Sample Category Title

A Busy Week of Prominent Data Releases

In focus today

Today will be light on the macro front, but in Denmark, focus turns to the release of the retail trade index for March at 8:00 CET. According to our own Spending Monitor, retail spending decreased 2.5% y/y in real terms in March compared to the same month last year. However, this fall was driven by the seasonal effect of Easter falling in March last year and April this year. Adjusted for seasonality, real spending increased 1.8% m/m in March, and we expect the consumption figures today to reflect this increase.

In Sweden, we will receive PPI data for March from Statistics Sweden at 8:00 CET. The PPI and price plans from the NIER survey (released on Tuesday) will play a crucial role in shaping inflation expectations, which will influence the Riksbank's ability to implement further rate cuts.

For the remainder of the week, we will receive a lengthy list of key data releases. Among the most important, we look out for PMI data from China and US Q1 GDP, due for release on Wednesday. On Thursday, we keep an eye on the monetary policy meeting at the Bank of Japan, while Friday's releases include both euro area April flash HICP and the US April Jobs Report.

Economic and market news

What happened Friday and over the weekend

In the US, the University of Michigan consumer sentiment was revised higher to 52.2 in April 2025 from a preliminary reading of 50.8. Despite the upward revision, consumer sentiment fell for a fourth consecutive month to the lowest level since July 2022, as consumers perceived risks to multiple aspects of the economy, in large part due to the ongoing uncertainty around trade policy and the potential for a resurgence of inflation looming ahead. Year-ahead inflation expectations jumped to 6.5% due to tariff announcements, though this figure was revised slightly down from 6.7% in the preliminary release.

In Japan, Tokyo April inflation (excl. fresh food) rose to 3.4%, beating consensus and indicating sustained and broadening price pressures. As stated by Governor Ueda, BoJ will continue to raise rates if inflation converges towards 2%-target (until now, it has been largely driven by food). However, he also noted how the trade war might decrease the likelihood of durable inflation. We have pushed our two expected rate hikes further down the road, with one in the autumn and another in the first quarter of 2026.

In China, industrial profits expanded by 0.8% y/y in the first three months of 2025, recovering from a 0.3% drop in the first two months of the year, amid further stimulus measures from Beijing. Additionally, private sector profits fell by 0.3%, a much softer drop than the 9.0% plunge in the prior period.

In the US-China trade war, conflicting messages emerged from members of Trump's cabinet regarding the ongoing trade negotiations with China over tariffs. Although President Trump claimed discussions were taking place and that he had spoken with Chinese President Xi Jinping, Beijing denied any such talks. Treasury Secretary Scott Bessent mentioned interactions with Chinese officials during IMF meetings but said he did not discuss tariffs. Meanwhile, Agriculture Secretary Brooke Rollins asserted that daily conversations with China about tariffs were occurring.

In geopolitics, Trump and Zelenskiy met one-on-one on Saturday, as many prominent state leaders travelled to Rome for the funeral of Pope Francis. The meeting, described as "very productive," marked their first encounter since a tense Oval Office meeting in February. After the meeting, Trump criticised Russian President Vladimir Putin's recent missile attacks on civilian areas in Ukraine, suggesting that alternative strategies such as banking or secondary sanctions might be necessary. On Sunday, Trump once again urged Russia to stop attacks, while US Secretary of State Marco Rubio said the Trump administration might abandon its attempts to broker a deal if Russia and Ukraine do not make headway. Republican Senator Lindsay Graham stated that the US could consider secondary tariffs on anyone involved in selling Russian oil. The idea was already floated in early April, but thus far the Trump administration has kept its powder dry. More pressure has been put on Zelenskiy, instead of Putin.

On another note, Greenland and Denmark agreed on Sunday to strengthen ties in response to US interest in acquiring Greenland. Greenland's PM Jens-Frederik Nielsen visited Denmark and met with Danish PM Mette Frederiksen to emphasise unity amid Trump's annexation ambitions. Both leaders stressed that only Greenlanders can decide their territory's future, rejecting US acquisition while seeking respectful partnership.

Equities: What a week in equities! S&P 500 rebounded by 5% last week and Nordic/European indexes by 3%. Cyclicals made a massive comeback, gaining >5% globally and thereby outperforming defensives by a huge margin. The turnaround in stocks even triggered a Zweig Breadth Thrust, which is a rare technical momentum indication of bull market. Friday was no different, with S&P 500 gaining 0.7% and Stoxx 600 0.4%. Investors are struggling for direction this morning though, with Asia unchanged and US futures dipping into negative.

FI & FX: Last week ended relatively quietly, with risk appetite holding up reasonably well, while US Treasury yields continued to decline. The 2Y US Treasury yield fell by 5bp, while both the 10Y and 30Y segments declined by 8bp. As a result, the US yield curve steepened modestly from the front end. In contrast, yields moved slightly higher in Europe, with the 2Y German government yield rising 3bp and the 10Y up 2bp, despite dovish comments from ECB's Holzmann. In the FX space, EUR/USD consolidated within the 1.13-1.14 range, as the USD sell-off took a breather, supported by positive headlines on US-China de-escalation and a more measured tone from the Trump administration regarding Fed independence. Overall, moves in G10 FX were modest - CHF and JPY weakened against the USD amid the improving risk environment. This week, focus turns to inflation, GDP and labour market data from the euro area and the USD, while the Bank of Japan is set to maintain its monetary policy stance unchanged on Thursday, while the Fed entered its blackout period on Saturday. This week, a flurry of global data will shape the macro narrative alongside trade-related headlines.

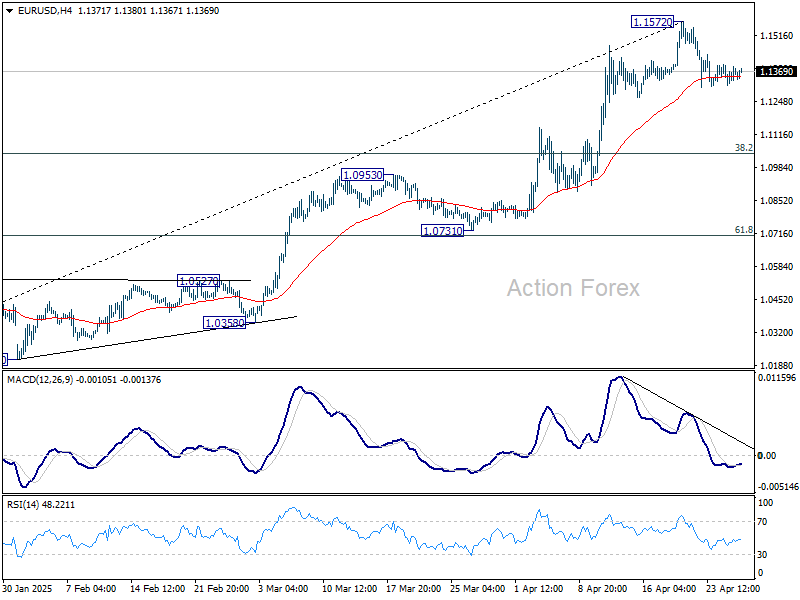

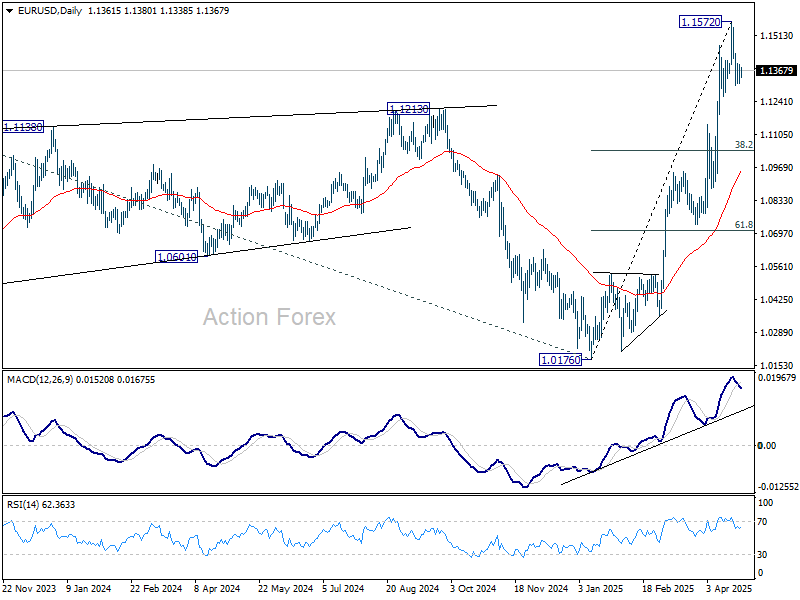

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1322; (P) 1.1358; (R1) 1.1401; More...

Despite loss of downside momentum as seen in 4H MACD, EUR/USD's correction from 1.1572 short term top could still extend lower. Nevertheless, strong support should be seen from 38.2% retracement of 1.0176 to 1.1572 at 1.1039 to contain downside. On the upside, break of 1.1572 will resume larger up trend.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0792) holds.

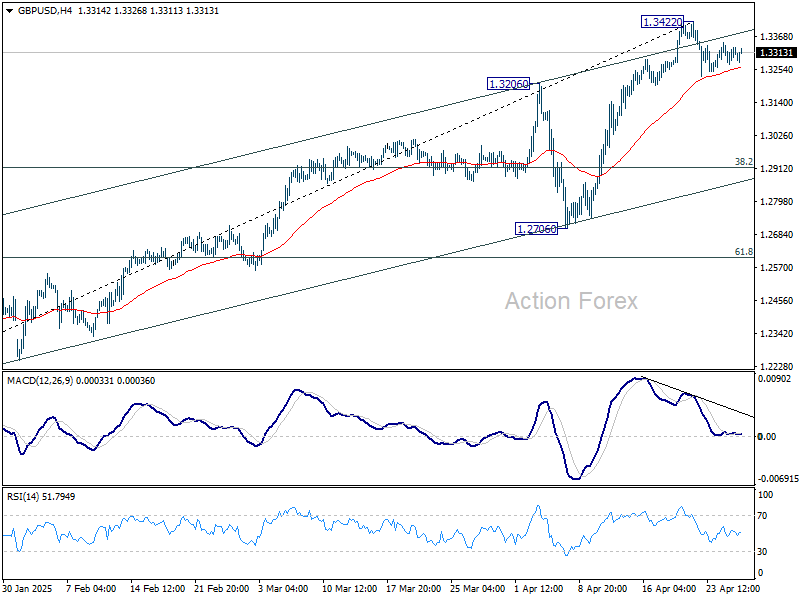

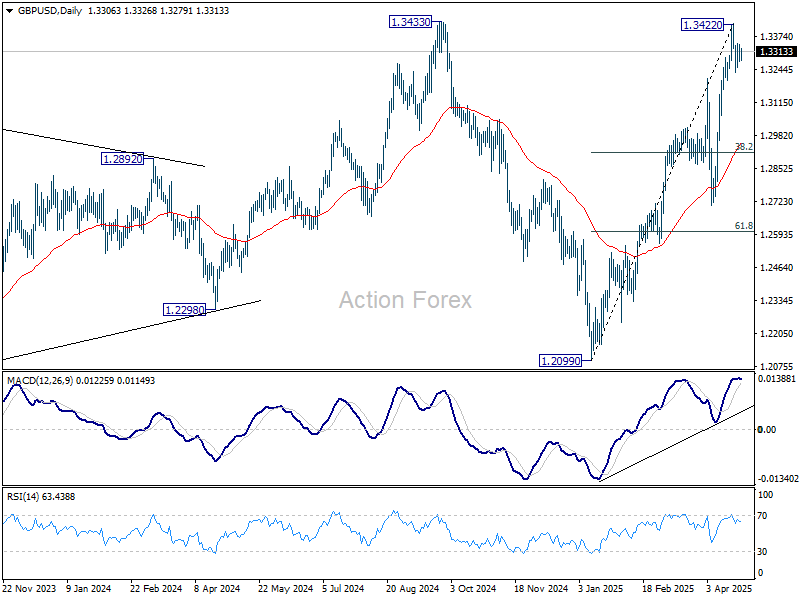

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3268; (P) 1.3318; (R1) 1.3361; More...

GBP/USD's correction from 1.3422 short term top could still extend lower. But downside should be contained by 38.2% retracement of 1.2099 to 1.3422 at 1.2917. On the upside, firm break of 1.3433 will resume larger up trend.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

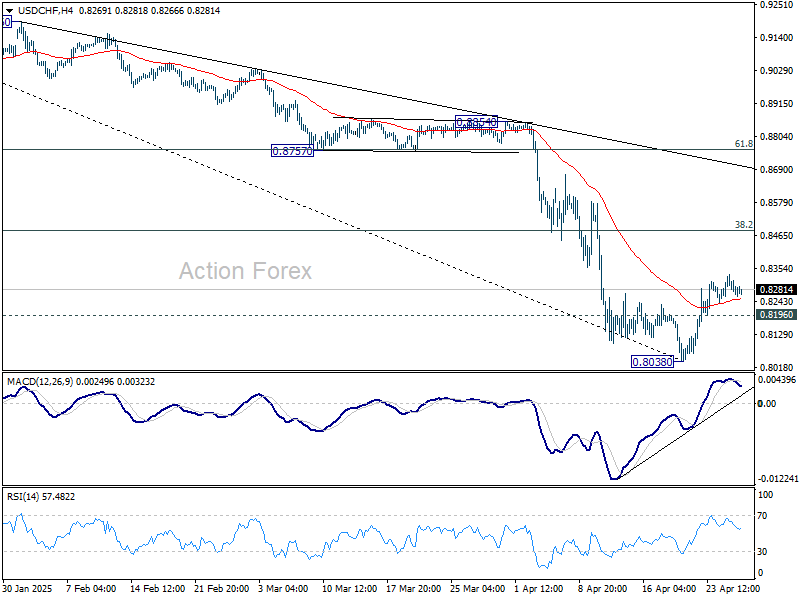

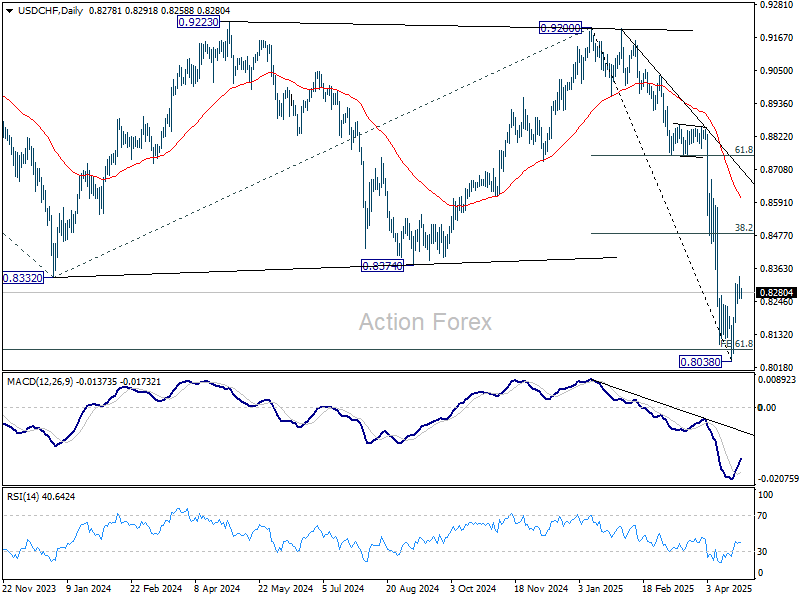

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8246; (P) 0.8290; (R1) 0.8321; More….

Despite loss of momentum as seen in 4H MACD, further rise remains mildly in favor in USD/CHF with 0.8196 minor support intact. However, upside should be limited by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. On the downside, below 0.8196 minor support will bring retest of 0.8038. Firm break there will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8794) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

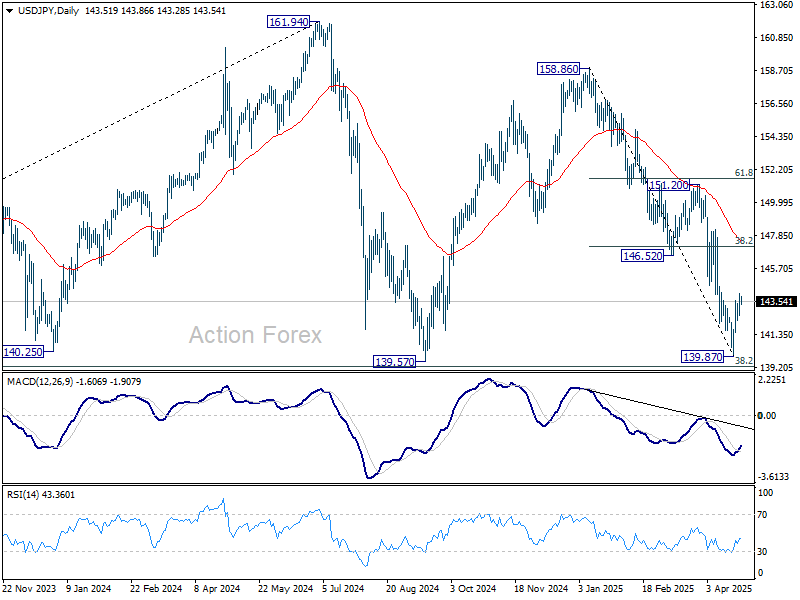

USD/JPY Daily Outlook

Daily Pivots: (S1) 142.82; (P) 143.42; (R1) 144.28; More...

Further rise is expected in USD/JPY with 142.26 minor support intact. However, near term outlook will stay bearish as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds. On the downside, break of 142.26 will argue that the recovery from 139.87 short term bottom has completed as a corrective move. Retest of 139.87 should then be seen next in this case.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

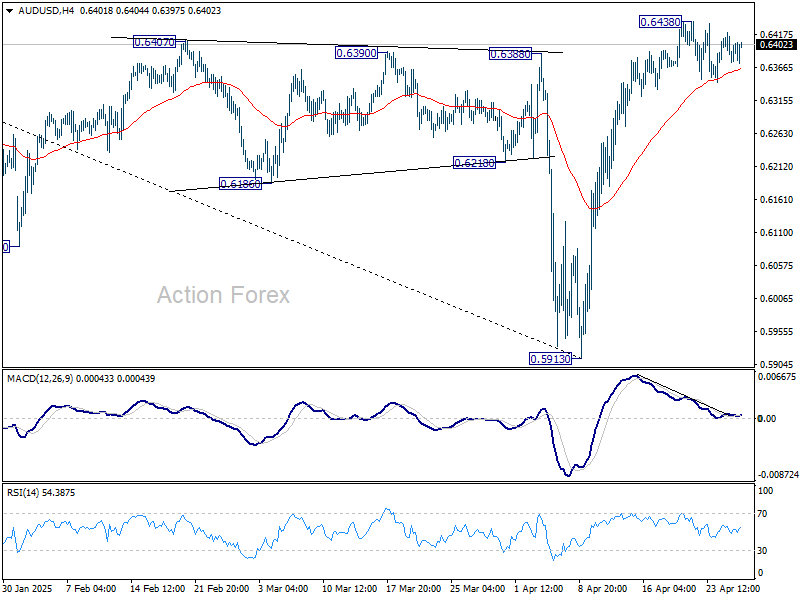

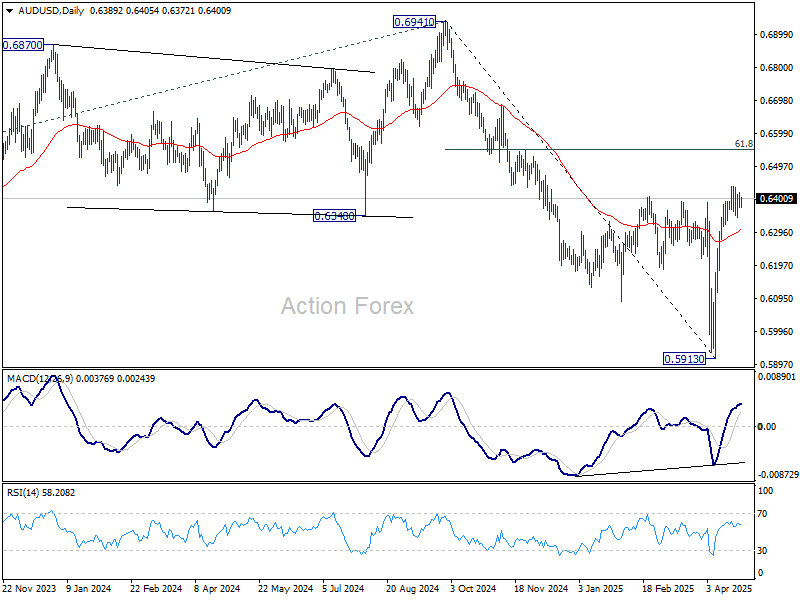

AUD/USD Daily Report

Daily Pivots: (S1) 0.6374; (P) 0.6398; (R1) 0.6420; More...

Intraday bias in AUD/USD remains neutral as consolidations continue below 0.6438. Further rally is expected as long as 55 D EMA (now at 0.6305) holds. Above 0.6438 will resume the rebound from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, sustained trading below 55 D EMA will argue that the rebound has completed and turn bias back to the downside.

In the bigger picture, as long as 55 W EMA (now at 0.6440) holds, the down trend from 0.8006 (2021 high) should resume later to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

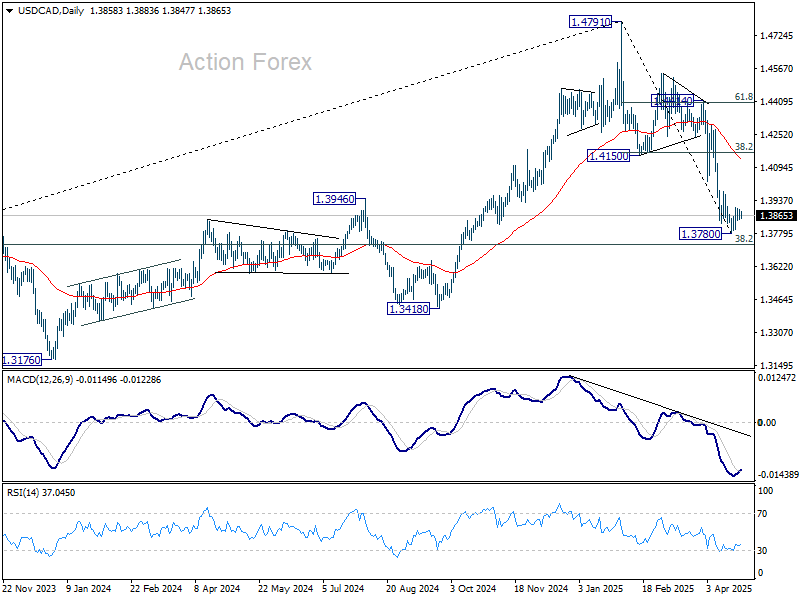

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3833; (P) 1.3863; (R1) 1.3883; More...

Further recovery remains mildly in favor in USD/CAD despite some loss of upside momentum as seen in 4H MACD. Still, even in case of another rise, upside should be limited by 1.4150 support turned resistance (38.2% retracement of 1.4791 to 1.3780 at 1.4166). On the downside, firm break of 1.3780 short term bottom will resume the whole fall from 1.4791.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4150 resistance turned support holds. firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

Subdued Start to a Heavy Data Week with Risk Sentiment Holding Steady

Trading was particularly subdued today, even by the quiet standards of a typical Monday in Asia. That’s not surprising, given the near-empty economic calendar offering little to move the markets. Instead, traders are exercising understandable caution ahead of a heavy barrage of important data releases later this week, including US and Eurozone GDP figures, inflation reports from the US, Eurozone, and Australia, and the US non-farm payrolls report.

Now that the peak of the tariff shock appears to have passed, at least for this current wave, the market's attention is shifting toward how these escalations are starting to materialize in hard economic data. Early indications from global PMIs and corporate earnings have been mixed, but this week's heavyweight releases will offer more definitive evidence. For now, the overall market mood remains cautiously optimistic, and there is still room for a further rebound in risk assets if the incoming data holds up or surprises to the upside.

Meanwhile, Yen will also be a major focus this week with BoJ’s rate decision and new economic projections due. Yen has softened notably since last week as risk appetite improved globally. Speculation is also building that BoJ might delay its next rate hike in response to tariff-induced uncertainties. Should the BoJ’s updated projections lean dovish, Yen could face another leg of weakness against its major counterparts.

Technically, USD/JPY’s recovery from the short-term bottom at 139.87 remains in favor as long as 142.26 minor support holds. However, the broader near-term outlook stays bearish unless the pair can break decisively above 38.2% retracement of 158.86 to 139.87 at 147.12. Failure to do so, followed by break back below 142.26, would argue that the recovery is a corrective move, and bring retest of 139.87 next.

In Asia, at the time of writing, Nikkei is up 0.43%. Hong Kong HSI is up 0.07%. China Shanghai SSE is down -0.03%. Singapore Strait Times is down -0.43%. Japan 10-year JGB yield is down -0.017 at 1.323.

Japan denies report of US preference for weaker Dollar and stronger Yen

Japanese officials moved swiftly to deny a media report suggesting that US Treasury Secretary Scott Bessent had conveyed a preference for a weaker Dollar and stronger Yen during recent bilateral meetings in Washington last week.

Japan’s top currency diplomat, Atsushi Mimura, emphasized to reporters that "the US side did not touch upon exchange-rate targets" in discussions between Finance Minister Katsunobu Kato and his US counterpart.

Finance Minister Kato also reiterated via social media that exchange-rate frameworks were not discussed, directly refuting the report published by the Yomiuri newspaper.

Meanwhile, Bessent himself described the talks with Japan as "very constructive" in a post on X, noting that they covered reciprocal trade issues and "matters pertaining to exchange rates" without mentioning any explicit preferences.

China reaffirms growth target, holds back on major stimulus

China pledged its full confidence in achieving this year’s growth target of around 5%, vowing to implement timely and multiple support measures as the country is now in full-fledged trade war with the US. However, no major stimulus was announced immediately, giving the impression that Beijing is not in a rush to roll out large-scale interventions. Authorities appear inclined to first monitor the trade shock’s timing and magnitude before deciding on more aggressive measures.

Zhao Chenxin, deputy head of the National Development and Reform Commission, stressed at a press conference today that China retains "ample policy reserves and plenty of policy space," and highlighted plans to stabilize employment and strengthen public employment services.

At a Politburo meeting chaired by President Xi Jinping last week, officials called for a “timely reduction” in interest rates and reserve requirement ratios to support the economy. Additional measures to aid struggling businesses, boost consumption among middle- and lower-income groups, and promote further development in technology and artificial intelligence were also emphasized.

As a touch of optimism, official data released over the weekend showed China’s industrial profits returning to growth in the first quarter. Cumulative profits rose 0.8% yoy to CNY 1.5T, reversing a -0.3% decline seen in the first two months.

High-stakes week ahead

It’s shaping up to be an extremely busy week for global markets, even though Monday’s economic calendar is near-empty. The action will pick up quickly, with BoJ rate decision and BoC summary of deliberations. Meanwhile, high-profile data releases include US GDP, PCE inflation, non-farm payrolls; Eurozone GDP and CPI' Australia’s CPI; Canada’s GDP; and China's PMIs.

Starting with BoJ, the central bank is widely expected to leave its short-term policy rate unchanged at 0.50% during this week’s meeting. According to a recent Reuters poll, only about half of economists still expect a hike to 0.75% in Q3, a notable drop from the 70% figure recorded in March. Market pricing now sees about a 65% chance of a 25bps hike by year-end.

The impact of Trump’s tariffs has made Japan’s economic outlook highly uncertain, particularly with manufacturing earnings expected to deteriorate. As a result, BoJ is likely to delay any further rate hikes, and is set to lower its economic growth forecast in the upcoming quarterly outlook. Nevertheless, BoJ is still expected to signal that rising wages and gradually firming inflation trends remain intact, keeping the door open for tightening when conditions allow.

From the US, a barrage of key releases will take center stage: the advance estimate of Q1 GDP, PCE inflation report, ISM manufacturing, and the all-important April non-farm payrolls. Fed officials have recently made it clear that May is too early for any rate cut, but there are increasing signs that attention is shifting back toward the employment side of the dual mandate. Should the labor market show signs of unexpected weakness, the probability of a Fed rate cut in June — currently hovering around 65% — could firm up sharply.

Turning to the Eurozone, flash GDP and CPI figures will be pivotal. Reports suggest a growing consensus within the ECB for another rate cut in June. Relief comes from the observation that the inflationary shock from US tariffs has been relatively muted, with Euro’s appreciation and weakening growth dynamics exerting deflationary pressure.

However, the durability of this trend is still in question. If Eurozone core inflation shows signs of re-acceleration, it could complicate ECB’s easing plans. Hence, this week’s CPI data will be crucial in either validating or challenging the market’s current expectation for further ECB easing.

In Australia, sentiment is shifting toward an imminent rate cut by RBA. Recent data have underwhelmed, with wage growth missing RBA’s own projections and consumption proving softer than expected. Coupled with lingering global trade uncertainties, particularly between the US and China, the case for another RBA rate cut to cushion the economy has strengthened considerably. Unless Australia’s Q1 CPI report delivers a major upside surprise this week, the market is likely to fully price in a rate cut at the May meeting.

Here are some highlights for the week:

- Tuesday: Germany Gfk consumer sentiment; Eurozone M3 money supply; US goods trade balance, house price index, consumer confidence.

- Tuesday: Japan industrial production, retail sales, housing starts; New Zealand ANZ business confidence; Australia quarterly CPI; China officials PMIs, Caixin PMI manufacturing; Eurozone GDP flash; Swiss KOF economic barometer; US ADP employment, GDP advance, Chicago PMI; personal income and spending, PCE inflation; Canada GDP, BoC summary of deliberations.

- Thursday: Japan PMI manufacturing final, consumer confidence, BoJ rate decision; Australia trade balance, import prices; Swiss retail sales; UK PMI manufacturing final, M4 money supply, mortgage approvals; US jobless claims, PMI manufacturing final, ISM manufacturing, construction spending; Canada PMI manufacturing.

- Friday: Japan unemployment rate, monetary base; Australia retail sales, PPI; Swiss PMI manufacturing; Eurozone PMI manufacturing final, CPI flash, unemployment rate; US non-farm payroll, factory orders.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3833; (P) 1.3863; (R1) 1.3883; More...

Further recovery remains mildly in favor in USD/CAD despite some loss of upside momentum as seen in 4H MACD. Still, even in case of another rise, upside should be limited by 1.4150 support turned resistance (38.2% retracement of 1.4791 to 1.3780 at 1.4166). On the downside, firm break of 1.3780 short term bottom will resume the whole fall from 1.4791.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4150 resistance turned support holds. firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

China reaffirms growth target, holds back on major stimulus

China pledged its full confidence in achieving this year’s growth target of around 5%, vowing to implement timely and multiple support measures as the country is now in full-fledged trade war with the US. However, no major stimulus was announced immediately, giving the impression that Beijing is not in a rush to roll out large-scale interventions. Authorities appear inclined to first monitor the trade shock’s timing and magnitude before deciding on more aggressive measures.

Zhao Chenxin, deputy head of the National Development and Reform Commission, stressed at a press conference today that China retains "ample policy reserves and plenty of policy space," and highlighted plans to stabilize employment and strengthen public employment services.

At a Politburo meeting chaired by President Xi Jinping last week, officials called for a “timely reduction” in interest rates and reserve requirement ratios to support the economy. Additional measures to aid struggling businesses, boost consumption among middle- and lower-income groups, and promote further development in technology and artificial intelligence were also emphasized.

As a touch of optimism, official data released over the weekend showed China’s industrial profits returning to growth in the first quarter. Cumulative profits rose 0.8% yoy to CNY 1.5T, reversing a -0.3% decline seen in the first two months.

Japan denies report of US preference for weaker Dollar and stronger Yen

Japanese officials moved swiftly to deny a media report suggesting that US Treasury Secretary Scott Bessent had conveyed a preference for a weaker Dollar and stronger Yen during recent bilateral meetings in Washington last week.

Japan’s top currency diplomat, Atsushi Mimura, emphasized to reporters that "the US side did not touch upon exchange-rate targets" in discussions between Finance Minister Katsunobu Kato and his US counterpart.

Finance Minister Kato also reiterated via social media that exchange-rate frameworks were not discussed, directly refuting the report published by the Yomiuri newspaper.

Meanwhile, Bessent himself described the talks with Japan as "very constructive" in a post on X, noting that they covered reciprocal trade issues and "matters pertaining to exchange rates" without mentioning any explicit preferences.