Sample Category Title

Markets Weekly Outlook – FOMC Minutes, Tariff Developments and Inflation Ahead

- US equity markets tumbled due to President Trump's tariff proposals, raising global growth concerns.

- Federal Reserve Chair Jerome Powell acknowledged tariffs' impact, emphasizing monitoring inflation and waiting for more data.

- The upcoming week focuses on further tariff developments, US jobs data, and central bank decisions in Australia and New Zealand.

- Technical analysis shows that the Nasdaq 100 has now entered a bear market, down 20% from all-time highs.

Week in review: Liberation day tariffs send markets tumbling

A bloodbath week for US Equity markets and markets as a whole has finally come to an end. Market sentiment soured after President Trump revealed his tariff proposals which weighed on global growth expectations and sent US stocks tumbling.

On Thursday, hedge funds sold stocks at their highest single-day amount since 2010. At the same time, retail investors bought $4.7 billion worth of stocks, the most in over a decade. Friday, the S&P 500 lost another $1.5 trillion in market value, bringing the total two-day losses to $3.5 trillion.

Friday's losses came about as China announced it will retaliate against U.S. President Donald Trump by imposing an extra 34% tariff on U.S. goods. This move intensifies the trade war, worrying investors and raising fears of a possible recession.

Source: LSEG, US Census Bureau

Developments this week saw investment bank J.P. Morgan increase their estimates to 60% that the global economy would enter a recession by year-end, up from 40% previously.

Big tech stocks dropped, pushing the Nasdaq closer to a bear market. Companies that rely heavily on China and Taiwan for manufacturing were hit hard, with Apple falling 6.4% and Nvidia dropping 7.7%.

The Nasdaq was set to close more than 20% below its record high from December.

It appears that market participants are now looking to the Federal Reserve and Chair Jerome Powell to be the saviour.

Federal Reserve Chair Jerome Powell told a business journalists' conference on Friday that the tariffs were "bigger than expected" and increased the risk of higher inflation and slower economic growth.

The Fed plans to wait for more data before deciding on monetary policy but will focus on keeping inflation under control if Trump's tariffs lead to lasting price increases, Powell said.

He didn’t directly comment on the U.S. stock market selloff but admitted that uncertainty is causing businesses to delay decisions.

"People are just waiting for clarity," Powell said. "I can't say when it will clear up, but it eventually will."

On the FX front, The U.S. dollar strengthened against major currencies like the euro and yen on Friday after Federal Reserve Chairman Jerome Powell discussed the impact of bigger-than-expected U.S. tariffs and took a cautious approach to future rate cuts.

The Aussie Dollar lost ground on Friday and hit five-year lows against the greenback after China announced its tariff stance and retaliation. The Swiss Franc and the Japanese Yen both benefitted this week from safe haven appeal, both gaining significant ground across the board.

Commodities were interesting to observe this week. Gold prices rose immediately after the tariff announcement but experienced a significant selloff since then. Gold reached a high of 3167 before the selloff saw prices touch a low of 3015 on Friday. The only explanation that I could draw was significant profit taking and the possibility that the tariffs were largely priced in.

Oil prices struggled this week as OPEC + announced further output increases. That coupled with tariff fears sent Oil prices to their lowest level since 2021. Friday's losses were around 8%. For more information on the OPEC + developments read Brent Oil price plummets: OPEC+ output hike & price outlook

Heading into next week and the tariff picture is far from clear. Market participants will do well to focus on potential deals between the US and other countries which could help sentiment improve. However, if no deals materialize and countries follow the China approach markets could be in for another week of pain.

The week ahead: Markets eye tariff developments and the FOMC minutes

The upcoming week will focus on U.S. President Donald Trump's plans for new tariffs. Alongside this, markets will also watch U.S. jobs data, an Australian central bank meeting, and a key eurozone inflation report.

Asia Pacific Markets

The main focus this week in the Asia Pacific region will be Chinese inflation and Japanese wage data as the BoJ eyes a rate hike in the coming months.

Next week, China's low inflation could give the central bank (PBoC) room to cut interest rates. March inflation data, due Thursday, is expected to show consumer prices staying weak, with a slight rise of just 0.1% year-on-year.

Meanwhile, producer prices are likely to remain negative for the 30th straight month as input costs keep falling. These deflationary pressures and high real interest rates could push the PBoC to lower rates, though it has held off so far, waiting for the right moment.

The Bank of Japan will be watching wage data this week as the central bank eyes another rate hike. Wages are expected to improve gradually. February saw stronger labor cash earnings, helped by solid bonus payouts. However, real cash earnings are likely to keep shrinking as inflation peaked in the same month. Inflation eased in March due to energy subsidies and lower fresh food prices, supporting the outlook for a steady rise in wages over time.

The Reserve Bank of New Zealand will announce its interest rate decision on Wednesday next week. Market participants are expecting the central bank to cut rates by 25 bps. Given the tariff developments and the backdrop of the New Zealand economy a 25 bps cut seems all but certain at this point.

Europe + UK + US

In developed markets, the US is the major data player next week with the Euro Zone and the UK enjoying a data reprieve.

The US economy is facing growing challenges as President Trump’s new trade policies spark concerns about higher prices and slower economic growth. Steep tariffs, which are paid by importing companies, could hurt profit margins and reduce consumer spending, especially as worries about job losses grow and stock markets decline. While markets are increasingly expecting the Federal Reserve to cut interest rates, another high core CPI and PPI reading next week might make the Fed cautious about acting soon.

I will also be watching consumer confidence, which could drop further after recent events, and monitoring whether government spending cuts tied to DOGE are improving the fiscal situation.

The UK does not have any high impact data releases but I will be keeping a close watch on Friday's GDP data print. After a slow January, I expect a small rebound in February's monthly GDP. These figures can be quite volatile, but despite a quieter end to 2024, the outlook for 2025 still seems positive, even with the recent tariff news.

There are still of course challenges as evidenced by the Goldman Sachs group which lowered its UK GDP forecast down to 0.7% from a previous 0.8%.

The UK government is significantly increasing spending this year, which should help support growth. However, weaker economic activity in the US and eurozone could become a big challenge later this year and into 2026.

Chart of the week - Nasdaq 100

This week's focus shifts to the Nasdaq 100 which has now dropped over 20% from its all-time highs signaling a bear market.

The nasdaq is currently resting at an area of support around 17304 and finished the week with 3 successive days of losses.

The period-14 RSI is now resting in oversold territory but as we know the RSI can remain in oversold territory for extended periods of time which means the bearish move may not be over.

This will also depend on how tariff developments shake up next week.

Immediate support rests at 17000 before the 16500 and 16000 handle comes into focus.

Resistance rests at around 17737 before the 18361 and 18852 handles come into focus.

Nasdaq 100 Daily Chart - April 4, 2025

Source: TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 17000

- 16500

- 16000

Resistance

- 17737

- 18361

- 18852

The Weekly Bottom Line: A Return to Turbulent Times

Canadian Highlights

- Canada initially appeared to have dodged tariffs on Trump’s Liberation day. But still facing three separate tariff actions, Canada’s effective tariff rate is close to 10%.

- Canada’s job market is already starting to show some softness, with net job losses and a higher unemployment rate in March.

- The jobs data has shifted market expectations towards an interest rate cut in April. We think further support is needed for Canada’s economy.

U.S. Highlights

- The U.S. announced sweeping ‘reciprocal’ tariffs due to go into effect over the next week, with all countries exporting to the U.S. soon to be subject to double digit surcharges.

- The employment report for March showed 228k new jobs added, illustrating robust health in the labor market prior to the recent volatility.

- Federal Reserve officials, including Chair Powell, noted that recent tariffs would add upside risks to inflation.

Canada – Trump’s Tariffs Sideswipe Markets

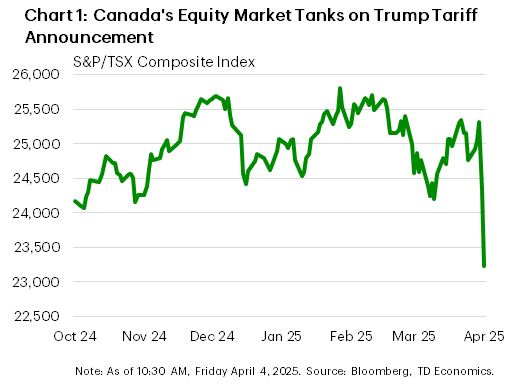

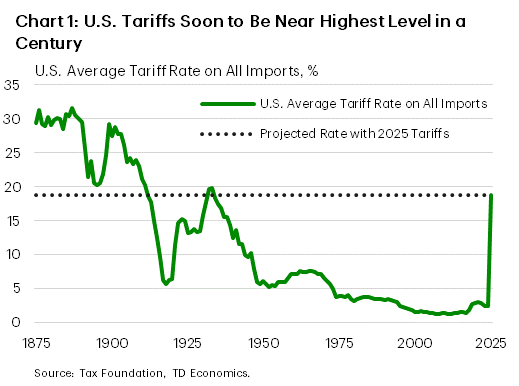

President Trump’s dreaded “Liberation Day”, saw the President make good on his campaign promise for a 10% universal tariff. Some countries received higher levies based on a bizarre calculation of trade “barriers” based on the size of the goods trade deficit with the U.S., with rates as high as 46% for Vietnam and 20% for the EU. Investor sentiment soured quickly; with many forecasters predicting the levies would tip the U.S. economy into recession. Global equity markets saw their largest one-day drops since 2020 on Thursday, with Toronto’s S&P TSX index dropping 3.8% (Chart 1). We don’t view this as an overreaction. We were not alone in pointing out that the market’s initial euphoria over Trump’s election win seemed to be favouring the economic positives of tax cuts and deregulation, rather than the disruption of upending 80 years of U.S. trade policy.

For Canada, there was some initial relief that we were not hit with any reciprocal tariff (see commentary). But zooming out, Canada already faces an effective tariff rate around 10%, depending on the degree of USMCA compliance among goods exports. Canada faces three separate 25% import tariffs: the 25% “fentanyl/illegal immigration” tariff, with 10% on energy and potash with a carve out for goods that are USMCA compliant, the 25% steel and aluminum tariff and a 25% tariff on finished vehicle imports. Fortunately, it is estimated that 80-90% of exports can become USMCA compliant, which would take down the effective tariff rate to roughly 4-5%. That is still double the 2% rate pre-Trump.

The current projected rate is only slightly lower than the 12.5% we assumed in our recent Quarterly Economic Forecast. If those tariffs remain in place for six months, Canada’s economy slips into a shallow recession.

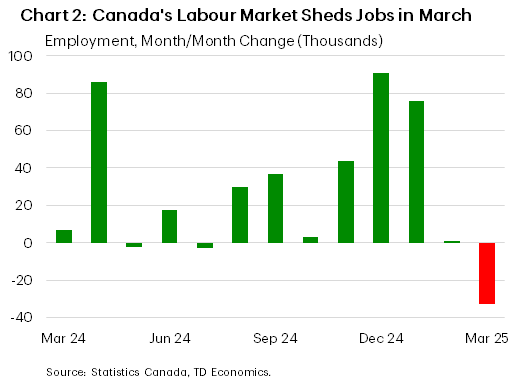

Canada’s job data for March reinforced a softer economic message. The labour market shed positions for the first time in more than three years (Chart 2), taking the unemployment rate higher by one tenth to 6.7%. There weren’t many silver linings in the report either. Job losses were in full-time positions in the private sector, and across most demographic groups. The share of people unemployed long-term also rose, and wage pressures eased. The job market may not be flashing red warning signs yet, but it is certainly yellow, and has softened significantly relative to the early post-pandemic period.

Looking at trends by sector, the losses in March were largest in the services sector, led by wholesale and retail trade (-29k; -1.0%), and information, culture and recreation (-20k; -2.4%). Although manufacturing (-7k; -0.4%) and construction (-4k; -0.2%) also saw job losses. Given the layoffs already announced in the auto sector this week, more are likely to come.

The Bank of Canada’s next interest rate announcement is on April 16th, and decision makers will still get to digest the BoC’s Business Outlook Survey and the March inflation report before then. Market odds of a rate cut increased sharply in the wake of the jobs data, to becoming the consensus view. We have argued that the Bank should cut rates further to support Canada’s economy in the face of the tariff threat, despite the risk of slightly higher inflation in the short run.

U.S. – A Return to Turbulent Times

We kicked off the second quarter this week with what has likely been the most anticipated day of the year so far. On it’s so-named ‘Day of Liberation’, the administration announced broad-based tariffs set to go into effect over the coming week. Equity markets and U.S. Treasury yields fell sharply over the following days on concerns over the economic impact of the policies. As of the time of writing, the S&P 500 is down 7.4% on the week, while the U.S. Treasury 10-year yield fell 33 basis-points (bps) to 3.93%.

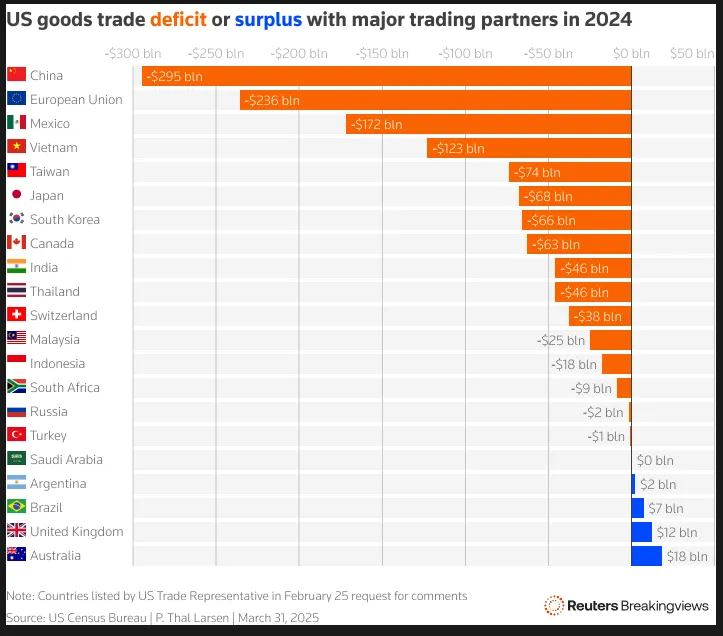

The tariffs announced by President Trump this week included a baseline 10% tariff on nearly every country that the U.S. trades with, scheduled to go into effect on April 5th, with varied upward revisions subsequently applied to 60 countries on April 9th. The latest tariffs will bring the effective tariff rate charged by the U.S. to its highest level in nearly a century (Chart 1). The countries likely to be the most impacted include China (which now faces a total stacked tariff rate of over 54%), the European Union (20%), and Vietnam (46%), although the effects, like the policy, are expected to be widespread. China has already announced that it will retaliate in equal force while the EU is preparing countermeasures. Some hope remains that negotiations can lead to the removal or some reduction of the tariffs before their full impact is felt, but for the time being it appears that we are witnessing the start of a trade war unlike any seen in generations.

Even before the most recent tariffs were announced, we were already starting to see some softening in the economic data. The ISM manufacturing and services purchasing manager indexes for March both showed a slowdown in demand and hiring activity, with business sentiment weakening on trade uncertainty. However, we have also seen consumers and businesses attempt to front-load purchases in advance of tariffs, with March vehicle sales hitting a four-year high and imports remaining more than 20% above year-ago levels through February.

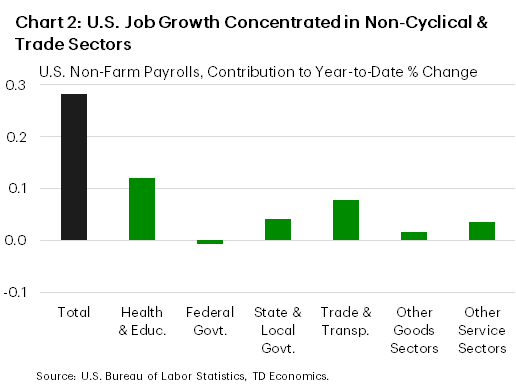

This behavior helped to keep the labor market healthy on aggregate in March, as 228k new jobs were added. Non-cyclical sectors, like health and education, as well as trade-exposed sectors contributed the lion’s share of the employment gains (Chart 2). While this was undoubtedly a solid report on the health of the labor market, we are likely to see some slowing in hiring over the coming months as trade policy uncertainty further weighs on business and consumer sentiment and tariffs begin to influence economic activity.

The next Federal Reserve meeting is still roughly a month away, but the views of Fed officials have likely become more consequential amid elevated uncertainty. During a presentation on Friday, Chair Powell noted that while the impact of tariffs remains uncertain, tariffs were likely to weigh on growth and raise inflation. As of the time of writing, markets are pricing in an 80% chance for 100bps in rate cuts by year-end. Next week’s CPI data release and the March FOMC meeting minutes will be parsed closely for further hints of the future direction of monetary policy as the administration’s ‘reciprocal’ tariffs are scheduled to come into effect. Assuming no changes occur between now and then, we will be entering a structurally different reality for global trade and finance.

Focus on Inflation Trends in Canadian Business Survey and U.S. CPI

Data in the coming week will be watched closely for impact from trade headwinds to prices in Canada and the U.S., following recent tariff announcements and progressively softening sentiment data.

It is still likely too early to see significant increases in final U.S. consumer prices from tariffs. We anticipate a slower 0.2% month-over-month rise in both headline and core consumer price index measures in March. This will nudge both annual core and headline inflation down to 3% and 2.7%, respectively. Core goods inflation is likely to hold steady, still underperforming services sector inflation—at least for another month.

But there are already signs that tariffs have begun to push up costs earlier in the production cycle. The latest ISM manufacturing survey suggested the share of U.S. firms facing higher prices rose drastically in March. “Dramatic increases” were noted especially for steel and aluminum products thanks to related tariffs. We expect goods inflation in the U.S. may heat up in the months ahead.

In Canada, focus will be on the Q1 Bank of Canada Business Outlook Survey (BOS) conducted during February. The survey asked key questions on business sales outlook, capacity constraints, investment and hiring intentions as well inflation expectations amid escalating trade tensions.

Indeed, the Q2 results will likely be a stark contrast to the last iteration in Q4 when business sentiment was buoyed by large and consecutive interest rate cuts from the BoC and early signs of a recovery in domestic demand toward the end of last year. We expect the near-term outlook dimmed while businesses scaled back hiring and investment plans, especially for those in the trade-exposed manufacturing industries.

Businesses’ expectations for input cost and inflation pressures likely both rose, mirroring the early survey released alongside the last BoC interest rate announcement that showed plans among businesses to pass on a large chunk of tariff related cost increases to consumers.

Moving forward, the BoC and U.S. Federal Reserve will be watching trends on inflation, expectations and business pricing behaviour (expected frequency and size of future price adjustments) very closely to ensure tariff-related price increases do not turn into continuing high inflation.

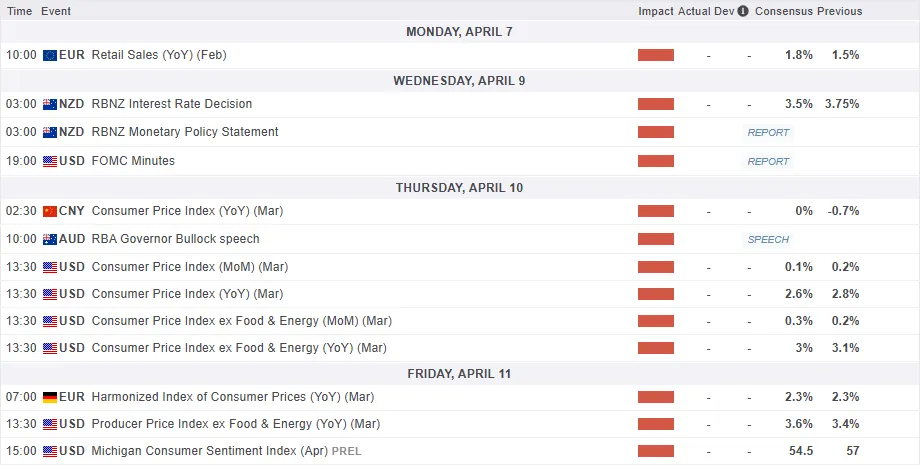

Summary 4/7 – 4/11

Monday, Apr 7, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Feb | 3.10% | 2.80% |

| 05:00 | JPY | Leading Economic Index Feb P | 107.8 | 108.3 |

| 06:00 | EUR | Germany Industrial Production M/M Feb | -0.90% | 2.00% |

| 06:00 | EUR | Germany Trade Balance (EUR) Feb | 17.8B | 16.0B |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Mar | 735B | |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Apr | -8.7 | -2.9 |

| 09:00 | EUR | Eurozone Retail Sales M/M Feb | 0.50% | -0.30% |

| 14:30 | CAD | BoC Business Outlook Survey | ||

| 22:00 | NZD | NZIER Business Confidence Q1 | ||

| 23:50 | JPY | Current Account (JPY) Feb | 2.74T | 1.94T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Feb | |

| Forecast: 3.10% | Previous: 2.80% | ||

| 05:00 | JPY | Leading Economic Index Feb P | |

| Forecast: 107.8 | Previous: 108.3 | ||

| 06:00 | EUR | Germany Industrial Production M/M Feb | |

| Forecast: -0.90% | Previous: 2.00% | ||

| 06:00 | EUR | Germany Trade Balance (EUR) Feb | |

| Forecast: 17.8B | Previous: 16.0B | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Mar | |

| Forecast: | Previous: 735B | ||

| 08:30 | EUR | Eurozone Sentix Investor Confidence Apr | |

| Forecast: -8.7 | Previous: -2.9 | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Feb | |

| Forecast: 0.50% | Previous: -0.30% | ||

| 14:30 | CAD | BoC Business Outlook Survey | |

| Forecast: | Previous: | ||

| 22:00 | NZD | NZIER Business Confidence Q1 | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Current Account (JPY) Feb | |

| Forecast: 2.74T | Previous: 1.94T | ||

Tuesday, Apr 8, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | NAB Business Confidence Mar | -1 | |

| 01:30 | AUD | NAB Business Conditions Mar | 4 | |

| 05:00 | JPY | Eco Watchers Survey: Current Mar | 45.3 | 45.6 |

| 06:45 | EUR | France Trade Balance (EUR) Feb | -6.2B | -6.5B |

| 10:00 | USD | NFIB Business Optimism Index Mar | 101.3 | 100.7 |

| 14:00 | CAD | Ivey PMI Mar | 53.2 | 55.3 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | NAB Business Confidence Mar | |

| Forecast: | Previous: -1 | ||

| 01:30 | AUD | NAB Business Conditions Mar | |

| Forecast: | Previous: 4 | ||

| 05:00 | JPY | Eco Watchers Survey: Current Mar | |

| Forecast: 45.3 | Previous: 45.6 | ||

| 06:45 | EUR | France Trade Balance (EUR) Feb | |

| Forecast: -6.2B | Previous: -6.5B | ||

| 10:00 | USD | NFIB Business Optimism Index Mar | |

| Forecast: 101.3 | Previous: 100.7 | ||

| 14:00 | CAD | Ivey PMI Mar | |

| Forecast: 53.2 | Previous: 55.3 | ||

Wednesday, Apr 9, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 02:00 | NZD | RBNZ Interest Rate Decision | 3.50% | 3.75% |

| 05:00 | JPY | Consumer Confidence Index Mar | 34.9 | 35 |

| 06:00 | JPY | Machine Tool Orders Y/Y Mar P | 3.50% | |

| 14:00 | USD | Wholesale Inventories Feb F | 0.30% | 0.30% |

| 14:30 | USD | Crude Oil Inventories | 6.2M | |

| 18:00 | USD | FOMC Minutes | ||

| 23:01 | GBP | RICS Housing Price Balance Mar | 8% | 11% |

| 23:50 | JPY | Bank Lending Y/Y Mar | 3.10% | 3.10% |

| 23:50 | JPY | PPI Y/Y Mar | 3.90% | 4.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 02:00 | NZD | RBNZ Interest Rate Decision | |

| Forecast: 3.50% | Previous: 3.75% | ||

| 05:00 | JPY | Consumer Confidence Index Mar | |

| Forecast: 34.9 | Previous: 35 | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Mar P | |

| Forecast: | Previous: 3.50% | ||

| 14:00 | USD | Wholesale Inventories Feb F | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 6.2M | ||

| 18:00 | USD | FOMC Minutes | |

| Forecast: | Previous: | ||

| 23:01 | GBP | RICS Housing Price Balance Mar | |

| Forecast: 8% | Previous: 11% | ||

| 23:50 | JPY | Bank Lending Y/Y Mar | |

| Forecast: 3.10% | Previous: 3.10% | ||

| 23:50 | JPY | PPI Y/Y Mar | |

| Forecast: 3.90% | Previous: 4.00% | ||

Thursday, Apr 10, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | CNY | CPI M/M Mar | -0.20% | |

| 01:30 | CNY | CPI Y/Y Mar | 0.10% | -0.70% |

| 01:30 | CNY | PPI Y/Y Mar | -2.30% | -2.20% |

| 12:30 | CAD | Building Permits M/M Feb | -0.90% | -3.20% |

| 12:30 | USD | Initial Jobless Claims (Apr 4) | 222K | 219K |

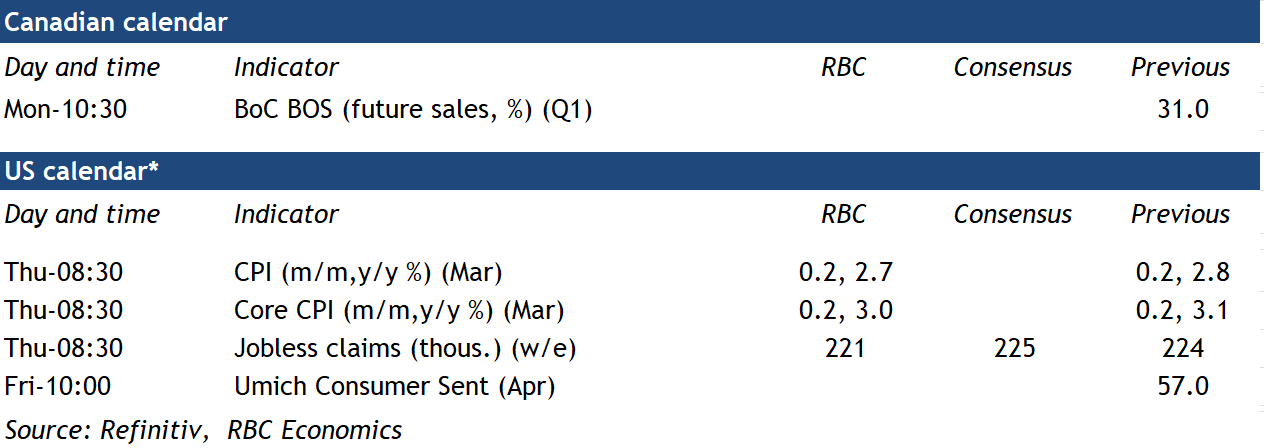

| 12:30 | USD | CPI M/M Mar | 0.20% | 0.20% |

| 12:30 | USD | CPI Y/Y Mar | 2.60% | 2.80% |

| 12:30 | USD | CPI Core M/M Mar | 0.30% | 0.20% |

| 12:30 | USD | CPI Core Y/Y Mar | 3.10% | |

| 14:30 | USD | Natural Gas Storage | 29B | |

| 22:30 | NZD | Business NZ PMI Mar | 53.9 | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Mar | 1.20% | 1.20% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | CNY | CPI M/M Mar | |

| Forecast: | Previous: -0.20% | ||

| 01:30 | CNY | CPI Y/Y Mar | |

| Forecast: 0.10% | Previous: -0.70% | ||

| 01:30 | CNY | PPI Y/Y Mar | |

| Forecast: -2.30% | Previous: -2.20% | ||

| 12:30 | CAD | Building Permits M/M Feb | |

| Forecast: -0.90% | Previous: -3.20% | ||

| 12:30 | USD | Initial Jobless Claims (Apr 4) | |

| Forecast: 222K | Previous: 219K | ||

| 12:30 | USD | CPI M/M Mar | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 12:30 | USD | CPI Y/Y Mar | |

| Forecast: 2.60% | Previous: 2.80% | ||

| 12:30 | USD | CPI Core M/M Mar | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 12:30 | USD | CPI Core Y/Y Mar | |

| Forecast: | Previous: 3.10% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 29B | ||

| 22:30 | NZD | Business NZ PMI Mar | |

| Forecast: | Previous: 53.9 | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Mar | |

| Forecast: 1.20% | Previous: 1.20% | ||

Friday, Apr 11, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | EUR | Germany CPI M/M Mar F | 0.30% | 0.30% |

| 06:00 | EUR | Germany CPI Y/Y Mar F | 2.20% | 2.20% |

| 06:00 | GBP | GDP M/M Feb | 0.10% | -0.10% |

| 06:00 | GBP | Industrial Production M/M Feb | 0.10% | -0.90% |

| 06:00 | GBP | Industrial Production Y/Y Feb | -1.50% | |

| 06:00 | GBP | Manufacturing Production M/M Feb | 0.20% | -1.10% |

| 06:00 | GBP | Manufacturing Production Y/Y Feb | -1.50% | |

| 06:00 | GBP | Index of Services 3M/3M Feb | 0.50% | 0.40% |

| 06:00 | GBP | Goods Trade Balance (GBP) Feb | -17.9B | -17.8B |

| 12:30 | USD | PPI M/M Mar | 0.20% | 0.00% |

| 12:30 | USD | PPI Y/Y Mar | 3.20% | |

| 12:30 | USD | PPI Core M/M Mar | 0.30% | -0.10% |

| 12:30 | USD | PPI Core Y/Y Mar | 3.40% | |

| 14:00 | USD | UoM Consumer Sentiment Apr P | 55 | 57 |

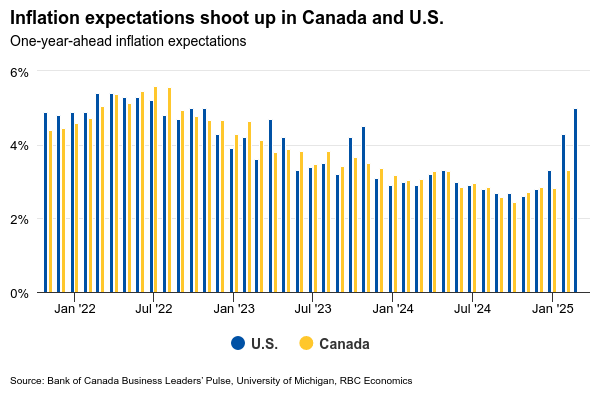

| 14:00 | USD | UoM Inflation Expectations Apr P | 5.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | EUR | Germany CPI M/M Mar F | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 06:00 | EUR | Germany CPI Y/Y Mar F | |

| Forecast: 2.20% | Previous: 2.20% | ||

| 06:00 | GBP | GDP M/M Feb | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 06:00 | GBP | Industrial Production M/M Feb | |

| Forecast: 0.10% | Previous: -0.90% | ||

| 06:00 | GBP | Industrial Production Y/Y Feb | |

| Forecast: | Previous: -1.50% | ||

| 06:00 | GBP | Manufacturing Production M/M Feb | |

| Forecast: 0.20% | Previous: -1.10% | ||

| 06:00 | GBP | Manufacturing Production Y/Y Feb | |

| Forecast: | Previous: -1.50% | ||

| 06:00 | GBP | Index of Services 3M/3M Feb | |

| Forecast: 0.50% | Previous: 0.40% | ||

| 06:00 | GBP | Goods Trade Balance (GBP) Feb | |

| Forecast: -17.9B | Previous: -17.8B | ||

| 12:30 | USD | PPI M/M Mar | |

| Forecast: 0.20% | Previous: 0.00% | ||

| 12:30 | USD | PPI Y/Y Mar | |

| Forecast: | Previous: 3.20% | ||

| 12:30 | USD | PPI Core M/M Mar | |

| Forecast: 0.30% | Previous: -0.10% | ||

| 12:30 | USD | PPI Core Y/Y Mar | |

| Forecast: | Previous: 3.40% | ||

| 14:00 | USD | UoM Consumer Sentiment Apr P | |

| Forecast: 55 | Previous: 57 | ||

| 14:00 | USD | UoM Inflation Expectations Apr P | |

| Forecast: | Previous: 5.00% | ||

Weekly Economic & Financial Commentary: A User’s Guide to Reciprocal Tariffs

Summary

United States: Liberation Day

- The echoes of reciprocal tariffs are reverberating through markets, raising expectations for Fed cuts and driving down yields. Tariff anticipation also drove an expansive U.S. trade deficit in February and increased price pressures in the manufacturing and services sector. Although risks to the outlook are elevated, the labor market remains solid at present, adding 228K jobs on net in March.

- Next week: NFIB (Tue.), CPI (Thu.), Consumer Sentiment (Fri.)

International: Meanwhile Everywhere Else...

- While new U.S. tariffs were the primary talk of the town in recent days, we also got a read on economic sentiment and monetary policy in several foreign economies. Sentiment data from China and Japan were somewhat encouraging, while the Reserve Bank of Australia and Colombia's central bank, BanRep, both opted to hold rates steady. Eurozone inflation data were generally favorable.

- Next week: Mexico CPI (Wed.), Reserve Bank of India Policy Rate (Thu.), Norway CPI (Thu.)

Credit Market Insights: The Widening Gyre

- Corporate bond spreads widened substantially Thursday in a repricing of recession risk following President Trump's tariff announcements. Spreads on investment grade corporate bonds widened by 8 bps to 102 bps and spreads for riskier high yield bonds increased more than 50 bps to 387 bps. The widening in the spreads was the worst one-day move for investment grade bonds since the bank failures in March 2023, and the worst one-day move for high yield bonds since the onset of the pandemic in the spring of 2020.

Topic of the Week: A User's Guide to Reciprocal Tariffs

- The Trump administration announced sweeping new tariffs on many U.S. trading partners this week. The administration utilized a formula primarily based on each nation's trade balance to derive the new tariff rates. By our estimates, the overall U.S. effective tariff rate now stands at 23%, the highest in many decades.

Week Ahead – US CPI and RBNZ Decision on Tap Amidst Tariff Mayhem

- Dollar traders await US CPI data amid global trade turbulence.

- RBNZ to cut by 25bps, could maintain dovish stance.

- China’s CPI and PPI to reveal tariff impact on inflation.

- Strong UK GDP data could help the pound climb higher.

Trump’s “Liberation Day” increases recession fears

The dollar suffered against all its major peers this week, while equites extended their bloodbath after US President Donald Trump announced more aggressive-than-anticipated tariffs on US trading partners.

Trump stated that his administration will proceed with a 10% baseline tariff on all imports to the US, while higher duties will be imposed on some of the nation’s biggest trading partners. For example, China was hit with a new 34% levy on top of the already imposed 20%, while closer allies like Japan and the UK were not exempted, with the former facing a 24% tariff rate and the latter the baseline 10%. The European Union will be subject to a 20% rate. The base 10% tariffs will go into effect on April 5 and the higher reciprocal rates on April 9, and both China and the EU were quick to respond that if those tariffs take effect, they will retaliate.

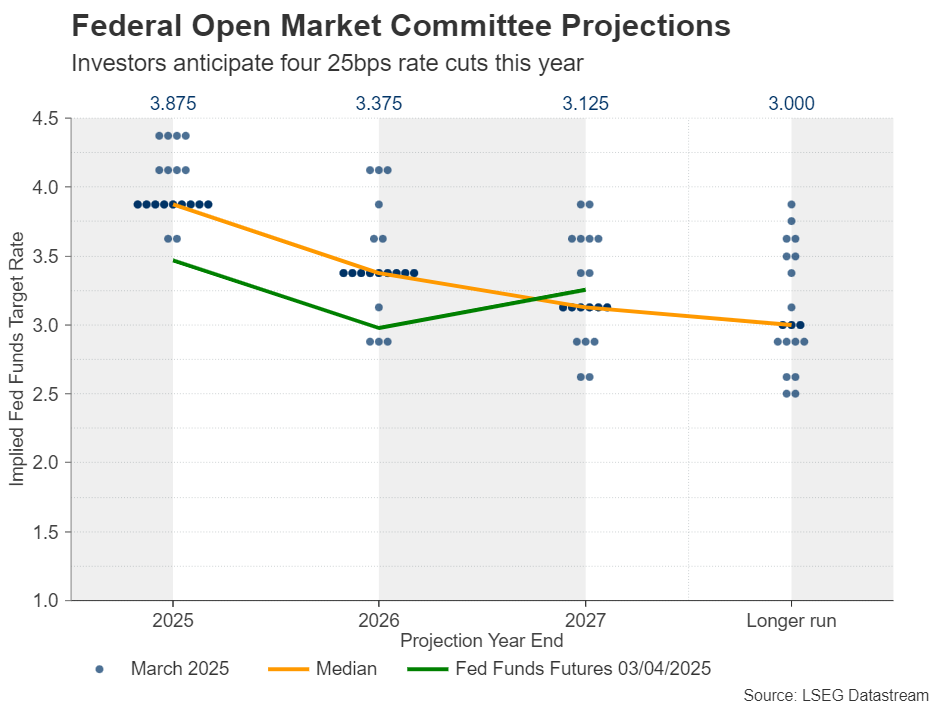

With the Atlanta Fed GDPNow model already pointing to a severe 3.7% contraction of the US economy, investors have become even more fearful about a potential recession this year, which is also evident by the fact that they have ramped up their Fed rate cut bets, despite the central bank sticking to its prior projection of 50bps worth of reductions for this year. Currently, investors are pricing in nearly 100bps worth of cuts by December, which translates into four quarter-point cuts.

Will sticky inflation complicate the Fed’s job

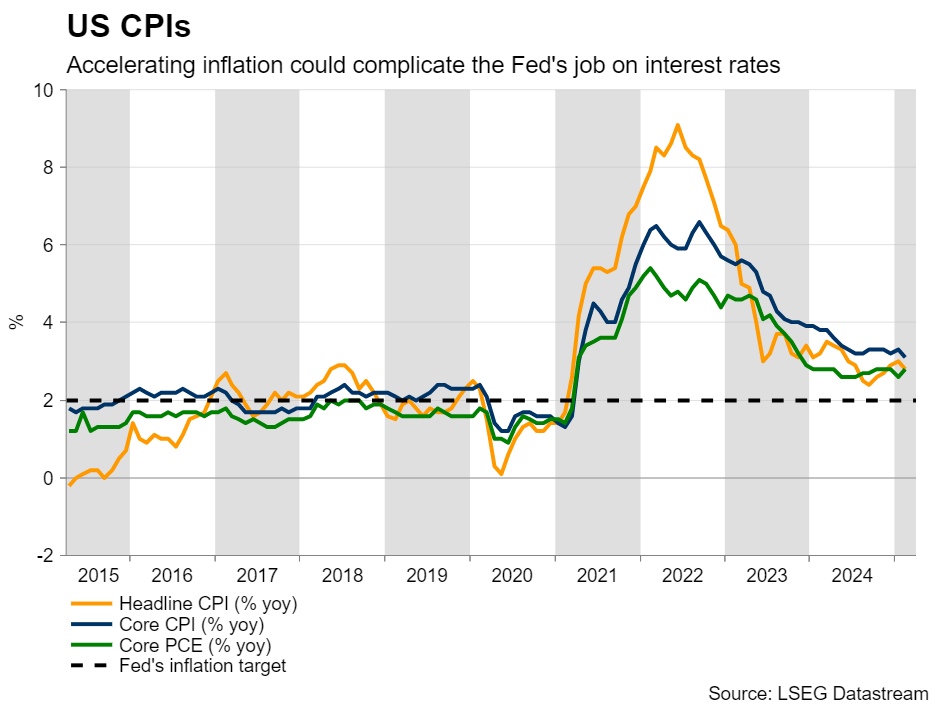

With all that in mind, dollar traders will fix their attention on the US CPI data for March, due out on Thursday. Tariffs are not only posing a threat to economic activity but also presenting an upside risk to inflation. Inflation in the US has been proving more persistent than expected, even before tariffs on steel and aluminium were incorporated into the calculation, with the core PCE index for February rising to 2.8% y/y.

This further complicates the Fed’s work as it may find itself between a rock and a hard place – trying to safeguard economic activity on the one hand and prevent inflation from spiralling out of control on the other. With the prices subindex of the ISM manufacturing PMI for March climbing to 69.4 from 62.4, the risks of the CPIs appear skewed to the upside.

Further acceleration may prompt traders to scale back some of their rate cut bets, and the dollar may stage a modest rebound alongside US Treasury yields. However, higher borrowing costs for longer could risk an even deeper recession down the line. Thus, with recession fears still elevated, any recovery in the US dollar could prove both limited and short-lived.

The minutes from the March 18-19 FOMC decision will be published on Wednesday, the PPI numbers for March on Thursday, and the preliminary University of Michigan (UoM) consumer sentiment index for April on Friday. Given that the latest Fed meeting took place before the April 2 tariff announcements – and bearing in mind that new economic projections, including a new dot plot, were released – the minutes may not draw significant market attention. Investors may instead focus more on additional signs of where inflation may be headed. Thus, beyond the CPI numbers, the PPI data and the UoM inflation expectations could also act as key market movers.

RBNZ set to cut rates, focus to fall on guidance

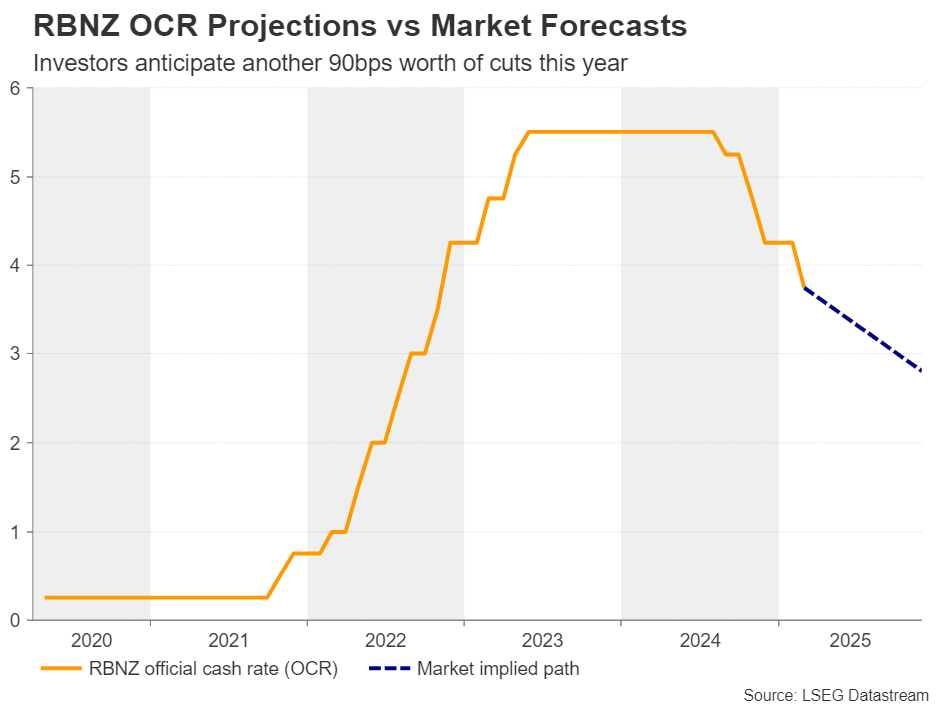

There is also a central bank deciding on monetary policy next week and that’s the Reserve Bank of New Zealand (RBNZ). At its latest gathering on February 19, this central bank lowered its benchmark interest rate by 50bps, signalling the likelihood of more reductions in the coming months and projecting that rates will be around 3% by year-end – 75bps below the current level of 3.75%. Officials also cited global uncertainties and domestic economic risks relating to US President Trump’s trade policies.

Since then, the only noteworthy economic data released from New Zealand have been the retail sales and GDP prints for Q4, both of which exceeded expectations. Yet, investors believe that the Bank should implement an additional 90bps in rate cuts before the end of the year.

With China, New Zealand’s main trading partner, being Trump’s primary focus when it comes to tariffs, it is difficult to envision a scenario where the RBNZ adopts a less dovish tone than it did previously. Market participants are nearly certain about a 25bps cut at this gathering, with the probability of a back-to-back quarter-point reduction in May standing at 75%.

Taking all this into account and considering the heightened risk that the trade war between the US and China could further escalate if China retaliates, the RBNZ may once again accompany its rate decision with a clear signal of its readiness to continue easing. This would likely encourage kiwi sellers to extend their positions.

China inflation and UK GDP also on the agenda

Speaking of China, during the Asian morning on Thursday, the world’s second-largest economy will release its CPI and PPI numbers for March and traders may be eagerly waiting to see the impact of the tariffs announced back on March 4 on consumer prices.

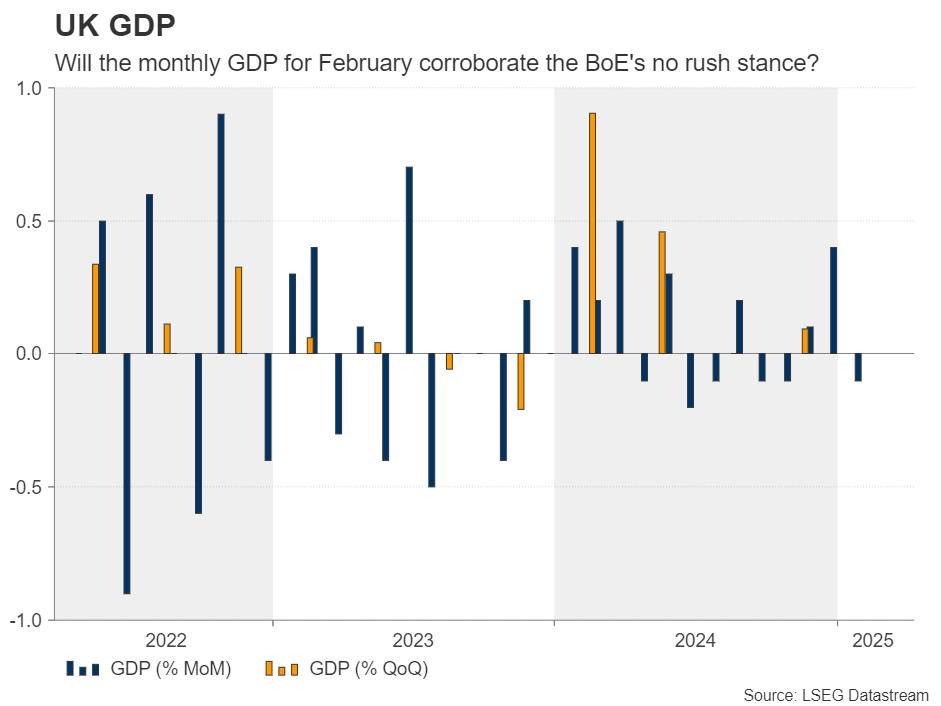

From the UK, the monthly GDP for February is due to be released on Friday, alongside the industrial and manufacturing production figures for the same month. UK data has been coming in slightly better than expected, with GDP for Q4 revealing moderate expansion despite forecasts of contraction. However, the monthly reading for January showed negative growth. The composite PMI improved in March, and retail sales for February significantly exceeded expectations.

Combined with the fact that UK inflation remains elevated despite slowing somewhat in February, the overall economic outlook supports the Bank of England’s stance that there is no urgency to cut rates aggressively, especially after the UK was subject only to the US baseline 10% tariff. However, market participants are still assigning a high 85% probability to a 25bps reduction at the next decision on May 8. Therefore, a strong set of data may be required to reduce that probability and allow the pound to gain further ground.

Weekly Focus – Promising Macro Data Drowns in Trade War Chaos

Liberation Day was the dominant theme in markets and the key driver this week. The escalation of the trade war turned out to be more extensive than what was expected by most analysts and priced in by investors. As a result, global equities nosedived with the US deepest in red, yields declined and oil prices took a big hit, not just from the perspectives of a demand shock but also more supply as OPEC+ announced an output hike in May.

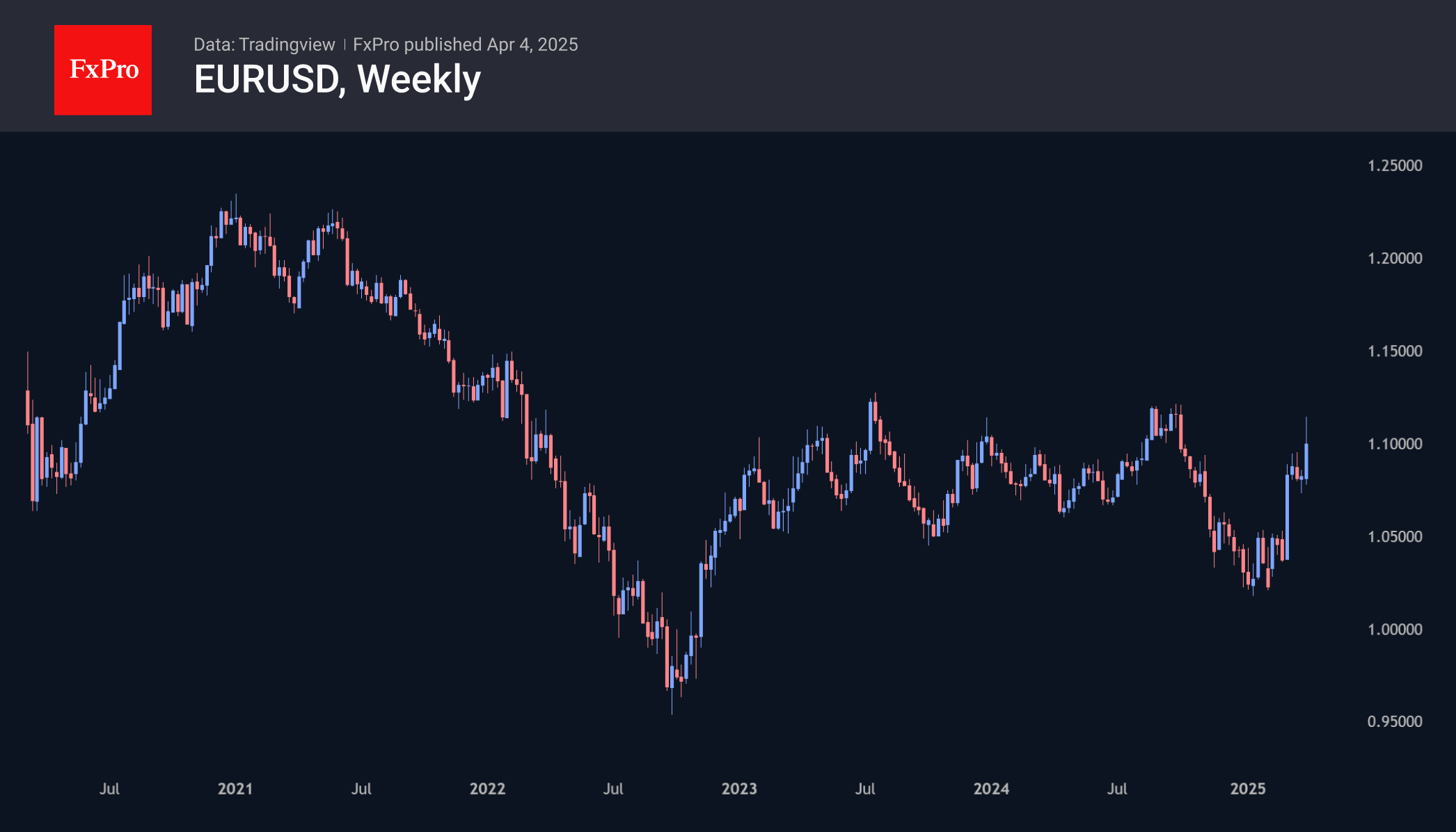

Betting markets now price above 50% probability of a US recession in 2025. This is also reflected in the FX market where the fear of recession overshadows the technical USD strengthening from increased tariffs. As a result, EUR/USD traded back above 1.10 for the first time since early October. JPY and CHF were the two natural outperformers.

The reciprocal tariff on EU goods will be 20%. Using estimates from the ECB-GLOBAL 2.0 model we estimate that the increase in tariffs will shave off 0.2-0.4 percentage points of euro area GDP in the coming year assuming that recent tariffs are unchanged in the entire period on all countries and there is retaliation. Retaliatory tariffs will of course be inflationary in Europe, but we expect the negative shock to the global economy will offset this, leading to lower prices, if anything. March HICP inflation declined to 2.2% as the underlying price pressure remains largely in line with the inflation target. The labour market still shows no signs of cracking as unemployment hit a new record low of 6.1% despite obvious German weakness. Even if ECB hawks did push back on ECB pricing, we still think conditions are in place for another rate cut in April. No scheduled data has the potential to move that picture much.

US tariffs on China are set to move to 65-70% on average according to our calculations, which will deal a serious hit to Chinese growth. This comes as both official and private PMIs indicate that stimulus is starting to kick in with manufacturing activity picking up in March.

Elsewhere in Asia, sthe Japanese Tankan business survey aimed nicely with Bank of Japan's cautious hiking cycle as non-manufacturing business conditions hit its highest since 1991. Inflation expectations edged higher on all horizons as the outlook for wage growth this year continues to look strong. A next hike already by the end of the month should be off the table for now, though, with the new tariffs, which will be particularly tough on Japanese car manufacturers.

Next week, we will continue to keep a close eye on the trade war, including potential deals or retaliation plans. The trade war escalation will to some extent be reflected in Euro Sentix, released on Monday and to a larger extent in US consumer sentiment released on Friday, where inflation expectations, which are already sky-high, will take key focus. We also get actual March US inflation data, which follows the comforting February release after a January price spike. Of course, US inflation will attract much attention going forward.

Sunset Market Commentary

Markets

Day two of the ‘US liberation era‘ was much like day one. The global risk-off continued unabatedly as investors try to the make-up their mind on the multiple consequences/further fall-out from the US profoundly recalibrating the global framework on free trade by announcing reciprocal tariffs. Almost zero visibility on how this process will continue keeps investors looking for shelter. European equities extended losses and investors assumed that mounting recession risks will force central banks to again come to the rescue, with core yields on a firm downtrend. At the least the assumption that further negative dominoes were likely to fall, was confirmed almost immediately. Around noon CET, China announced retaliation for the 34% US ‘base-line’ tariff on Chinese imports, matching it with a similar levy on US imports. In addition, the country announced export restrictions on rare earths and launched an anti-dumping probe, amongst other measures. The risk sell-off accelerated. Usually, on the first Friday of a new month, the US payrolls reports takes center stage. Today, it was no more than a footnote for trading. The US economy in March added a solid 228k jobs, admittedly with a 48k downward revision for the previous to months. The unemployment rate rose from 4.1% to 4.2%, but this was due to a higher participation rate. Average hourly earnings was close to expectations (0.3% M/M, 3.8% Y/Y). More than analyzing the payrolls, the market focus was on the cash open of US equity markets and on a first US reaction to the China retaliation. The market photo just after the open op US equity markets reads: US equities decline about 3.0 % for the major indices. The Eurostoxx 50 is also ceding about 4.0%. Treasuries and Bunds continue their assent, betting of CB help. US yield decline 9-10 bps across the curve. US money markets are discounting (more than) a full 25 bps Fed rate cut in June and a cumulative 100 bps EOY 2025. Bunds even outperform Treasuries with German yields declining from 15 bps (2-y) to 10 bps (30-y). Something to keep an eye on: After a period of extreme calm on intra-EMU government bond markets, 10-y spreads vs Bunds for the likes of Italy and Greece are widening about 6 bps. The USD sell-off is talking a breather. DXY (re)gains marginal ground (102.25). The EUR/USD rally also takes a pauze (1.103). The retaliation of China against the US also has further negative fall-out on the likes of the Aussie (AUD/USD 0.6125 from 0.6325) and kiwi dollar (NZD/USD 0.565 from 0.5795). To close this hectic week, markets still have at least one wildcard to look out for. Fed Chair Powell is scheduled to speaks on the economy around the close of European markets. Will he already give any hints on how the Fed assesses evolving risks between growth and inflation?

News & Views

The FAO Food Price Index was nearly unchanged in March, averaging at a 127.1 points, to be 6.9% lower y/y and down 20.7% from the peak exactly three years ago. On a headline basis, declines in cereals and sugar price offset increases of meat and vegetable oils. The dairy price index remained stable. Going more into detail, dropping wheat and maize prices amid improving crop conditions pushed down the cereals price index. Rice prices fell too on weak import demand and ample exportable supplies. Sugar prices generally fell on signs of weaker global demand and easing concerns over tight supplies. Meat prices increased primarily thanks to pig meat on rising demand. Ovine meat prices also increased, supported by strong global demand ahead of the Easter holidays. Meanwhile, poultry meat prices remained largely stable. The continued increase in the oil price index was driven by higher prices of palm (supply driven), soy (international demand driven), rapeseed and sunflower (both demand and supply) oils.

Canadian employment fell by 32.6k in March, driven exclusively by full time jobs (-62k). Part time employment still added 29.5k jobs. The decline in March followed little change in February and three consecutive months of growth in November, December and January totaling 211k. Employment declined in wholesale and retail trade (-29k), as well as information, culture and recreation (-20k). There were increases in the 'other services', such as personal and repair services (+12k) and utilities (+4.2k). The employment rate declined to 60.9% while the unemployment rate rose to 6.7%. The latter has now been above the pre-Covid average of 6% for exactly a year. Hourly wages grew by 3.5% y/y, easing from 4% in February. Overall, Canadian payrolls were sub-par and adds to the existing downward CAD pressure today. USD/CAD reverses much of yesterday’s steep decline to return north of 1.42. Money markets expect the Bank of Canada to continue cutting rates from the current 2.75% to around 2% by end this year.

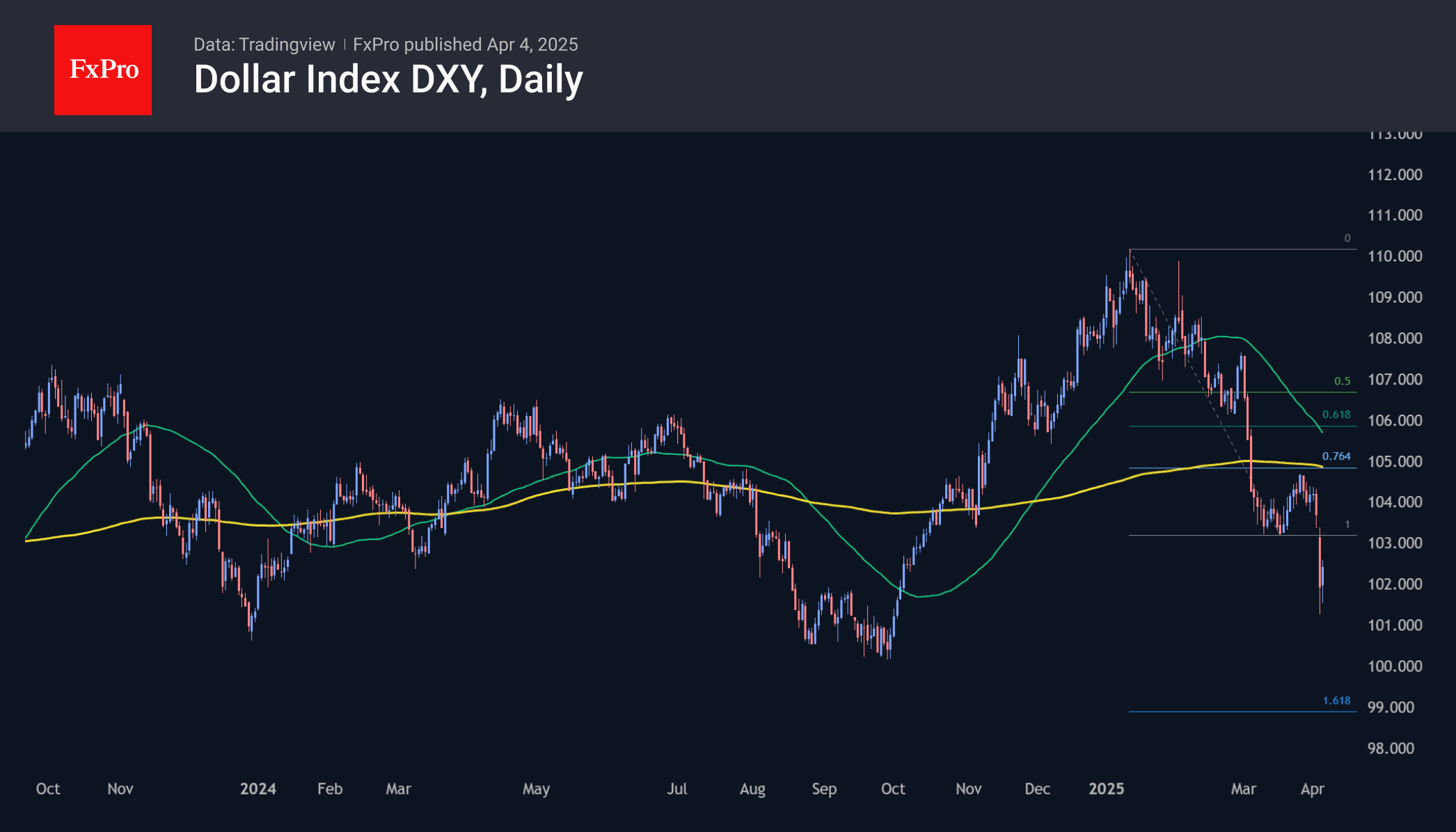

Tariff Wars Made Dollar a Risky Asset

The fall in the U.S. dollar accelerated at the start of April as the shock of trade tariffs caused capital flight from U.S. assets. We don’t know yet how long this trend will be. In finance, it is often said, “America sneezes, and the world gets a fever.” Even if the problems originated in the US, the impact on the markets of other countries will be more substantial.

Dollar Index confirmed the prevailing downtrend.

The dollar index moved sharply below its previous support, confirming the prevailing downtrend. The technical target of the current drop now looks like the area from 99 to 100. The lower boundary represents the Fibonacci extension of the first impulse. The upper boundary passes through the psychologically significant round level, which stopped the dollar’s decline in September-October last year.

Among the dollar’s competitors, the euro and the yen are the biggest gainers so far. These are the next two largest capital markets after the dollar, where investors are hoping to weather the storm. The euro returned to local highs against the dollar and the pound. EURUSD has also been near the upper boundary of the trading range for the last three years, and it is ready to break it and move further up.

Canada Sheds Jobs in March as Tariffs Issue Their First Blow

The Canadian labour market shed 32.6k positions in March, driven by a decline full-time positions (-62k).

Job losses pushed the unemployment rate up 0.1 percentage point (ppt) to 6.7%. The labour force participation rate decreased by 0.1 ppt to 65.2%.

Employment by sector showed declines in trade exposed wholesale and retail trade sector (-29k), as well as culture and recreation (-20k). Personal and repair services saw a decent job gain of +12k.

Lastly, total hours worked recovered from a bad weather-induced fall in February (+0.4% on the month, from -1.3%). Meanwhile wages were up a stable 3.6% year-on-year (from 3.8% in February).

Key Implications

Has it begun? The impact of trade tariffs appears to be working its way through the economy. Businesses and consumers are naturally hesitant in the face of heightened political uncertainty. Today's report reflects this, with full-time jobs in the cyclically sensitive private sector driving the losses. Those that lose their jobs are also taking longer to find work, a sign that the Canadian labour market is starting to loosen in response to the imposition of tariffs.

The Bank of Canada is increasingly likely to cut its policy rate further. While pricing for April is still undecided, we think the bank should keep cutting by at least another 50 bps (cumulative) over the coming months in order to cushion the blow from tariffs. Today's discouraging jobs report showcases the downside risks to the economy, which warrants further action from the BoC.