Sample Category Title

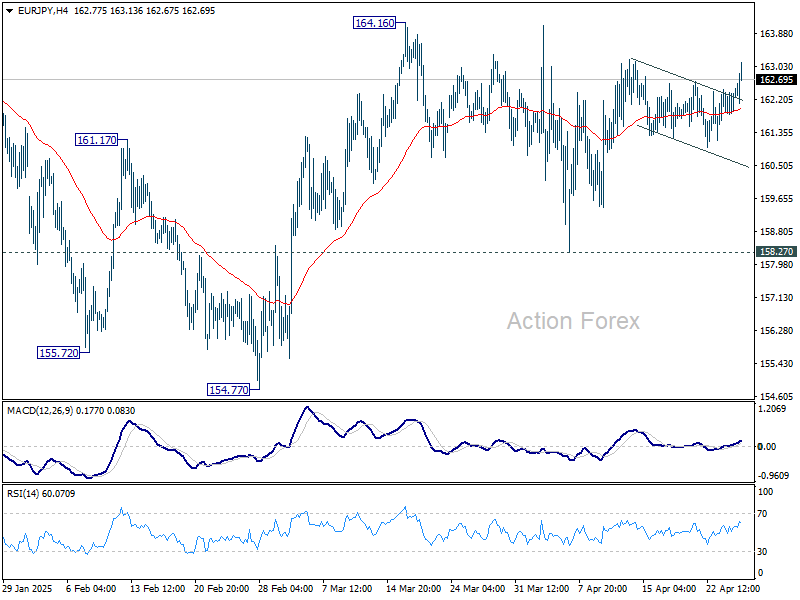

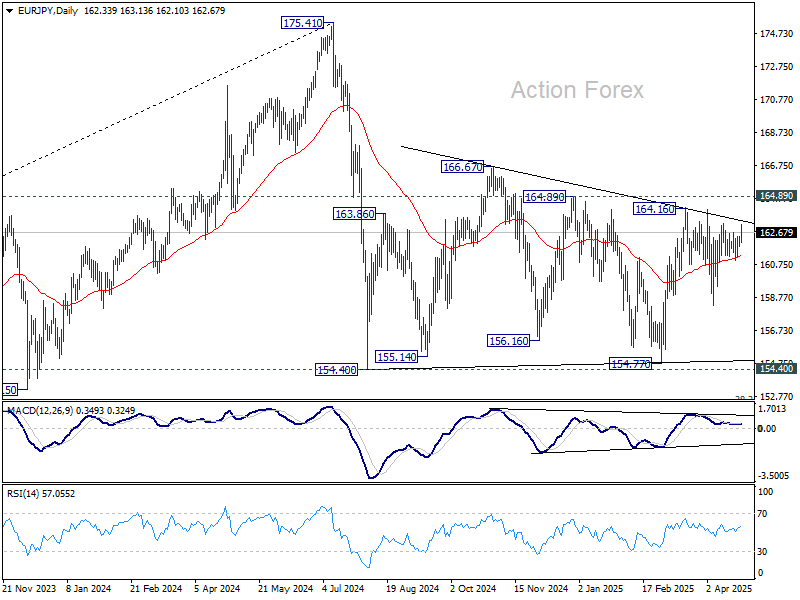

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.01; (P) 162.27; (R1) 162.71; More...

Range trading continues in EUR/JPY and outlook is unchanged. Intraday bias remains neutral. On the upside, above 164.16 will resume the rally from 154.77 to 164.89 resistance, and then 166.67. However, decisive break of 158.27 support will bring deeper decline back to 154.77 support. Overall, sideway consolidation pattern from 154.40 is still extending.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

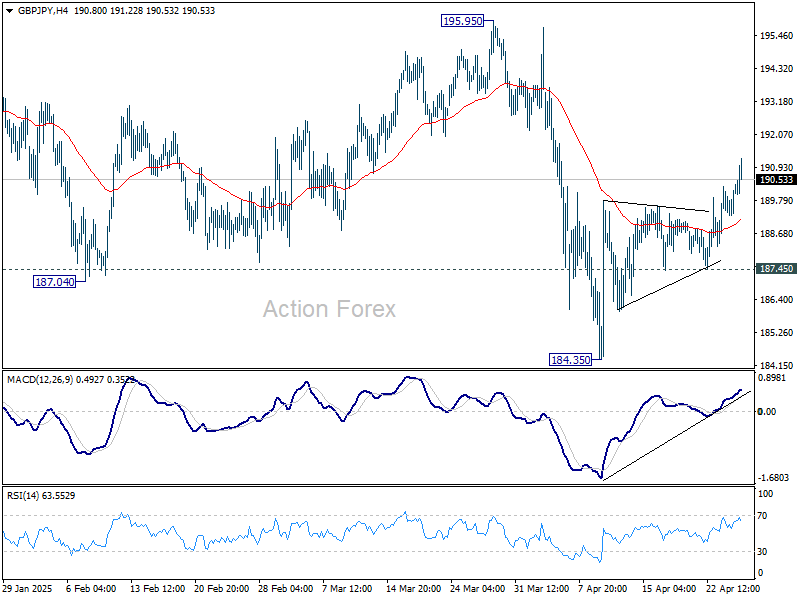

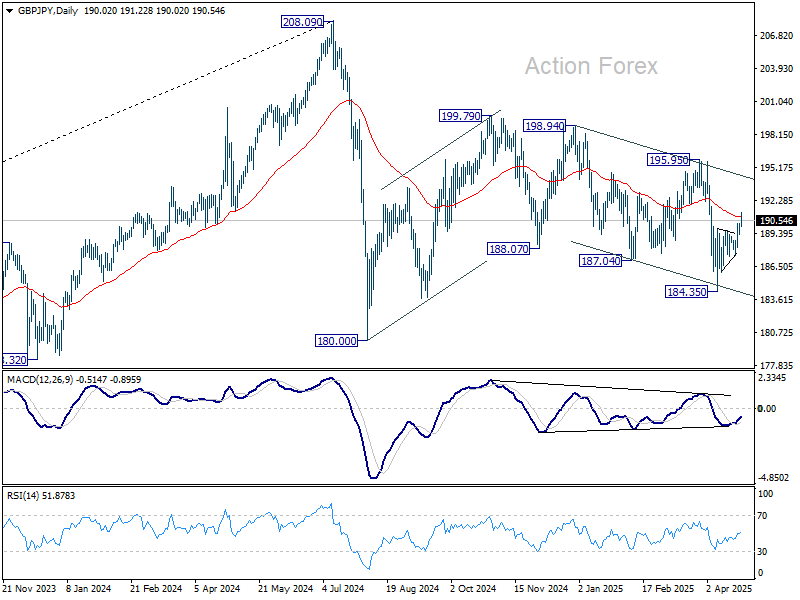

GBP/JPY Daily Outlook

Daily Pivots: (S1) 189.57; (P) 189.98; (R1) 190.65; More...

GBP/JPY's rebound from 184.35 extended higher today and break of 190.06 resistance suggests that fall from 195.95 has completed already. Intraday bias is back on the upside for 195.95 resistance next. Firm break there will argue that whole choppy decline from 199.79 has finished too. On the downside, below 187.45 will bring retest of 184.35 support instead.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

WTI Crude Oil Remains Bearish on Oversupply Fears

- Recently suffering its worst 6-day performance in over three years, WTI crude oil has recently found support, trading ~15% higher than lows made earlier this month

- Currently trading around $63.65 per barrel, WTI will need to break resistance held around $66.07 to extend rally from lows

- Fresh US sanctions on Iranian energy exports could raise some questions on global supply, with no recent progress made on nuclear negotiations

With recent weeks hallmarked by a less-than-stellar economic outlook coupled with a low market appetite for risk, the consequent fallout has been decisively negative for world oil prices.

Having already surrendered gains made earlier this year, concerns about the future of global trade, compounded by fears of a potential supply glut, have recently spelled trouble for oil, falling to multi-year lows of around $55.23 per barrel (WTI) on April 9th.

A chart showing the recent price action of WTICOUSD. OANDA, TradingView, 25/04/2024.

Having since found support amid a brief period of comparative market optimism, WTI will need to break resistance around $66.07 to extend gains further.

WTI: Trump, “Liberation Day” & US-China tensions

With the consumption of oil inextricably linked to industry, manufacturing, and general economic prosperity, recent announcements regarding tariffs and the associated disruption in trade were felt in full force by the oil markets.

Following the announcement of reciprocal tariffs on April 2nd, otherwise known as “Liberation Day”, uncertainty on the future of global trade, and a potential for escalating trade wars would send WTI prices into a tailspin, achieving fresh lows unseen since 2021.

Having agreed to a 90-day pause in reciprocal tariffs since, WTI pricing has been able to stablise, hoping that Trump and his administration can successfully reach amicable trade agreements with key trading partners, like the European Union and China.

The latter is not only currently subject to a 145% levy on most imports to the United States, but also the second-highest consumer of oil globally, making any developments in US-China trade agreements particularly poignant for the future of WTI.

At the time of writing, the White House has made some suggestions that progress is being made on this front, but only time will tell what the likely terms of this agreement could be.

As for WTI pricing, any suggestion of a further expansion of trade tariffs or worsening of trade relations will likely negatively impact oil pricing in the short term, with the opposite being true if the US can reach agreements with key trading partners.

WTI: OPEC tensions

With tensions high amid a slump in oil manufacturing profitability, recent OPEC policy that maintains a commitment to an increase in production has come under scrutiny by some party members.

Most noticeably, this comes by way of Kazakhstan, which recently made commitments to prioritise ‘national interest’ rather than the demands of OPEC+. Ranking 12th in world oil production last year, Kazakhstan will not be the first to exceed production quotas, with non-compliance a rising issue amongst ranks.

With US oil inventories falling in Wednesday’s session, markets now turn their attention to OPEC’s next meeting scheduled for May 5th.

WTI: United States sanctions on Iranian energy exports

With sanctions targeting Iranian energy exports recently renewed, some questions are to be asked regarding how recent developments will affect oil supply in the Middle East.

Having previously offered relief from sanctions when compliant with the United States' demands to limit its nuclear program, recent sanctions have expanded in scope to now cover Liquid Petroleum Gas (LPG), a key export of the Iranian economy.

While discussions are ongoing, markets will remain tentative. Any suggestion of disruption to supply could positively affect WTI pricing.

WTI: Technical analysis & outlook

With price failing to break above the 21-day daily EMA in Wednesday’s session, the short-term outlook for WTI remains bearish. Currently trading in a period of consolidation, if price breaks below the ~$62.51 level, we can likely expect further moves to the downside

When using the ADX on the daily timeframe, trend strength is observed to be falling, but remains a ‘strong trend’. All other factors being the same, this suggests the current bearish trend is set to continue in the short term

Markets Saw Some ‘Openings’ Fed Could Give More Weight to Labour Market

Markets

Market sentiment these days is fluid and conditional to all kinds of headlines. For once, during yesterday’s session, the ‘news flow-headlines-rumours combo’ protractedly moved from a hesitant start toward a risk-on session. US indices closed the session with gains from 1.23% (Dow) to 2.74% (Nasdaq). On the trade war, the best news was that there were no new negative headlines from the US administration. Even more, US President Trump said that his administration was having talks with China on trade (admittedly even as this was denied by China). Still market saw this as another sign of potential (US-sided) de-escalation. On the monetary policy front, markets saw some ‘openings’ that the Fed in its dual mandate (over time) could give some more weight to labour market developments rather than to inflation. Cleveland Fed President Beth Hammack indicated that the Fed could move in June IF they have clear and convincing data by then. At the same time, she indicated that she isn’t operating with a base case scenario. Even so, the market picked it up as a dovish signal. Fed governor Waller indicated that tariffs might cause layoffs and that the would support rate cuts in case of a significant rise in unemployment. But he indicated that he doesn’t expect significant effects of the tariffs to become apparent before July. Minneapolis Fed Kashkari mentioned that enough uncertainty may cause lay-offs. For now, this is all conditional. Recent data showed no outspoken weakening of the labour market yet (US jobless claims yesterday again were reported at a low 222k). Even so, it was enough for markets to price a higher probability of Fed easing in H2. US yields in a steepening move declined between 8.7 bps (5-y) and 4.7 bps (30-y). Markets now see about 65% of a 25 bps cut in June and it is more than fully discounted for July. The focus turns the labour market data. German yields moved in a similar way easing between 6.1 bps (2-y) and 3.4 bps (30-y). The move was supported by ECB Rehn keeping the option open of bigger rate cuts if necessary. Chief economist Lane later kept a more balanced tone, as he wasn’t that negative on EMU growth. Of late the impact of both interest rate differentials/expectations and/or risk sentiment the dollar often was different from the ‘standard’ market reaction function. Still, yesterday the combination of lower US yields and risk-on weighed slightly on the dollar. DXY eased to 99.28 (close). EUR/USD ‘rebounded’ to close at 1.139.

Risk sentiment in Asia this morning remains constructive as trade tensions are easing further. According to sources referred to by financial news agencies, China is considering suspending its 125% tariff at least on some key US goods to mitigate the economic damage. In a first reaction, the dollar gains against the likes of the yen (USD/JPY 143.75) and the euro (EUR/USD 1.133) that recently profited from the Sell US trade. Later today, the eco calendar is thin. Markets might keep still keep an eye at the inflation expectations measures of the Final U. of Michigan consumer confidence release. After recent easing, US yields are nearing first support levels (2-y 4.70% area, 10-y 4.25% area). UK March retail sales reported this morning were strong (0.4% M/M and 2.6M% Y/Y). The reaction of sterling is close to non-existent (EUR/GBP 0.8535).

News & Views

Tokyo inflation figures remained uncomfortably high in April. Headline inflation accelerated from 0.3% M/M to 0.4% M/M with core inflation (ex fresh food) and services inflation sticky at respectively 0.5% M/M and 0.3% M/M. In annual terms, headline Tokyo CPI rose from 2.9% to 3.5% with the ex fresh food gauge spiking from 2.4% to 3.4%. Both are the highest levels since April 2023, more than markets expected and way above the BoJ’s 2% inflation target. A low base from last year’s school-fee waiver, a sharp pickup in rent and price adjustments for the new fiscal year contributed to the acceleration. The BoJ recently shifted the onus to economic risks from stemming from the developing trade war, but faces a difficult task turning a blind eye to price developments later this year. The BoJ meets next week with money markets currently only attaching a 5% probability to a new rate hike.

UK consumer confidence (GfK) deteriorated from -19 in March to -23 in April, the weakest level since November 2023. GfK comments that it was an extraordinarily unsettling month as the tariffs controversy filtered through to consumer sentiment. All five categories making up the index have declined. The biggest monthly move came in the “general economic situation over next 12 months” category, which fell from -29 to -37 (vs -21 one year ago). Also “personal financial situation over next 12 month” took a relatively big hit, from 1 to -3. Offering some glimmers of hope, there’s only limited impact on major purchase intentions (-19 from -17). The savings index rose from 25 to 30.

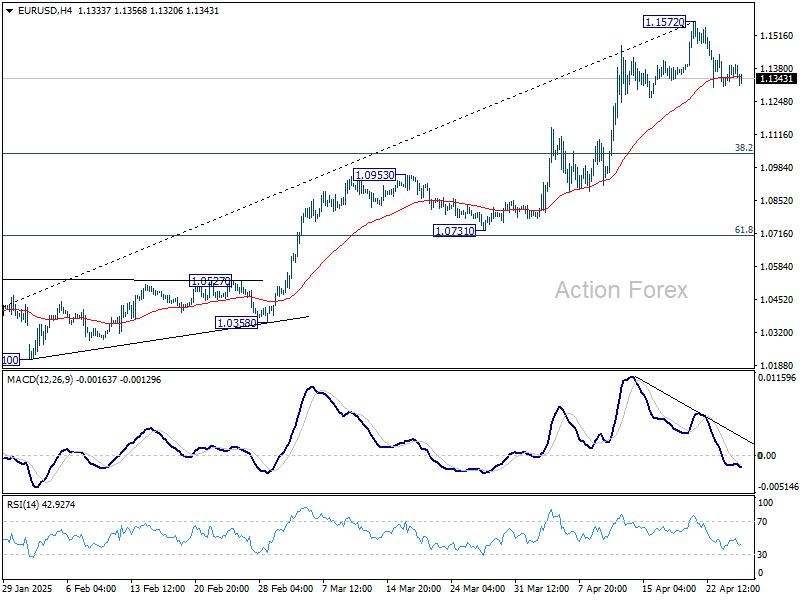

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1337; (P) 1.1367; (R1) 1.1420; More...

No change in EUR/USD's outlook and intraday bias stays mildly on the downside. Pullback from 1.1572 short term top could extend lower. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039. On the upside, break of 1.1572 will resume larger up trend.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0776) holds.

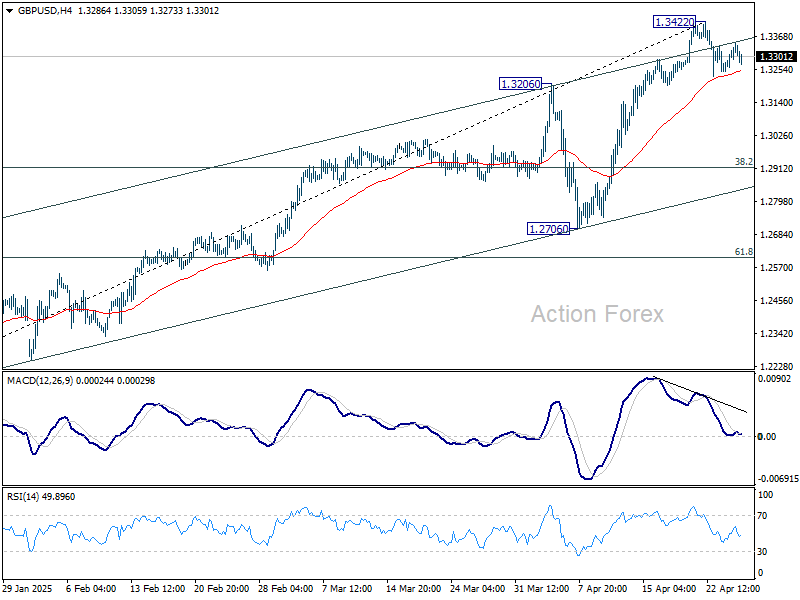

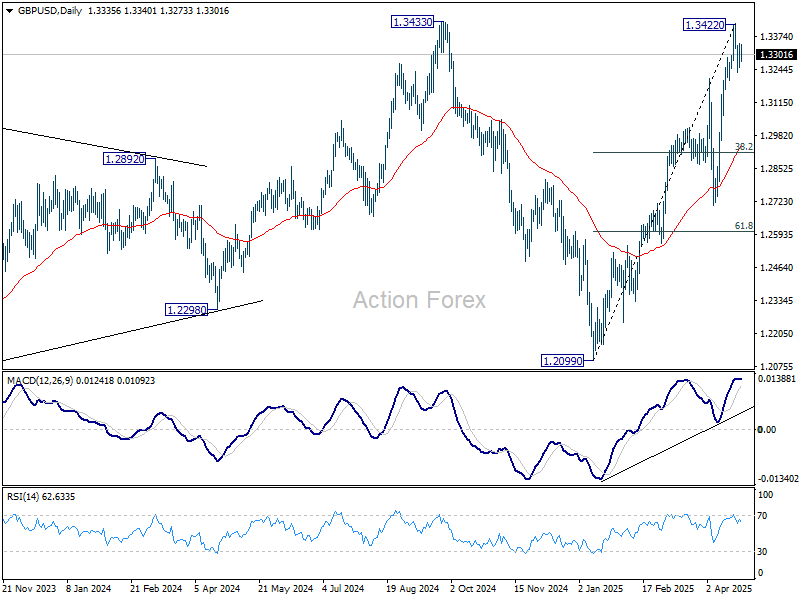

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3277; (P) 1.3313; (R1) 1.3375; More...

Intraday bias in GBP/USD remains mildly on the downside at this point. Pullback from 1.3422 short term top would continue lower. But downside should be contained by 38.2% retracement of 1.2099 to 1.3422 at 1.2917. On the upside, firm break of 1.3433 will resume larger up trend.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

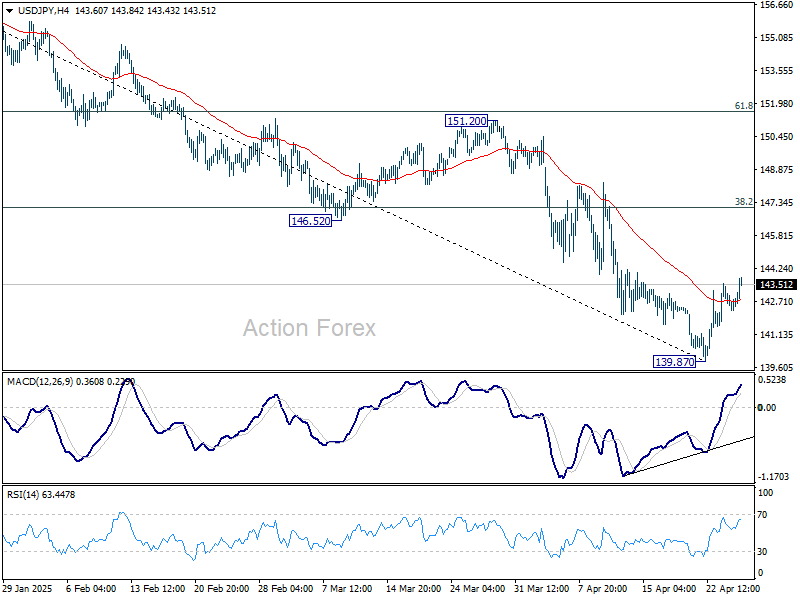

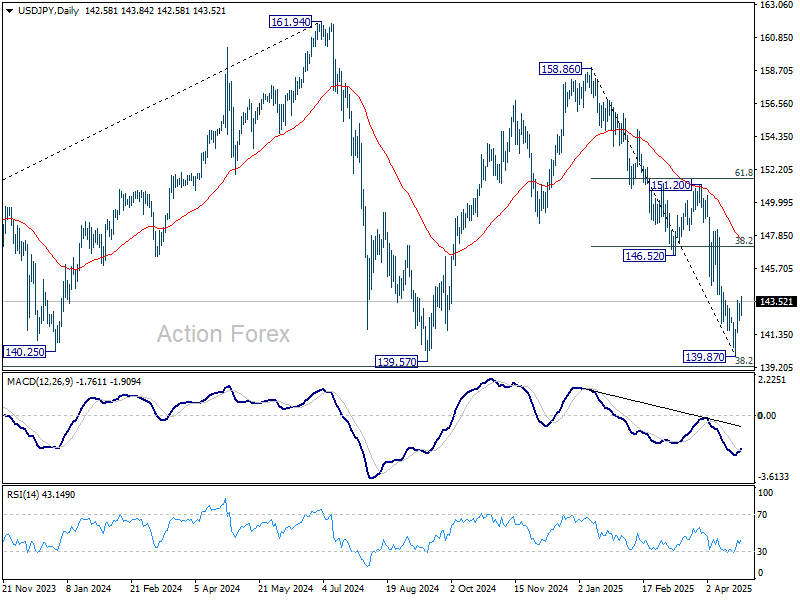

USD/JPY Daily Outlook

Daily Pivots: (S1) 142.12; (P) 142.78; (R1) 143.29; More...

Intraday bias in USD/JPY remains mildly on the upside. Rebound from 139.87 short term bottom could extend higher. But overall risk will stay on the downside as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds. On the downside, decisive break of 139.26 will carry larger bearish implications.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

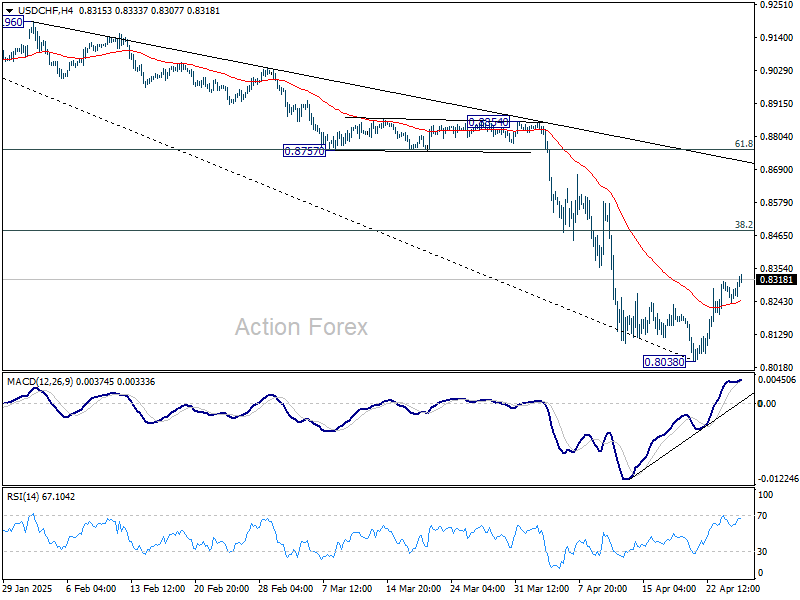

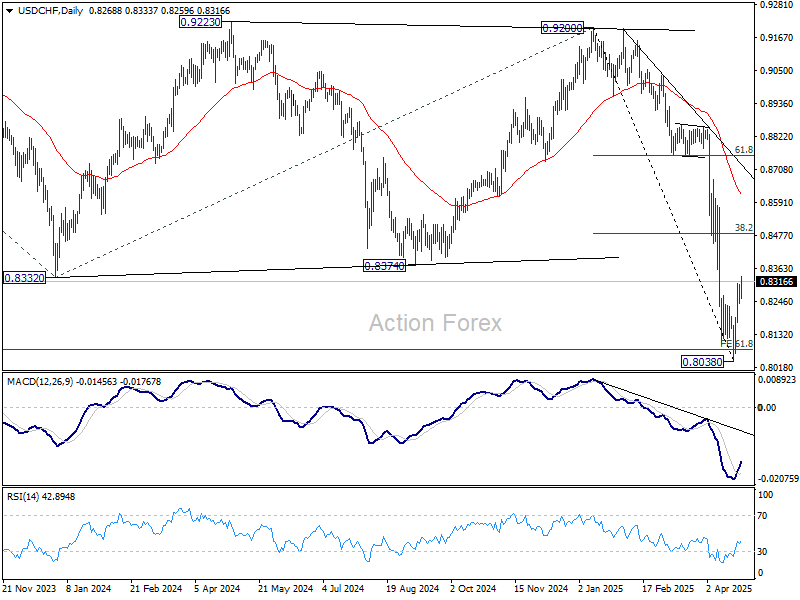

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8237; (P) 0.8273; (R1) 0.8306; More….

Intraday bias in USD/CHF remains mildly on the upside for the moment. Corrective recovery from 0.8038 short term bottom could extend to 38.2% retracement of 0.9200 to 0.8038 at 0.8482. But upside should be limited there. On the downside, break of 0.8038 will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8794) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

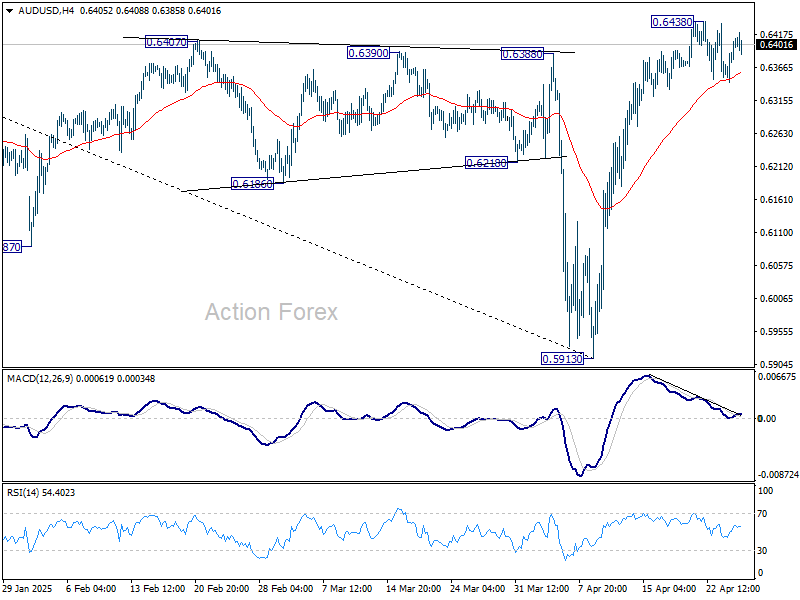

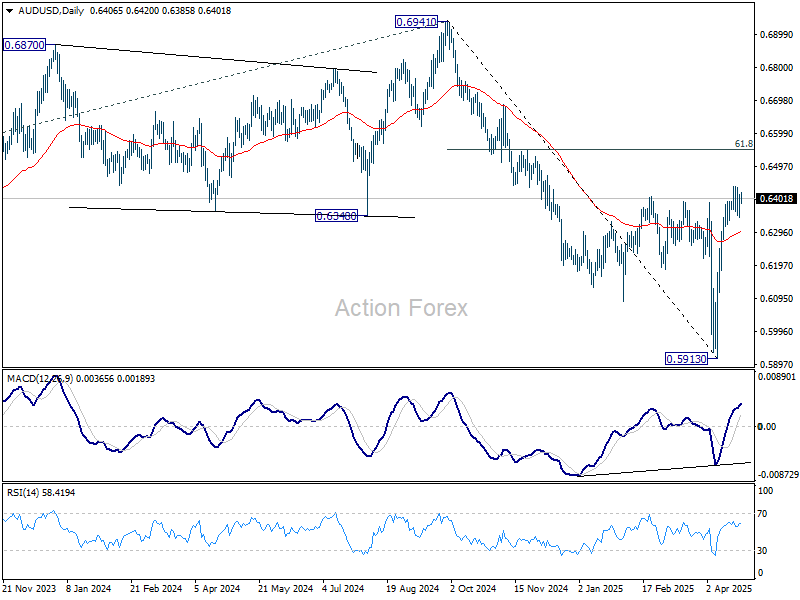

AUD/USD Daily Report

Daily Pivots: (S1) 0.6364; (P) 0.6389; (R1) 0.6433; More...

AUD/USD is staying in consolidations below 0.6438 and intraday bias stays neutral. Further rally is expected as long as 55 D EMA (now at 0.6302) holds. Above 0.6438 temporary top will resume the rebound from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, sustained trading below 55 D EMA will argue that the rebound has completed and turn bias back to the downside.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA (now at 0.6443) will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

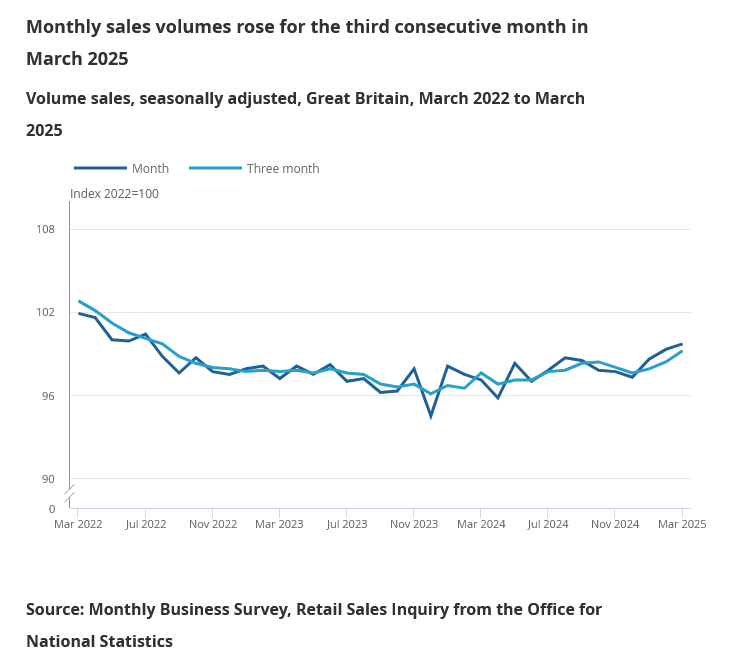

UK retail sales rise 0.4% mom in March, 1.6% qoq in Q1

UK retail sales surprised to the upside in March, rising by 0.4% mom, defying market expectations for a -0.3% mom decline.

The unexpected strength was attributed largely to favorable weather conditions, which lifted sales at clothing and outdoor retailers. However, this gain was partially offset by weaker performance at supermarkets.

Looking beyond the monthly figure, the broader quarterly performance painted an encouraging picture of consumer resilience. Retail sales volumes grew by 1.6% qoq 1.7% yoy in Q1. These results indicate that UK consumers remain relatively active despite broader economic uncertainties.