Sample Category Title

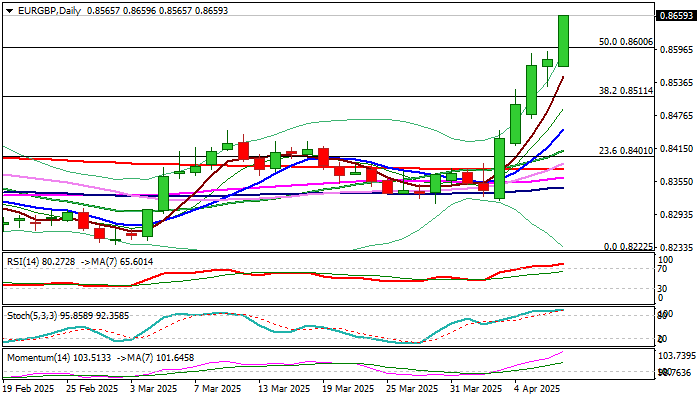

EURGBP Extends Steep Ascend into Fifth Straight Day

EURGBP holds in steep ascend for the fifth consecutive day, strongly supported by rising risk aversion on the latest escalation of trade war, as Euro turned to safe haven asset (along with yen and Swiss franc) on weakening dollar.

Fresh acceleration higher on Wednesday (the price was up almost 1% until early US trading) hit the highest since early January 2024, while the pair advanced nearly 4% in the latest five-day rally.

Bulls broke through important barriers at 0.8600 (50% retracement of 0.8978/0.8225) and 0.8624/44 (former tops of Aug 9 / Apr 23 last year) generating fresh bullish signals.

Important Fibo barrier at 0.8689 (61.8%) comes in focus, although bulls may take a breather for consolidation as strongly overbought daily studies suggest.

Dips should be shallow (in currently very favorable fundamentals) and offer better levels to re-enter firmly bullish market.

Good supports at 0.8600/0.8550 should ideally contain.

Res: 0.8689; 0.8714; 0.8765; 0.8800

Sup: 0.8624; 0.8600; 0.8550; 0.8511

Yen Surges to Six-Month High, BoJ Cautious

The Japanese yen continues to make inroads against the US dollar. In the North American session, USD/JPY is up 1.1% on Wednesday, trading at 144.60. Earlier, the yen strengthened to 143.98, its strongest level since Sept. 2024.

BoJ's Ueda: BoJ could pause in response to US tariffs

Bank of Japan Governor Kazuo Ueda said on Wednesday that the central bank will have to determine the impact of US trade policy on growth and inflation in Japan. Ueda said that US tariffs had created new uncertainty and signaled that the BoJ might hold off on further interest rates until the situation became more clear.

Ueda repeated that the BoJ would raise rates if the economy continued to improve, and currently, underlying inflation was rising and moving closer to 2% target. The uptake is that the BoJ is being very cautious with all the turmoil in the markets and is dampening expectations of a rate hike at the May 1 meeting.

FOMC minutes - still relevant?

The Federal Reserve will post its minutes of the March rate meeting. Investors scrutinize the minutes for policy clarity but global economic developments are unfolding so quickly that it's questionable if the minutes will be relevant with the massive market sell-off and the trade war between the US and China.

Earlier today, the US lifted tariffs on China to an astounding 104% and China has retaliated with an 84% counter-tariff. The turmoil in the financial markets has nervous investors looking for safer shores, and are parking their funds in safe-haven assets like the Japanese yen and the Swiss franc. In April, the yen has jumped 3.3% against the US dollar, while the Swiss franc has soared 5% against the greenback.

USD/JPY Technical

- USD/JPY has pushed below support at 145.46 and is putting pressure on support at 144.64

- There is resistance at 146.79 and 147.61

Fed’s Kashkari: Rate cut bar now higher amid inflation risks from tariffs

Minneapolis Fed President Neel Kashkari warned that the unexpectedly high and broad scope of recently imposed US tariffs has created "larger direct economic effect and larger shock to confidence".

In a blog post today, he noted that this has increased the "hurdle" for Fed to adjust interest rates in either direction. He emphasized that due to the inflationary pressures tariffs are likely to bring in the "near term", the bar for cutting rates is also "higher" even in the face of rising unemployment.

Kashkari expressed concern that due to uncertainty of escalating trade tensions and retaliatory measures from other countries, "risk of unanchoring inflation expectations seems to have increased notably".

At the same time, he acknowledged that the demand for investment capital is likely to decline due to weaker growth prospects, which would naturally lower the neutral interest rate (r*). This dynamic could make current monetary policy stance relatively tighter without any Fed action.

Ultimately, Kashkari struck a cautious but flexible tone, noting that while Fed should be especially wary of cutting rates amid rising inflation risks, it must also remain responsive to rapidly changing conditions.

“No monetary policy response, up or down, should be completely off the table,” he concluded.

Sunset Market Commentary

Markets

The stakes are high for tonight. The US Treasury sells $39bn of 10-yr Notes as part of its mid-month refinancing operation. The auction occurs against the background of huge volatility, and weakness, in long-term bonds. US Treasuries sell off as some market parties are forced to unwind leveraged positions, with stagflation worries, loss of credibility, weakening public finances and foreign pressure (diverting FX reserves away) adding to the perfect storm. The US 30-yr yield this morning tested the psychological 5% mark (YtD top). Apart from a brief spell in 2023 (5.18% top), it’s been since 2007 that the very long end traded at higher levels. Even if tonight’s auction doesn’t raise market stress, there remain serious hurdles later this week with March US CPI inflation, a $22bn 30-yr bond auction and the April University of Michigan consumer survey. As a reminder: a failed 30-yr bond auction and evaporating liquidity served as a catalyst at the height of the Covid pan(dem)ic for Fed intervention. These included reopening the Primary Dealer Credit Facility to help keep primary dealers play their role during times of stress, relaunching the Money Market Mutual Fund Liquidity Facility to backstop those funds or providing more unlimited liquidity through the Commercial Paper Funding Facility. Similar action is possible this time around, but other initiatives like steep rate cuts or shifting back to quantitative easing are less likely at the moment given the completely different inflation (outlook) compared to March 2020. The sell-off in longer Treasuries spread to other bond markets as well. The Japanese 30-yr yield closed 17 bps higher (+27 bps intraday), reversing some of the move higher on talk of a meeting between the BoJ, MoF and FSA on measures to maintain market stability. The UK 30-yr yield adds over 25 bps at the moment, pushing it to the highest level since 1998. During the September 2022 Gilt sell-off (unfunded mini budget by Truss-Kwarteng), the BoE was equally forced to take emergency action to calm turmoil (long-term bond buying). Corporate (both HY and IG) and sovereign bond spreads are widening. Damage on European bond markets remains contained for now. The EU 30-y swap rate adds 5 bps with the German 30-yr yield broadly unchanged. A wide range of ECB governors hit the wire. Apart from ECB Holzmann, they all favour action next week (25 bps rate cut being our preferred scenario). Views diverge beyond April depending on the focus on either downside growth risks or upside inflation risks. For now, we stick to the long pause idea beyond April, even as EMU money markets discount an ECB rate bottom around 1.5% by the end of the year.

Nervousness in the bond market triggers more risk aversion on stock markets with the escalating trade war adding to a worsening sentiment. China raised tariffs on US goods to 84% while the EU adopted tariffs on €21bn of US goods in the metals dispute. Risks are for president Trump to announce “major tariffs on pharmaceuticals” soon. European stock markets suffer another 3%+ setback with US indices opening flattish after yesterday’s swoon. Brent crude prices traded below $60/b for the first time since early 2021. The US dollar loses ground across the board against JPY (USD/JPY < 145), the euro (EUR/USD 1.1070), CHF (USD/CHF testing 2023 & 2024 lows; weakest since dropping EUR/CHF 1.20 floor in 2015), but also smaller currencies like CAD, AUD or NZD. Weakness in UK gilts hits sterling with EUR/GBP extending this week’s rally to 0.8660 (from 0.8350 on the eve of “Liberation Day”).

News & Views

The IFO institute’s Quarterly Economic Experts survey showed expectations about short-run inflation rates no longer declining. Long-term inflation expectations increased slightly. Global average inflation is expected at 4% this year (from 3.9%). For 2026 it’s 3.9% and p to 2028, it remains high at 3.8% (from 3.5%). Inflation expectations vary widely across the world regions. Expectations have risen particularly in North America to reach 3.2% in 2025 (from 2.6%), 3.2% in 2026 and 3.3% in 2028. For 2025, experts expect the lowest inflation rates in Western Europe (2.1%). In other parts of Europe (Southern: 3.4%, Eastern: 7.4%) they remain above central bank targets.

Czech National Bank board member Prochazka indicated room to cut rates further, but inflation risks might warrant the CNB to extend its policy pause to longer than one meeting. Prochazka indicated that the mix of ongoing domestic price pressure and global risk question the CNB’s current stop-and-go approach. CZK FRA rates today only decline marginally at the very short end (e.g. 3/6 months) but decline further for tenors toward the end of the year. EUR/CZK is holding relatively stable despite the overall risk-off (EUR/CZK 25.19).

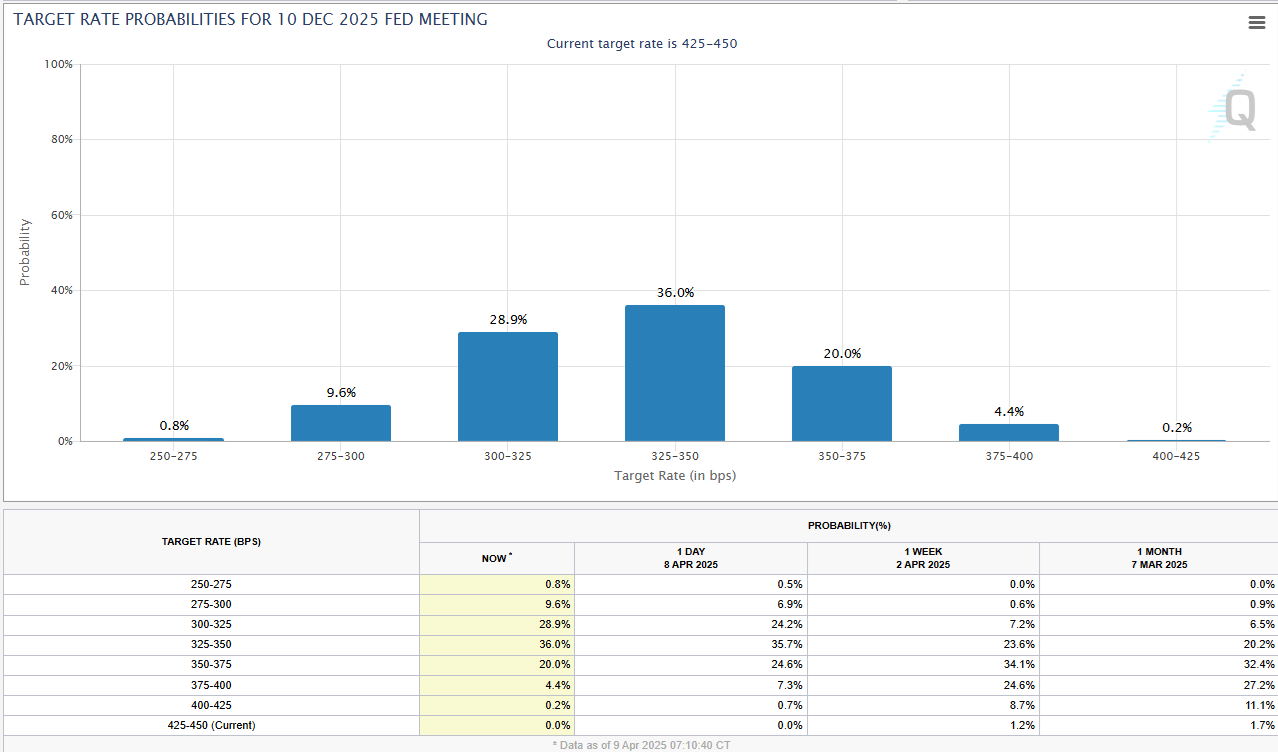

Dollar Pressured as Markets Betting on a Dovish Fed

Over the past week, the probability of a key Fed rate cut in May jumped from 11% to 47% and reached nearly 60% on Tuesday.

Market now pricing 100-point rate cut to 3.25%-3.50% with 75% probability.

For year-end, the market now sees the prevailing scenario as a 100-point rate cut to 3.25%-3.50% or lower with a 75% probability, although a month ago, those odds were barely above a quarter.

This could be a technical move reflecting a flight to defensive short-term government bonds. The jump in 10- and 30-year long-term government bond yields, which typically fall along with declining short-term yields, supports this hypothesis.

Such erratic movements increase pessimism about the outlook for equities, where liquidation of margin positions may continue or intensify.

While this is usually favourable for the dollar, we are now seeing increased pressure on the US currency due to the sell-off in equities and long-term bonds.

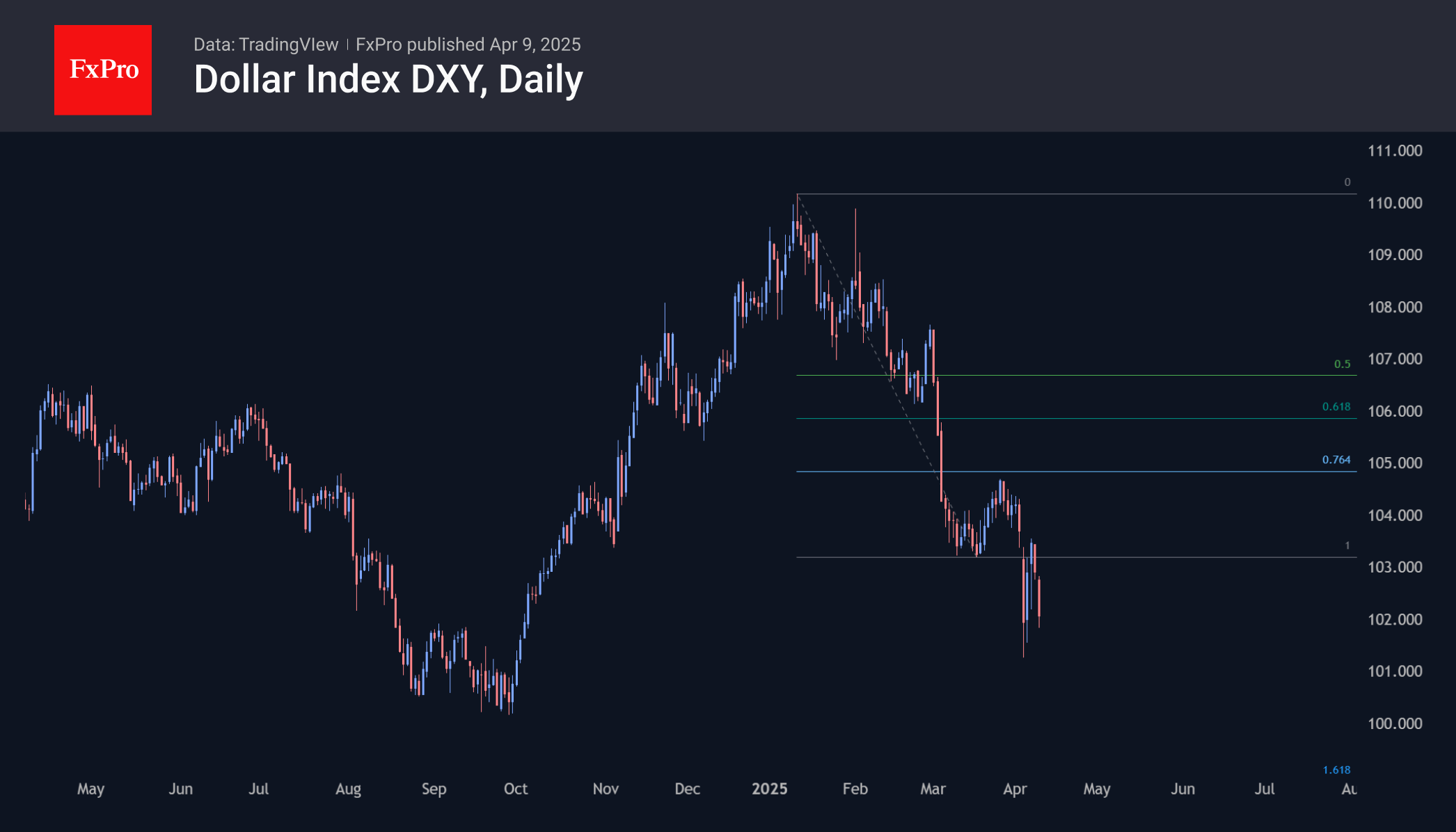

Dollar index has already been in an active decline phase since early April

Technically, the dollar index has already been in an active decline phase since early April, having broken sharply below the March support area. The rebound at the start of the week only closed the gap without changing the pattern, which suggests a fall to the 99 area – almost 3% from current levels.

Although other major economies are also expected to accelerate rate cuts, markets tend to play down the changes in the US first. This has caused the dollar to rise before the rate hike cycle begins in 2022 and fall before the first cuts in 2024 and 2020. In terms of stress and uncertainty, the current situation resembles March 2020.

EUR/USD Outlook: Euro Benefits from US-China Escalation, Markets Price in April ECB Rate Cut

- EUR/USD has risen due to escalating US-China trade tensions, despite markets anticipating an ECB rate cut in April.

- China has announced tariffs on US goods in response to US tariffs, increasing fears of further trade war escalation, Euro becomes a beneficiary.

- Technically, EUR/USD is testing resistance at the 1.1100 hurdle and approaching overbought levels, suggesting a retracement may be on its way.

EUR/USD has been on a good run this week and jumped this morning as tensions between the US and China escalated. The latest escalation has left the US Dollar and in particular the US Dollar index on the back foot.

The DXY is testing last week's lows at the time of writing and this has helped EUR/USD rise despite markets pricing an ECB rate cut in April.

US Dollar Index Daily Chart, April 9, 2025

Source: TradingView

The performance of the Euro has surprised me to say the least. This morning we saw traders fully price ECB rate cuts in April for the first time. This was followed by Morgan Stanley lowering the Euro area's 2025 GDP forecast to 0.8% vs prior forecast of 1.0% while also saying that they expect the ECB benchmark rate to reach 1.5% in December 2025 vs the prior forecast of June 2026.

This was further echoed by a Reuters report which stated that the European Central Bank (ECB) now expects Trump’s tariffs to hurt the Eurozone's growth more than first thought. Sources say the earlier estimate of a 0.5 percentage point impact is too low, with one suggesting it could exceed 1 percentage point.

These are supposedly dovish moves for the Euro which under normal circumstances might have seen a market reaction. However, given the dynamics around the trade war markets have been focusing elsewhere. We have discussed this at length of late, the trade war overshadowing economic data releases and news. This trend seems to be intact for now.

US-China trade war escalates

US President Donald Trump's additional tariffs on China went into effect yesterday with China refusing to bow to President Trump's wishes. Instead Chinese authorities through the Finance Ministry announced that it will impose additional tariffs of 84% on US goods to come into effect on April 10.

The news sent risk assets like S&P 500 tumbling this morning as fears ramp up over further escalation. China added more firm to the unreliable list as China's Premier Li chaired a symposium on the economic situation with experts and businesses.

Premier Li acknowledged that while external factors may cause pressure the Government is ready to deal with it. Premier Li also touched on expanding local demand, something he called a long-term goal.

The Federal Reserve (Fed) will release the minutes from its March meeting later today. However, since this meeting happened before the tariff announcements, traders might not pay much attention to it as tariffs continue to dominate the discourse.

If this is the case, expect any further tit-for-tat between US-China to lead to potential EUR strength against the US dollar based on recent history.

Technical Analysis on EUR/USD

EUR/USD Daily Chart, April 9, 2025

Source: TradingView.com

Looking at the EUR/USD daily chart, the pair is on course for a third successive day of gains.

The pair is currently testing an area of resistance at the 1.1100 hurdle, can the rally continue?

There is definitely scope for further upside but I think that will require a prolonged standoff between the US-China. Any deal that may arise between the two could send EUR/USD tumbling..

As we have seen above, tariffs are having an impact on everything from growth to monetary policy at present.

Looking at the period 14-RSI and it is approaching overbought levels once more. This means that a retracement the likes of which occurred on April 3 could repeat itself.

This is definitely worth monitoring moving forward.

OAU-PRS-236-MarketPulse-variant1-Square

Key levels to pay attention to

Support

- 1.1000

- 1.0948

- 1.0900

Resistance

- 1.1100

- 1.1200

- 1.1250

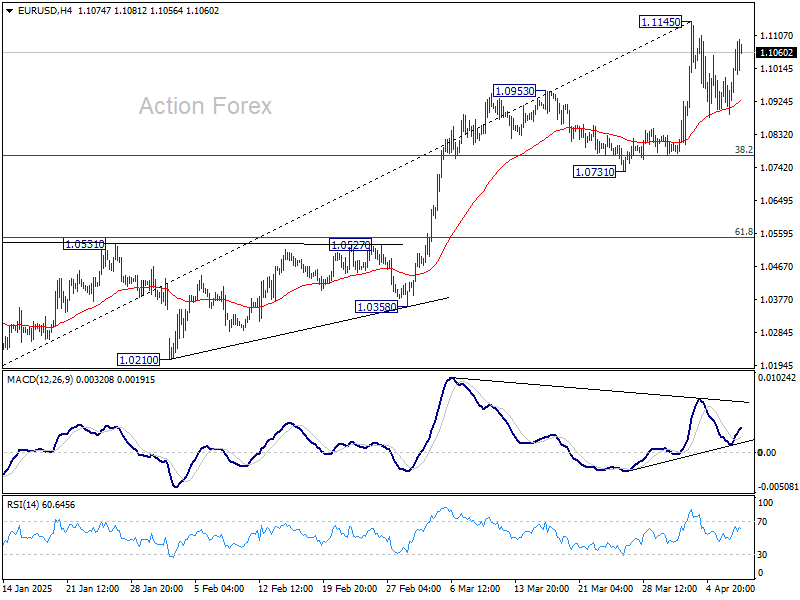

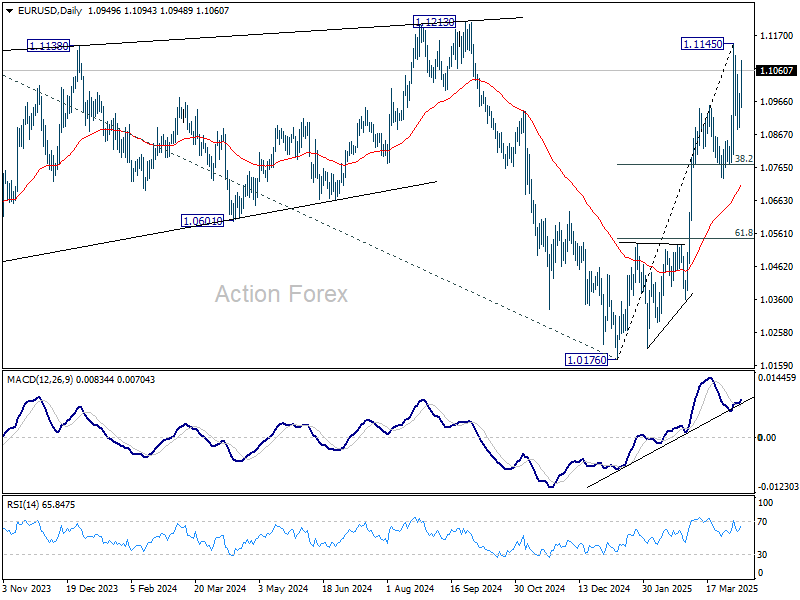

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0901; (P) 1.0946; (R1) 1.1004; More...

Range trading continues in EUR/USD and intraday bias remains neutral. More consolidations could be seen, but in case of another retreat, downside should be contained by 38.2% retracement of 1.0176 to 1.1145 at 1.0775. On the upside, above 1.1145 will resume the rally from 1.0176 to 1.1213/74 key resistance zone next.

In the bigger picture, fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through the multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0731 support holds.

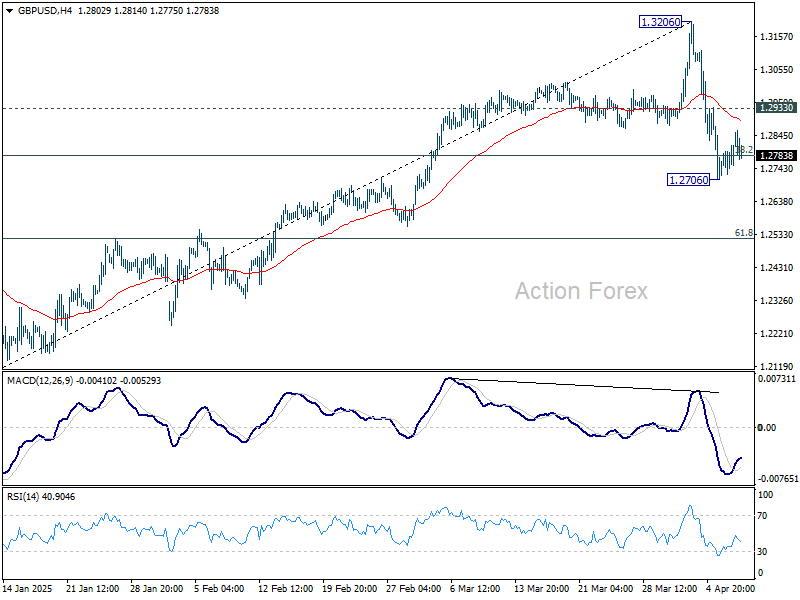

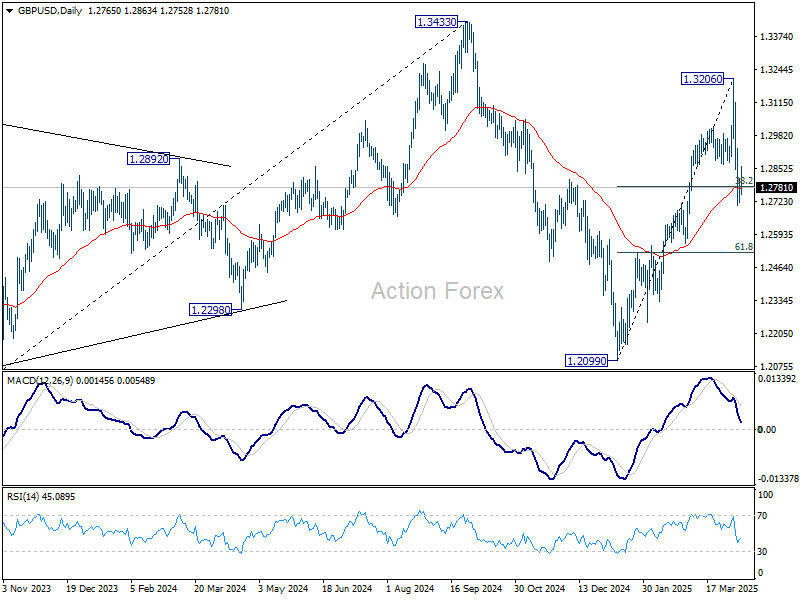

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2713; (P) 1.2764; (R1) 1.2815; More...

GBP/USD is staying in consolidation above 1.2706 and intraday bias remains neutral. Risk will stay on the downside with 1.2933 minor resistance intact. Break of 1.2706 will resume the decline from 1.3206 to 61.8% retracement of 1.2099 to 1.3206 at 1.2522. Nevertheless, firm break of 1.2933 will bring stronger rebound back to retest 1.3206 high.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

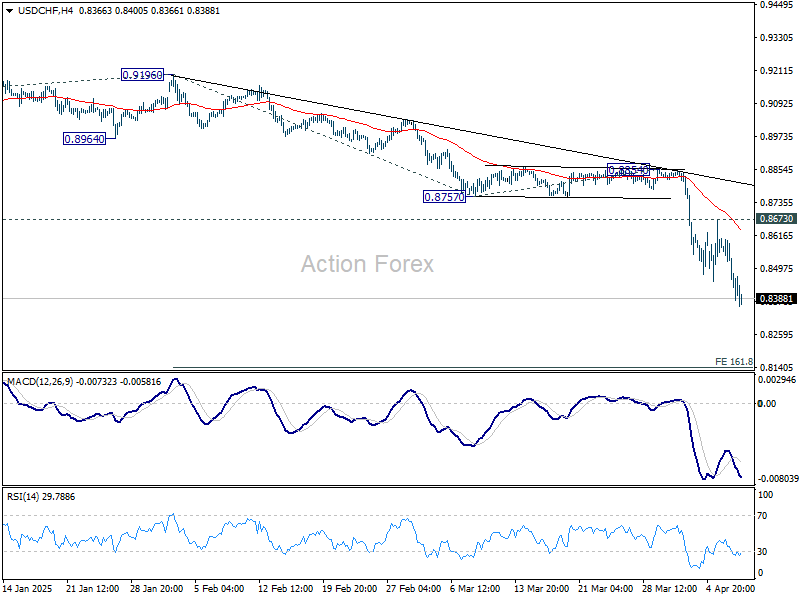

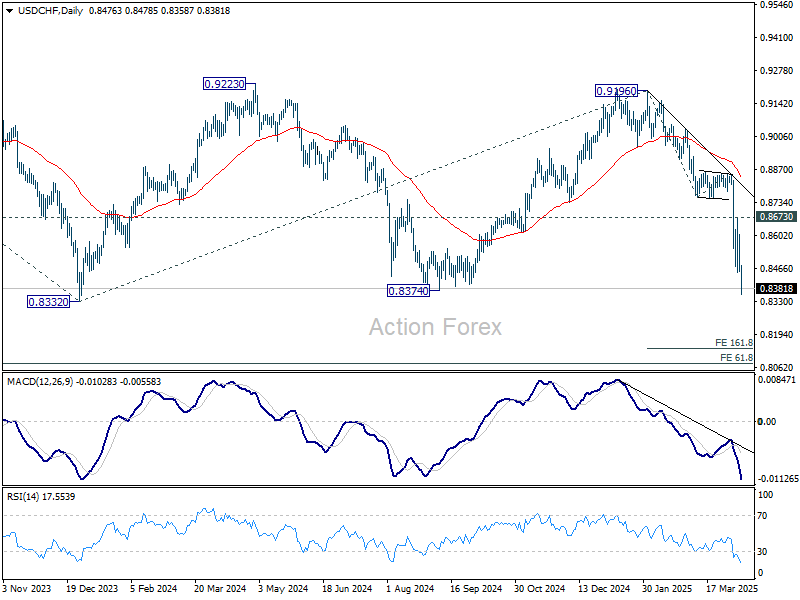

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8416; (P) 0.8518; (R1) 0.8581; More…

Intraday bias in USD/CHF remains on the downside at this point. Current fall from 0.9196 is in progress. Sustained break of 0.8332/8374 key support zone will confirm larger down trend resumption. Next near term target is 161.8% projection of 0.9196 to 0.8757 from 0.8854 at 0.8144. On the upside, break of 0.8673 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption. Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075.

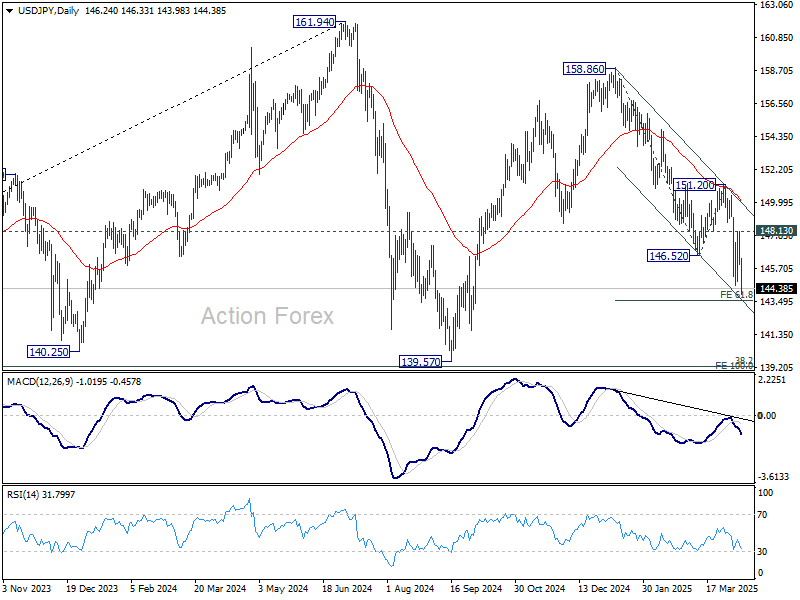

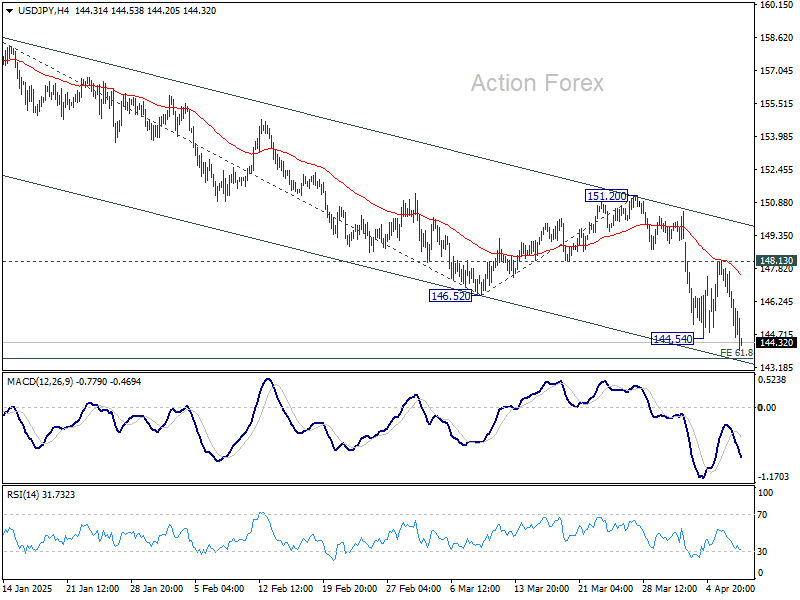

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.46; (P) 146.79; (R1) 147.61; More...

Intraday bias in USD/JPY is back on the downside with break of 144.54 support. Fall from 158.86 is resuming to 158.86 to 146.52 from 151.20 at 143.57. Break there will target 139.57 low. On the upside, break of 148.13 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.