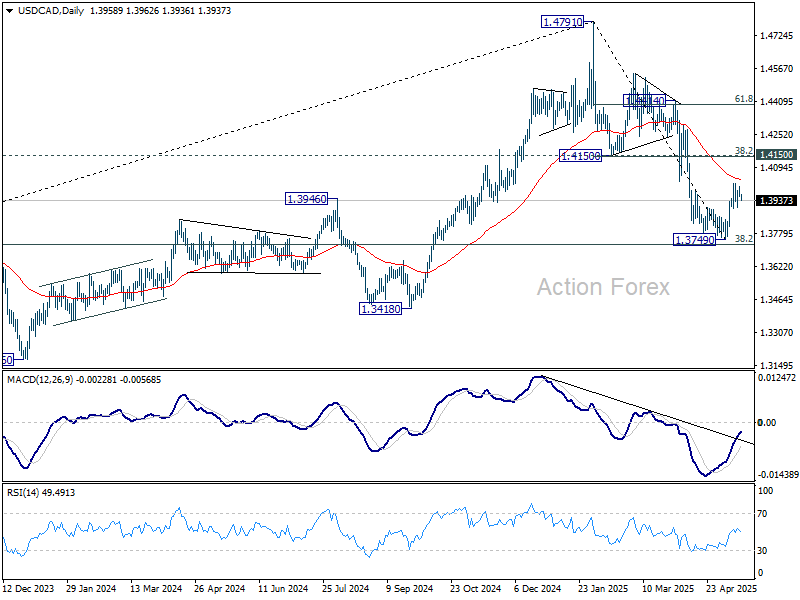

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3942; (P) 1.3973; (R1) 1.3991; More...

Intraday bias in USD/CAD stays neutral a this point. Further rise is in favor with 1.3898 minor support intact. Above 1.4014 will resume the rebound from 1.3749 to 1.4150 cluster resistance (38.2% retracement of 1.4791 to 1.3749 at 1.4147). However, break of 1.3898 minor support will indicate that the rebound has completed, and bring retest of 1.3749.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4150 resistance turned support holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

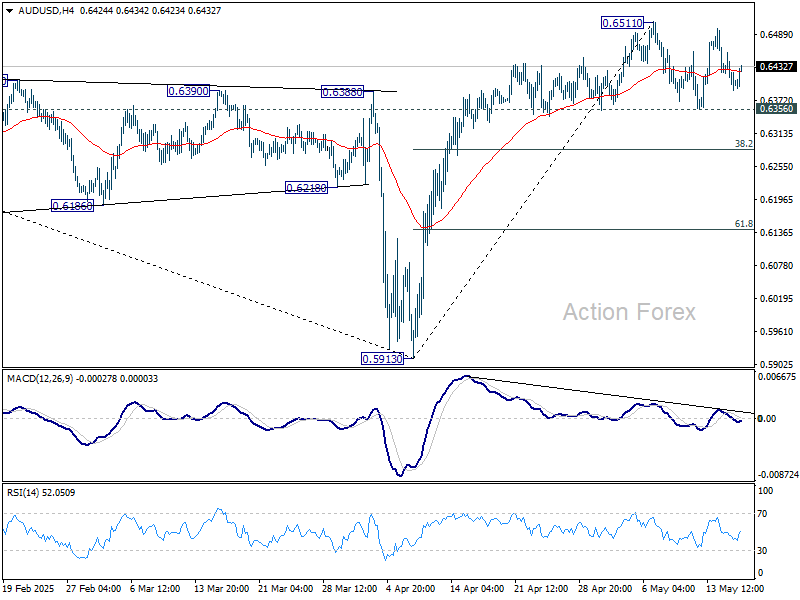

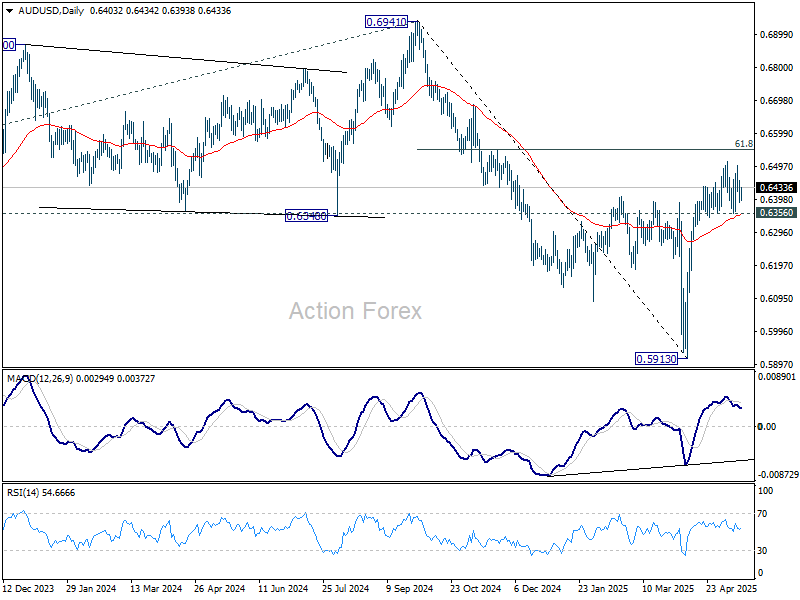

AUD/USD Daily Report

Daily Pivots: (S1) 0.6379; (P) 0.6418; (R1) 0.6446; More...

Intraday bias in AUD/USD remains neutral for the moment. On the upside, firm break of 0.6511 will resume the rally from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, break of 0.6356 will bring deeper pullback to 38.2% retracement of 0.5913 to 0.6511 at 0.6283.

In the bigger picture, as long as 55 W EMA (now at 0.6441) holds, down trend from 0.8006 (2021 high) should resume later to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

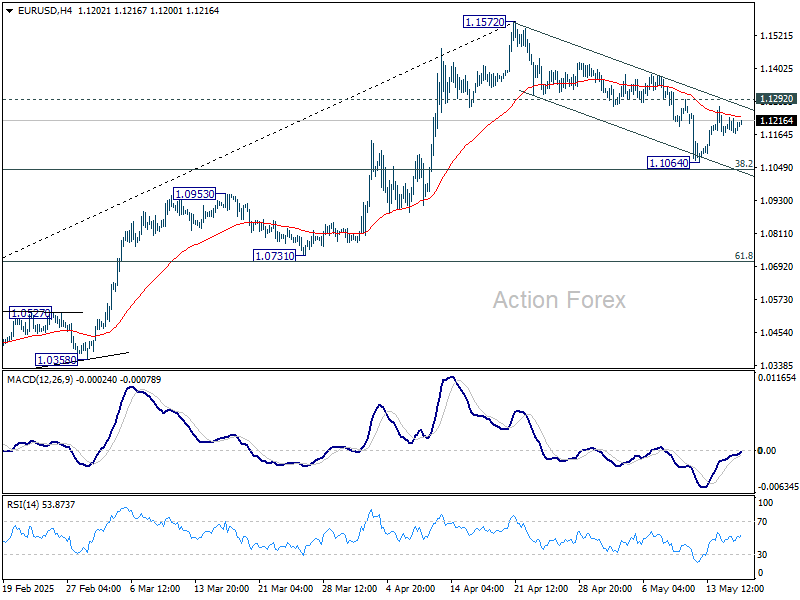

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1157; (P) 1.1192; (R1) 1.1220; More...

Intraday bias in EUR/USD remains neutral for the moment. On the upside, break of 1.1292 resistance will argue that correction from 1.1572 has completed after defending 38.2% retracement of 1.0176 to 1.1572 at 1.1039. Intraday bias will be back on the upside for retesting 1.1572. However, sustained break of 1.1039 will dampen this view and target 61.8% retracement at 1.0709 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0789) holds.

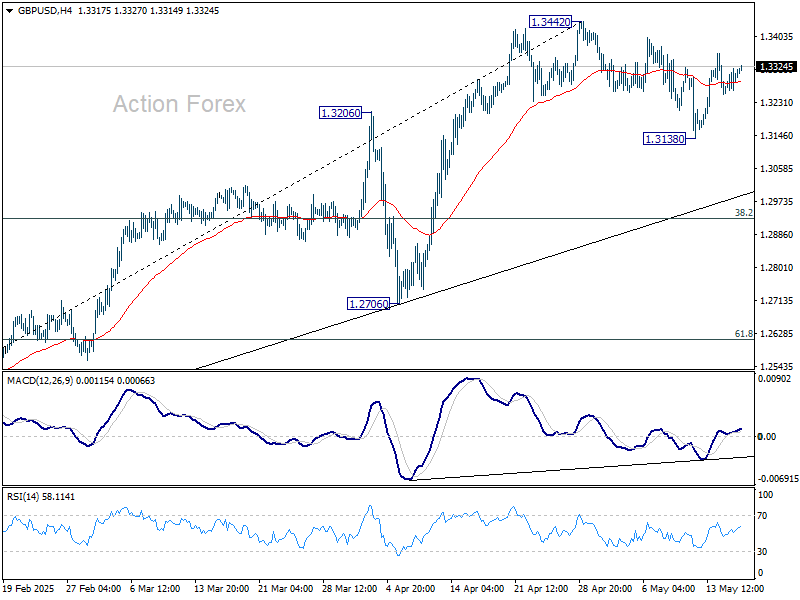

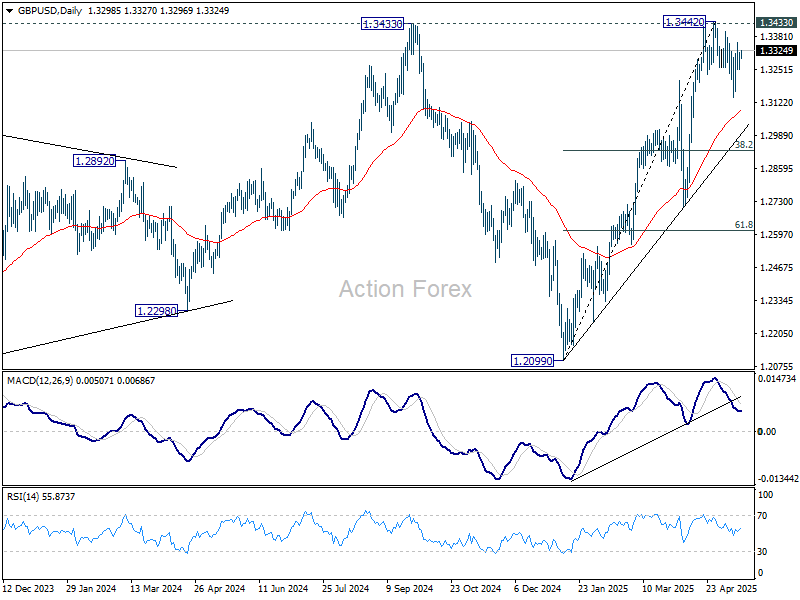

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3263; (P) 1.3292; (R1) 1.3331; More...

Outlook in GBP/USD is unchanged and intraday bias stays neutral. On the upside, decisive break of 1.3433/42 key resistance zone will confirm larger up trend resumption. Nevertheless, below 1.3138 will resume the correction from 1.3442. But downside should be contained by 38.2% retracement of 1.2099 to 1.3442 at 1.2929 to bring rebound.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could either be resuming the up trend, or the second leg of a consolidation pattern. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on decisive break of 1.3433 at a later stage.

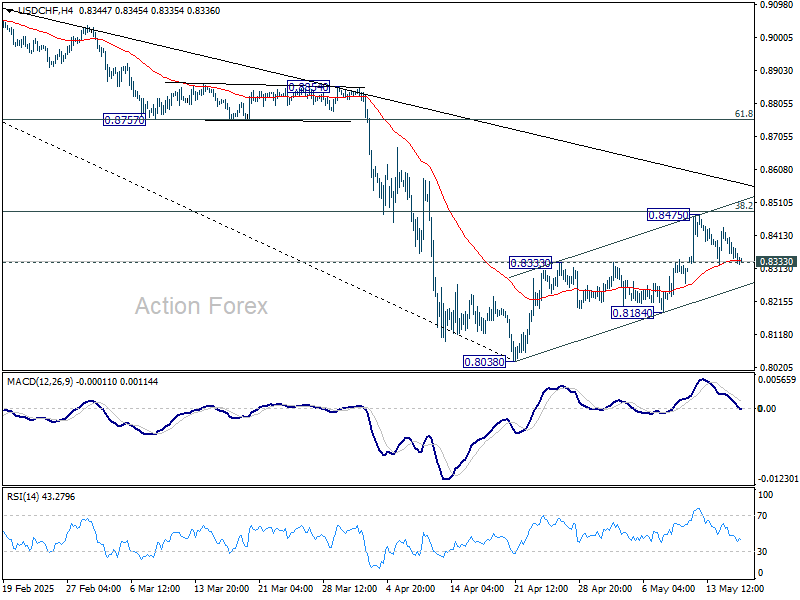

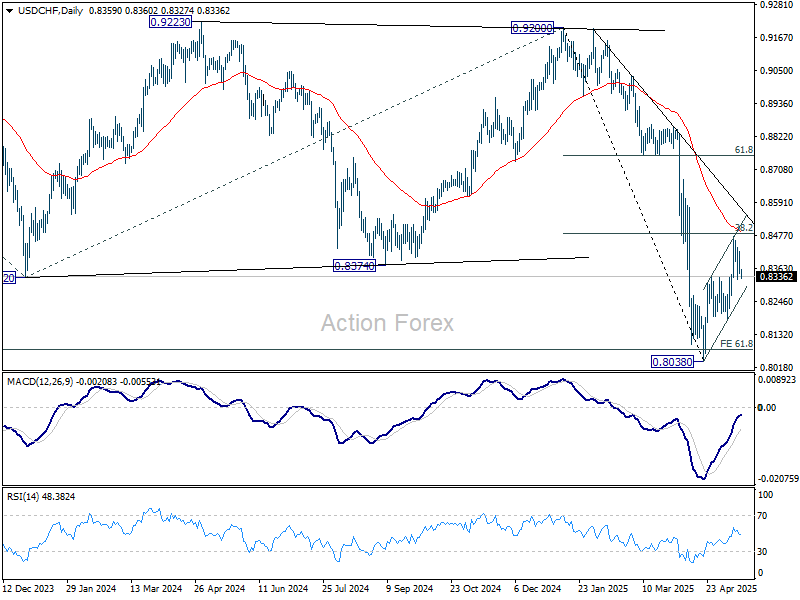

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8328; (P) 0.8377; (R1) 0.8409; More….

Intraday bias in USD/CHF stays neutral at this point. On the downside, firm break of 0.8333 resistance turned support will argue that corrective rebound from 0.8038 has completed at 0.8475, after rejection by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. Intraday bias will be back on the downside for 0.8184, and then retest of 0.8038 low. However, sustained trading above 0.8482 will dampen this bearish view and target 61.8% retracement at 0.8756 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8750) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

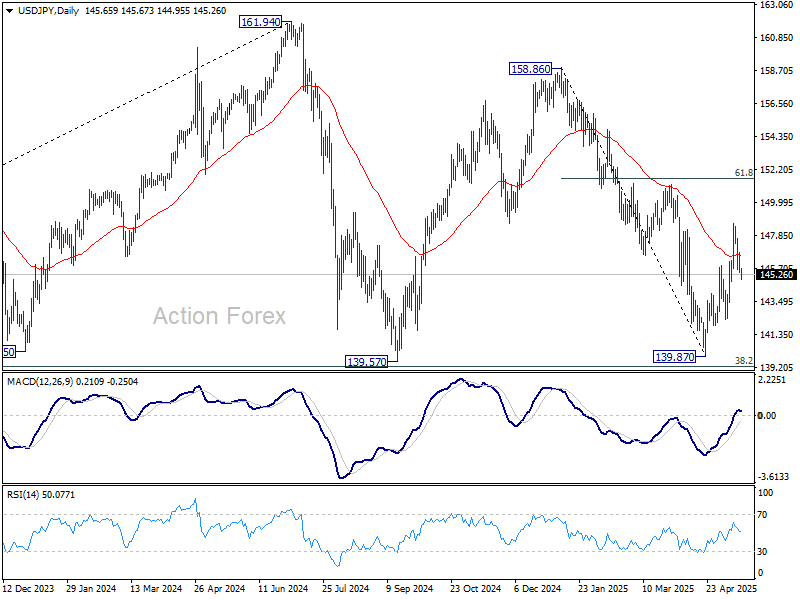

USD/JPY Daily Outlook

Daily Pivots: (S1) 145.13; (P) 145.97; (R1) 146.53; More...

Intraday bias in USD/JPY remains neutral and more consolidations could be seen below 148.64. . Further rally is expected as long as 144.02 resistance turned support holds. As noted before, fall from 158.86 could have completed 139.87 already. Above 148.64 will target 61.8% retracement of 158.86 to 139.87 at 151.60 next. However, firm break of 144.02 will bring retest of 139.87 low instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Weak Data Overlooked as Yen Rises on Risk-Off Mood

Mild risk-off mood is helping Yen to extend its near-term rebound, despite fresh signs of economic weakness at home. Japan’s economy was already showing signs of strain even before the impact of US tariffs, with Q1 GDP contracting more sharply than expected. BoJ is left in an increasingly precarious position, wedged between deteriorating growth and persistent inflationary pressures.

A recent Reuters poll taken between May 7 and 13 revealed a significant shift in market expectations, with 67% of economists now projecting that BoJ will hold its policy rate at 0.50% through the third quarter. That’s up sharply from just 36% a month ago, highlighting how tariff-related risks have changed expectations for near-term tightening.

On the trade front, Japan is preparing a third round of negotiations with the US, as it seeks to secure exemptions from tariffs on automobiles and auto parts. In return, Tokyo is reportedly considering a set of concessions, including increased imports of US corn and soybeans, regulatory changes to auto inspection standards, and cooperation in shipbuilding technology.

Chief negotiator Ryosei Akazawa is expected to travel to Washington as early as next week, though the timeline hinges on progress in working-level talks. Meanwhile, Finance Minister Katsunobu Kato will travel to Canada for G7 meetings, where he may hold bilateral discussions with US Treasury Secretary Scott Bessent on foreign exchange matters.

Overall for the week so far, Yen is currently the top performer, followed by Sterling and then Dollar. Kiwi is the weakest, trailed by Euro and Swiss Franc. Loonie and Aussie sit in the middle of the pack. The overall tone in the currency markets remains mixed.

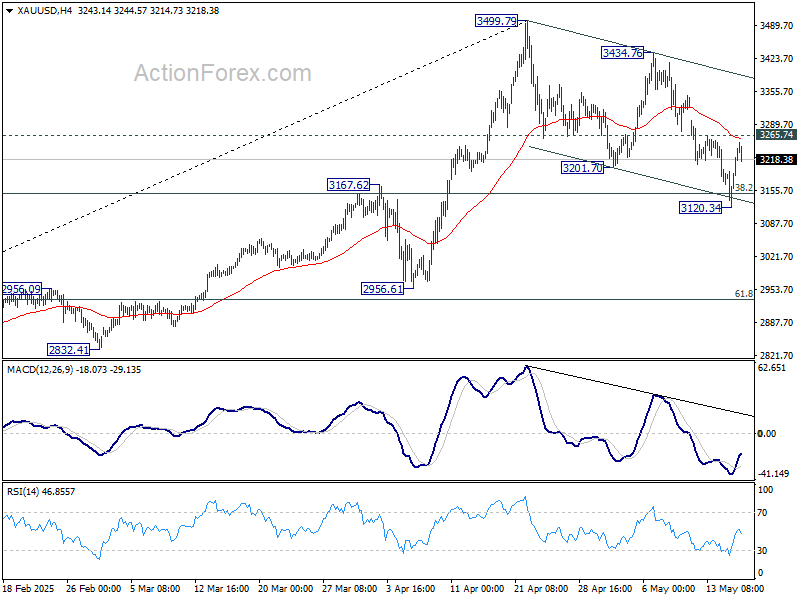

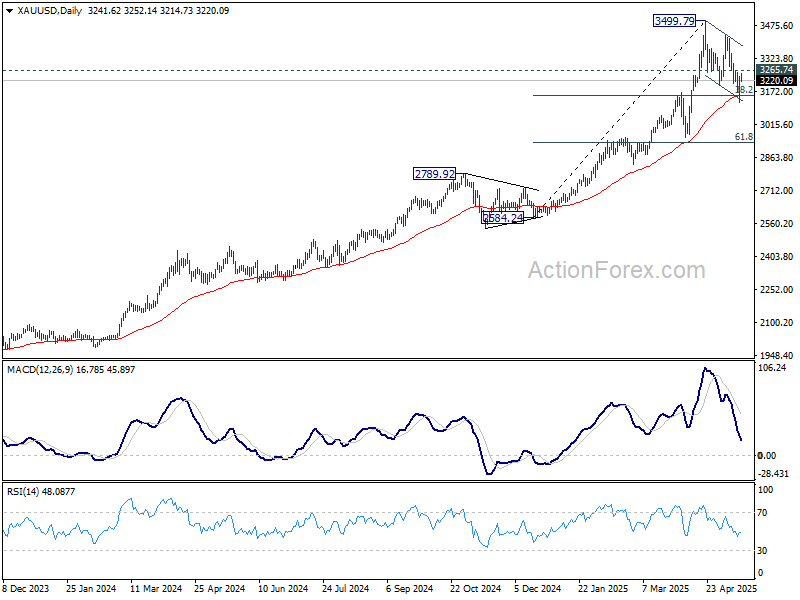

Technically, Gold has bounced from key cluster support around 3150, including 55 D EMA (now at 3151.09) and 38.2% retracement of 2584.24 to 3499.79 at 3150.04. It's possible that correction from 3499.79 has completed already. Firm of 3265.74 will reinforce this bullish case, and suggest that larger up trend is ready to resume. If realized, that should be accompanied by another round of selloff in Dollar. However, sustained break of 3150 will dampen this view and bring deeper fall to 61.8% retracement at 2933.98.

In Asia, at the time of writing, Nikkei is down -0.06%. Hong Kong HSI is down -0.40%. China Shanghai SSE is down -0.34%. Singapore Strait Times is down -0.20%. Japan 10-year JGB yield is down -0.016 at 1.463. Overnight, DOW rose 0.65%. S&P 500 rose 0.41%. NASDAQ fell -0.18%. 10-year yield fell -0.073 to 4.455.

Looking ahead, Eurozone trade balance in the main feature in European session. Later in the day, US will release housing starts and building permits, and import prices. But attention will be on U of Michigan consumer sentiment and inflation expectations.

Japan’s GDP contracts -0.2% qoq in Q1, export drag offsets capex gains

Japan’s economy shrank by -0.2% qoq in Q1, marking its first contraction in a year and falling short of the -0.1% qoq consensus. On an annualized basis, GDP contracted by -0.7%, a sharp disappointment compared to expectations for -0.2%.

The weakness was largely driven by external demand, which subtracted -0.8 percentage points from growth as exports declined -0.6% qoq while imports jumped 2.9% qoq.

Domestically, the picture was mixed. Private consumption, comprising more than half of Japan’s output, was flat on the quarter. However, capital expenditure provided some support, rising by a solid 1.4% qoq.

Meanwhile, inflation pressures showed no sign of easing, with the GDP deflator accelerating from 2.9% yoy to 3.3% yoy, above expectations of 3.2% yoy.

RBNZ inflation expectations rise to 2.41%, further easing seen ahead

RBNZ’s latest Survey of Expectations for May revealed a notable uptick in inflation forecasts across all time horizons.

One-year-ahead inflation expectations climbed from 2.15% to 2.41%, while two-year expectations rose from 2.06% to 2.29%. Even long-term projections edged higher, with five- and ten-year-ahead expectations increasing to 2.18% and 2.15% respectively.

Despite the upward revisions in inflation outlook, expectations for monetary policy point clearly toward easing.

With the Official Cash Rate currently at 3.50%, most respondents anticipate a 25 bps cut by the end of Q2. Looking further ahead, the one-year-ahead OCR expectation also declined from 3.23% to 2.91%.

NZ BNZ manufacturing rises to 53.9, recovery gains ground

New Zealand’s BusinessNZ Performance of Manufacturing Index edged up from 53.2 to 53.9 in April. The gain was driven by improvements in employment and new orders, up to 55.0 and 51.4 respectively, with employment reaching its highest level since July 2021. However, production eased slightly to 53.8.

BNZ Senior Economist Doug Steel noted that while the sector isn’t booming, the recovery is clear, with the PMI rebounding sharply from a low of 41.4 last June.

Still, he cautioned, "there remain questions around how sustainable it is given uncertainty stemming from offshore”.

Fed's Barr: Solid economy faces threats from tariff-driven supply disruptions

Fed Governor Michael Barr highlighted solid growth, low unemployment, and continued progress on disinflation in the US economy. However, he flagged growing concern over rising trade-related uncertainty, which has begun to weigh on consumer and business sentiment.

In a speech overnight, Barr specifically pointed to the vulnerability of small businesses, which are more exposed to "disruptions to supply chains and distribution networks".

These firms are integral to broader production networks, and failures in this segment could trigger cascading effects across the economy.

Drawing a parallel to the pandemic, Barr noted that "disruptions can have large and lasting effects on prices, as well as output," leading to lower growth and higher inflation ahead.

USD/JPY Daily Outlook

Daily Pivots: (S1) 145.13; (P) 145.97; (R1) 146.53; More...

Intraday bias in USD/JPY remains neutral and more consolidations could be seen below 148.64. . Further rally is expected as long as 144.02 resistance turned support holds. As noted before, fall from 158.86 could have completed 139.87 already. Above 148.64 will target 61.8% retracement of 158.86 to 139.87 at 151.60 next. However, firm break of 144.02 will bring retest of 139.87 low instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

RBNZ inflation expectations rise to 2.41%, further easing seen ahead

RBNZ’s latest Survey of Expectations for May revealed a notable uptick in inflation forecasts across all time horizons.

One-year-ahead inflation expectations climbed from 2.15% to 2.41%, while two-year expectations rose from 2.06% to 2.29%. Even long-term projections edged higher, with five- and ten-year-ahead expectations increasing to 2.18% and 2.15% respectively.

Despite the upward revisions in inflation outlook, expectations for monetary policy point clearly toward easing.

With the Official Cash Rate currently at 3.50%, most respondents anticipate a 25 bps cut by the end of Q2. Looking further ahead, the one-year-ahead OCR expectation also declined from 3.23% to 2.91%.

Everybody, Breathe…

The US–China 90-day deal shows that actual outcomes are typically less bad than the ambit claims the Trump administration first announces.

Once again, the US administration has shown that its initial announcements are usually ambit claims. These claims are rolled back to something less self-destructive, so long as the other party is willing to offer something in return. It is all part of the deal ‘process’, as well as something of a dominance display.

Trade between the US and China was never going to come to a sudden stop, except by accident. That would have been too damaging to both parties. Neither was the US in a position to demand that its allies break trade ties with China – a question that we have been asked several times in recent months.

For these reasons, we have maintained the view that the US would not fall into a serious recession, though it would take a noticeable hit to growth; that China would manage to reach its 5% growth target for 2025; and that the RBA did not need to and would not panic. It is early days, but so far these core assessments have been borne out.

Some of the initial market reaction therefore proved overblown. To be fair, though, this was partly because pricing needs to reflect the whole range of possibilities, including the downside scenarios that now look less likely. It is only after those uncertainties are largely resolved that we see pricing converging to be in line with a base-case view. Once again, it is worth keeping one’s head and not overreacting to short-term fluctuations. This will be particularly relevant in the coming months. Trade and other data flow will be unusually volatile as the rush to beat the tariffs and the payback slump afterwards work their ways through, making it hard to see underlying trends.

The reduction in trade uncertainties supports the reduction in other uncertainties. While it is not clear where US–China tariffs will settle after the 90-day pause, it seems more likely that it will be close to (or even lower than) where they are now, not the three-digit trade-stopping rates that were previously announced. This means a smaller hit to growth in China from the trade war, and thus a smaller task for the Chinese authorities to achieve their 5% growth target for 2025. We can therefore be a bit more confident that the task will be achieved and our base-case view for China will also come to fruition.

There is still a longer-term partial disentanglement to come. A complete decoupling into separate trade spheres is too self-destructive to be realistic, at least in the short term, and no longer looks to be a material risk. Plenty of Western companies and governments might nonetheless decide that they do not want to be quite so dependent on China as a single source of supply of key inputs, whether that be specific minerals or ingredients for pharmaceuticals, and so on.

This cuts both ways, though. Given the recent behaviour of the Trump administration on the USMCA trade deal, rule of law and defence issues, plenty of European and Canadian companies and governments may well be coming to the view that they also do not want to be quite so dependent on US providers of defence systems, cloud computing services and other specialised exports that the US has dominated up to now. Certainly there were a few mutterings along these lines related to me by our offshore customers in recent months.

Implications for Australia

Australia was always a small target for the Trump administration’s trade policy. A 10% tariff rate is entirely survivable, especially when the exchange rate of the destination country is at least that much overvalued. The Trump administration has proven that it will indeed do deals, as well as negotiating with itself to offer unilateral concessions like the original 90-day pause and the electronics carve-out. There is nonetheless an argument it might be better to avoid drawing attention to ourselves by attempting to get carve-outs that other countries are not getting.

There is, however, a role Australia can play by telling our own story. Australia tried hiding behind a tariff wall for decades. It was not the path to prosperity, as it turned out. It certainly did not create a vibrant manufacturing sector that could compete on the world stage. Manufacturing exports did eventually blossom – some even called it a boom – but only in the 1990s and early 2000s after the tariff wall was dismantled. While the boom in iron ore and LNG exports since the mid-2000s has squeezed manufacturing’s share of Australia’s total export volumes, at around 6½% it is still noticeably higher than in the late 1970s and early 1980s.

There are certainly protections that other countries have used to develop their manufacturing sectors as they begin to engage with the rest of the world. As well as the more obvious policies such as subsidies and tariffs, these include keeping one’s exchange rate low by building up foreign exchange reserves. But these are tactics of poor countries growing richer. There is no real evidence that the same tactics work for countries that are already rich, as Australia’s 20th century experience showed. If only the US administration understood this.