Sample Category Title

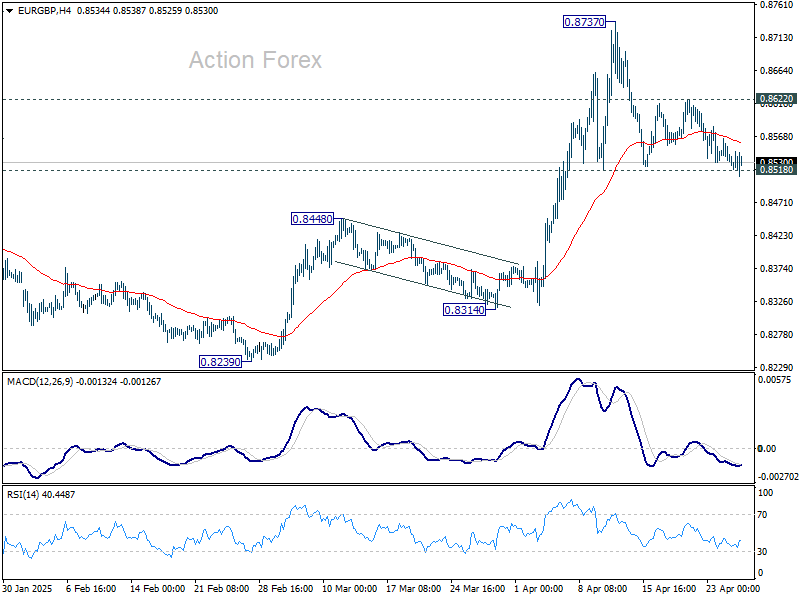

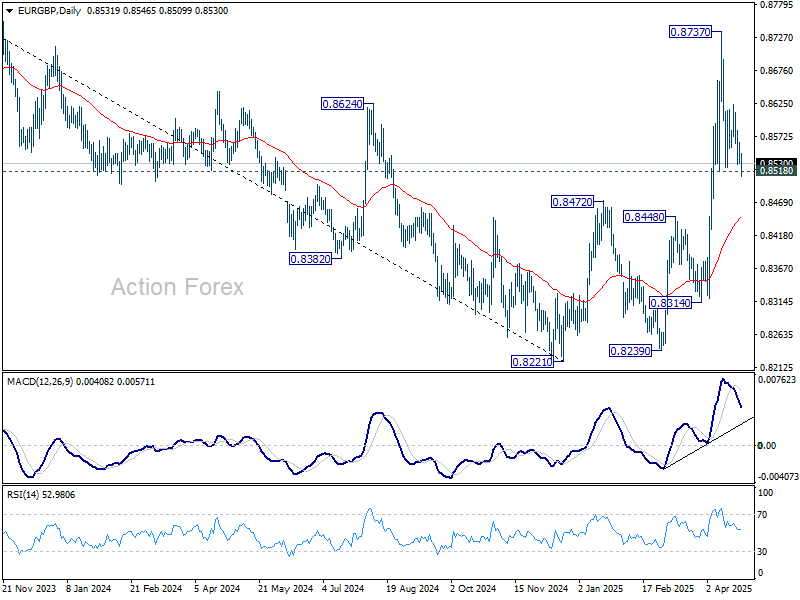

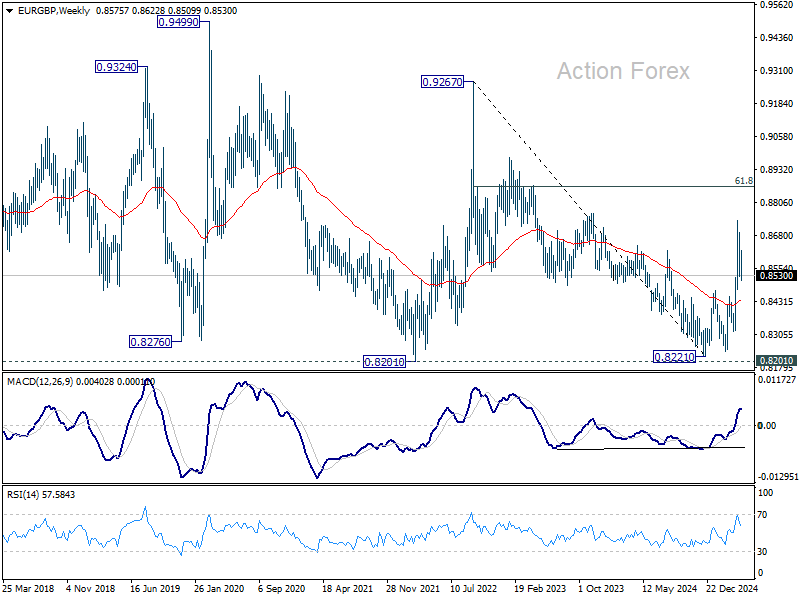

EUR/GBP Weekly Outlook

EUR/GBP's consolidation from 0.8737 continued last week and outlook is unchanged. Initial bias stays neutral this week first. Further rise is expected as long as 0.8518 support holds. On the upside, 0.8622 minor resistance will bring retest of 0.8737 first. Firm break there will resume the larger rally from 0.8221. However, sustained break of 0.8518 will bring deeper fall back to 55 D EMA (now at 0.8447).

In the bigger picture, down trend from 0.9267 (2022 high) should have completed at 0.8221, just ahead of 0.9201 key support (2024 low). Rise from 0.8221 is likely reversing the whole fall. Further rise should be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867 next. This will remain the favored case as long as 0.8472 resistance turned support holds.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

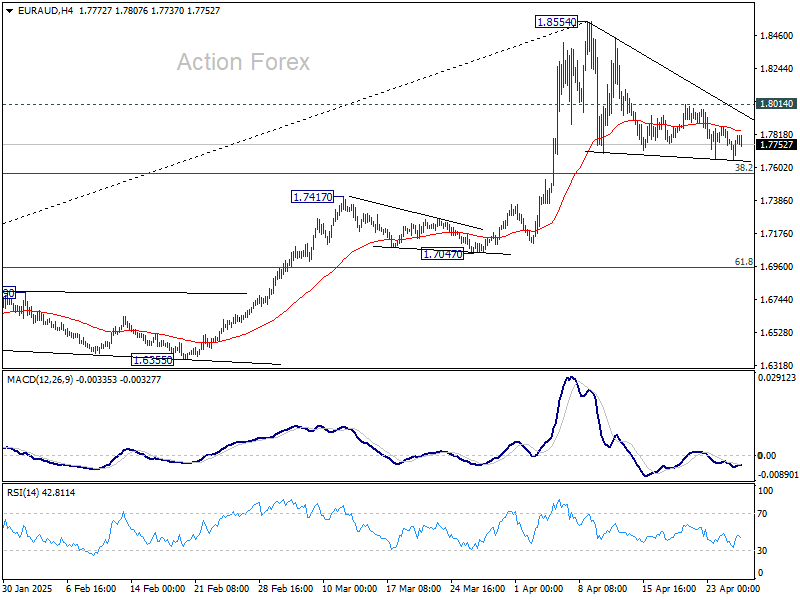

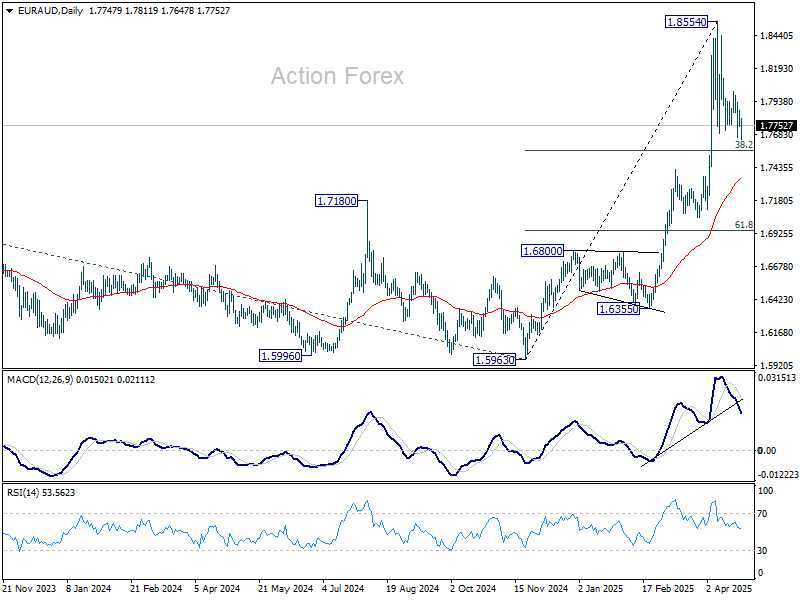

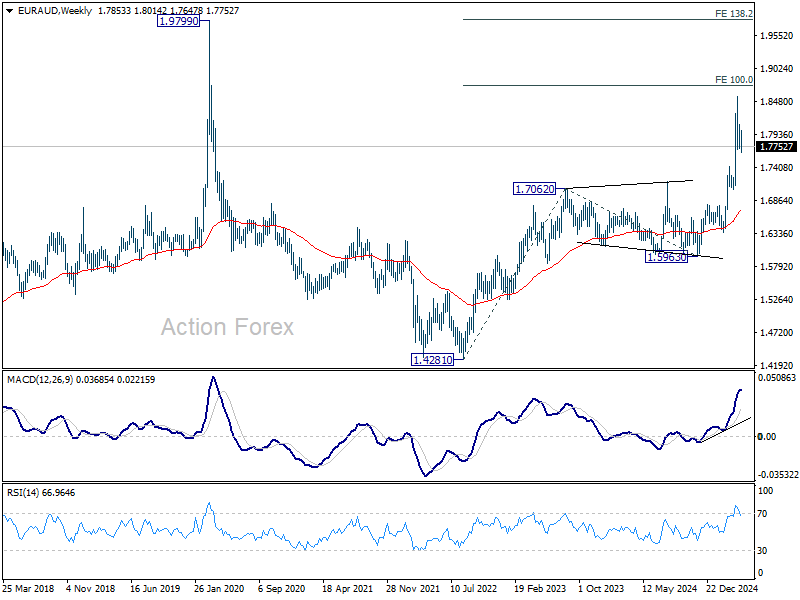

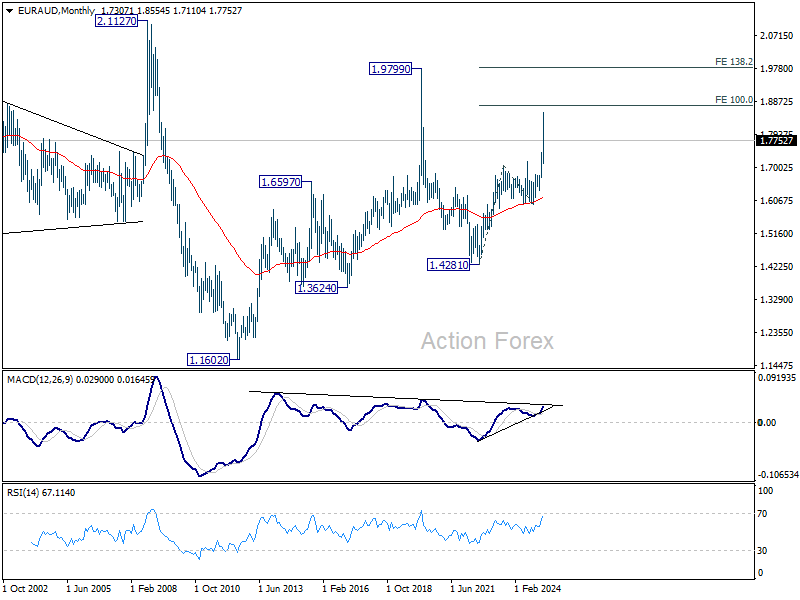

EUR/AUD Weekly Outlook

EUR/AUD's consolidation from 1.8854 continued last week and outlook is unchanged. Initial bias remains neutral this week first. Downside should be contained by 38.2% retracement of 1.5963 to 1.8854 at 1.7750. On the upside, above 1.8014 minor resistance will bring retest of 1.8554 first. Firm break there will resume larger up trend. However, firm break of 1.7750 will bring deeper fall to 55 D EMA (now at 1.7354).

In the bigger picture, up trend from 1.4281 (2022 low) is in progress for 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. Firm break there will pave the way to 138.2% projection at 1.9806, which is close to 1.9799 (2020 high). Outlook will remain bullish as long as 1.7062 resistance turned support (2023 high) holds even in case of deep pullback.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6199) holds, this second leg could still extend higher. However, firm break of the above mention 1.8744 projection level with strong momentum will argue that it's indeed resuming the up trend from 1.1602 (2012 low).

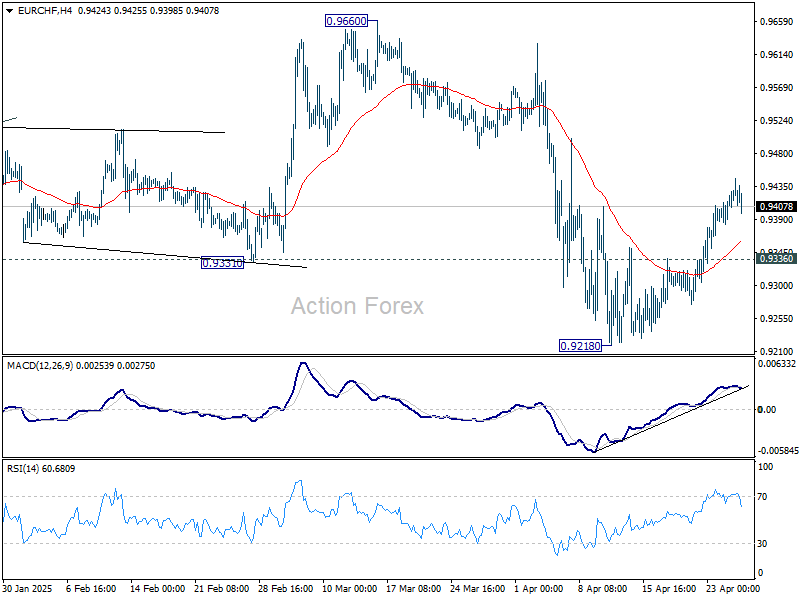

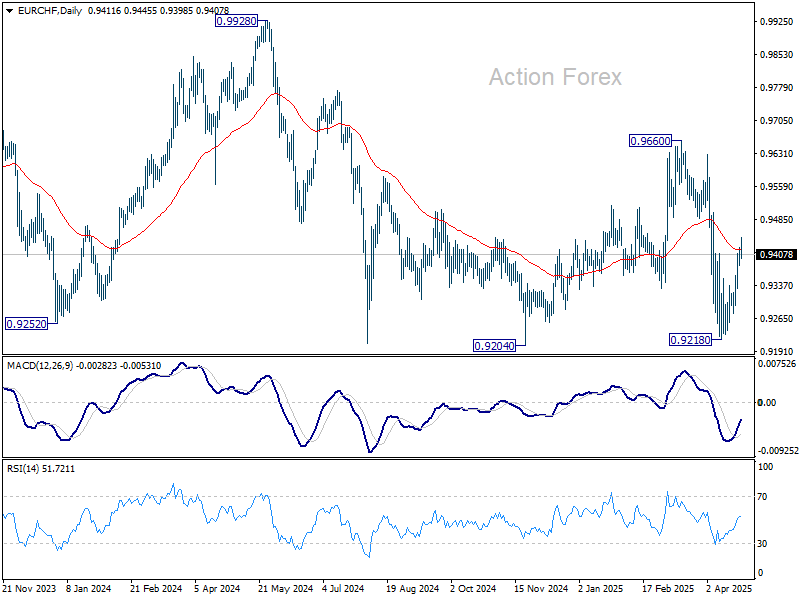

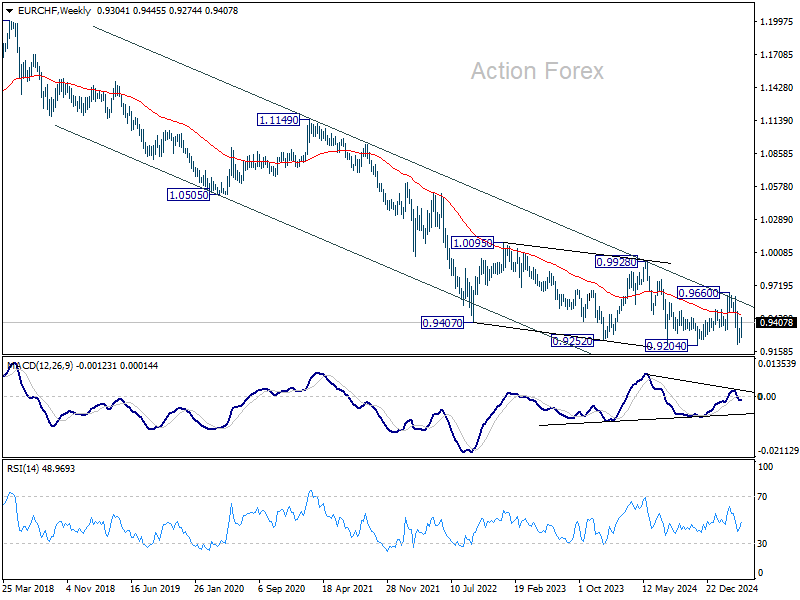

EUR/CHF Weekly Outlook

EUR/CHF's stronger than expected rebound last week suggests that fall from 0.9660 has already completed at 0.9218, ahead of 0.9204 low. Rebound from 0.9218 is either a corrective move, or the third leg of the pattern from 0.9204. In either case, further rally is expected this week as long as 0.9336 support holds, towards 0.9660. However, break of 0.9336 will bring retest of 0.9204/18 support zone.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9555) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

In the long term picture, overall long term down trend is still in force in EUR/CHF. Outlook will continue to stay bearish as long as 55 M EMA (now at 0.9962) holds.

Global Risk Sentiment Brightens, But Caution Lingers Around US Assets

Global risk sentiment showed further improvement last week, with stock markets around the world posting impressive gains. Although headlines continued to focus on the confusing state of U.S.-China trade tensions, there was quiet but notable progress on multiple trade fronts, including US talks with Japan, South Korea and India.

US equities rebounded alongside the global rally even though they still lack the decisive momentum needed to confirm that a durable bottom has been established. European markets, on the other hand, painted a far more encouraging picture.

The strength of the rebound in European equities suggests that the worst of the April selloff may already be behind us. Moreover, there is a growing sense that the sharpest phase of the tariff crisis has passed, and that incremental improvements could take root from here.

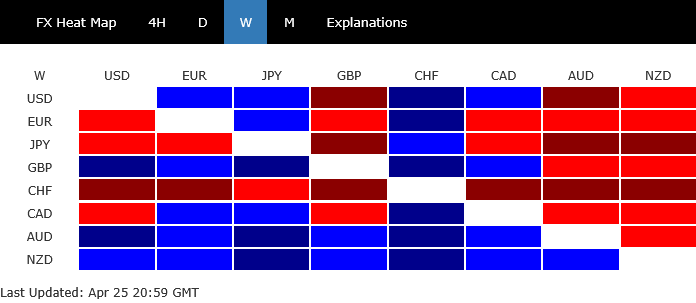

The shift in sentiment was clearly reflected in the currency markets too. Kiwi ended the week as the strongest performer, followed by Aussie and Sterling. All three currencies benefited from the rebound in risk appetite, with investors rotating out of safe-haven assets and into higher-yielding or growth-linked currencies. On the other end, the safe-haven trio—Swiss Franc, Yen, and Euro—underperformed, as investors rotated away from defensive assets amid easing fears. Dollar and Loonie finished in the middle of the pack.

While the equity rally suggests a return of broader risk appetite, investor interest in US assets has yet to fully recover. This is likely due to ongoing concerns over U.S. policy consistency and the uncertain path for trade negotiations. Until clearer signals emerge from Washington and stronger technical confirmations develop in US stock markets, Dollar may continue to lag behind the recovery seen elsewhere.

Markets Rally on Trade Progress, But Major Hurdles with China and EU Remain

Global stock markets extended their strong rally last week. There seems to be growing optimism that the worst phase of the tariff crisis may be behind us, at least for now. Trade negotiations appear to be picking up momentum across several fronts, offering hope for partial resolutions. Recent economic data, particularly PMI surveys from the Eurozone and the US, suggest that businesses have been bracing well for uncertainty, cushioning the blow from trade tensions.

In an interview with Time magazine on Friday, US President Donald Trump said he expects "many" trade deals to fall into place over the next three to four weeks. Positive signals are emerging from several bilateral channels too. Japan’s Economy Minister Ryosei Akazawa is set to visit Washington this week for a second round of talks. US Treasury Secretary Scott Bessent has hinted that a US-South Korea trade deal could be finalized as early as next week. US and India are reported to have agreed on the terms for a bilateral deal covering trade in goods, services, and critical sectors like e-commerce and minerals. Switzerland also announced it was among a group of 15 countries given "somewhat preferential treatment" in tariff talks, with Swiss President Karin Keller-Sutter indicating that the 90-day truce could be extended for active negotiating partners.

However, not all fronts are moving smoothly. Despite initial discussions, talks between the US and the EU have yet to yield tangible compromises. Progress remains slow, even in setting a basic framework for formal negotiations. The slow movement with Europe highlights that achieving broad global de-escalation is far from guaranteed.

Meanwhile, the situation with China remains the murkiest. Rumors continue to swirl about informal discussions, but no clear confirmation has been provided by either side. Trump insists that some communication with Beijing is ongoing, while Chinese officials deny that any talks are happening. Although there were earlier hopes for de-escalation, Trump has reiterated that tariffs on China will remain in place unless "they give us something substantial."

Without a clear breakthrough or even a defined negotiation channel, US-China trade tensions remain a major overhang for global markets, tempering some of the broader optimism.

European Strength Offers Hope, Caution Persists for US Indexes

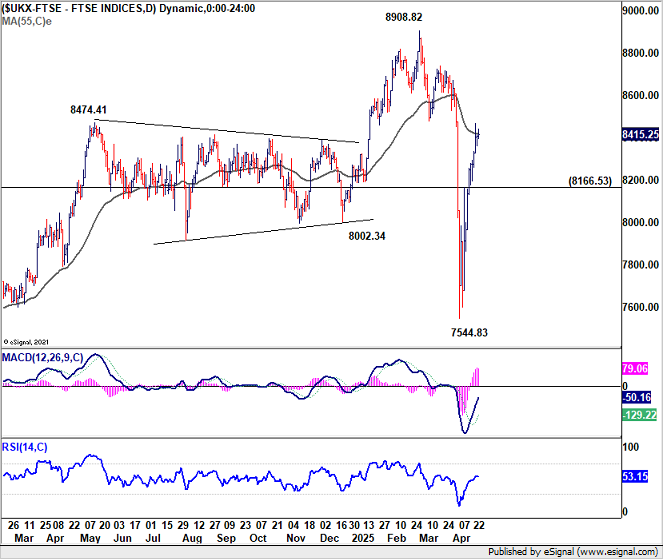

While US stocks have staged a strong rebound recently, the technical backdrop remains somewhat unconvincing. The recovery lacks decisive confirmation, particularly in DOW. In contrast, the outperformance seen in European markets is offering hope that the worst of the market correction could already be behind us. Particularly in the UK and Germany, technical signals suggest that early April's steep selloff may have been a medium-term shakeout rather than the start of a long-term bearish trend.

In the UK, FTSE 's breach of 55 D EMA (now at 8420.51) and break of 55 W EMA (now at 8260.66) suggest that corrective fall from 8900.82 has already completed at 7554.83. Price actions from 8908.82 is likely just a medium term consolidations pattern, rather than a long term bearish trend reversal. The range of the consolidations should be set between 38.2% retracement of 4898.79 to 8902.82 at 7376.99 and 8908.82.

Nevertheless, for the near term, while further rise could be seen as long as 8166.53 support holds, FTSE should start to lose momentum above 55 D EMA.

Germany’s DAX tells a similar story. The index’s corrective fall from the 23476.01 has likely completed at 18489.91. What we are seeing now is a medium-term consolidation rather than a full trend reversal. The range is set between 38.2% retracement of 8255.65 to 23476.01 at 17661.83 and 23476.01.

For the near term, further rise is in favor as long as 21044.61 support hold. But DAX should lose momentum as it approaches 23476.01 high.

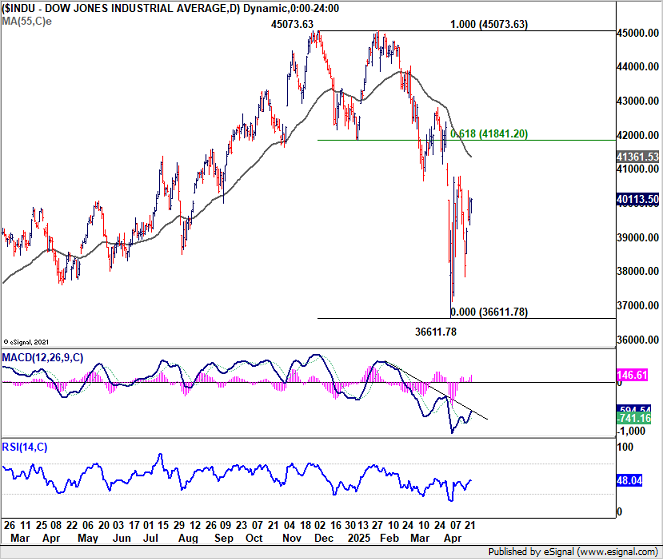

Turning to the US, developments in Europe suggest that DOW may eventually find solid support from 38.2% retracement of 18213.65 to 45073.63 at 34813.12 to contain downside even in case of another fall, should another selloff occur. Still, firm break of 55 D EMA (now at 41361.53) is needed to indicate that fall from 45703.63 has completed. Or risk will remain on the downside for the near term.

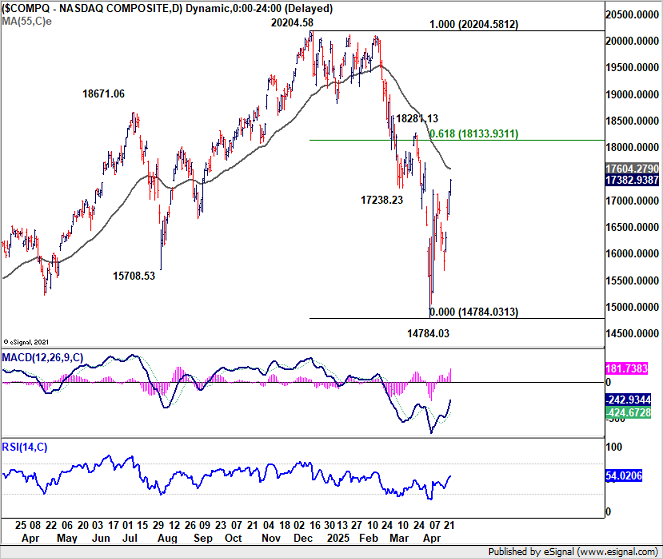

NASDAQ's picture is a little bit more promising than DOW. Firm break of 55 D EMA (now at 17604.27) will indicate that fall from 2024.58 has completed at 14783.03, after defending 38.2% retracement of 6631.42 to 20204.58 at 15019.63. That should set the range for medium term consolidations for NASDAQ.

Dollar Struggles Despite Risk Stabilization, Policy Uncertainty Remains a Drag

While risk sentiment has shown signs of stabilizing in global markets, and even hints at a return of risk appetite, this does not necessarily imply a renewed interest in US assets. In particular, both the Dollar and US. Treasuries continue to face headwinds until investors see more policy consistency from the Trump administration. Markets remain wary of abrupt shifts in trade policy, tariff threats, and broader economic strategies, which cloud the overall investment climate for Dollar-based assets.

Another important factor is the evolving US trade balance. Should the Trump administration succeed in narrowing the US trade deficit, there could be a meaningful structural impact on the demand for Dollar-denominated assets. A narrower deficit would mean fewer surplus Dollars circulating abroad to be recycled into US Treasuries and other assets, potentially pushing yields higher and softening the Dollar's appeal at the same time, particularly if fiscal deficits remain large.

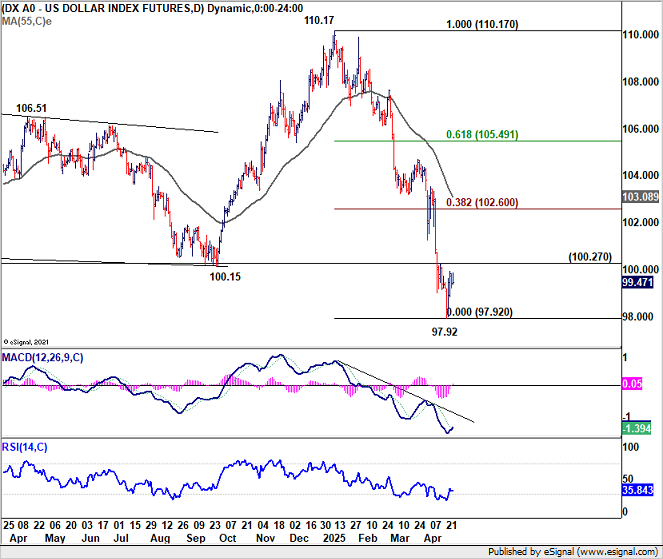

Technically, Dollar Index's recovery from 97.92 short term bottom is lacking decisive momentum. As long as 100.27 resistance holds, near term risk will remain on the downside for another fall through 97.92 sooner rather than later. Break of 97.92 will pave the way to 100% projection of 114.77 to 99.57 from 110.17 at 94.97 next.

Nevertheless, firm break of 100.27 would set the stage for stronger rebound to 38.2% retracement of 110.17 to 97.92 at 102.60, even still as a corrective move.

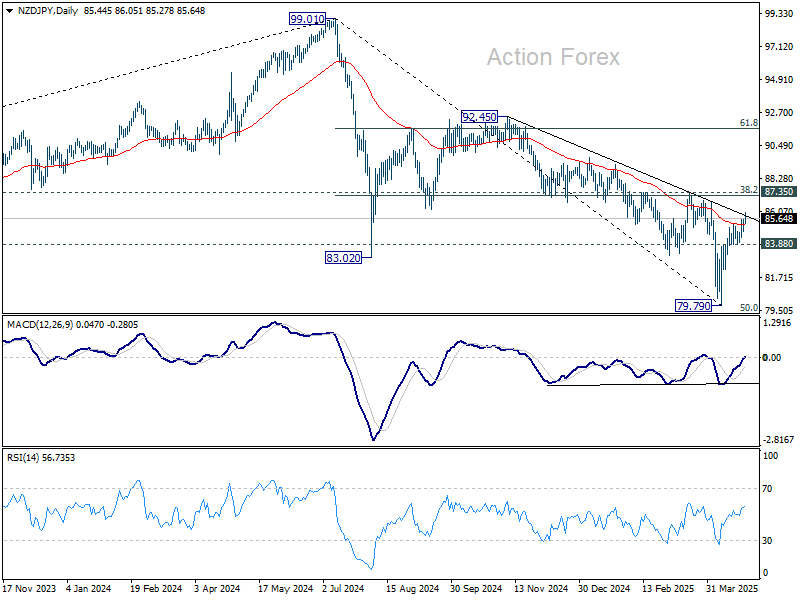

NZD/JPY Extends Rebound, Bullish Reversal Hinges on 87.35 Break

NZD/JPY extended the rebound from 79.79 last week as risk sentiment continued to improve. The breach of falling trend line resistance is a tentative sign that fall from 92.45 has completed at 79.79. Further rise is now in favor as long as 83.88 support holds.

On the upside, decisive break of 87.35 cluster resistance (38.2% retracement of 99.01 to 79.79 at 87.13) will argue that corrective decline from 99.01 has already completed too. Further rally should then be seen to 61.8% retracement at 91.66.

However, rejection by 87.13/35 will keep near term outlook bearish. Break of 83.88 support will bring retest of 79.79, and possibly resumption of the down trend from 99.01 too.

EUR/CHF Weekly Outlook

EUR/CHF's stronger than expected rebound last week suggests that fall from 0.9660 has already completed at 0.9218, ahead of 0.9204 low. Rebound from 0.9218 is either a corrective move, or the third leg of the pattern from 0.9204. In either case, further rally is expected this week as long as 0.9336 support holds, towards 0.9660. However, break of 0.9336 will bring retest of 0.9204/18 support zone.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9555) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

In the long term picture, overall long term down trend is still in force in EUR/CHF. Outlook will continue to stay bearish as long as 55 M EMA (now at 0.9962) holds.

Summary 4/28 – 5/2

Monday, Apr 28, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 10:00 | GBP | CBI Realized Sales Apr | -20 | -41 |

| 23:01 | GBP | BRC Shop Price Index Y/Y Apr | -0.20% | -0.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 10:00 | GBP | CBI Realized Sales Apr | |

| Forecast: -20 | Previous: -41 | ||

| 23:01 | GBP | BRC Shop Price Index Y/Y Apr | |

| Forecast: -0.20% | Previous: -0.40% | ||

Tuesday, Apr 29, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | EUR | Germany GfK Consumer Sentiment May | -26 | -24.5 |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Mar | 4.00% | 4.00% |

| 09:00 | EUR | Eurozone Economic Sentiment Apr | 94.5 | 95.2 |

| 09:00 | EUR | Eurozone Industrial Confidence Apr | -10.7 | -10.6 |

| 09:00 | EUR | Eurozone Services Sentiment Apr | 2.4 | |

| 09:00 | EUR | Eurozone Consumer Confidence Apr F | -16.7 | -16.7 |

| 12:30 | USD | Goods Trade Balance (USD) Mar P | -146.3B | -147.9B |

| 12:30 | USD | Wholesale Inventories Mar P | 0.70% | 0.30% |

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Feb | 4.80% | 4.70% |

| 13:00 | USD | Housing Price Index M/M Feb | 0.30% | 0.20% |

| 14:00 | USD | Consumer Confidence Apr | 87.1 | 92.9 |

| 23:50 | JPY | Industrial Production M/M Mar P | -0.70% | 2.30% |

| 23:50 | JPY | Retail Trade Y/Y Mar | 3.60% | 1.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | EUR | Germany GfK Consumer Sentiment May | |

| Forecast: -26 | Previous: -24.5 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Mar | |

| Forecast: 4.00% | Previous: 4.00% | ||

| 09:00 | EUR | Eurozone Economic Sentiment Apr | |

| Forecast: 94.5 | Previous: 95.2 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Apr | |

| Forecast: -10.7 | Previous: -10.6 | ||

| 09:00 | EUR | Eurozone Services Sentiment Apr | |

| Forecast: | Previous: 2.4 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Apr F | |

| Forecast: -16.7 | Previous: -16.7 | ||

| 12:30 | USD | Goods Trade Balance (USD) Mar P | |

| Forecast: -146.3B | Previous: -147.9B | ||

| 12:30 | USD | Wholesale Inventories Mar P | |

| Forecast: 0.70% | Previous: 0.30% | ||

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Feb | |

| Forecast: 4.80% | Previous: 4.70% | ||

| 13:00 | USD | Housing Price Index M/M Feb | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 14:00 | USD | Consumer Confidence Apr | |

| Forecast: 87.1 | Previous: 92.9 | ||

| 23:50 | JPY | Industrial Production M/M Mar P | |

| Forecast: -0.70% | Previous: 2.30% | ||

| 23:50 | JPY | Retail Trade Y/Y Mar | |

| Forecast: 3.60% | Previous: 1.40% | ||

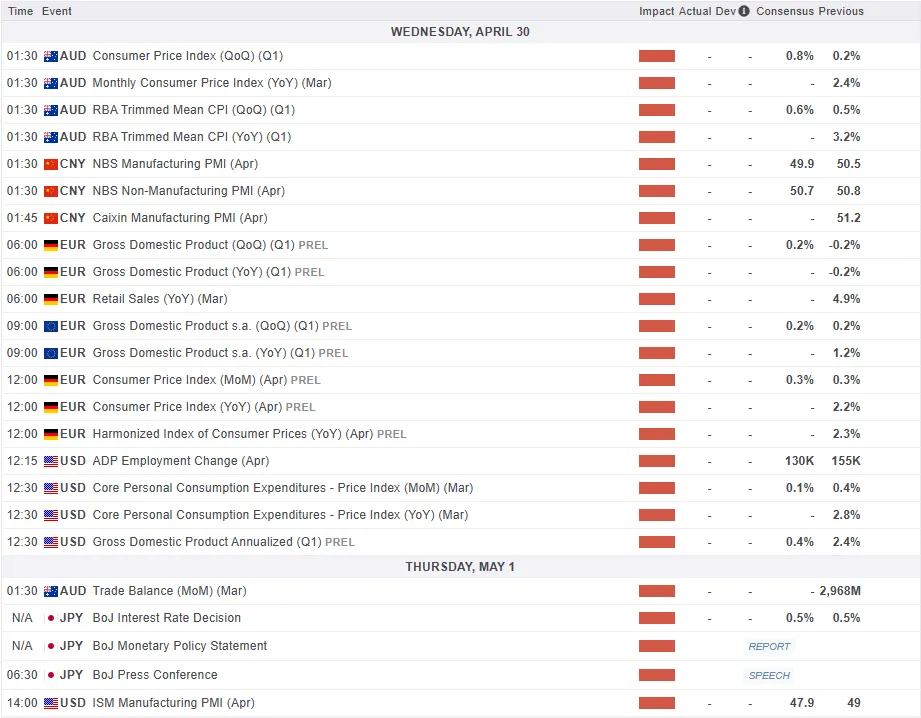

Wednesday, Apr 30, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence Apr | 57.5 | |

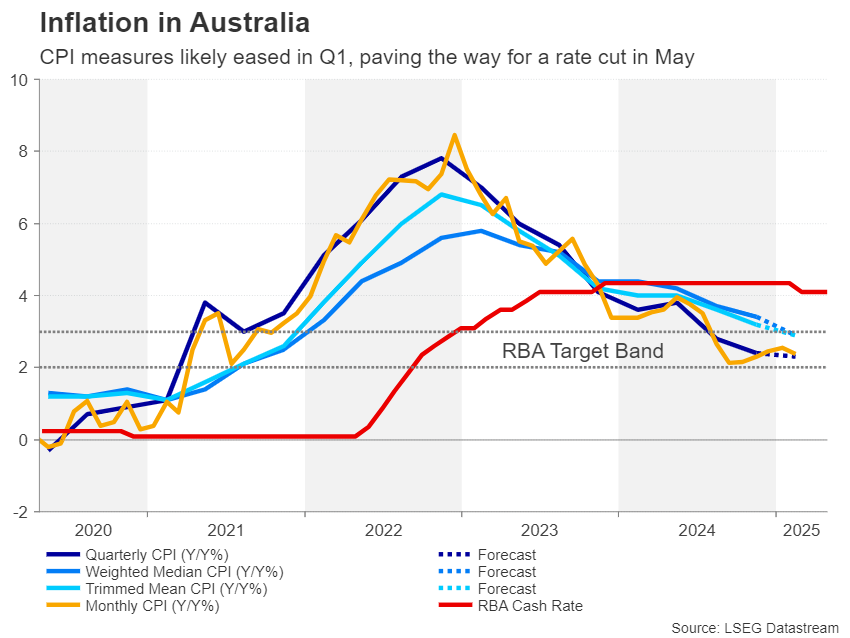

| 01:30 | AUD | Monthly CPI Y/Y Mar | 2.20% | 2.40% |

| 01:30 | AUD | CPI Q/Q Q1 | 0.80% | 0.20% |

| 01:30 | AUD | CPI Y/Y Q1 | 2.20% | 2.40% |

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q1 | 0.80% | 0.50% |

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q1 | 3.20% | |

| 01:30 | CNY | NBS Manufacturing PMI Apr | 49.9 | 50.5 |

| 01:30 | CNY | NBS Non-Manufacturing PMI Apr | 50.7 | 50.8 |

| 01:45 | CNY | Caixin Manufacturing PMI Apr | 49.9 | 51.2 |

| 05:00 | JPY | Housing Starts Y/Y Mar | 1.00% | 2.40% |

| 06:00 | EUR | Germany Import Price Index M/M Mar | -0.70% | 0.30% |

| 06:00 | EUR | Germany Retail Sales M/M Mar | -0.40% | 0.80% |

| 06:45 | EUR | France GDP Q/Q Q1 P | 0.10% | -0.10% |

| 07:00 | CHF | KOF Economic Barometer Apr | 102 | 103.9 |

| 07:55 | EUR | Germany Unemployment Change Mar | 15K | 26K |

| 07:55 | EUR | Germany Unemployment Rate Mar | 6.30% | 6.30% |

| 08:00 | EUR | Germany GDP Q/Q Q1 P | 0.20% | -0.20% |

| 08:00 | CHF | UBS Economic Expectations Apr | -10.7 | |

| 09:00 | EUR | Eurozone GDP Q/Q Q1 P | 0.20% | 0.20% |

| 12:00 | EUR | Germany CPI M/M Apr P | 0.30% | |

| 12:00 | EUR | GermanyCPI Y/Y Apr P | 2.20% | |

| 12:15 | USD | ADP Employment Change Apr | 130K | 155K |

| 12:30 | CAD | GDP M/M Feb | 0.40% | |

| 12:30 | USD | GDP Annualized Q1 P | 0.40% | 2.40% |

| 12:30 | USD | GDP Price Index Q1 P | 2.30% | |

| 12:30 | USD | Employment Cost Index Q1 | 0.90% | 0.90% |

| 13:45 | USD | Chicago PMI Apr | 45.9 | 47.6 |

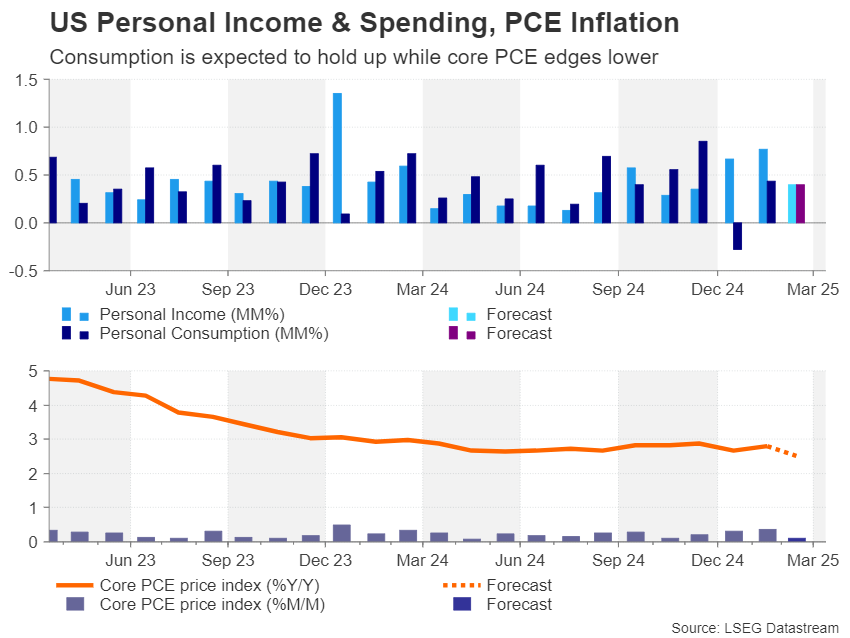

| 14:00 | USD | Personal Income M/M Mar | 0.40% | 0.80% |

| 14:00 | USD | Personal Spending Mar | 0.60% | 0.40% |

| 14:00 | USD | PCE Price Index M/M Mar | 0.30% | |

| 14:00 | USD | PCE Price Index Y/Y Mar | 2.50% | |

| 14:00 | USD | Core PCE Price Index M/M Mar | 0.10% | 0.40% |

| 14:00 | USD | Core PCE Price Index Y/Y Mar | 2.80% | |

| 14:00 | USD | Pending Home Sales M/M Mar | -0.30% | 2% |

| 14:30 | USD | Crude Oil Inventories | 0.2M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence Apr | |

| Forecast: | Previous: 57.5 | ||

| 01:30 | AUD | Monthly CPI Y/Y Mar | |

| Forecast: 2.20% | Previous: 2.40% | ||

| 01:30 | AUD | CPI Q/Q Q1 | |

| Forecast: 0.80% | Previous: 0.20% | ||

| 01:30 | AUD | CPI Y/Y Q1 | |

| Forecast: 2.20% | Previous: 2.40% | ||

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q1 | |

| Forecast: 0.80% | Previous: 0.50% | ||

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q1 | |

| Forecast: | Previous: 3.20% | ||

| 01:30 | CNY | NBS Manufacturing PMI Apr | |

| Forecast: 49.9 | Previous: 50.5 | ||

| 01:30 | CNY | NBS Non-Manufacturing PMI Apr | |

| Forecast: 50.7 | Previous: 50.8 | ||

| 01:45 | CNY | Caixin Manufacturing PMI Apr | |

| Forecast: 49.9 | Previous: 51.2 | ||

| 05:00 | JPY | Housing Starts Y/Y Mar | |

| Forecast: 1.00% | Previous: 2.40% | ||

| 06:00 | EUR | Germany Import Price Index M/M Mar | |

| Forecast: -0.70% | Previous: 0.30% | ||

| 06:00 | EUR | Germany Retail Sales M/M Mar | |

| Forecast: -0.40% | Previous: 0.80% | ||

| 06:45 | EUR | France GDP Q/Q Q1 P | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 07:00 | CHF | KOF Economic Barometer Apr | |

| Forecast: 102 | Previous: 103.9 | ||

| 07:55 | EUR | Germany Unemployment Change Mar | |

| Forecast: 15K | Previous: 26K | ||

| 07:55 | EUR | Germany Unemployment Rate Mar | |

| Forecast: 6.30% | Previous: 6.30% | ||

| 08:00 | EUR | Germany GDP Q/Q Q1 P | |

| Forecast: 0.20% | Previous: -0.20% | ||

| 08:00 | CHF | UBS Economic Expectations Apr | |

| Forecast: | Previous: -10.7 | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q1 P | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 12:00 | EUR | Germany CPI M/M Apr P | |

| Forecast: | Previous: 0.30% | ||

| 12:00 | EUR | GermanyCPI Y/Y Apr P | |

| Forecast: | Previous: 2.20% | ||

| 12:15 | USD | ADP Employment Change Apr | |

| Forecast: 130K | Previous: 155K | ||

| 12:30 | CAD | GDP M/M Feb | |

| Forecast: | Previous: 0.40% | ||

| 12:30 | USD | GDP Annualized Q1 P | |

| Forecast: 0.40% | Previous: 2.40% | ||

| 12:30 | USD | GDP Price Index Q1 P | |

| Forecast: | Previous: 2.30% | ||

| 12:30 | USD | Employment Cost Index Q1 | |

| Forecast: 0.90% | Previous: 0.90% | ||

| 13:45 | USD | Chicago PMI Apr | |

| Forecast: 45.9 | Previous: 47.6 | ||

| 14:00 | USD | Personal Income M/M Mar | |

| Forecast: 0.40% | Previous: 0.80% | ||

| 14:00 | USD | Personal Spending Mar | |

| Forecast: 0.60% | Previous: 0.40% | ||

| 14:00 | USD | PCE Price Index M/M Mar | |

| Forecast: | Previous: 0.30% | ||

| 14:00 | USD | PCE Price Index Y/Y Mar | |

| Forecast: | Previous: 2.50% | ||

| 14:00 | USD | Core PCE Price Index M/M Mar | |

| Forecast: 0.10% | Previous: 0.40% | ||

| 14:00 | USD | Core PCE Price Index Y/Y Mar | |

| Forecast: | Previous: 2.80% | ||

| 14:00 | USD | Pending Home Sales M/M Mar | |

| Forecast: -0.30% | Previous: 2% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 0.2M | ||

Thursday, May 1, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

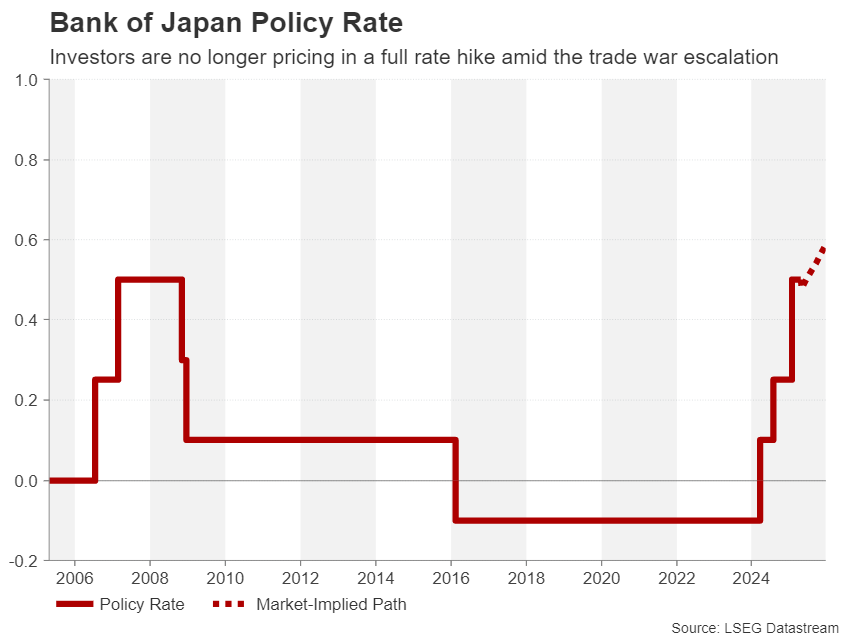

| JPY | BoJ Interest Rate Decision | 0.50% | 0.50% | |

| 00:30 | JPY | Manufacturing PMI Apr F | 48.5 | 48.5 |

| 01:30 | AUD | Import Price Index Q/Q Q1 | 0.30% | 0.20% |

| 01:30 | AUD | Trade Balance (AUD) Mar | 3.10B | 2.97B |

| 05:00 | JPY | Consumer Confidence Index Apr | 34 | 34.1 |

| 06:30 | CHF | Real Retail Sales Y/Y Mar | 1.90% | 1.60% |

| 08:30 | GBP | M4 Money Supply M/M Mar | 0.20% | 0.20% |

| 08:30 | GBP | Mortgage Approvals Mar | 65K | 65K |

| 08:30 | GBP | Manufacturing PMI Apr F | 44 | 44 |

| 11:30 | USD | Challenger Job Cuts Y/Y Apr | 204.80% | |

| 12:30 | USD | Initial Jobless Claims (Apr 25) | 221K | 222K |

| 13:30 | CAD | Manufacturing PMI Apr | 46.3 | |

| 13:45 | USD | Manufacturing PMI Apr F | 50.7 | 50.7 |

| 14:00 | USD | ISM Manufacturing PMI Apr | 47.9 | 49 |

| 14:00 | USD | ISM Manufacturing Prices Paid Apr | 70.2 | 69.4 |

| 14:00 | USD | ISM Manufacturing Employment Apr | 44.7 | |

| 14:00 | USD | ISM Manufacturing New Orders Index Apr | 45.2 | |

| 14:00 | USD | Construction Spending M/M Mar | 0.30% | 0.70% |

| 14:30 | USD | Natural Gas Storage | 88B | |

| 22:45 | NZD | Building Permits M/M Mar | 0.70% | |

| 23:50 | JPY | Monetary Base Y/Y Apr | -2.00% | -3.10% |

| 23:30 | JPY | Unemployment Rate Mar | 2.40% | 2.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| JPY | BoJ Interest Rate Decision | ||

| Forecast: 0.50% | Previous: 0.50% | ||

| 00:30 | JPY | Manufacturing PMI Apr F | |

| Forecast: 48.5 | Previous: 48.5 | ||

| 01:30 | AUD | Import Price Index Q/Q Q1 | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 01:30 | AUD | Trade Balance (AUD) Mar | |

| Forecast: 3.10B | Previous: 2.97B | ||

| 05:00 | JPY | Consumer Confidence Index Apr | |

| Forecast: 34 | Previous: 34.1 | ||

| 06:30 | CHF | Real Retail Sales Y/Y Mar | |

| Forecast: 1.90% | Previous: 1.60% | ||

| 08:30 | GBP | M4 Money Supply M/M Mar | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 08:30 | GBP | Mortgage Approvals Mar | |

| Forecast: 65K | Previous: 65K | ||

| 08:30 | GBP | Manufacturing PMI Apr F | |

| Forecast: 44 | Previous: 44 | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Apr | |

| Forecast: | Previous: 204.80% | ||

| 12:30 | USD | Initial Jobless Claims (Apr 25) | |

| Forecast: 221K | Previous: 222K | ||

| 13:30 | CAD | Manufacturing PMI Apr | |

| Forecast: | Previous: 46.3 | ||

| 13:45 | USD | Manufacturing PMI Apr F | |

| Forecast: 50.7 | Previous: 50.7 | ||

| 14:00 | USD | ISM Manufacturing PMI Apr | |

| Forecast: 47.9 | Previous: 49 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Apr | |

| Forecast: 70.2 | Previous: 69.4 | ||

| 14:00 | USD | ISM Manufacturing Employment Apr | |

| Forecast: | Previous: 44.7 | ||

| 14:00 | USD | ISM Manufacturing New Orders Index Apr | |

| Forecast: | Previous: 45.2 | ||

| 14:00 | USD | Construction Spending M/M Mar | |

| Forecast: 0.30% | Previous: 0.70% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 88B | ||

| 22:45 | NZD | Building Permits M/M Mar | |

| Forecast: | Previous: 0.70% | ||

| 23:50 | JPY | Monetary Base Y/Y Apr | |

| Forecast: -2.00% | Previous: -3.10% | ||

| 23:30 | JPY | Unemployment Rate Mar | |

| Forecast: 2.40% | Previous: 2.40% | ||

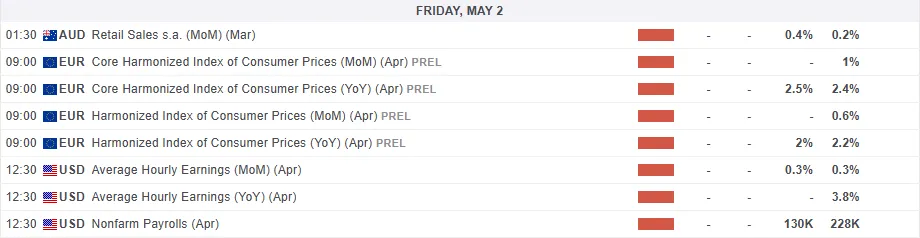

Friday, May 2, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Retail Sales M/M Mar | 0.40% | 0.20% |

| 01:30 | AUD | PPI Q/Q Q1 | 0.80% | |

| 01:30 | AUD | PPI Y/Y Q1 | 3.70% | |

| 07:30 | CHF | Manufacturing PMI Apr | 48.7 | 48.9 |

| 07:50 | EUR | France Manufacturing PMI Apr F | 48.2 | 48.2 |

| 07:55 | EUR | Germany Manufacturing PMI Apr F | 48 | 48 |

| 08:00 | EUR | Eurozone Manufacturing PMI Apr F | 48.7 | 48.7 |

| 08:00 | EUR | ECB Economic Bulletin | ||

| 09:00 | EUR | Eurozone Unemployment Rate Mar | 6.10% | 6.10% |

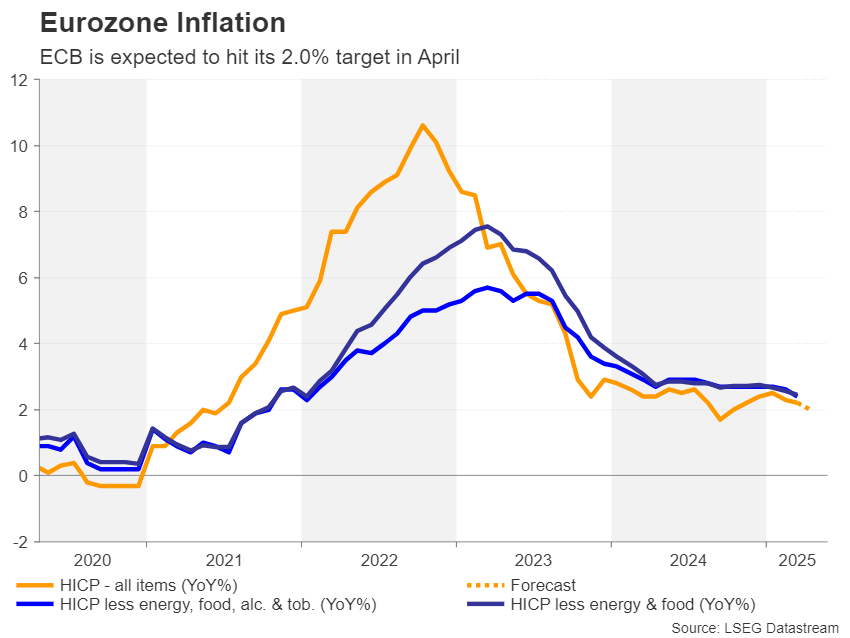

| 09:00 | EUR | Eurozone CPI Y/Y Apr P | 2.10% | 2.20% |

| 09:00 | EUR | Eurozone CPI Core Y/Y Apr P | 2.50% | 2.40% |

| 12:30 | USD | Nonfarm Payrolls Apr | 130K | 228K |

| 12:30 | USD | Average Weekly Hours Apr | 34.2 | 34.2 |

| 12:30 | USD | Unemployment Rate Apr | 4.20% | 4.20% |

| 12:30 | USD | Average Hourly Earnings M/M Apr | 0.30% | 0.30% |

| 14:00 | USD | Factory Orders M/M Mar | 4.20% | 0.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Retail Sales M/M Mar | |

| Forecast: 0.40% | Previous: 0.20% | ||

| 01:30 | AUD | PPI Q/Q Q1 | |

| Forecast: | Previous: 0.80% | ||

| 01:30 | AUD | PPI Y/Y Q1 | |

| Forecast: | Previous: 3.70% | ||

| 07:30 | CHF | Manufacturing PMI Apr | |

| Forecast: 48.7 | Previous: 48.9 | ||

| 07:50 | EUR | France Manufacturing PMI Apr F | |

| Forecast: 48.2 | Previous: 48.2 | ||

| 07:55 | EUR | Germany Manufacturing PMI Apr F | |

| Forecast: 48 | Previous: 48 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Apr F | |

| Forecast: 48.7 | Previous: 48.7 | ||

| 08:00 | EUR | ECB Economic Bulletin | |

| Forecast: | Previous: | ||

| 09:00 | EUR | Eurozone Unemployment Rate Mar | |

| Forecast: 6.10% | Previous: 6.10% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Apr P | |

| Forecast: 2.10% | Previous: 2.20% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Apr P | |

| Forecast: 2.50% | Previous: 2.40% | ||

| 12:30 | USD | Nonfarm Payrolls Apr | |

| Forecast: 130K | Previous: 228K | ||

| 12:30 | USD | Average Weekly Hours Apr | |

| Forecast: 34.2 | Previous: 34.2 | ||

| 12:30 | USD | Unemployment Rate Apr | |

| Forecast: 4.20% | Previous: 4.20% | ||

| 12:30 | USD | Average Hourly Earnings M/M Apr | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 14:00 | USD | Factory Orders M/M Mar | |

| Forecast: 4.20% | Previous: 0.60% | ||

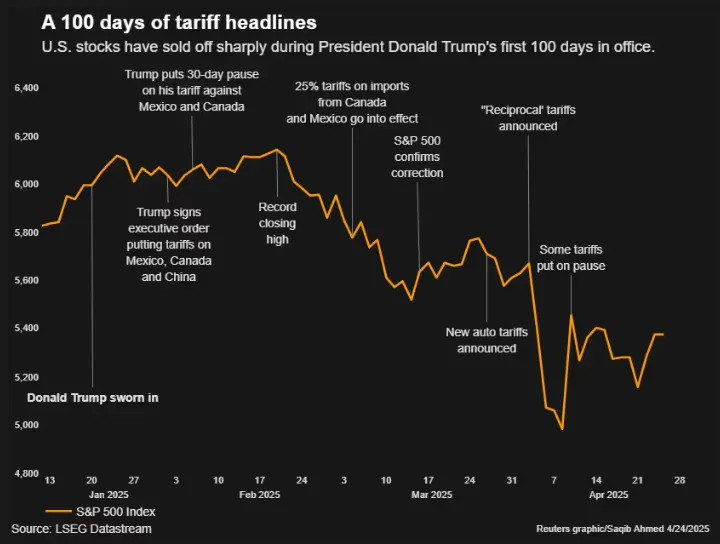

Markets Weekly Outlook – Data Dump Ahead as Tariff Concerns Linger

- Global stocks saw a positive week due to easing US-China trade war concerns, despite mixed messages from President Trump.

- Gold experienced a decline as safe haven flows decreased, while Bitcoin saw a significant increase.

- The US Dollar Index is aiming for its first weekly gain since mid-March but remains vulnerable below the 100.00 level.

- The upcoming week is packed with high-impact data releases from Asia Pacific, Europe, UK, and the US, potentially raising recession fears.

Week in review: Trump and Bessent eye China deal as markets grow optimistic

Global stocks ended the week on a solid note as early week concerns around Federal Reserve independence and the ongoing US-China trade war dissipated. President Trump and Treasury Secretary Bessent have tempered rhetoric as they eye a deal with China.

The comments by both parties went a long way to restoring some confidence in the market and this has seen a notable shift in sentiment. Risk assets have risen at a steady pace for the majority of the week, while safe haven flows have taken a knock.

Friday saw US equities largely muted as market participants continue to wait for more information on the US-China situation. The mood remained somewhat uneasy after the US President Donald Trump said he would see it as a "total victory" if tariffs on foreign imports reach 50% within a year.

He also mentioned talks with China about a tariff deal and claimed Chinese President Xi Jinping had called him, though Beijing denies any negotiations are happening. The mixed messages dampened some optimism, which had been boosted by China granting exemptions on the steep 125% tariffs for certain U.S. imports.

Despite the uncertainty on Friday, all in all market participants should see this as a positive week.

At the time of writing the S&P 500 has gained 4% this week, while the Nasdaq is up 5.6% and the Dow has risen 2.4%. The increases are largely due to hopes that U.S.-China trade tensions may ease.

The overall Mood remains cautious as the economic outlook worsens and tariffs hurt company earnings. The benchmark index remains below levels prior to the April 2 announcement, and is over 10% off its February record close.

Source: LSEG

The dollar was set for its first weekly gain since mid-March on Friday, influenced by mixed signals about U.S.-China relations improving. It rose 0.82% against the yen to 143.775 and 0.42% against the Swiss franc to 0.82985. Meanwhile, the euro dropped 0.24% to $1.1363, and the pound fell 0.12% to $1.332, despite unexpectedly strong UK retail sales.

On the commodities front, Gold has struggled as safe haven flows have slowed down this week. The early week flurry which sent Gold to $3500/oz has disappeared as hopes of a trade deal escalate.

Gold is trading down 1.6% for the week and on course to print a massive shooting star candlestick close on the weekly timeframe. This does not bode well for bulls especially if any trade deals are struck or announced over the weekend or early next week.

For now, a return to the weekly high at $3500/oz may require an escalation in trade tensions once more, otherwise the level may remain out of reach in the short term.

Bitcoin has been a big beneficiary this past week with the world's largest crypto benefiting from the improved sentiment. At the time of writing Bitcoin is up around 10% for the week.

Oil prices dropped on Friday and were on track for a weekly loss of over 2%, as markets expected an oversupply. Fears around oversupply were exacerbated when some OPEC+ members proposed increasing oil production again in June, according to a report earlier this week.

The week ahead: Shortened trading week brings a host of data releases

The upcoming week will be a busy one with a barrage of high impact data releases scheduled. There are also lingering concerns around tariffs which are unlikely to dissipate soon.

President Trump said on Friday that he expects trade deals in the next three to four weeks which leaves the door open for further twists and turns in the saga.

Asia Pacific Markets

It will be a busy week for the Asia Pacific region with high impact data from Japan, China and Australia all on the agenda.

In Japan, the Bank of Japan (BoJ) is expected to keep interest rates unchanged for now, despite high inflation and uncertainty about U.S. trade policies. However, it is likely to indicate plans for rate hikes in the coming months.

It's a busy week in China as a potential trade deal with the US comes into focus. Beyond that markets are eagerly watching for the first PMI data since tariff conflicts worsened. On Sunday, China will release industrial profits data, which will show if profits turned positive after falling 0.3% year-on-year in the first two months. On Wednesday, China’s official and Caixin PMIs will reveal how tariffs have affected the manufacturing sector.

In the Pacific region we have some inflation data for Q1 being released in Australia. The RBA prefers the quarterly data as it provides a more stable view of inflationary trends. Markets expect CPI to rise due to higher food and electricity costs, even though service prices have slightly decreased.

Europe + UK + US

In developed markets, it will be a huge week for US data. Next week’s U.S. data could raise recession fears. Consumer confidence is expected to drop as households worry about rising prices from tariffs, job losses, and potential government benefit cuts. Falling investments and wealth are making people spend less

A weak first-quarter GDP report is likely. A surge in imports earlier this year, driven by fears of tariffs, may have hurt growth. Consumer spending and investments in March likely kept the economy growing, but future quarters may be worse.

April's jobs report will show slower hiring due to economic uncertainty. Layoffs remain rare, but slower job growth could slightly increase unemployment as more people look for jobs than the market can absorb.

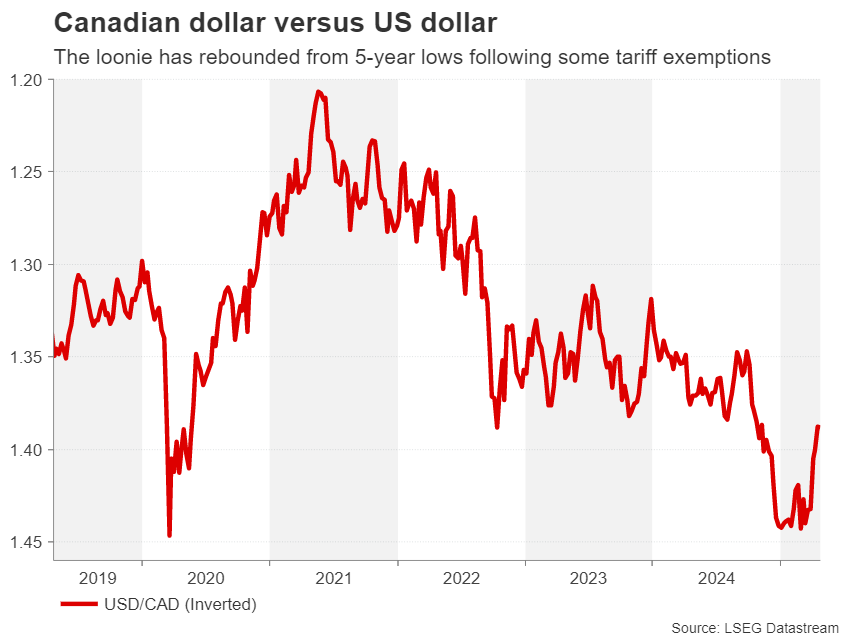

Canada's election has taken an unexpected turn after Donald Trump suggested making Canada the 51st U.S. state. The Conservative Party has lost support, while the Liberal Party has gained momentum under its new leader, Mark Carney, former head of the Bank of Canada and the Bank of England. The winner will have to tackle the economic impact of a trade war, as 75% of Canada’s exports go to the U.S.

Europe also has a busy week ahead with a host of high impact data releases. Euro GDP preliminary numbers for Q1 will be released on Wednesday 09:00am GMT time.

The week will come to a close on Friday with Eurozone CPI preliminary numbers. Markets are expecting a slight uptick on the YoY print to 2.5% from a previous print of 2.4%.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Week - US Dollar Index (DXY)

This week's focus remains on the US Dollar Index.

The index is on course for its first weekly gain since mid-March but the index looks set to close below a key level of 99.57.

Without a break above the 100.00 key psychological level the DXY remains vulnerable to further downside.

Immediate resistance rests at 100.00, 100.61 and 101.18.

Looking at key areas of support and we have the 99.00 handle, 98.30 and of course the 97.70.

US Dollar Index (DXY) Daily Chart - March 28, 2025

Source: TradingView.Com (click to enlarge)

The Weekly Bottom Line: Searching for the Signal Amidst A Lot Of Noise

Canadian Highlights

- Next Monday’s federal election will be the show stealer. The Liberals are ahead in the polls, and if they do indeed prevail, we could see more government spending than what we baked into our forecast.

- Even with a potential government stimulus boost, the economy is still likely poised to sour in the coming months. We expect that will lead the Bank of Canada to trim its policy rate.

- February was a soft month for consumer retail spending. March looks to have been a firmer month, but we’re retaining our view that consumption is headed for a slowdown.

U.S. Highlights

- Trade tensions between the world’s two largest economies simmered this week, with the U.S. administration hinting that the tariffs on China would likely be lowered in the very near future.

- But President Trump appeared frustrated with the lack of progress among other countries, and threatened to reimpose the reciprocal tariffs in the coming weeks if trade deals weren’t signed.

- Amidst all the uncertainty, the housing recovery appears to be on hold. Existing home sales declined to a six-month low in March.

Canada – Election Anticipation

Some optimism returned to Canadian financial markets this week. Equities breathed a sigh of relief, with the TSX on track to rise about 2.5% on the week. President Trump signaled a de-escalation of the U.S. trade war with China and assured that he would retain Federal Reserve chief Powell, despite disagreeing with his stance on monetary policy (to put it lightly). Bond yields were also slightly higher at time of writing, although the Canadian dollar dipped a touch on the back of some upward movement in the USD. It wasn’t completely smooth sailing, however, with the U.S. President warning that the 25% tariff in place on cars imported from Canada could go up. He also re-iterated some of his grievances with his northern neighbour when questioned about the upcoming Canadian election.

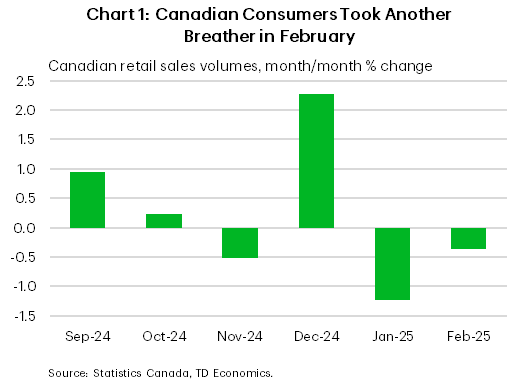

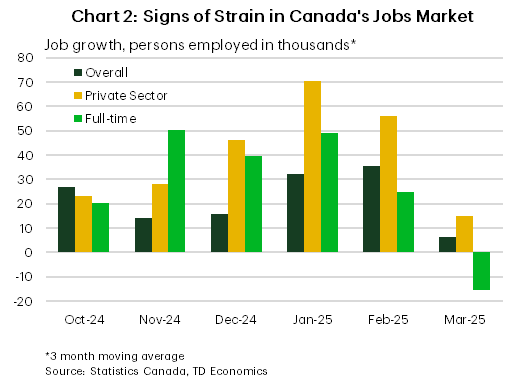

This week also offered a pulse-check on the state of the Canadian consumer via the February retail spending report, and the results were less than encouraging. Retail sales volumes declined 0.4% month-on-month, pulled down by weakness in new vehicle purchases (which continued to pullback after surging in the back half of last year) and housing-related sales (mirroring the weakness in the housing market). Some of the drop in overall sales volumes may have been weather-related given major winter storms that took place that month. Still, it marked the second straight monthly decline (Chart 1). Statcan’s flash estimate showed a 0.7% m/m rebound in March, but given all of the headwinds facing the consumer, we still expect spending growth to cool moving forward.

All eyes are on next Monday’s federal election. It’s a two-horse race between the Liberals and Conservatives, with both parties releasing their costed platforms this week. Net new stimulus measures in the Liberal plans amount to an average of about 1% of GDP over the forecast horizon, driven by spending and abetted by tax cuts. In contrast, tax reductions are the name of the game for the Conservatives, with relief pledged for household incomes, housing, and seniors to name a few. On the opposite side of the ledger, the Conservatives are pledging to scale back spending slightly, instead leaning on a bevy of tax cuts to support the economy and, ultimately, grow revenues. The Liberal plan sees the deficit averaging about 1.7% of GDP over the next several years. It’s lower under the Conservative plan, but the party included a projected boost to revenues from the anticipated lift to economic growth from their new measures, which is something the Liberals largely didn’t do.

As of now, polling and betting markets are leaning towards a Liberal victory. If that occurs, there is some upside risk to our assumption that fiscal stimulus across all levels of government would amount to 1% of GDP. All else equal, a larger-than-expected dose of government stimulus could offer a boost to the economy. However, a large chunk of new spending in the Liberal plan is capital investment, and so could take longer to have an impact on the economy as projects take time to get up and running. More importantly, the economy is likely to sour in short order, with next week’s GDP report set to show that growth softened in February and Canada’s labour market already displaying signs of cooling (Chart 2). As such, the Bank of Canada remains on course to trim their policy rate in the coming months.

U.S. – Searching for the Signal Amidst A Lot Of Noise

Disentangling the signal from the noise on U.S. trade matters is becoming an increasingly difficult task. This week, President Trump and U.S. Treasury Secretary Scott Bessent both called out the tariffs on China as being “too high”. At 145%, Bessent said trade with China becomes “unsustainable” and that he expects the current situation to de-escalate in the “very near future”. China appears open to negotiations and even went as far as exempting some U.S. goods from its retaliatory tariffs. The abrupt U-turn in the administration’s tone alongside President Trump’s assurance that he will not remove Fed Chair Powell, helped to fuel a mid-week rally in U.S. equities, with the S&P 500 ending the week up 3.5%. But investors remained skeptical of whether the move to de-escalate was the beginning of a broader pivot or simply backpedaling on the overly punitive levies imposed on China given the significant economic repercussions.

Despite claims of over 90 countries having offered to negotiate trade terms, President Trump appears to be growing frustrated with the lack of progress made on reaching deals. He even went as far threatening to re-impose the “reciprocal” tariffs on some countries over the coming weeks if trade deals weren’t signed.

But even if there’s a big push on trade negotiations over the coming weeks, at least some economic damage has already been done. In the April release of the Federal Reserve’s Beige Book, several districts noted a considerable worsening in the economic outlook amid heightened uncertainty stemming from tariffs. Spending on both business and leisure travel were down, with some districts seeing an outright decline in international visitors. On inflation, many businesses noted that they’re already seeing input costs rise and that they expect to pass-on at least some of the additional costs to consumers. But this may not be possible for some consumer-facing sectors, who are already reporting more tepid demand.

Estimates done by Reuters suggest that of the S&P 500 companies who have already reported quarterly earnings, over 90% have mentioned tariff risks in their earnings transcripts. This is more than double what was mentioned the prior quarter and underscores how today’s uncertainty is touching nearly all industries. This does not bode well for capital spending.

The housing recovery is also looking to be on hold. Existing home sales declined 5.9% m/m in March, falling to a six-month low of 4.0 million units (Chart 1). With mortgage rates again within spitting distance of 7%, and households increasingly worried about employment prospects, we’re likely to see a further pullback in sales activity over the coming months. Construction activity was also sharply lower in March, amid elevated trade uncertainty and higher input costs. Homebuilder confidence for April remained soft, suggesting little rebound in near future.

Our current tracking for first quarter real GDP (released April 30th) suggests economic growth grew by just 0.3% annualized after expanding by an above trend pace of 2.9% through the second half of 2024 (Chart 2). But the GDP release will play second fiddle to next week’s more timely April jobs report. Expectations are that the economy added 130k jobs in April, a meaningful stepdown from March’s 228k pace.

Weekly Economic & Financial Commentary: Fed Remains in a Holding Pattern

Summary

United States: Holding the Line

- Hard economic data broadly remain resilient and continue to hold the line, even as sentiment and survey data show trade-policy-induced uncertainty is a foremost concern. Regional purchasing manager indexes and the Beige Book were weighed down by the uncertain outlook, while durable goods orders came in stronger than expected.

- Next week: Q1 GDP (Wed.), ISM Manufacturing Index (Thu.), Employment (Fri.)

International: European Sentiment Underwhelms Amid Heightened Uncertainty

- Compared to recent weeks' headlines and market turbulence, this was somewhat of a lighter week in terms of international economic data. To start, we got the April Eurozone PMIs this week, and the results were generally underwhelming, contributing at the margin to our view that the risks are tilted toward more European Central Bank easing than we currently forecast. The United Kingdom PMIs were notably soft, possibly signaling lackluster growth prospects for the economy.

- Next week: China PMIs (Wed.), Eurozone PMIs (Wed.), Bank of Japan Policy Rate (Thu.)

Interest Rate Watch: Fed Remains in a Holding Pattern

- The tone from this week's Fedspeak maintained the majority opinion the FOMC held at its March meeting—a desire to hold rates steady on account of above-target inflation and elevated uncertainty. It appears most officials are comfortable waiting to assess the comprehensive impact of pending policy shifts before making further adjustments to the federal funds rate.

Topic of the Week: Déjà Vu

- President Trump suggested that tariffs on China may be reduced if the two nations reach a fair deal. Although it’s hard to know exactly what such a deal might look like, U.S.-China Phase One and Phase Two trade agreement negotiations during the president’s first term offer some insight. Our expectation is that U.S. tariffs on China will be brought down from their current extraordinary levels but will remain elevated above historical norms.

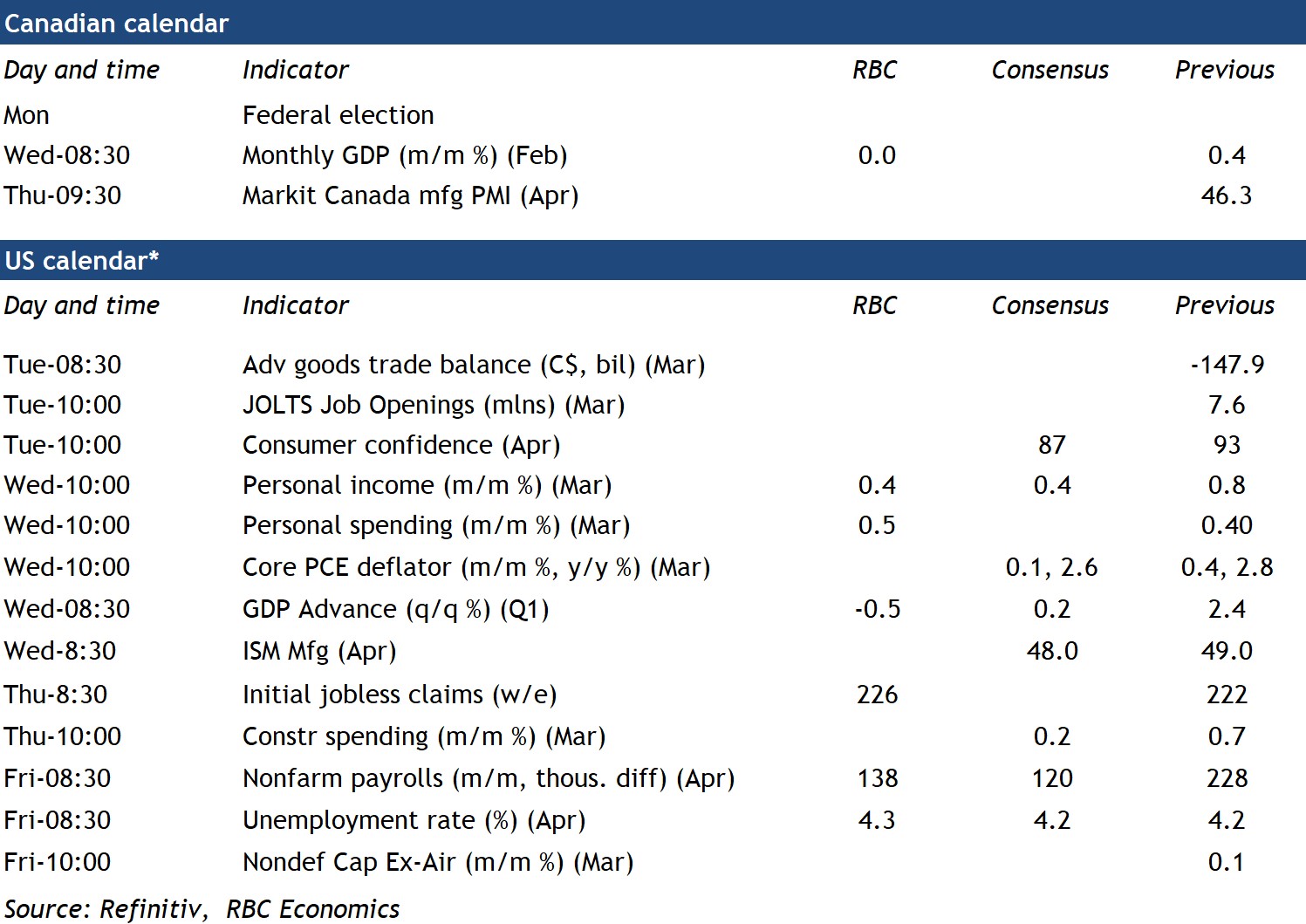

Canada’s Elections Put North American GDP Data in Focus

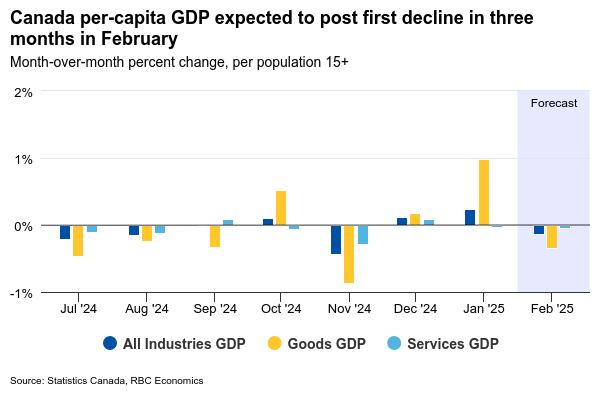

With Canadians heading to the polls on Monday, we’re watching February’s gross domestic product report on Wednesday, including an early estimate for March, for clues on what type of economy the next government inherits as tariff headwinds continue to build.

We expect a flat reading for February GDP—broadly in line with Statistics Canada’s early estimate a month ago that showed output was “essentially unchanged,” which is a sharp slowing from a 0.4% increase in January and ending a two month run of per-capita increases.

This cooling is expected to be broad-based across sectors, but also reflects a 6% drop in non-conventional oil extraction. Home resales also pulled back more than 7% as a drop in consumer confidence coupled with severe winter weather in parts of the country caused potential buyers to delay purchases. Meanwhile, manufacturing output likely held largely steady and retail sale volumes fared better than feared given plunging consumer confidence.

The preliminary estimate for March GDP could look softer. Employment declined by 33,000 in March—the largest decline in three years—and, the unemployment rate ticked higher. The advance estimate of March retail sales was higher (+0.7%), likely boosted in part by a rush to buy vehicles ahead of auto tariffs in April. But the early estimate of March manufacturing sales was down 1.9%, potentially reflecting the early impact of tariffs imposed in early in the month.

In the United States, we expect GDP edged outright lower in Q1—in part due to a pull-back in net trade as imports surged ahead of new tariffs, but consumer spending growth also slowed sharply, potentially to a rate below 1% for the first time since 2020.

Tariffs represent a significant risk to the U.S. economy, but it is likely too early to see a significant pullback in labour markets. Jobless claims remain low and early indicators of hiring demand from online job postings are not flagging a sharp decline into early April. We expect payroll employment rose by 138,000 in March with the unemployment rate ticking up to 4.3%.

Week ahead data watch

Week Ahead: US GDP, Inflation and Jobs in Focus Amid Tariff Mess – BoJ Meets

- Barrage of US data to shed light on US economy as tariff war heats up.

- GDP, PCE inflation and nonfarm payrolls reports to headline the week.

- Bank of Japan to hold rates but may downgrade growth outlook.

- Eurozone and Australian CPI also on the agenda, Canadians go to the polls.

Trump continues to sow tariff confusion

There was finally some relief for financial markets in the past week when US President Trump offered investors a rare glimmer of hope that there is light at the end of the trade war tunnel. However, it didn’t take long for the light to start dimming again as the trade conflict took another complicated turn after it became apparent that the Trump administration’s climbdown in the standoff against China isn’t as big as previously anticipated.

Trump’s carrot-and-stick approach in his bid to get China onto the negotiating table isn’t proving very effective, particularly when the carrot is much smaller than the stick. For Beijing, the trade war has escalated to a level where national pride is at stake, hence, it is not blinking as easily as Trump assumed it would. This is already posing a problem for the White House, which has signalled that the Trump administration is willing to lower the exorbitant 145% tariff rate within two-three weeks if there is a deal.

But according to Chinese officials, the two sides have not even started talks, casting doubt on Trump’s negotiating tactic. Furthermore, other concessions, for example on auto tariffs for US car manufacturers, are far from a done deal, with Trump even threatening to raise them for auto imports from Canada.

All this is only worsening the uncertainty for US businesses rather than offering some clarity. So, although the acknowledgement by the White House that it is keeping an eye on the market turbulence and Trump is keen to reach trade agreements with America’s main trading partners is a positive sign, it does little in terms of easing the immediate fears about the country’s economic prospects.

Dollar and Wall Street on recession watch

Those concerns will either be fuelled or reduced in the coming week, as there’s a flurry of top-tier economic releases on the way. Kicking things off on Tuesday are the consumer confidence index for April and JOLTS job openings for March. On Wednesday, the advance estimate for GDP growth will be monitored very closely amid some predictions that the US economy contracted in the first quarter.

The Atlanta Fed’s GDPNow model is estimating an annualized drop of 2.2% in GDP, but analysts according to a Reuters poll are forecasting growth of 0.4%, down sharply from the Q4 pace of 2.4%.

The ADP employment survey is also out on Wednesday, along with the latest PCE inflation and consumption numbers. The all-important core PCE price index is expected to have risen by 0.1% month-on-month in March to give an annual figure of 2.5%, which would be a decrease from the prior 2.8%.

Personal consumption is forecast to have maintained month-on-month growth of 0.4%, suggesting that US households continue to spend at a healthy clip.

Other data on Wednesday will include the Chicago PMI as well as pending home sales. On Thursday, the Challenger Layoffs for April might attract some attention but the bigger focus that day will be the ISM manufacturing PMI. The index is expected to have declined in April from 49.0 to 47.9, with investors also likely to track the direction of the employment and prices sub-indices.

The real highlight, however, will be Friday’s nonfarm payrolls report, amid the intense speculation about how soon the Fed will cut rates. Jobs growth is projected to have slowed from 228k in March to 130k in April, with the unemployment rate staying unchanged at 4.2%. Average earnings probably grew by 0.3% in April.

A disappointing NFP print, combined with a soft core PCE reading could bolster expectations of a 25-basis-point rate cut in June as opposed to July, though bets for the May meeting would likely remain very low. For the US dollar, a worrying set of data would almost certainly be negative, but on Wall Street, stocks could rise if increased rate cut hopes are not overshadowed by recession fears.

BoJ to keep rates steady as outlook deteriorates

The Bank of Japan is not anticipated to announce any changes to its monetary policy settings when it meets on Thursday, as policymakers take time to assess the impact of Donald Trump’s tariffs on the Japanese economy before deciding whether to hike interest rates again.

Inflation in Japan edged up to 3.2% y/y in March as per the core CPI measure and the BoJ remains confident that the recent wage growth momentum is now becoming more sustainable. However, the downside risks to growth have increased markedly since February when Trump unleashed the first of many waves of tariffs, with Japan not being spared from the universal 10% levies, nor the sectoral tariffs on steel and autos.

The BoJ is therefore expected to lower its growth forecasts in its latest quarterly Outlook Report. The question is whether the Bank will also cut its inflation projections or keep them more or less unchanged. Policymakers don’t think at this stage that tariffs pose a significant danger to their inflation goal so they will probably keep the door to future rate hikes wide open.

If Governor Ueda goes a step further and explicitly signals that further rate hikes are likely in the coming months, this could boost the yen, which is enjoying strong safe-haven demand lately.

In terms of data, the preliminary industrial output for March is due on Wednesday, to be followed by some jobs stats on Friday.

Euro looks to flash GDP and CPI as uptrend stalls

The flash PMI numbers for April painted a grim picture for the Eurozone economy as businesses were hit by a new round of duties. With the impact of the US tariffs on global trade only now being felt, investors will probably ignore the preliminary GDP figures for the first quarter that are out on Wednesday.

Even if the euro area notched up impressive growth in the first three months of the year, this is unlikely to dampen rate cut expectations for the European Central Bank as inflation is falling and growth forecasts are being downgraded. ECB policymakers have already slashed rates by a total of 175 bps and have strongly hinted that they’re not done yet.

If Friday’s flash CPI data shows that inflationary pressures continue to subside, the ECB will have little reason to pause. The headline rate of CPI moderated to 2.2% y/y in March and is forecast to ease further to 2.0% in April.

The euro could come under some pressure if the CPI prints are on the soft side, but the primary driver in the FX domain will be the US dollar, and specifically, sentiment towards Trump’s trade policies. Fresh efforts by the White House to defuse tensions could spur another bounce in the US dollar, setting back the euro’s uptrend.

Australian CPI may not alter RBA bets

Inflation will also be in the spotlight in Australia where the quarterly CPI readings will be published on Wednesday. The Reserve Bank of Australia has only cut rates once during this cycle amid slow progress in getting inflation under control.

The monthly measure dipped from 2.5% to 2.4% y/y in February in a huge relief after rising for three consecutive months. The quarterly figure covering the first three months of 2025 is expected to inch lower too. But for the RBA, the underlying gauges of CPI might be more important. If they extend their decline in Q1 and the monthly rate also falls, there would be nothing stopping the RBA from cutting rates in May.

However, this may not necessarily trigger much reaction in the Australian dollar, as a 25-bps rate cut is already fully priced in for May and for almost every other meeting in the remainder of the year.

Aussie traders will also be watching the manufacturing PMIs out of China for any signs that the steep US levies are hurting the world’s second largest economy. Both the official and Caixin manufacturing PMIs are due on Wednesday.

Canadians to likely pick Carney as next PM

Canadians will be voting in a general election on Monday after former Bank of England and Bank of Canada governor Mark Carney called a snap vote following Justin Trudeau’s resignation. Carney’s Liberal party was all set to lose the election until Trump’s trade tirade reinvigorated the party among voters.

Trudeau’s and Carney’s handling of Trump’s threats to Canada’s economy as well as its sovereignty appear to have earned them plaudits, pushing the Liberals ahead of the Conservatives, who were poised for victory before the trade war escalation.

There’s still room for surprises, however, as the Liberals may fail to win a majority, and with their current coalition partners, the New Democratic Party, expected to lose most of its seats, a hung parliament may not go down well with Canada’s stock market and the local dollar.

But should the Liberals secure a majority, the Canadian dollar could gain slightly, although it’s likely to benefit more from a shock Conservative win, as they’ve pledged bigger tax cuts.