Sample Category Title

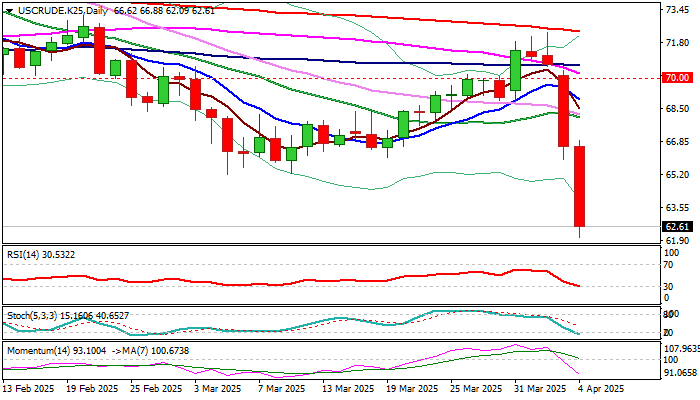

WTI Oil: Bears Hold Grip After Massive Losses in Past Two Days

WTI oil price remains in a steep fall for the second straight day and hits the lowest levels since December 2021 on Friday, after US tariffs rattled global markets and soured sentiment.

Unexpected decision of OPEC+ group to increase production above consensus from May, added to strong bearish outlook.

Oil prices fell around 11% in less than two days, on track for the worst week since the first week of October 2023.

Key longer-term supports at $62.42/$61.79 (lows of Dec/Aug 2021 that formed a higher base on monthly chart) are under increased pressure.

Firm break of these levels to signal further weakness with immediate target at $60.00 (psychological), loss of which to expose $53.87 (Fibo 61.8% of $6.52/$130.48 uptrend).

Bears show so far limited signs of fatigue despite recent massive losses, however oversold daily studies and Friday’s profit taking may keep bears on hold for some time.

According to current situation, upticks are likely to be limited and offer better levels to re-enter firmly bearish market.

Former base at $65.22/25 (Mar 5/11) act as resistance which should limit recovery action.

Res: 63.00; 64.49; 65.22; 65.98.

Sup: 62.00; 61.70; 60.86; 60.00.

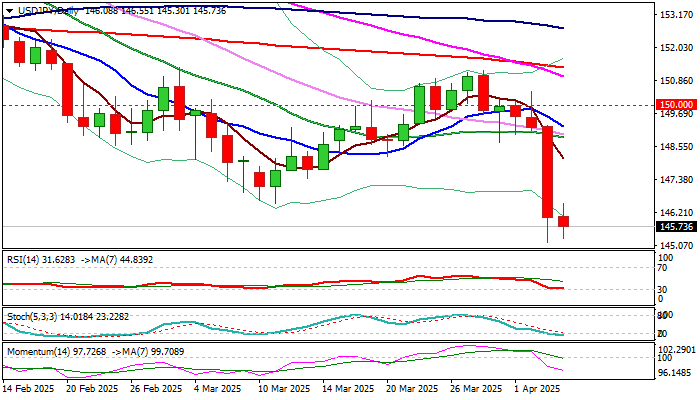

Yen Pummels US Dollar, Nonfarm Payrolls Next

The Japanese yen has extended its gains on Friday. In the European session, USD/JPYis trading at 145.44, down 0.52% on the day. The yen is trading at its strongest level since September 2024.

US nonfarm payrolls expected to drop

Investors are still digesting the massive losses sustained in the financial markets, but will have to shift and focus on today's US nonfarm payrolls. The market estimate stands at 135 thousand, lower than the February gain of 151 thousand. The US labor market has been softening at a gradual pace and the Fed is hoping that trend continues.

Federal Reserve policymakers were looking at two rate cuts this year, but President Trump's bombshell tariff announcement will force the Fed to re-examine its growth and inflation forecasts.

What can we expect from the Fed?

That is no simple question, as the tariffs have sent the equity markets tumbling and deep uncertainty hangs in the air. The tariffs will boost inflation but also dampen growth, making for a tricky balance for the Fed. The money markets expect a slower US economy to dictate rate policy rather than inflation and that could mean as many as four cuts in 2025 if the economy tips into a recession.

Japan's household spending recovered in February with a gain of 3.5% m/m, after a 4.5% decline in January. This crushed the market estimate of 0.5% and was the strongest pace of growth since March 2022. The Bank of Japan is keeping a close eye on consumption as it determines when to raise interest rates and it is unclear how the new US tariffs will affect consumer confidence and spending.

WTI Oil Technical Outlook: Bears Gaining Strength for a Major Bearish Breakdown

- Global recession risk has triggered a significant drop in oil prices.

- WTI crude is now facing a negative double whammy from weak external demand and excess supplies built up.

- WTI crude is now breaching below a key major range support at US$65.40.

Since our last publication, the price actions of West Texas Oil CFD (a proxy of the WTI crude oil futures) have staged the expected corrective rebound sequence and rallied by 7.2% to print an intraday high of US$72.48/barrel on 2 April (a whisker below the US$73.50 medium-term resistance highlighted in our report) before the announcement of “US Liberation Day” reciprocal trade tariffs.

The West Texas Oil CFD has shaped a significant bearish reversal ex-post “US Liberation Day”, and plummeted by 6% on 3 April, its worst daily loss since early September 2022.

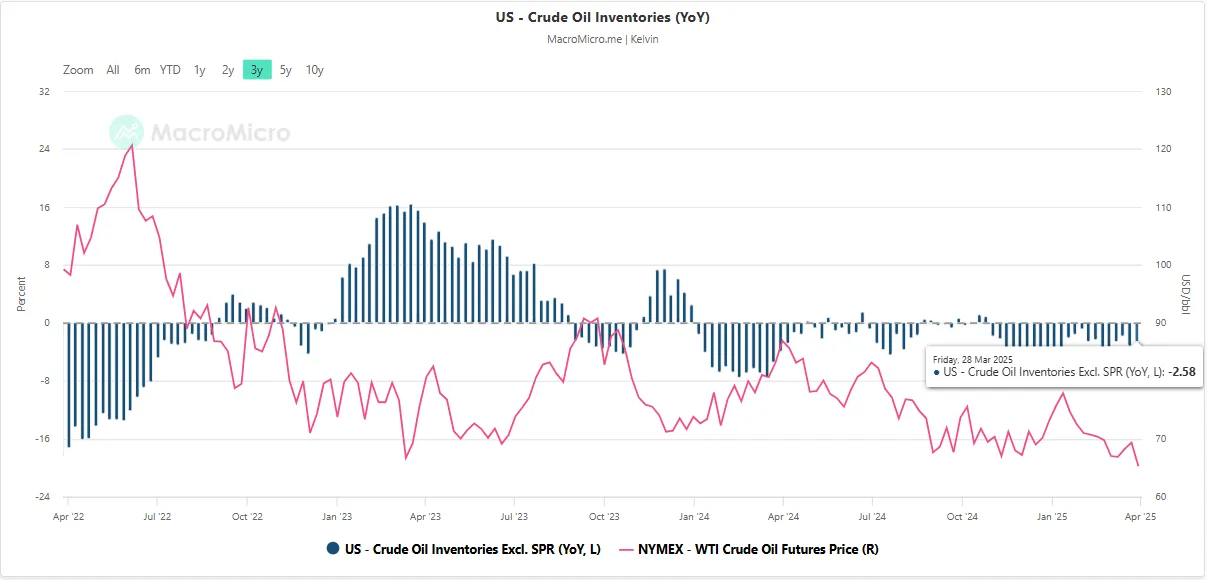

Headwinds from weak demand and excess supply

Fig 1: EIA US crude oil inventories excluding SPR (y/y change) with WTI crude oil futures as of 28 Mar 2025 (Source: MacroMicro)

WTI crude has a negative double whammy hit caused by demand and supply factors. Firstly, the rising probability of a stagflation environment in the US has triggered a global recession alarm, in turn, weakening demand for oil as business activities slow down.

Secondly, OPEC+ producers have agreed to boost the cartel's oil output by 411,000 barrels per day next month, coupled with a recent lesser magnitude of drawdown of US crude oil inventories seen in the past three weeks that may add another layer of downside pressure in oil prices.

The growth of US crude oil inventories excluding the Strategic Petroleum Reserve (SPR) on a year-on-year basis has an indirect correlation with the movement of WTI crude oil, as build-up in oil inventories puts downside pressure on oil prices.

Since 13 December 2024, the drawn down of US crude oil inventories (excluding SPR) has slowed down from -5.11% y/y to -2.58% y/y as of 28 March 2025 based on data from the US Energy Information Administration (EIA) (see Fig 1).

US 65.40 key support is looking vulnerable

Fig 2: West Texas Oil CFD medium-term trend as of 4 Apr 2025 (Source: TradingView)

Current intraday price actions of the West Texas Oil CFD (a proxy of the WTI crude oil futures) have recorded a further drop of 3.2% on Friday, 4 April, and breached below the major “Descending Triangle” range support of US$65.40 at this time of writing (see Fig 2).

In addition, the daily MACD trend indicator has just flashed out a bearish crossover condition, and inched below its centreline, which increases the probability of a major bearish breakdown below the US$65.40 major range support.

A daily close below US$65.40 may trigger the start of a medium-term bearish impulsive down move sequence to expose the next medium-term support zone of US$$60.20/58.80.

However, a clearance above the US$72.50 medium-term pivotal resistance (also the key 200-day moving average) invalidates the bearish scenario to kickstart another round of choppy corrective rebound phase for the next medium-term resistances to come in at US$76.00 and US$80.30

Markets Eye US, Canada Job Reports, US Dollar Steadies

The Canadian dollar has taken a break after an impressive three-day rally, in which the currency climbed about 2%. In the European session, USD/CAD is trading at 1.4148, up 0.39%. On Thursday, the Canadian dollar touched 140.26, its strongest level since December.

US nonfarm payrolls expected to dip

The hottest financial news is understandably the wave of selling in the equity markets, but there are some key economic releases today as well. The US and Canada will both release the March employment report later today.

The US releases nonfarm payrolls, with the markets projecting a gain of 135 thousand, after a gain of 151 thousand in February. This would point to the US labor market cooling at a gradual pace, which suits the Federal Reserve just fine. The Fed will also be keeping a watchful eye on wage growth, which is expected to tick lower to 3.9% y/y from 4.0%. The unemployment rate is expected to hold at 4.1%.

The employment landscape is uncertain, with the DOGE layoffs and newly-announced tariffs expected to dampen wage growth in the coming months.

Canada's employment is expected to improve slightly to 12 thousand, after a negligible gain of 1.1 thousand in February. Unemployment has been stubbornly high and is expected to inch up to 6.7% from 6.6%.

Canada vows retaliatory tariffs against US

US President Donald Trump's tariff bombshell on Wednesday did not impose new tariffs on Canada, but trade tensions continue to escalate between the two allies. Canada said it would mirror the US stance and impose a 25% tariff on all vehicles imported from the US that do not comply with the US-Canada-Mexico-Canada free trade deal. The US has promised to respond to any new tariffs against the US, which could mean a tit-for-tat exchange of tariffs between Canada and the US.

US/Canada Technical

- USD/CAD has pushed above resistance at 1.4088 and 141.26. The next resistance line is 1.4170

- 1.4044 and 1.4006 are the next support levels

USD/JPY: Bears Take a Breather But Recovery Likely Limited

USDJPY edged higher on Friday morning, showing a partial recovery of Thursday’s 2.1% drop (the biggest daily drop since 1 May 2024).

Long lower shadows of daily candles of today/Thursday) point to growing bids) although recovery is unlikely to accelerate as fundamentals remains favorable for safe haven Japanese yen.

Risk aversion is on the rise and continues to prompt traders into safety, while dollar remains under strong pressure from tariffs and hopes of more dovish Fed’s stance on interest rates, although the central bank will remain extremely cautious and base its future decisions on economic conditions.

Release of US March labor data will be key economic event today, with non-farm payrolls likely slowing in March, but forecasts point to still steady conditions and more negative impact from mass firing of public sector workers to likely show in coming months.

Fresh bears look for weekly close below broken pivots at 146.95/53 (Fibo 61.8% of 139.57/158.87/Mar 11 low respectively) to validate bearish signal (the pair is on track for a weekly loss of about 2.5%) and focus next targets at 144.13 (Fibo 76.4%) violation of which to unmask140.00/139.27 (psychological/Fibo 38.2% of larger 102.59/161.95 uptrend) in extension.

Initial resistance at 146.60 (Marr 11 former low / Fibo 23.6% of 153.20/145.18 bear-leg) holds for now and should ideally cap upticks.

Res: 146.60; 147.48; 148.19; 148.90.

Sup: 145.18; 144.13; 143.65; 142.97.

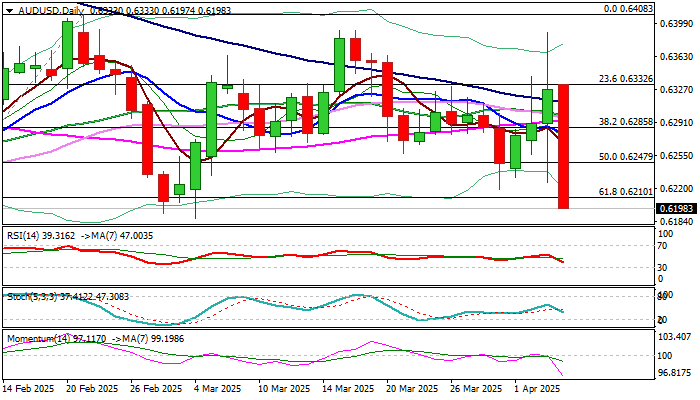

AUD/USD Top Loser of Asian/Early European Trading on Friday

AUDUSD was sharply down during Asian / early European sessions on Friday, falling over 2% so far and being the top loser of the day.

The Ausie dollar remains under strong pressure from risk aversion that continue to weaken stocks and commodities, with stronger dollar on Friday morning, adding to negative near term outlook.

Today’s bearish acceleration has so far retraced over 61.8% of 0.6087/0.6408 and pressuring pivotal support at 0.6187 (Mar 4 low) with firm break here to generate fresh bearish signal.

Daily studies turned to full bearish configuration and contribute to growing risk of further losses (Australian dollar is on track for the biggest daily drop since 10 Apr 2024).

Broken daily cloud base at 0.6248 (also broken 50% retracement of 0.6087/0.6408) reverted to solid resistance which should cap upticks and keep bears in play.

We look for fresh signals from the US labor data (due later today).

Res: 0.6210; 0.6248; 0.6284; 0.6300.

Sup: 0.6187; 0.6163; 0.6131; 0.6100.

USD/JPY Collapses to a 6-month Low: Safe-Haven Assets in Demand

USD/JPY is at a six-month low near 145.57 on Friday after posting a 2% gain in the previous session.

Key factors driving the USD/JPY movement

US President Donald Trump’s sweeping duties have fuelled demand for safe-haven assets. This week, Trump announced a 10% base tariff on all imports, set to take effect on 5 April. Around 60 countries are expected to face higher duties, including China (54% tariff), the EU (20%), Japan (24%), India (27%) and Vietnam (46%).

The market reacted quickly and powerfully. A new wave of tariff measures signals potentially uncontained inflation and sluggish global GDP growth. At the same time, demand increased across the full spectrum of safe-haven assets, including the yen.

Statistics from Japan showed that personal spending fell less than expected in February, suggesting some resilience in the economy.

The 2025 baseline scenario suggests that the Bank of Japan will raise interest rates this year, although uncertainty surrounding global trade and domestic economic conditions casts a shadow over the outlook.

Technical outlook: USD/JPY

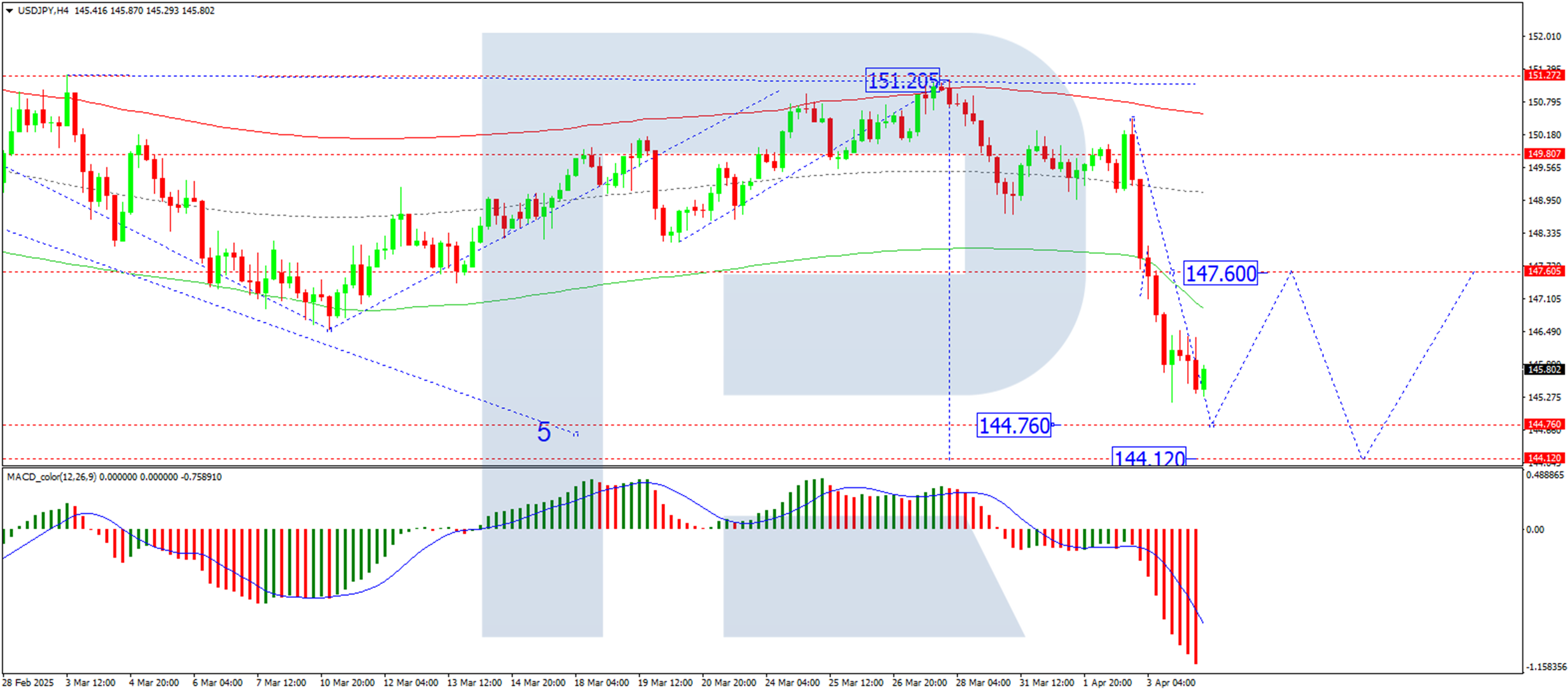

On the H4 chart, the USD/JPY pair has breached the 147.60 level to the downside and continues to form a wave towards the 144.76 level. The target is local. After reaching it, a correction to 147.60 is possible. Once the correction is complete, a further wave down to 144.12 is likely. Technically, this scenario is confirmed by the MACD indicator. Its signal line is below the zero level and is pointing sharply downwards.

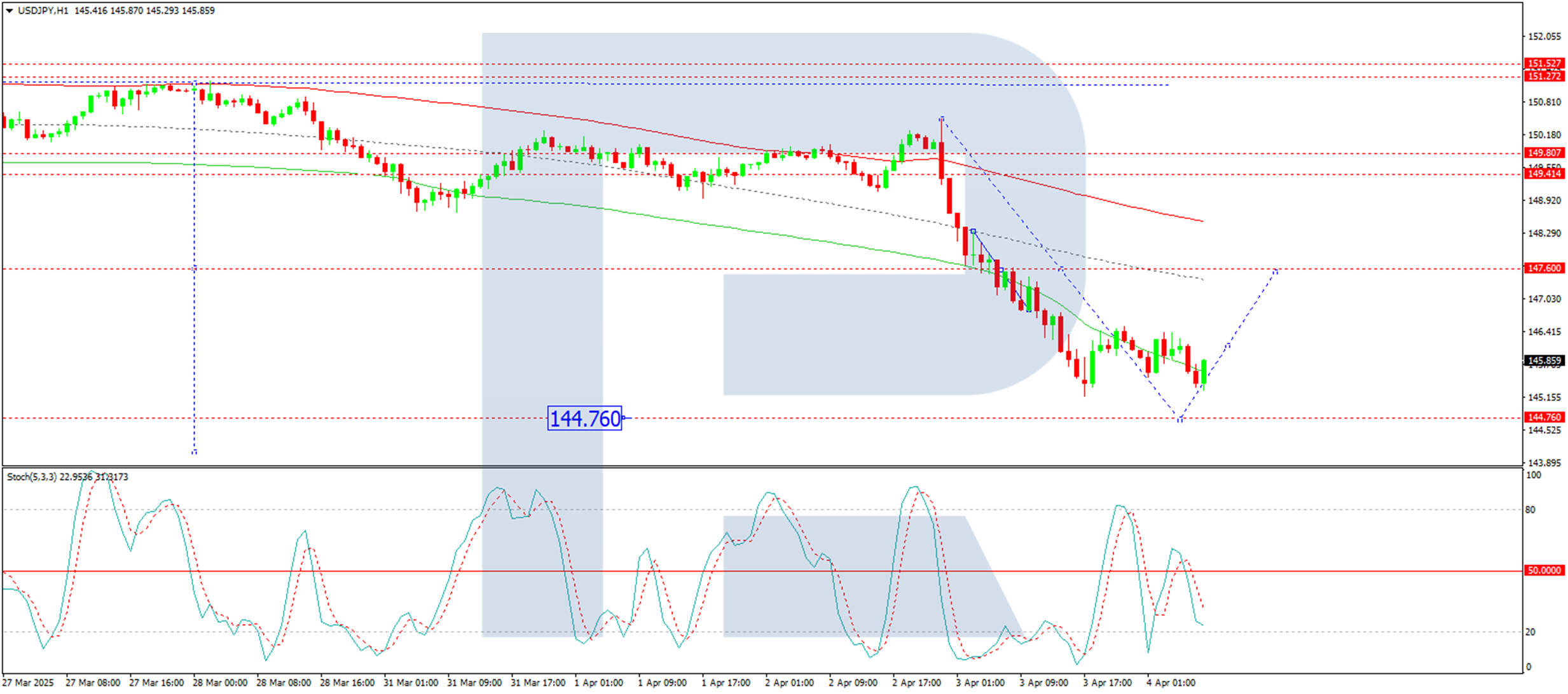

On the H1 chart, USD/JPY has formed a consolidation range around 147.60. Following the downside breakout, the development of the third wave is underway. The target is at 144.76. Once this is reached, a corrective wave is likely. The first correction target is at 146.06. Technically, this scenario is confirmed by the Stochastic oscillator. Its signal line is below 50 and heading directly towards 20.

Conclusion

With trade war fears escalating and demand for safe-haven assets surging, USD/JPY remains under pressure. Technical indicators suggest further downside, though a short-term correction is possible. Traders should monitor 144.76 as the next key support, with BoJ policy signals and global trade developments likely to determine the pair’s next significant move.

Bitcoin (BTCUSD) Elliott Wave : Calling the Decline After 3 Waves Bounce

Hello fellow traders. In this technical article we’re going to look at the Elliott Wave charts of Bitcoin (BTCUSD) published in members area of the website. As our members know, Bitcoin is currently correcting its short-term cycle from the 76,612 low. In the following analysis, we will break down the Elliott Wave forecast and identify the key target area.

BTCUSD Elliott Wave 1 Hour Chart 04.02.2025

The pullback still looks incomplete at the moment. We count five waves down from the peak, suggesting we have only the first leg ((a)) of wave 2 which is unfolding as a Zig Zag pattern. As long as the price remains below 88760 peak , we anticipate another leg down as proposed on the chart.

BTCUSD Elliott Wave 1 Hour Chart 04.04.2025

The price has remained below the 88,760 peak, and the expected decline has followed. BTCUSD has yet to reach the extreme zone. There may be further short-term weakness, with potential support between 80,967 and 79,159. At this stage, we do not recommend selling.

BTC/USD Analysis: Bitcoin Price at a Critical Support Level

In our 28 January report, "Bitcoin Price Holds Above $100k. For Now?", we highlighted the heightened volatility surrounding Trump’s inauguration. We speculated that major market players might have capitalized on this surge to lock in profits from long positions, potentially preparing for a bearish market phase. Since then, Bitcoin's price has dropped by approximately 20%.

BTC/USD Chart Analysis Today

Fresh price data allows for a refined trend channel (marked in blue), capturing several bullish factors for cryptocurrency investors. These include capital inflows into Bitcoin ETFs and Trump’s fulfilled promise to establish a National Cryptocurrency Reserve.

However, Bitcoin is now testing the lower boundary of this critical channel. Notably, bulls have made two attempts to reclaim the uptrend:

→ The first attempt (marked by an arrow) took place on 11 March, but the $88,000 level proved to be strong resistance, pushing Bitcoin’s price back to the lower channel boundary.

→ The second attempt occurred this week but also appears unsuccessful, as the price once again failed to break above $88,000. BTC/USD has now retreated back to the lower boundary of the trend channel.

A long upper wick (marked by an arrow) signals bearish aggression, triggered by news of Trump’s tariffs. This development raises the risk of a bearish breakout from the long-term ascending channel.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*Important: At FXOpen UK, Cryptocurrency trading via CFDs is only available to our Professional clients. They are not available for trading by Retail clients. To find out more information about how this may affect you, please get in touch with our team.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

NFP Preview April 2025: NFP Forecast, Dollar & Dow Jones Analysis (DJIA)

- US Nonfarm Payrolls data for March 2025 is released April 4th, with expected job growth of 135K-140K.

- Market reaction is heavily influenced by recent tariff announcements and expectations of Federal Reserve policy changes.

- Fed Chair Powell's speech following the data release is crucial for market direction and potential rate cuts.

- Technical analysis of Dow Jones shows bullish divergence, while the US Dollar Index (DXY) is oversold.

The US Bureau of Labor Statistics is set to release the non-farm payroll and jobs data for March 2025 on Friday, April 4th, 2025.

Job Market Expectations for February

Analysts are projecting a more subdued pace of job creation this time, with consensus estimates of 135K–140K new jobs added in March, down from February’s tally of 151K. The unemployment rate is anticipated to hold steady at 4.1%, while average hourly earnings are forecast to rise 0.3% month-over-month, maintaining an annual growth rate of 4.0%.

These expectations reflect concerns around economic headwinds, including trade-related uncertainties and inflation pressures stemming from recent global tariff disputes.

Key Estimates for the March Report:

- Nonfarm Payrolls: 135K–140K (consensus)

- Unemployment Rate: 4.1% (unchanged)

- Average Hourly Earnings (MoM): 0.3%

- Labor Force Participation Rate: Consensus data not released, but prior levels stood at 62.4%.

Market reaction and implications of the data

Markets are no doubt still reeling and coming to terms with President Trump's liberation day tariff announcements. The US Dollar and equity markets have both faced significant selloffs with the Magnificent 7 Index now down over -30% from its all time high seen on December 18th.

The S&P 500 is down -7.5% year-to-date with large cap tech beyond bear market territory.

The impact of the tariff announcements also saw the Nasdaq 100 record its largest single-day point loss in HISTORY. The index lost a total of -1060 points and came just 1.5% away from triggering the first circuit breaker since March 2020.

Given the impact tariffs are having on markets and what we have seen in the lead up to the announcement, how important will the NFP and jobs data be?

This is where it gets intriguing to say the least. There is a school of thought that given recent developments the role of the Federal Reserve will be crucial moving forward. The uncertainties created by tariffs and potential slowdown of growth may be offset by Federal Reserve policy and rate cuts.

Another sign of this comes from the behavior of bond markets and the US dollar in the face of the recent selloff. Behavior suggests that markets are hoping the Federal Reserve will step in to provide relief by accelerating rate cuts to help absorb the shock.

After the jobs data today we have a speech by Fed Chair Powell which could prove crucial. If he speaks with more urgency, stock markets might stabilize. If not, more selling is likely. Either way, it seems rate cuts will happen sooner, leading to lower yields, higher bond prices, and a weaker dollar.

With that in mind, the NFP release today takes on a new dimension altogether.

Potential impact on the us dollar index (DXY), S&P 500 and Dow Jones (DJIA)

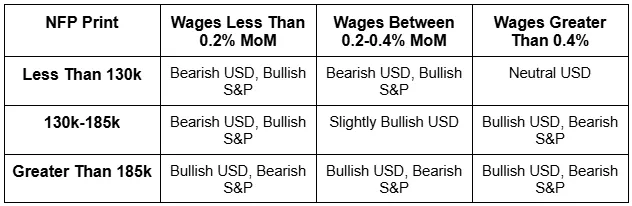

Here’s how the market might respond to different outcomes in March’s job numbers:

Potential Impact on the US Dollar, US Indices Based on the Data Released

Source: LSEG, TradingEconomics. Table Created by Zain Vawda

The US Dollar Index (DXY) is heavily oversold while indexes like the S&P and Dow Jones are also nearing similar territory. Given the strong bearish momentum caused by the tariff announcement, it's hard to see them bouncing back unless the upcoming NFP report significantly beats expectations.

Will that help alleviate growth fears and help the stock market as well or just the US Dollar? This and many questions will be what market participants grapple with heading into today's data releases.

I think we could get more clarity from Fed Chair Powell's remarks rather than the actual data print and this is where I will be keeping a close watch.

Technical Analysis - Dow Jones (DJIA)

Looking at the Dow Jones which is hovering just above oversold territory having printed fresh YTD lows yesterday.

The index has one silver lining in the face of the current market dynamics in that the technical picture does offer a sliver of hope.

There is bullish divergence in play on the Dow Jones daily chart as price makes lower lows, but the RSI makes higher lows. This can signal that the downward momentum is weakening, and a price reversal to the upside might be coming.

There is also the psychological 40000 level just hovering below the current price level. If this level is broken then the 39588 handle may provide support.

A recovery from here however may face resistance at 40537, 40738,41095 and 41400.

Of course, the countless dynamics at play and current sentiment remains tilted to further downside. Whether the NFP can arrest this slump remains to be seen.

US Dollar Index (DXY) Daily Chart, April 4, 2025

Source: TradingView (click to enlarge)

Support

- 40231

- 40000

- 39588

Resistance

- 40537

- 41095

- 41400