Sample Category Title

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2713; (P) 1.2764; (R1) 1.2815; More...

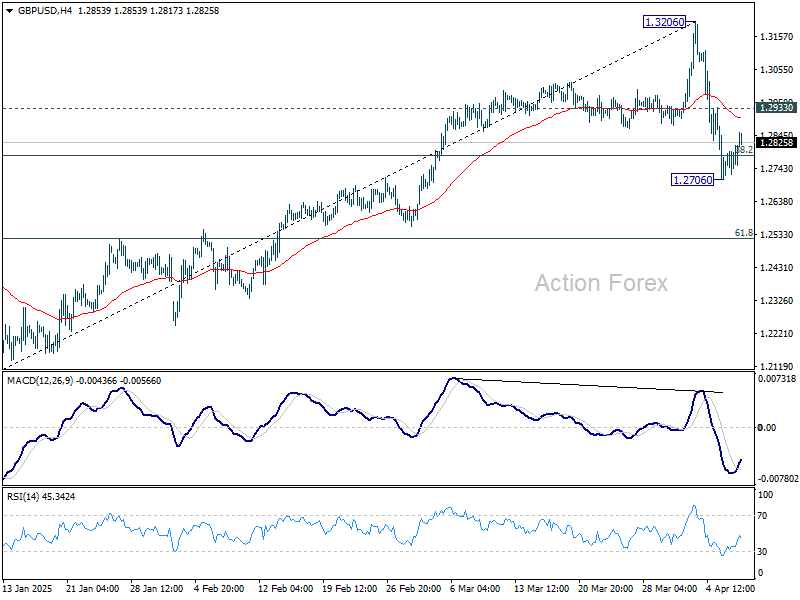

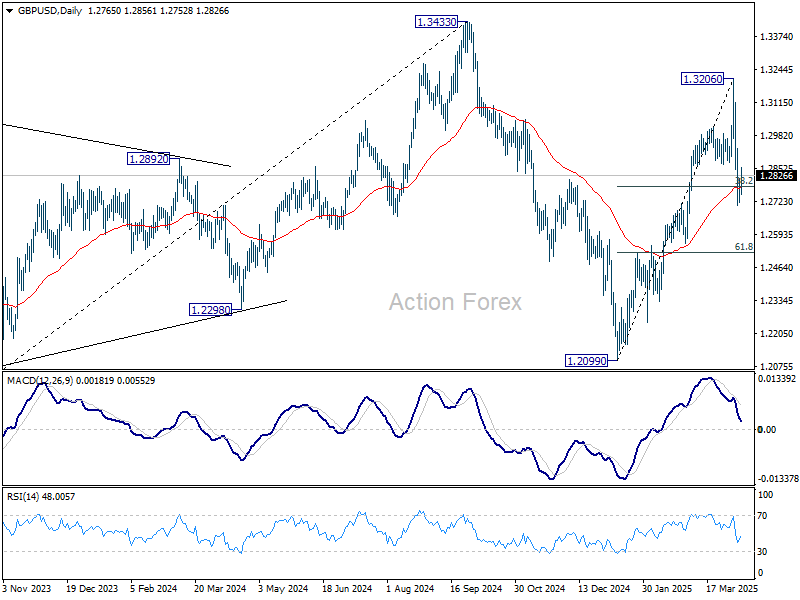

Intraday bias in GBP/JPY is turned neutral first with current recovery. Some consolidations would be seen but risk will stay on the downside with 1.2933 minor resistance intact. Break of 1.2706 will resume the decline from 1.3206 to 61.8% retracement of 1.2099 to 1.3206 at 1.2522. Nevertheless, firm break of 1.2933 will bring stronger rebound back to retest 1.3206 high.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8416; (P) 0.8518; (R1) 0.8581; More…

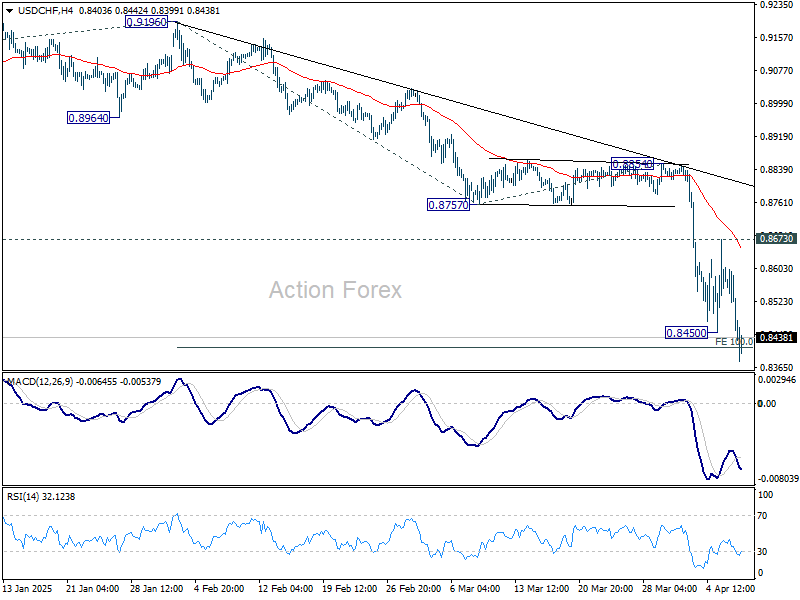

USD/CHF's decline from 0.9196 resumed after brief consolidations and intraday bias is back on the downside. Firm break of 0.8332/8374 key support zone will confirm larger down trend resumption. On the upside, break of 0.8673 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption. Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075.

AUD/USD Daily Report

Daily Pivots: (S1) 0.5907; (P) 0.5997; (R1) 0.6046; More...

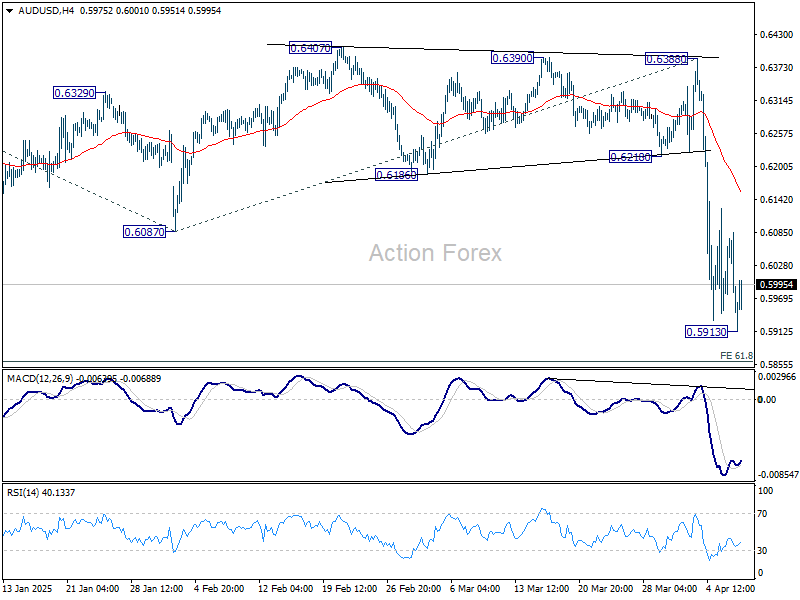

AUD/USD dips to 0.5913 but quickly recovered. Intraday bias stays neutral and more consolidations could be seen. Outlook will stay bearish as long as 55 4H EMA (now at 0.6155) holds. Break of 0.5915 will resume larger decline to 61.8% projection of 0.6941 to 0.6087 from 0.6388 at 0.5860.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 0.6388 resistance holds.

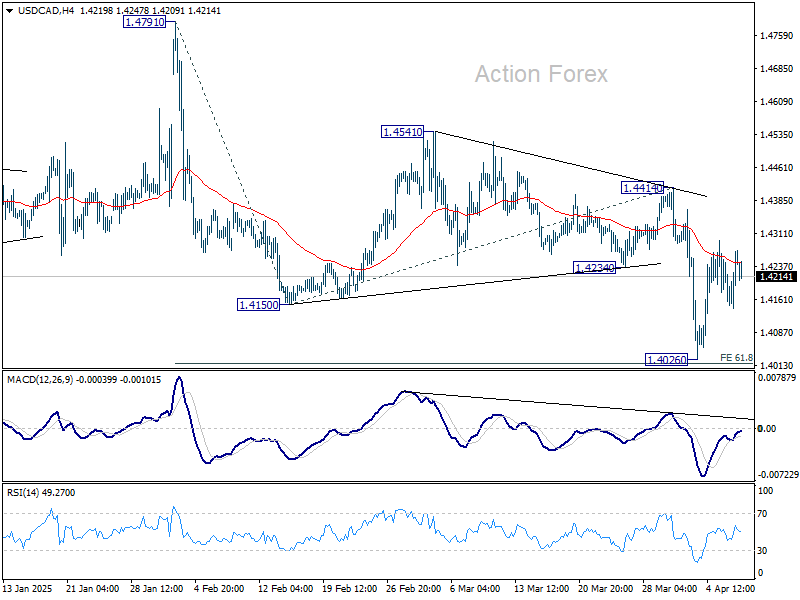

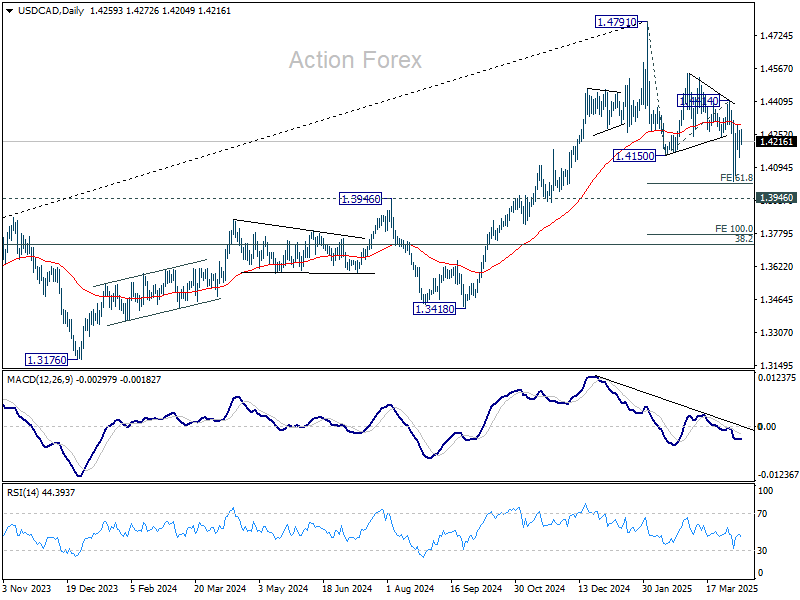

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4181; (P) 1.4226; (R1) 1.4309; More...

Range trading continues in USD/CAD and intraday bias stays neutral. On the upside, firm break of 1.4414 resistance will suggest that the decline from 1.4791 has completed as a three wave correction, and turn bias back to the upside for retesting 1.4791 high. However, firm break of 61.8% projection of 1.4791 to 1.4150 from 1.4414 at 1.4018, could prompt downside acceleration to 100% projection at 1.3773 next.

In the bigger picture, focus is now on 1.3976 resistance turned support (2022 high), which is close to 55 W EMA (now at 1.4001). Strong rebound from there will retain medium term bullishness. That is, up trend from 1.2005 is still in progress for breaking through 1.4791 at a later stage. However, sustained break there should confirm medium term topping at 1.4791. Deeper correction would be seen to 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727.

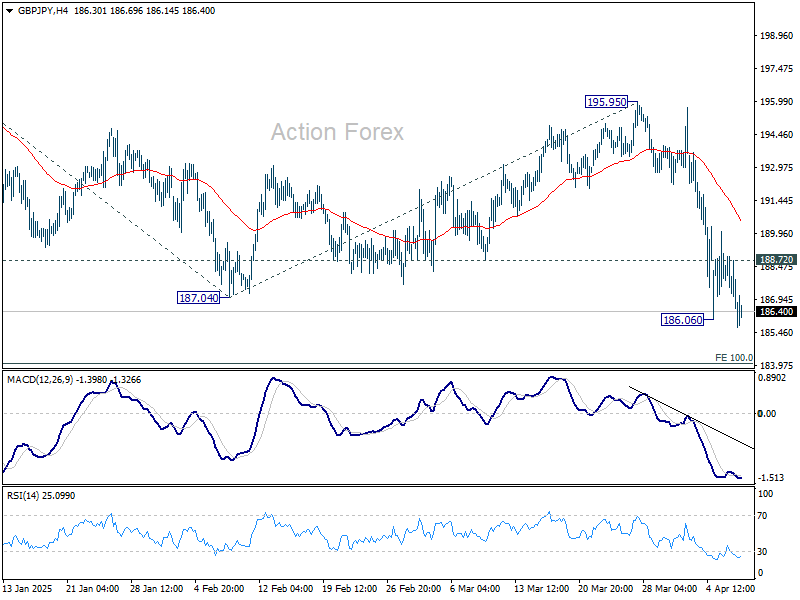

GBP/JPY Daily Outlook

Daily Pivots: (S1) 185.88; (P) 187.41; (R1) 188.28; More...

GBP/JPY's fall resumed after brief recovery and intraday bias is back on the downside. Current decline should target 100% projection of 198.94 to 187.04 from 195.95 at 184.05. On the upside, above 188.72 will turn intraday bias neutral again. But after all, risk will stay on the downside as long as 55 4H EMA (now at 190.52) holds.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

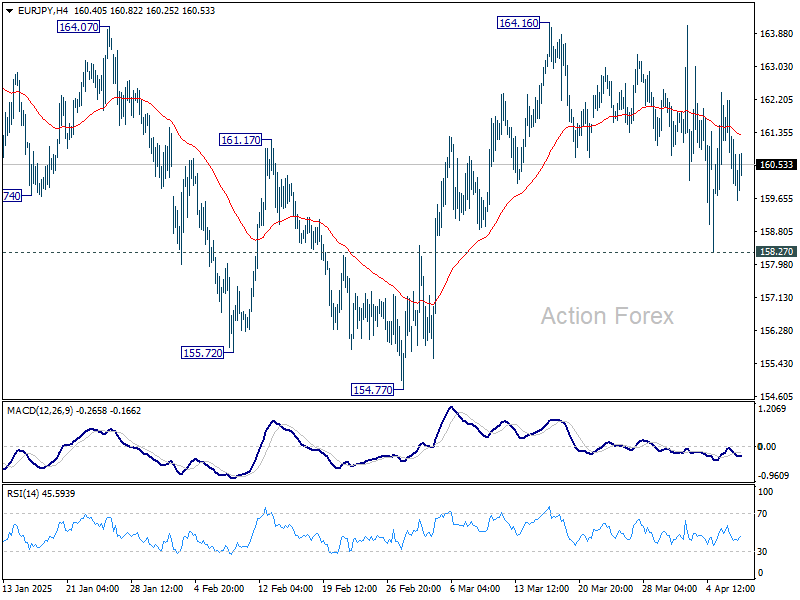

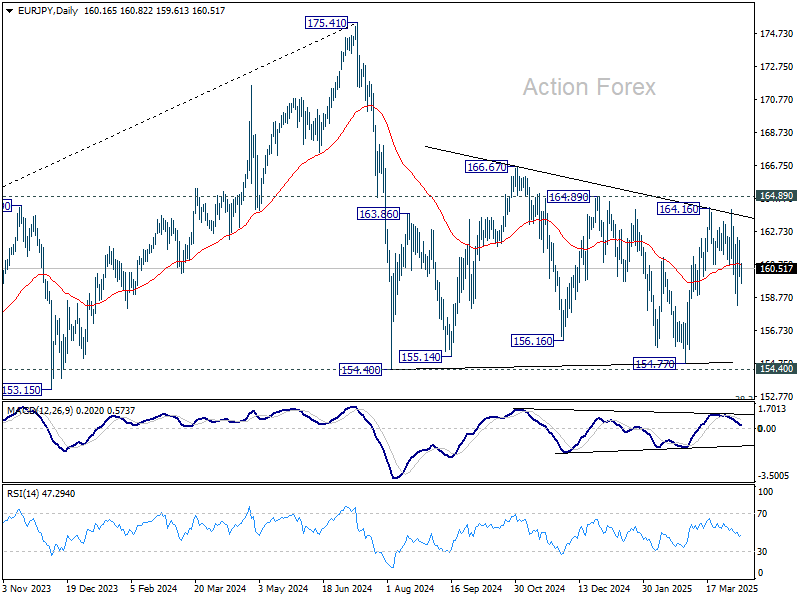

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.50; (P) 160.85; (R1) 161.68; More...

Intraday bias in EUR/JPY remains neutral as range trading continues. On the upside, above 164.16 will resume the rally from 154.77 to 164.89 resistance, and then 166.67. However, decisive break of 158.27 support will bring deeper decline back to 154.77 support. Overall, sideway consolidation pattern from 154.40 is still extending.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

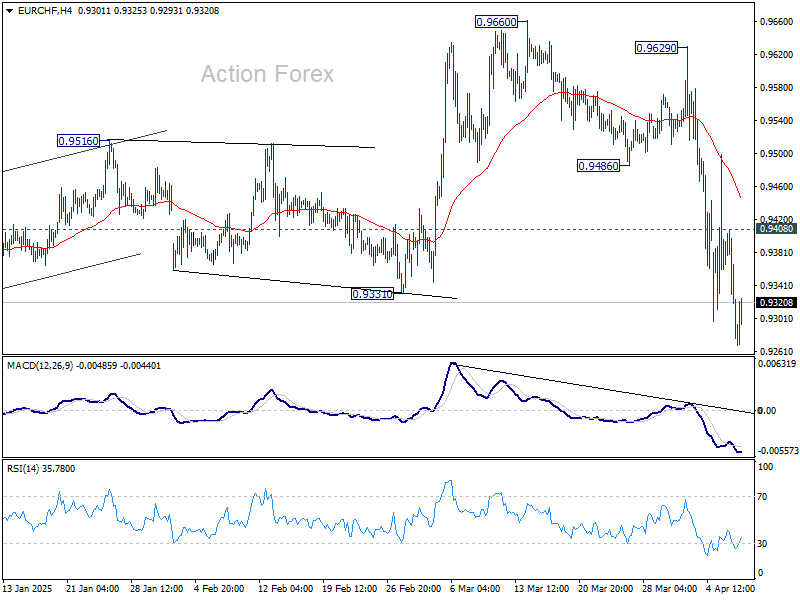

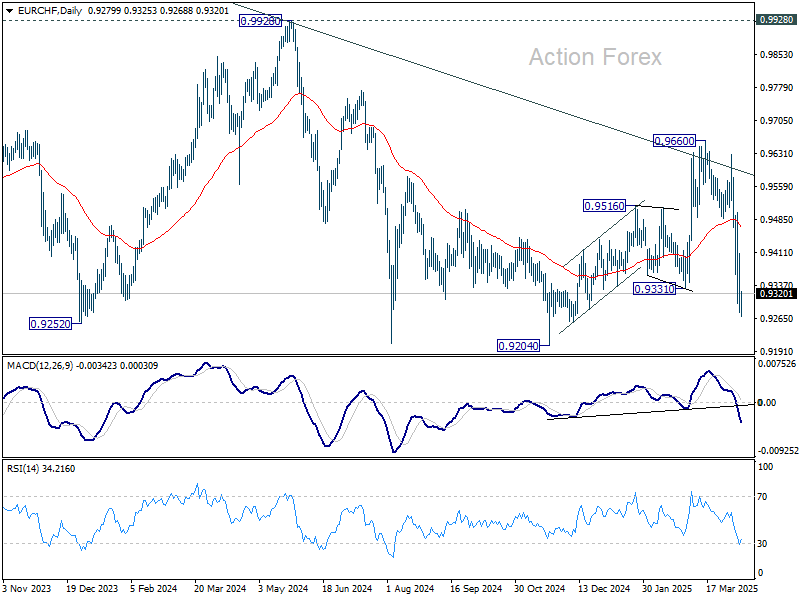

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9282; (P) 0.9392; (R1) 0.9492; More....

EUR/CHF's fall from 0.9660 continues today and intraday bias stays on the downside. Break of 0.9331 support suggests that rise form 0.9204 has already completed as a three-wave correction. Deeper decline should be seen to retest 0.9204 low next. On the upside, above 0.9408 minor resistance will turn bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, rejection by long-term falling channel resistance (now at 0.9600) will retain medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Downside breakout through 0.9204 low would then be in favor at a later stage.

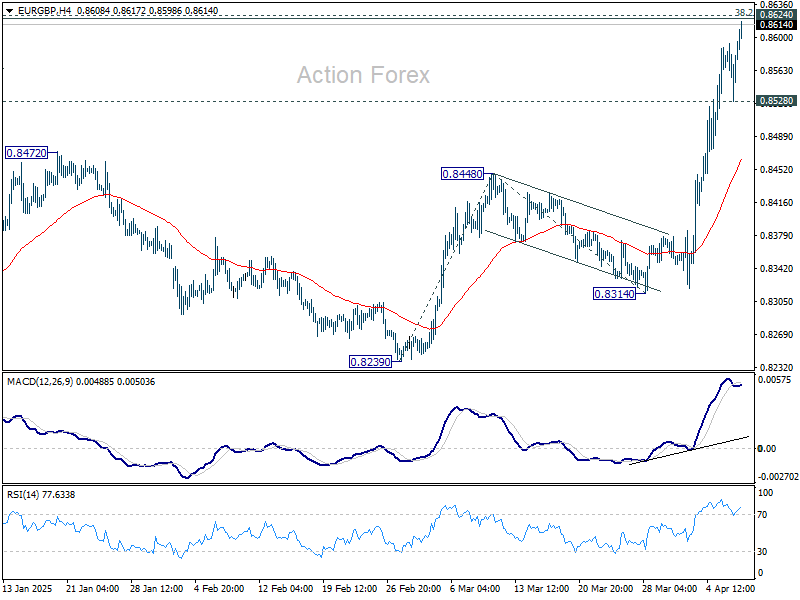

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8544; (P) 0.8569; (R1) 0.8610; More...

Intraday bias in EUR/GBP stays on the upside with immediate focus on 0.8624 key cluster resistance next. Decisive break there will be an important indication of larger bullish trend reversal. Next near term target will be 161.8% projection of 0.8239 to 0.8448 from 0.8314 at 0.8652. On the downside, break of 0.8528 minor support will turn intraday bias neutral first. But outlook will remain bullish as long as 0.8448 resistance turned support holds, in case of retreat.

In the bigger picture, the break of medium term channel resistance is a bullish signal. Down trend from 0.9267 (2022 high) could have completed at 0.8221, just ahead of 0.9201 key support (2022 low). Firm break of 0.8624 cluster resistance (38.2% retracement of 0.9267 to 0.8221 at 0.8621) will confirm this bullish case and target 61.8% retracement at 0.8867 next. Nevertheless, rejection by 0.8624 will keep medium term outlook neutral at best.

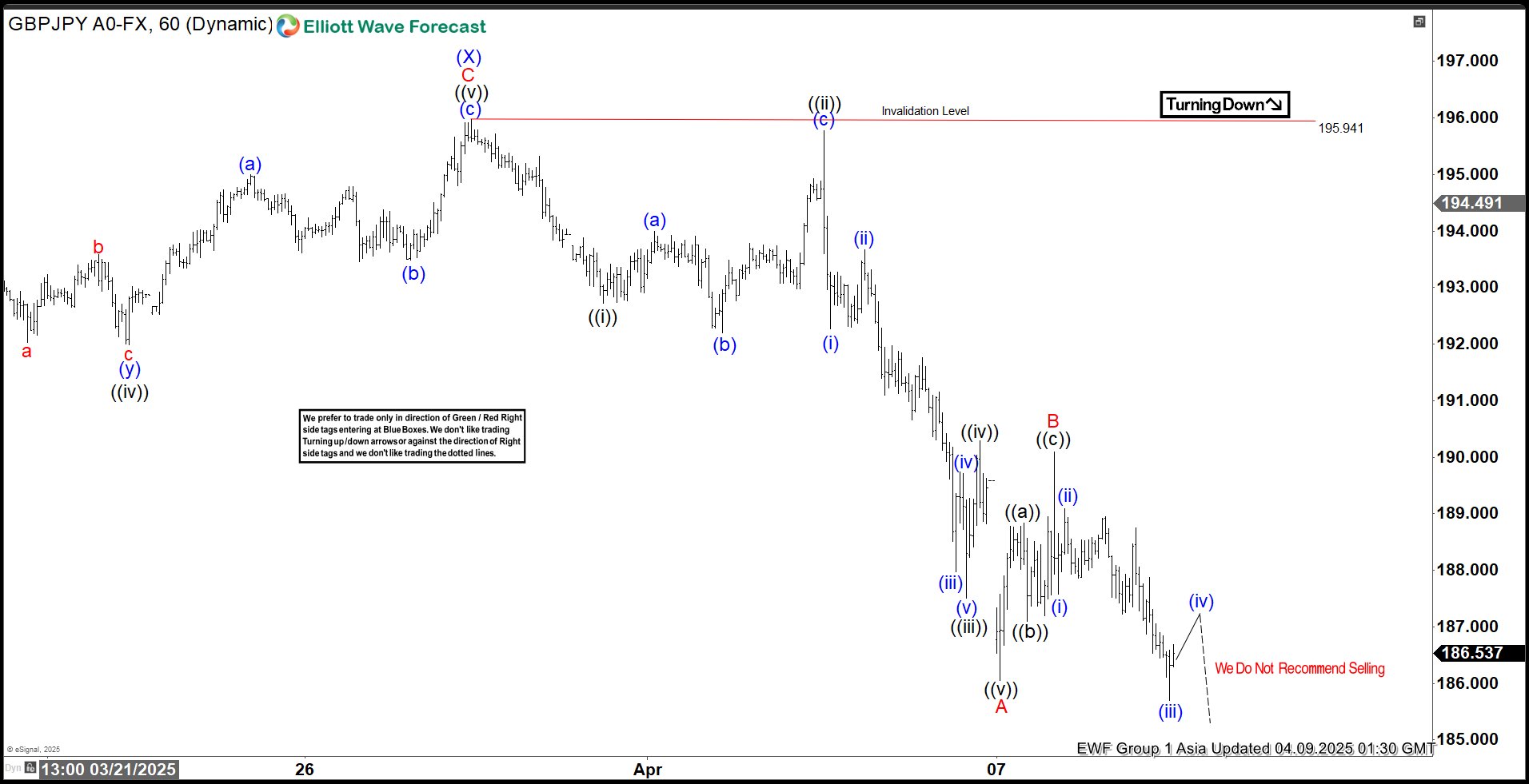

Elliott Wave Indicates Bearish Sequence for GBPJPY, Favoring a Downward Trajectory

The Elliott Wave perspective indicates that GBPJPY has entered a bearish sequence from its October 30, 2024 high. It signals further downside potential. From that peak, wave (W) concluded at 187.05, followed by a wave (X) rally that terminated at 195.94, as illustrated in the accompanying 1-hour chart. Currently, wave (Y) is unfolding lower, exhibiting an internal zigzag structure.

Breaking it down from the wave (X) high, wave ((i)) declined to 192.7. The subsequent wave ((ii)) rally peaked at 195.77. The pair then resumed its descent in wave ((iii)), reaching 187.51, before a wave ((iv)) bounce concluded at 190.29. The final leg, wave ((v)), completed at 186.05, marking the end of wave A in a higher degree. From there, wave B unfolded as a zigzag corrective pattern: wave ((a)) rose to 188.83, and wave ((b)) pulled back to 187.09. Wave ((c)) advanced to 190.08, completing wave B. The pair has since resumed its decline in wave C.

In the near term, as long as the pivotal high at 195.94 remains intact, any rallies are expected to falter in a 3, 7, or 11 swing structure, reinforcing the outlook for further downside. Traders monitoring this setup should anticipate limited upside and watch for confirmation of this bearish continuation.

GBPJPY 60 Minute Elliott Wave Chart

GBPJPY Video

https://www.youtube.com/watch?v=R06XEUzIPrw

A Day in the Shadow of Reciprocal Tariffs

In focus today

In the US, we will look out for any announcements following the implementation of Trump's reciprocal tariffs. Later in the day, Fed's Barkin is scheduled to speak, and the release of the FOMC minutes could give clues on discussions on the reaction function and the state of USD liquidity. In terms of recent tightening of financial conditions, we expect the Fed to adopt a wait-and-see approach, focusing on stabilising markets through verbal guidance before easing rates. Current market pricing suggests nearly five 25bp rate cuts this year, with a 50% chance of the first cut in the May meeting.

In the euro area, today's focus will be on the EU voting of the Commission's proposal to impose retaliatory tariffs of up to 25% on EUR21bn worth of US imports. This could trigger an even more aggressive response from Washington. Furthermore, we have a string of ECB speakers on the wire. The governing council seems to be in agreeance that the US trade policy aggression could provide a significant blow to global growth, so the question will be to what extend the hawkish camp still sees upside risks to inflation associated with tariffs.

Overnight, China is set to release CPI data.

Economic and market news

What happened overnight

In the US, President Trump's reciprocal tariffs took full effect this morning at 6.01 CET, targeting countries with the largest US trade deficits, while others remain subject to a 10% baseline tariff. Notably, a 104% tariff on Chinese goods has been implemented, following recent days' trade war escalation between the US and China. Speculations about a Chinese retaliation including CNY weakening and outright selling of US assets are now circulating in the media.

At a White House event Tuesday evening, President Trump mentioned that numerous countries are eager to make deals, expressing optimism that China would also pursue an agreement. Moreover, Trump signalled he may not be done with tariffs, and major tariffs on pharmaceutical import should soon be expected.

In New Zealand, the Reserve Bank of New Zealand lowered its policy rate to 3.50% (prior: 3.75%), as widely expected.

In commodities space, oil prices dropped to their lowest in more than four years in early trade on Wednesday, with Brent spot trading in the USD 60-61/barrel range this morning.

Long-end US Treasury yields are up by 20bp since yesterday despite risky assets seeing additional weakening. The sell-off was isolated to the bond market, which suggests that a correction in term premia was behind the move. Rumours about Chinese selling of US assets, hedge funds unwinding their US Treasury exposure and weak demand at yesterday's 3Y Treasury auction were all potential causes. Markets will await the outcome of tonight's 10Y UST auction, which will give further hints on whether the correction in yields since yesterday has added sufficient demand for duration.

What happened yesterday

In the euro area, the ECB speakers seemed aligned on the risk of a major demand shock following the new US tariffs. Germany's Nagel (hawk) stated that the new trade policy course in Washington has 'significantly worsened the global out, while Simcus (neutral/hawk) said that a 25bp cut next week 'will be needed', although he abstained from providing guidance on whether he expects another cut in June.

In Sweden, home prices were unchanged on the month in March, according to HOX Valueguard, following declines in January and February. The drop in transactions underlines household pessimism now showing up in hard data. In the coming months, the housing market faces further downside risk. Stock price declines affect household wealth as well as the overall sentiment, which could weigh on home price growth. In addition, a downtick in transactions indicate increasing supply. However, speculation about rate cuts might provide some relief.

In Denmark, the industrial production rebounded in February, rising by 5.1% after a significant drop in January. Despite this improvement, the output over the past three months remains lower than the previous period, partly due to fluctuations in pharmaceutical production.

In geopolitics, US Treasury Secretary Bessent criticised China's escalation of trade war tensions calling it "a big mistake", as the White House clarified the enforcement of additional 50% tariffs. Furthermore, during a Senate Finance committee hearing, USTR Greer confirmed that President Trump will not grant exemptions from new global tariffs, while efforts are being made to accelerate trade negotiations. Greer also clarified that the proposed fees for Chinese-built ships at U.S. ports will not all necessarily be cumulative.

In Ukraine, President Zelenskiy announced the capture of two Chinese nationals fighting for Russia in eastern Ukraine, raising concerns about China's involvement in the conflict. Ukraine is seeking responses from both China and the US, while the US State Department expressed disturbance over the claims.

Equities: Another volatile trading day, taking equities sharply lower and VIX back above 50. Equity markets are 80% determined by Trump, 15% comes from the unexpected rally in yields (more on that below) and 5% is the oversold positioning. However, valuation is in isolation not too low for an outright buy argument, macro data is completely outdated and Q1 earnings are too. This is why equity markets cannot simply "cope" with new tariffs threats and why we are not in the "it is all priced in" camp.

What looked like a rebound day for equities was therefore capped by new tariff threats from Trump (this time on pharma) and zero signs of China backing down. S&P 500 closed down -1.6% taking it -19% off its February record. This was not a capitulation session, far from it, with investors very picky on what to buy and sell. Investors - and we - were caught off guard by yields, sending real estate and consumer discretionary lower. Materials also a standout, weaker on fears on how tariffs will affect the Chinese economy. Meanwhile, an odd mix of banks, industrials and utilities outperformed, in a sign that investors are not yet wanting to add too much risk in cyclicality when tariff uncertainty is this high.

Asian and European futures are playing catch this morning, with Nikkei 225 down as much as -4% after the rally yesterday. Despite that the >100% tariffs are now live, investors are calmer in China (Hang Seng -1.6% and Shenzhen even 0.6% higher).

FI&FX: Risky assets gained from the start of yesterday's session, but the tailwinds faded gradually as the Trump administration stood firm on its intention to implement the reciprocal tariffs (and the Chinese 50% add-on) today. S&P 500 closed 1.5% lower after being up by 4% from the start of the session. This emphasises the current extreme intraday volatility. DXY is 1% lower since yesterday with EUR/USD now back above the 1.10 mark. EUR/CHF broke below the 0.93 mark as risk sentiment started to deteriorate again. EUR/NOK has moved above 12 as energy prices plunged further. Brent is trading at USD60.5/bbl this morning, the lowest level since early 2021. Long-end US Treasury yields have risen 20bp since yesterday despite the sell-off in risky assets.