Sample Category Title

Global Markets Rattled by US Tariffs, Again

Hopes of seeing Donald Trump roll back tariffs before they go live were dashed this morning—along with sentiment across global financial markets.

The Nikkei is down more than 2%, a Bloomberg index tracking Asian currencies fell to a record low, and European and US futures hint at another very, very ugly trading session, with losses between 2–4% at the time of writing. I won’t say much about yesterday’s rebound: moves of that magnitude – above 2–3% – aren’t sustainable unless there’s a clear resolution to the tariff problem.

China, on the other hand, is seeing limited losses across the CSI 300 companies. Despite being hit by 104% tariffs starting today, Chinese authorities said they will "fight to the end." That likely includes massive and unprecedented measures to keep the economy afloat. One of them: letting the yuan weaken to absorb part of the tariff cost. The USDCNY has dropped to its lowest levels since 2007 this morning. Expect rate cuts, liquidity injections, and other measures to follow, one after the other, as China digs in.

And China isn’t alone in promising support. The Reserve Bank of India (RBI) and the Reserve Bank of New Zealand (RBNZ) cut their interest rates by 25bp each. Kenya slashed its own rates by 75bp, pointing to tariff policy, and the European Central Bank (ECB) is expected to cut by 25bp at next week’s meeting – and the next.

Politics, politics

Trump’s trade policies continue to weigh on the US dollar, on rising recession bets—the dumbest recession in world history, probably. The Federal Reserve (Fed) hasn’t yet given public support to investors; instead, Fed members tell US monetary policy is well-positioned to cope with tariff disruptions. But a deeper selloff could change their minds.

Naturally, Fed officials—like everyone else—are worried about the impact massive tariffs will have on the US economy. Right now, we don’t know who will pay for them. Will exporters absorb the majority of the costs to protect their US market share? That would be the dream scenario for Trump: US consumers untouched, government coffers filled, and a political win. Or will exporters pass costs on to US consumers, thinking this won’t last and better to seek new markets? In that case, US inflation will rise, leaving the Fed irritated—and forced to act.

The Fed could still help the US economy weather the shock, but inflation would inevitably hit the economy—and people—and eventually Donald Trump at the mid-term elections.

China, for one, seems to be betting on that: losing market share now while hoping Americans will be hardly hit by inflation to reconsider Trump. I'm no political expert, but if negotiations don’t produce a reasonable outcome for European countries, the most logical move may be to make peace with China, so everyone takes a softer hit. It’s a bizarre twist—given how high global geopolitical tensions are—but it's up to politicians to be smart enough.

In FX, the dollar’s weakness pushes the EURUSD over the 1.10 mark again. Levels below 1.10 offer interesting dip-buying opportunities—especially if the global trade war intensifies, which it likely will. The euro could draw in some ‘safe haven’ flows. In fact, despite Europe's own stimulus plans, German bunds are increasingly seen as an alternative to US Treasuries. The German 10-year yield has been dropping steadily since mid-March, while the US 10-year spiked from under 4% to over 4.50% in just three sessions. The US 30-year hit 5% a few hours ago as companies are selling their liquid assets while investors simply don’t want to take the risk.

There are also rumours that China may be dumping US Treasuries in retaliation. All in all, the rising financial stress may require Fed intervention in the coming hours or days. But in the longer run, if the US isolates itself, the global ‘safe haven’ balance could shift—and Europe might benefit.

One hope is that the US resolves this from within. Elon Musk called Peter Navarro “truly a moron” and “dumber than a sack of bricks,” while Republican Senator Tillis asked, “whose throat do I get to choke if this turns out to be wrong?”

While they’re looking for someone to blame… a potential replacement of US Treasuries by gold—by China and other central banks—could partly explain gold’s rally past the $3,000 mark. Gold is well bid this morning amid the fire and dust.

US crude, on the other hand, traded below $57pb this morning as the escalating trade war hammers global growth prospects. The outlook remains negative. The next natural target for the bears is the psychological $50pb level.

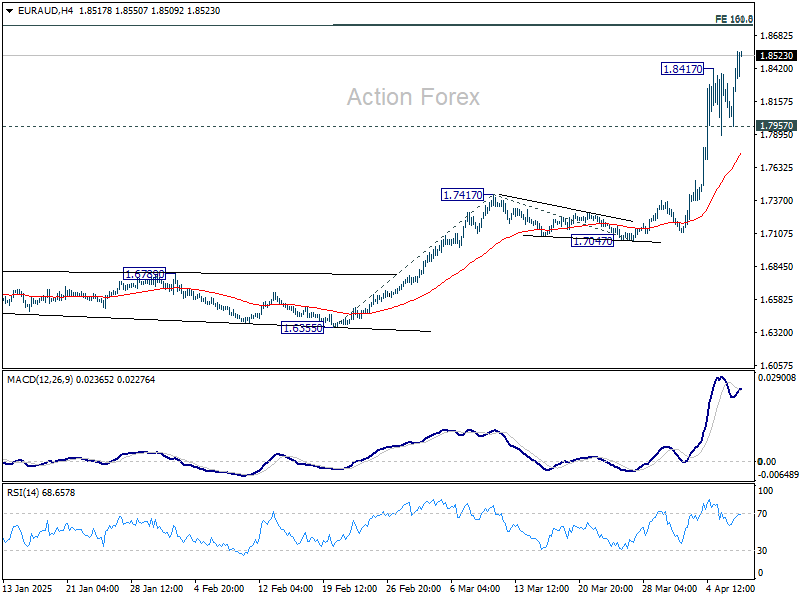

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.8097; (P) 1.8259; (R1) 1.8560; More...

EUR/AUD's rally resumed after brief retreat and intraday bias is back on the upside. Current up trend should target 161.8% projection of 1.6355 to 1.7417 from 1.7047 at 1.8765 next. On the downside, below 1.7957 minor support could now indicate short term topping, possibly on bearish divergence condition in 4H MACD, and bring lengthier consolidations.

In the bigger picture, up trend from 1.4281 (2022 low) is in progress, and in reacceleration phase as seen in W MACD. Next target is 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. Firm break there will pave the way to 138.2% projection at 1.9806, which is close to 1.9799 (2020 high). Outlook will remain bullish as long as 1.7417 resistance turned support holds even in case of deep pullback.

Reciprocal Tariffs Take Effect; China Hit with 104% Rate

The rebound in US stock markets proved short-lived, with major indexes slipping back into the red by the end of Tuesday's session. NASDAQ led the losses, as sentiment turned increasingly fragile. Asian markets followed suit, opening lower with large intraday volatility across the region. Concerns about a global recession continue to weigh heavily on investors' minds, particularly as the commodity complex offers no reprieve—oil prices plunged to fresh four-year lows on fears of a steep demand collapse.

Gold, traditionally a safe haven, is fighting to hold above the 3000 psychological level. The safe-haven metal has been benefiting from the market’s defensive posture. In the currency space, Dollar extended its slide, joined by other risk-sensitive currencies including Aussie, Kiwi and Loonie. Sterling wasn’t spared either. Meanwhile, Euro, Yen, and Swiss Franc are holding firm as traders flock toward relative safety amid escalating trade tensions.

The key driver of current market anxiety is the formal implementation of US reciprocal tariffs today, with the most aggressive action aimed at China. An eye-watering 104% effective tariff rate now applies to Chinese imports, effectively escalating the bilateral conflict into a full-blown trade war. Adding fuel to the fire, US President Donald Trump signed an executive order tripling tariff rates on low-value Chinese packages shipped through international postal systems.

This rapidly escalating standoff between the world’s two largest economies marks a dangerous phase in global trade, with both nations seemingly unwilling to blink first. The economic fallout remains difficult to quantify at this stage, but the longer the impasse drags on, the more serious the risks to global growth and supply chains. Perhaps most troubling is the collateral damage to third-party nations, which are now caught between the crosshairs of US-China economic warfare.

More tariff action is on the horizon. Adding more fuel to the fire, Trump indicated during a political dinner that a major new round of tariffs targeting pharmaceuticals would be announced "very shortly." These measures are expected to be aimed at shifting pharmaceutical production out of China and back into the US, with rates speculated to reach 25% or higher. The move has sparked concern not only about inflation in drug prices but also about global supply chain disruptions in the healthcare sector.

Elsewhere, Canada confirmed its retaliation, implementing 25% tariffs on US-made vehicles. Japan, another major trading partner, is bracing for heightened scrutiny. Finance Minister Katsunobu Kato noted that exchange rate policies may enter upcoming discussions, indicating that Washington's pressure on currencies—particularly Yen—could be a brewing flashpoint.

Technically, an immediate focus in on 1.0741 in GBP/CHF as selloff accelerates further this week. Firm break there will solidify the case that corrective pattern from 1.0183 has already completed, be it counted as at 1.1675 or 1.1501. Larger down trend should then be ready to resume through 1.0183 (2022 low).

In Asia, at the time of writing, Nikkei is down -4.14%. Hong Kong HSI is down -1.43%. China Shanghai SSE is up 0.21%. Singapore Strait Times is down -2.44%. Japan 10-year JGB yield is down -0.024 at 1.255. Overnight, DOW fell -0.84%. S&P 500 fell -1.57%. NASDAQ fell -2.15%. 10-year yield rose 0.107 to 4.262.

RBNZ cuts 25bps, trade barriers as downside risk to both growth and inflation

RBNZ delivered a widely expected 25bps cut in the Official Cash Rate, bringing it to 3.50%. The policy statement highlighted that the recently announced global trade barriers create "downside risks to the outlook for economic activity and inflation" in New Zealand.

The central bank noted that with inflation close to the midpoint of its target range, it is in the "best position" to respond to economic shifts. RBNZ added it has "has scope to lower the OCR further as appropriate", depending on how the impact of tariffs evolves.

This leaves the door wide open for further easing, particularly if global economic headwinds intensify or domestic data disappoints.

NZD/USD edged lower earlier today with broad risk aversion, but there is no particular selloff after RBNZ's decision.

Technically, the breach of 0.5515 support suggests that recent fall from 0.6378 is resuming. Near term risk will stay on the downside as long as 0.5644 resistance holds. Next target is 61.8% projection of 0.6378 to 0.5515 from 0.5852 at 0.5319.

But more importantly, sustained trading below 0.5467 (2020 low) would confirm resumption of whole downtrend from 0.8835 (2014 high). That would pave the way to 61.8% projection of 0.7463 to 0.5511 from 0.6378 at 0.5172 in the medium term.

Fed’s Goolsbee: Tariff shock far exceeds expectations; Daly calls for caution

Chicago Fed President Austan Goolsbee and San Francisco Fed President Mary Daly both sounded cautious overnight amid rising uncertainty from the unfolding global tariff war.

Goolsbee highlighted the unexpected magnitude of the tariff impact, calling them a “way bigger” shock than anticipated. He likened them to a "negative supply shock" and acknowledged that Fed's appropriate policy response is unclear.

He warned of ripple effects through slower consumer and business activity, especially in a post-pandemic economy still scarred by past inflationary surges.

Meanwhile, Daly struck a more measured tone, noting that while she is "a little concerned" about the inflationary effects of tariffs, she emphasized Fed's current policy is well-positioned and policymarkers can "just tread slowly and tread carefully."

"The thing that's really important is you stay steady in the boat while you think about not what's happening over the last two days, but the net effect of the slate of changes that any administration wants to take," she added.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.8097; (P) 1.8259; (R1) 1.8560; More...

EUR/AUD's rally resumed after brief retreat and intraday bias is back on the upside. Current up trend should target 161.8% projection of 1.6355 to 1.7417 from 1.7047 at 1.8765 next. On the downside, below 1.7957 minor support could now indicate short term topping, possibly on bearish divergence condition in 4H MACD, and bring lengthier consolidations.

In the bigger picture, up trend from 1.4281 (2022 low) is in progress, and in reacceleration phase as seen in W MACD. Next target is 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. Firm break there will pave the way to 138.2% projection at 1.9806, which is close to 1.9799 (2020 high). Outlook will remain bullish as long as 1.7417 resistance turned support holds even in case of deep pullback.

First Impressions: RBNZ Monetary Policy Review

The RBNZ delivered the expected 25bp OCR cut in April and maintained an easing bias. Risks related to global developments were noted, but the overall tone didn’t suggest a sense of undue alarm.

RBNZ 9 April OCR Review

- As widely expected, the RBNZ lowered the OCR by 25bps to 3.5%.

- The RBNZ sees downside risks to the medium-term inflation outlook.

- But the overall tone doesn’t suggest a sense of undue alarm.

- High uncertainty about the outlook due to global developments was recognised, along with a sense that events are still recent.

- The RBNZ sees the domestic economy as having evolved in line with their February expectations.

- Westpac expects another 25bp cut in May. The downside risks to the outlook imply risks of further easing from there, but data will determine the extent to which these crystallise.

OCR cut by 25bps to 3.50%, as expected

As strongly signalled in the February MPS, and more than fully priced by markets, the RBNZ today announced a further 25bps reduction in the OCR to 3.5%.

More importantly, regarding the outlook for policy at future meetings, the RBNZ indicated that they see downside risks to growth and inflation reflecting the global trade shock unfolding in recent days. The view on downside risks to growth looks like a consensus view:

“Against this backdrop, the recently announced increases in tariffs in the United States, retaliation from several trading partners, and heighted geoeconomic uncertainty will have a significant negative impact on global growth. This will have adverse effects for domestic economic activity.”

Regarding inflation there is more uncertainty, although still a sense of downside medium term risks:

“Most members of the Committee consider that recent global policy developments have shifted the balance of risk for New Zealand inflation lower over the medium term. Others note that, while uncertainty around the inflation outlook has increased, the risks remain balanced at this stage.”

The outlook for interest rates looks tilted towards more easing. A 25bp cut at the May Monetary Policy Statement looks like a firm possibility. There are appreciable chances of additional easing, either in May or later, depending on how global events evolve and on how these translate to the New Zealand outlook. The MPC is not tying their hands here in that regard.

Regarding the impact of the change in the global outlook, the RBNZ’s read looks as expected. Hence, they see the predictable downside risks to growth and hopes of inflation being controlled over the medium term, while acknowledging the uncertainty about what happens in the short term.

The MPC notes, correctly, that both the supply and demand sides of the global economy have changed, and there is little that monetary policy can do to counteract the more permanent losses to the supply side of the economy.

“The adaptation of global supply chains to increased trade barriers will take longer to work through. It was noted that monetary policy cannot offset the long-term negative supply-side effects of higher barriers to international trade.”

The role of the New Zealand dollar is acknowledged as play a role in buffering the economy from this global shock. Westpac’s view is that the exchange rate will do most of heavy lifting in that regard. That the RBNZ says the recent decline in the NZD will “help” cushion the blow implies there is a role of interest rates as well – reasonably:

“The recent decline in the New Zealand dollar will help to cushion the immediate effect of decreased global demand for New Zealand exports. Lower oil prices will also support domestic consumption and production.”

Finally, importantly the RBNZ sees the overall economy as having evolved as expected in recent months, albeit with some differences in the composition of growth.

“Economic activity in New Zealand has evolved largely as expected since the February Monetary Policy Statement. Higher-than-expected export prices and a lower exchange rate have supported primary sector incomes and overall economic growth. While monetary restraint has been removed at pace, household spending and residential investment have remained weak.”

It doesn’t appear that there is a significant “starting point” difference for the RBNZ to account for leading into the global tariff shock.

Hence regarding the outlook for interest rates, the path is clear for further OCR cuts. The scale and timing of cuts will depend on unfolding events.

“As the extent and effect of tariff policies become clearer, the Committee has scope to lower the OCR further as appropriate. Future policy decisions will be determined by the outlook for inflationary pressure over the medium term.”

Westpac’s interpretation and rate call

The RBNZ’s statement did not convey any sense of undue alarm. The downside risks to the trading partner outlook are clear and appropriately highlighted in the press release and the Statement of Record.

It’s likely the 25bp cut to 3.25% we currently forecast in the May Monetary Policy Statement will occur. The choice is likely between 25 and 50bp but it’s hard to say how large the adjustment will be now.

There are downside risks to our current forecast of a trough in the OCR of 3.25%. We will assess these forecasts considering emerging events, financial market developments and domestic data when we review our forecasts in May when we prepare the Economic Overview, or sooner if appropriate.

The RBNZ is correct in not being prescriptive in terms of how global events will evolve and how they will impact on NZ. The reaction of the New Zealand dollar will be key in that regard. We expect the New Zealand dollar to take on a significant part of the adjustment – especially if darker scenarios emerge. This will complicate the usual playbook of cutting rates to support growth.

If significant rate cuts are required, then these will likely further cement in the tentative recovery of the domestic economy that has been taking hold up until now. Large OCR cuts could end up being procyclical if the NZD is doing its job and providing stimulus.

Future things to watch

Looking ahead to the 28 May MPS, the case for future easing will depend on how the global outlook evolves and how that is expected to impact the outlook for activity and inflation In New Zealand.

We are not aware of any scheduled commentary from the RBNZ in coming days on the monetary policy outlook. Chief Economist Paul Conway will be holding a webinar on Tuesday 15 April. This webinar is not advertised as having monetary policy content – but worth watching nonetheless.

As far as domestic economic indicators are concerned, the key high frequency indicators to watch are:

- Consumer and business confidence surveys (24 and 30 April)

- The PMI and PSI surveys (11 and 14 April, 16 and 19 May)

- Filled jobs (29 April) and job advertisements (16 April and 14 May)

- Housing market indicators (mid-April and May)

In addition, the Q1 CPI (17 April) will of course be key in determining the baseline for headline and non-tradable inflation. The Q1 labour market reports (7 May) will be critical as these will set the tone for expectations of the path for the unemployment rate and growth in labour costs in coming quarters. The RBNZ likely needs to modestly upgrade its peak unemployment rate forecast. These reports will tell us by how much. The lead-up to the Budget on 22 May will also be of interest given the risks that the Government expands spending to cover pressing priorities in both operational and capital spending, notwithstanding recent comments made by the Minister of Finance.

Aside from economic data, developments in international commodity prices – especially for New Zealand’s key exports – and the exchange rate will also be important in gauging the extent to which additional interest rate support is likely to be required to ensure that spare capacity in the economy is eliminated, and that inflation stays close to the centre of the RBNZ’s target band.

RBNZ cuts 25bps, trade barriers as downside risk to both growth and inflation

RBNZ delivered a widely expected 25bps cut in the Official Cash Rate, bringing it to 3.50%. The policy statement highlighted that the recently announced global trade barriers create "downside risks to the outlook for economic activity and inflation" in New Zealand.

The central bank noted that with inflation close to the midpoint of its target range, it is in the "best position" to respond to economic shifts. RBNZ added it has "has scope to lower the OCR further as appropriate", depending on how the impact of tariffs evolves.

This leaves the door wide open for further easing, particularly if global economic headwinds intensify or domestic data disappoints.

NZD/USD edged lower earlier today with broad risk aversion, but there is no particular selloff after RBNZ's decision.

Technically, the breach of 0.5515 support suggests that recent fall from 0.6378 is resuming. Near term risk will stay on the downside as long as 0.5644 resistance holds. Next target is 61.8% projection of 0.6378 to 0.5515 from 0.5852 at 0.5319.

But more importantly, sustained trading below 0.5467 (2020 low) would confirm resumption of whole downtrend from 0.8835 (2014 high). That would pave the way to 61.8% projection of 0.7463 to 0.5511 from 0.6378 at 0.5172 in the medium term.

(RBNZ) OCR: 3.5% – Further reduction in OCR appropriate

The Monetary Policy Committee today agreed to reduce the Official Cash Rate by 25 basis points to 3.5 percent.

Annual consumer price inflation remains near the mid-point of the Monetary Policy Committee’s 1 to 3 percent target band. Firms’ inflation expectations and core inflation are consistent with inflation remaining at target over the medium term.

Economic activity in New Zealand has evolved largely as expected since the February Monetary Policy Statement. Higher-than-expected export prices and a lower exchange rate have supported primary sector incomes and overall economic growth. While monetary restraint has been removed at pace, household spending and residential investment have remained weak.

The recently announced increases in global trade barriers weaken the outlook for global economic activity. On balance, these developments create downside risks to the outlook for economic activity and inflation in New Zealand.

Having consumer price inflation close to the middle of its target band puts the Committee in the best position to respond to developments. As the extent and effect of tariff policies become clearer, the Committee has scope to lower the OCR further as appropriate. Future policy decisions will be determined by the outlook for inflationary pressure over the medium term.

Summary Record of Meeting – April 2025

Annual consumer price inflation remains near the mid-point of the Monetary Policy Committee’s 1 to 3 percent target band. Firms’ inflation expectations and core inflation are consistent with inflation remaining at target over the medium term. The recently announced increases in global trade barriers have weakened the outlook for global economic activity and, on balance, create downside risks to the outlook for inflation in New Zealand over the medium term.

Domestic economic activity has evolved largely as projected in February

The Committee discussed developments in domestic economic activity. Higher-than-expected export prices and a lower exchange rate have supported primary sector incomes and overall economic growth. However, household spending and residential investment have been weaker than expected.

The Committee noted that substantial spare productive capacity remains in the economy. This reflects the preceding period of restrictive interest rates, subdued global economic activity, and lower government consumption as a share of the economy. Overall, expectations of future inflation and the degree of spare productive capacity in the economy are consistent with annual CPI inflation remaining close to the target midpoint over the medium term.

Recent declines in interest rates and higher export earnings are expected to support economic growth. The pace of growth is expected to be modest, as potential GDP growth is constrained by ongoing weakness in productivity growth and low net immigration. The Committee noted that the full economic impact of cuts in the OCR since August 2024 are yet to be fully realised.

Recent increases in tariffs and uncertainty about global trade policy have weakened the outlook for global economic activity

Against this backdrop, the recently announced increases in tariffs in the United States, retaliation from several trading partners, and heighted geoeconomic uncertainty will have a significant negative impact on global growth. This will have adverse effects for domestic economic activity.

The implications of increased tariffs for global and domestic inflation are more ambiguous

The Committee noted that the impact of increased tariffs on global inflation is unclear at this point, particularly given the recency of the announcement and the possibility of further changes in global trade policy settings. The implications for inflation will vary by country.

Several factors stemming from tariff increases could put upward pressure on global prices over the medium term. Prices will rise in tariff-imposing countries, reflecting the higher cost of imports. Increased trade protectionism and uncertainty will also lower the productive capacity of the global economy. The costs of trade could also rise as global supply chains adapt to increased trade restrictions and geoeconomic fragmentation.

The Committee noted that there were several factors that could offset these cost and supply-side elements. For New Zealand, demand for our exports is likely to decrease, reflecting weaker activity in our trading partner economies, especially in Asia. Increased uncertainty around global trade policy will also weigh on investment and spending, as will declines in asset prices.

Trade diversion effects could also lower the prices of New Zealand’s imports, as some global exports targeted by tariffs are redirected to our market. Lower global oil prices will also lower New Zealand import prices.

The global policy response will be an important consideration in gauging the implications of increased tariffs for medium-term inflation in New Zealand. For example, an easing in fiscal and monetary policy in our trading partners could mitigate some of the expected downturn in global economic activity. The Committee noted fiscal policy had been eased in China and Europe recently. Structural reforms, trade, and industrial policy responses may also offset some of the impacts of increased trade barriers.

The recent decline in the New Zealand dollar will help to cushion the immediate effect of decreased global demand for New Zealand exports. Lower oil prices will also support domestic consumption and production.

The Committee was briefed on the financial market reaction to the tariff announcements. While price movements in currency, equity and fixed-income markets have been large there are currently no significant signs of dysfunction in financial markets.

The monetary policy response to tariffs will focus on the medium-term implications for inflation

Most members of the Committee consider that recent global policy developments have shifted the balance of risk for New Zealand inflation lower over the medium term. Others note that, while uncertainty around the inflation outlook has increased, the risks remain balanced at this stage.

The Committee noted that the increase in tariffs will take time to work through the global economy. The direct price increases for economies imposing tariffs and the dampening impact of increased economic uncertainty on global demand will occur relatively quickly. The adaptation of global supply chains to increased trade barriers will take longer to work through. It was noted that monetary policy cannot offset the long-term negative supply-side effects of higher barriers to international trade.

The Committee agreed to lower the OCR

The Committee noted that the preceding cuts to the OCR have yet to have their full effect on the economy.

With CPI inflation close to the mid-point of the target range, significant spare capacity in the economy, and a weaker activity outlook stemming from global trade policy, the Committee agreed that a further reduction in the OCR was appropriate.

The Committee agreed that a 25 basis point reduction in the OCR would be consistent with their mandate of maintaining low and stable inflation. As the extent and effect of tariff policies become clearer, the Committee has scope to lower the OCR further as appropriate. Future policy decisions will be determined by the outlook for inflationary pressure over the medium term.

Attendees

Members of MPC: Christian Hawkesby (Chair), Bob Buckle, Carl Hansen, Karen Silk, Paul Conway, Prasanna Gai

Treasury Observer: James Beard

MPC Secretary: Adam Richardson

Fed’s Goolsbee: Tariff shock far exceeds expectations; Daly calls for caution

Chicago Fed President Austan Goolsbee and San Francisco Fed President Mary Daly both sounded cautious overnight amid rising uncertainty from the unfolding global tariff war.

Goolsbee highlighted the unexpected magnitude of the tariff impact, calling them a “way bigger” shock than anticipated. He likened them to a "negative supply shock" and acknowledged that Fed's appropriate policy response is unclear.

He warned of ripple effects through slower consumer and business activity, especially in a post-pandemic economy still scarred by past inflationary surges.

Meanwhile, Daly struck a more measured tone, noting that while she is "a little concerned" about the inflationary effects of tariffs, she emphasized Fed's current policy is well-positioned and policymarkers can "just tread slowly and tread carefully."

"The thing that's really important is you stay steady in the boat while you think about not what's happening over the last two days, but the net effect of the slate of changes that any administration wants to take," she added.

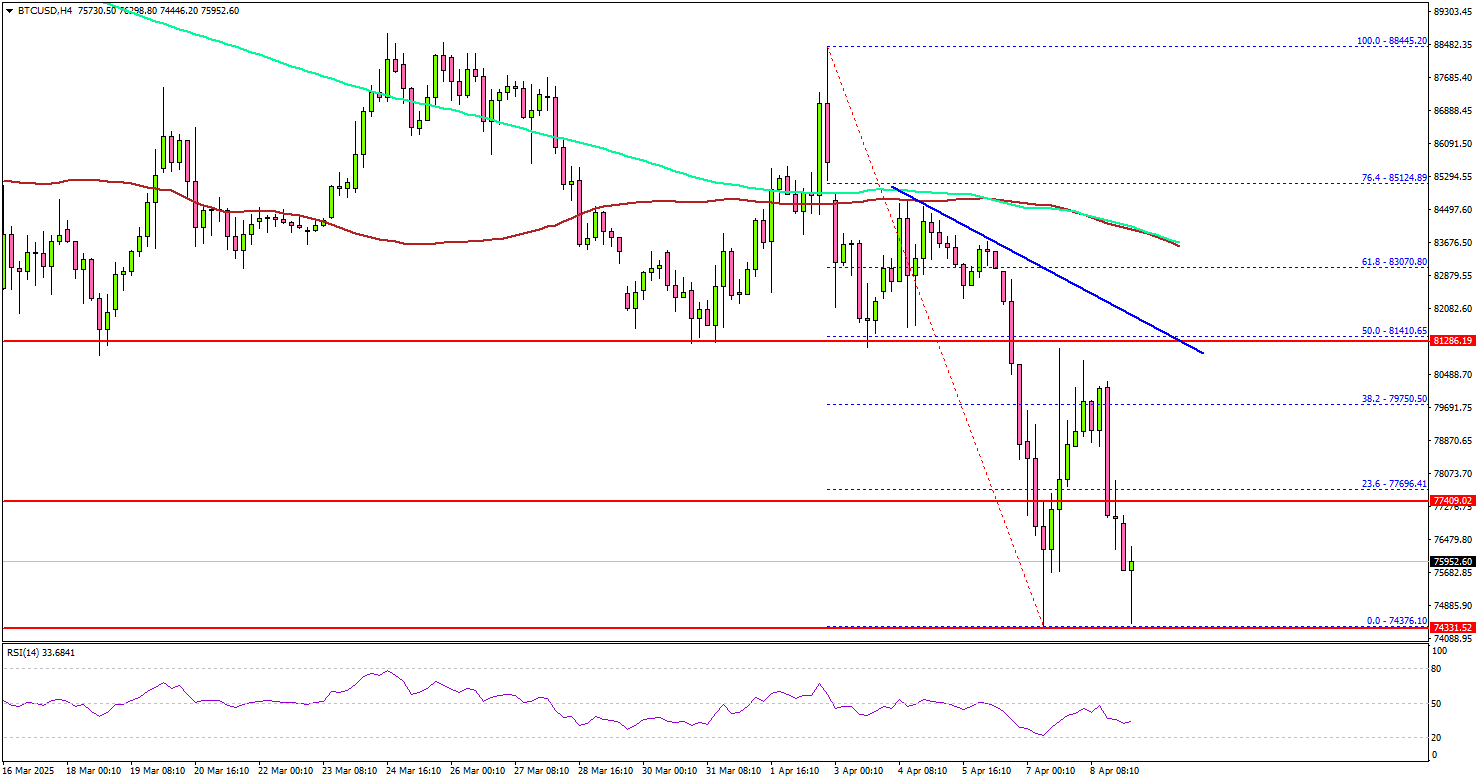

Bitcoin Stuck In The Struggle Zone—Will It Break Free?

Key Highlights

- Bitcoin price started a recovery wave after a sharp drop to $75,000.

- BTC is trading below a connecting bearish trend line with resistance at $81,500 on the 4-hour chart.

- Ethereum price declined heavily and even tested the $1,420 zone.

- WTI crude oil prices started a consolidation phase near $60.00.

Bitcoin Price Technical Analysis

Bitcoin price started a major decline below $85,000 against the US Dollar. BTC declined below $80,000 and tested $75,000 before the bulls appeared.

Looking at the 4-hour chart, the price settled below the $82,000 level, the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). A low was formed at $74,376 and the price started an upside correction.

There was a move above the $78,000 level. The price climbed above the 38.2% Fib retracement level of the downward move from the $88,445 swing high to the $74,376 low.

On the upside, the price could face resistance near the $81,500 level. There is also a connecting bearish trend line forming with resistance at $81,500 on the same chart. The trend line is close to the 50% Fib retracement level of the downward move from the $88,445 swing high to the $74,376 low.

The next key resistance is $83,000. The main resistance could be $85,000. A successful close above $85,000 might start another steady increase. In the stated case, the price may perhaps rise toward the $88,000 level. Any more gains might call for a test of $90,000.

Immediate support is near the $78,000 level. The next key support sits at $76,800. A downside break below $76,800 might send Bitcoin toward the $75,000 support. Any more losses might send the price toward the $73,200 support zone.

Looking at Ethereum, there was a major decline below $2,000 and $1,800 before the bulls appeared near the $1,420 level.

Today’s Economic Releases

- FOMC Minutes.

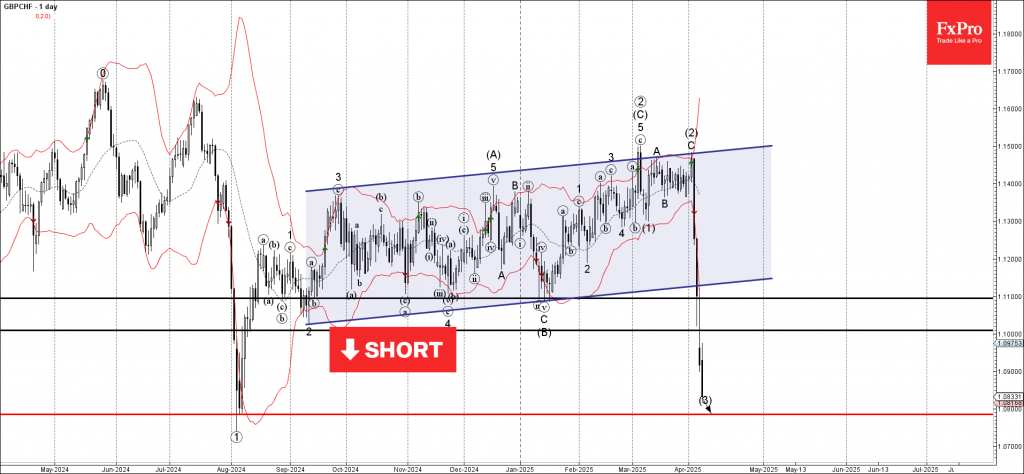

GBPCHF Wave Analysis

GBPCHF: ⬇️ Sell

- GBPCHF broke the support zone

- Likely to fall to support level 1.0785

GBPCHF currency pair recently fell sharply through the support zone between the support levels 1.1000 and 1.1100. The breakout of this support zone was preceded by the breakout of the daily up channel from September.

The breakout of these support levels accelerated the active intermediate impulse wave (3) from the start of August.

Given the strongly bullish Swiss franc sentiment seen recently, GBPCHF currency pair can be expected to fall to the next support level 1.0785, the target price for the completion of the active intermediate impulse wave (3).

WTI Wave Analysis

WTI: ⬇️ Sell

- WTI broke the long-term support zone

- Likely to fall to support level 55.00

WTI crude oil recently broke the long-term support zone set between the support levels 60.00 and 65.00. This support zone has stopped all downward corrections from the middle of 2021.

The breakout of this support zone accelerated the active downward impulse wave 3, which belongs to the intermediate impulse wave (3) from the start of 2024.

Given the strong downtrend seen on the weekly WTI charts, WTI crude oil can be expected to fall to the next support level 55.00, the target price for the completion of the active impulse wave (3).