Sample Category Title

Nikkei (NKD) Appears Poised to Continue Broader Corrective Trend

The Nikkei (NKD) has been trending lower since its peak on July 8, 2024. We indicate this decline follows a “double three” Elliott Wave pattern, characterized by a series of distinct movements. After reaching that high, the index fell to 30,720, rebounded to 40,675, and is now progressing downward in a zigzag formation as the internal within “wave y.” The index dropped to 36,275, rose to 38,029 with intermediate fluctuations, and has since resumed its downward trajectory.

This ongoing move lower has already reached 33,525, followed by a recovery to 34,975. We anticipate the index will extend further downward to complete this phase. Afterwards, a temporary rally is expected to provide a correction before the next decline resumes. We anticipate the index will extend further downward to complete this phase. Afterwards, a temporary rally is expected to provide a correction before the next decline resumes.

In the near term, as long as the high of 38,029 remains intact, any upward movements are likely to be limited, setting the stage for additional downside. Investors should monitor these developments closely as the Nikkei continues to navigate this pattern

Nikkei 60 Minute Elliott Wave Chart

NKD Video

https://www.youtube.com/watch?v=eCWtSXB_IeA

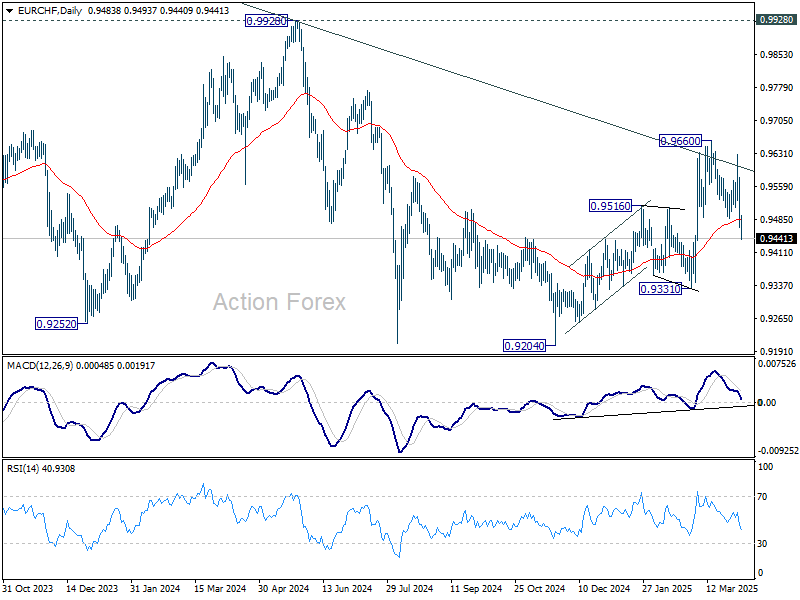

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9445; (P) 0.9517; (R1) 0.9567; More....

EUR/CHF's fall from 0.9660 resumed with downside acceleration. Current development suggests that rise from 0.9204 has completed as a three-wave correction, after rejection by long-term falling channel resistance. Intraday bias is back on the downside for 0.9331 support first. On the upside, above 0.9486 support turned resistance will turn intraday bias neutral again first.

In the bigger picture, rejection by long-term falling channel resistance (now at 0.9600) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Downside breakout through 0.9204 low is in favor at a later stage.

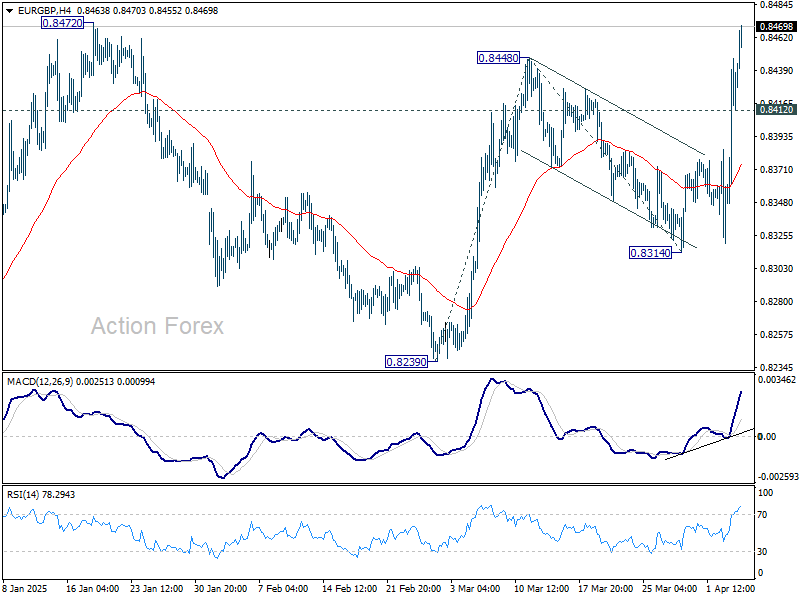

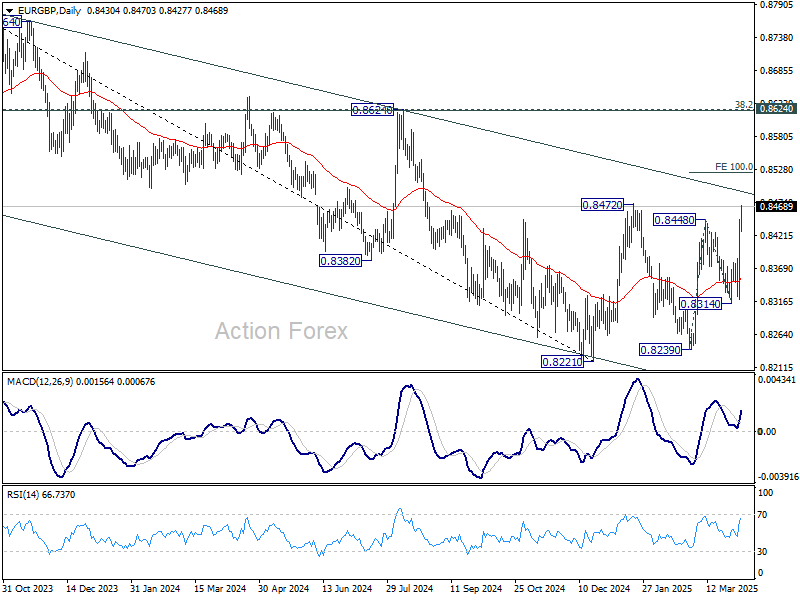

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8352; (P) 0.8401; (R1) 0.8483; More...

Intraday bias in EUR/GBP stays on the upside for medium term channel resistance (now at 0.8490). Firm break there will target 100% projection of 0.8239 to 0.8448 from 0.8314 at 0.8523. On the downside, below 0.8412 minor support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, EUR/GBP is still bounded inside medium term falling channel. While rebound from 0.8221 might extend higher, it could still develop into a corrective pattern. Overall outlook will be neutral at best and down trend from 0.9267 (2022 high) could extend, at least until decisive break of channel resistance (now at 0.8490).

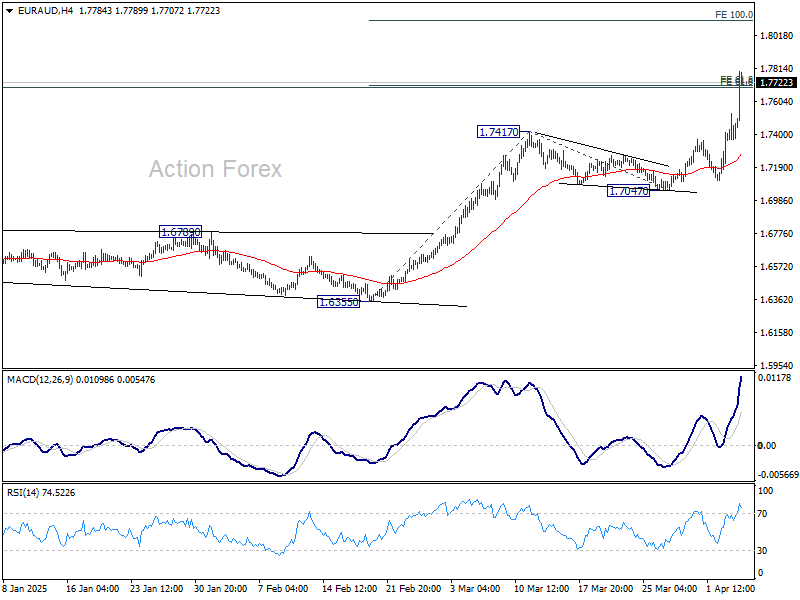

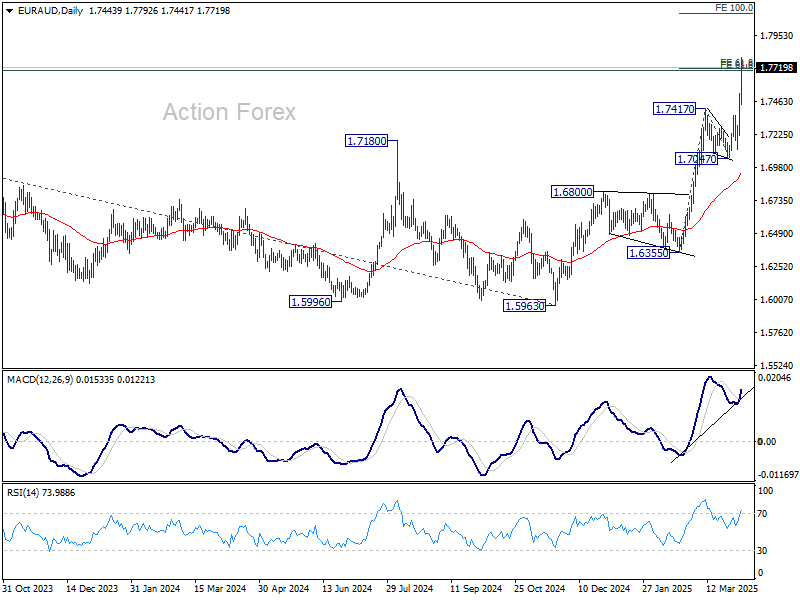

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7279; (P) 1.7405; (R1) 1.7587; More...

EUR/AUD's up trend resumed through 1.7417 and met 61.8% projection of 1.6355 to 1.7417 from 1.7047 at 1.7703 already. There is no sign of topping yet. Intraday bias stays on the upside. Sustained trading above 1.7703 will target 100% projection at 1.8109. For now, outlook will stay bullish as long as 1.7047 support holds, in case of retreat.

In the bigger picture, up trend from 1.4281 (2022 low) is in progress and has met 61.8% projection of 1.4281 to 1.7062 from 1.5963 at 1.7682 already. Sustained trading above 1.7682 will pave the way to 100% projection at 1.8744. Outlook will remain bullish as long as 1.7062 resistance turned support holds (2023 high) even in case of deep pullback.

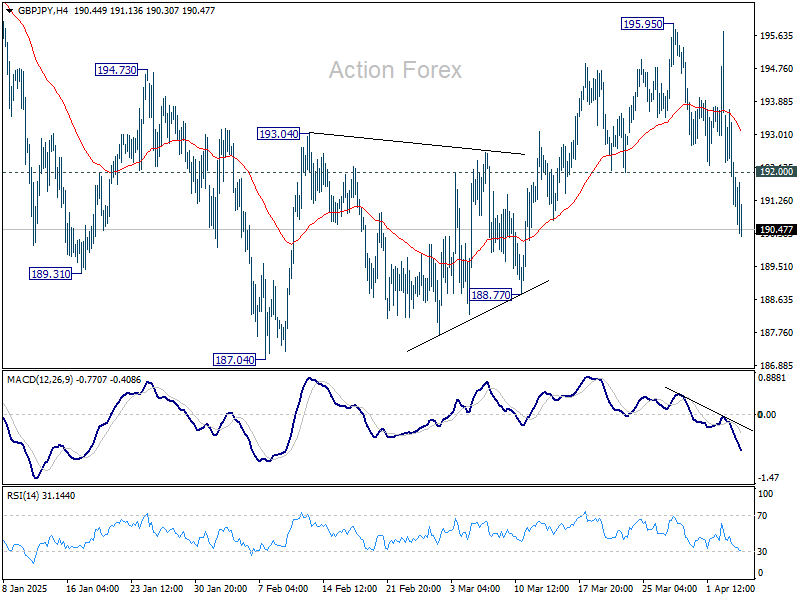

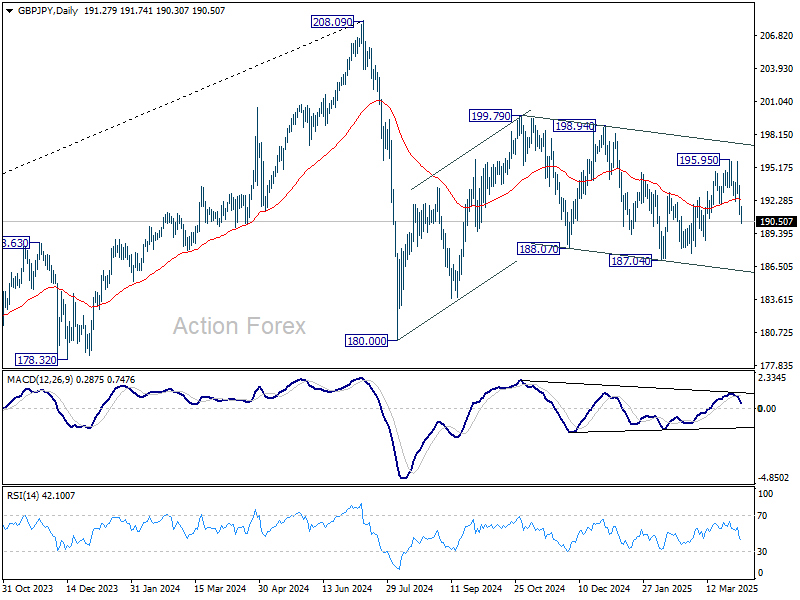

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.32; (P) 192.20; (R1) 193.26; More...

Break of 192.00 support suggests that GBP/JPY rebound from 107.04 has completed at 195.95. Intraday bias is back on the downside for 188.77 support first. Break there target 187.04. Overall, corrective pattern from 180.00 is still extending. Another rise might still be seen as long as 187.04 support holds.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

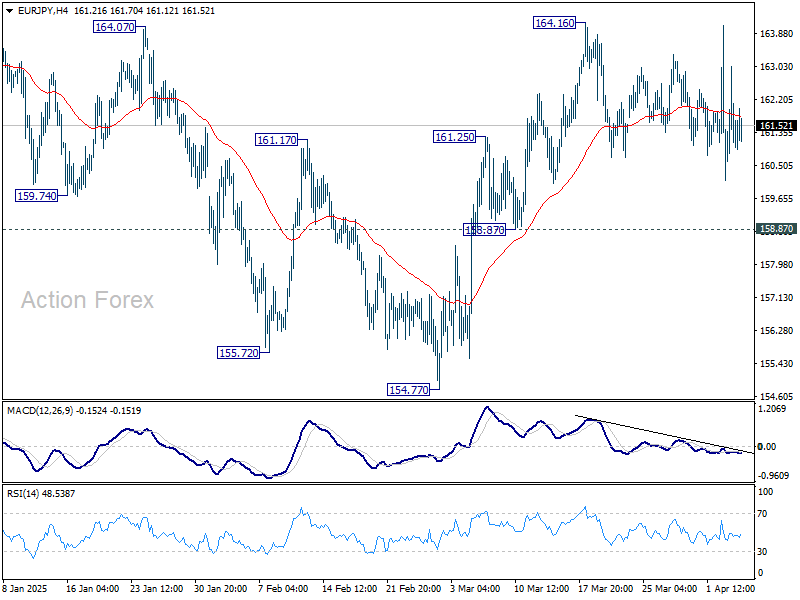

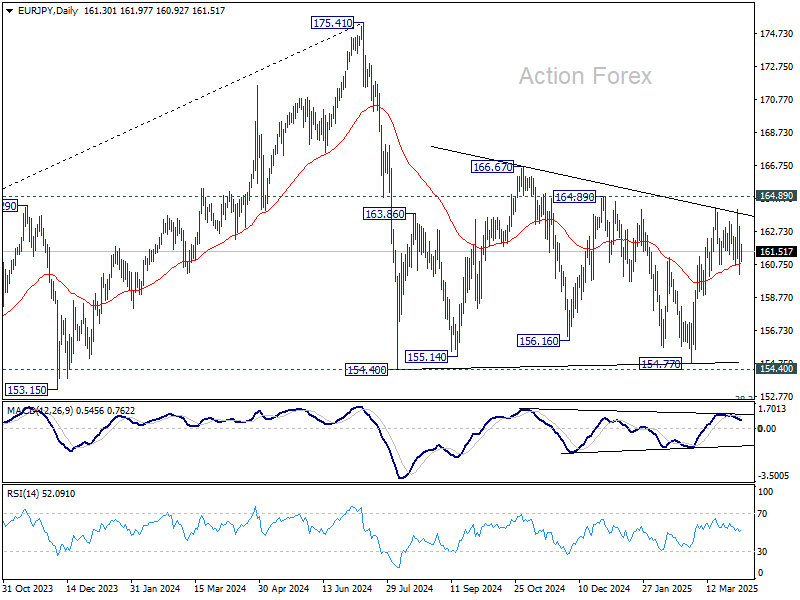

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.01; (P) 161.53; (R1) 162.96; More...

Range trading continues in EUR/JPY and intraday bias remains neutral. On the upside, above 164.16 will resume the rally from 154.77 to 164.89 resistance, and then 166.67. However, break of 158.87 support will bring deeper decline back to 154.77 support. Overall, sideway consolidation pattern from 154.40 is still extending.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

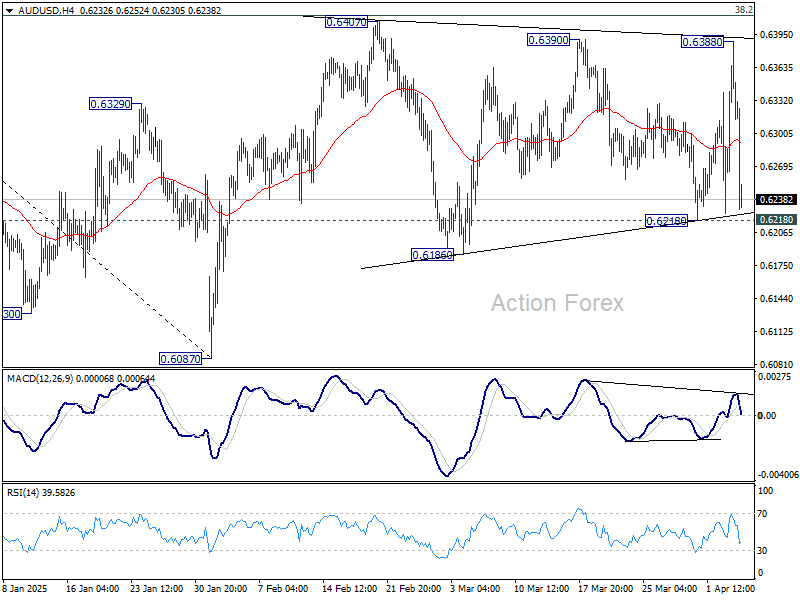

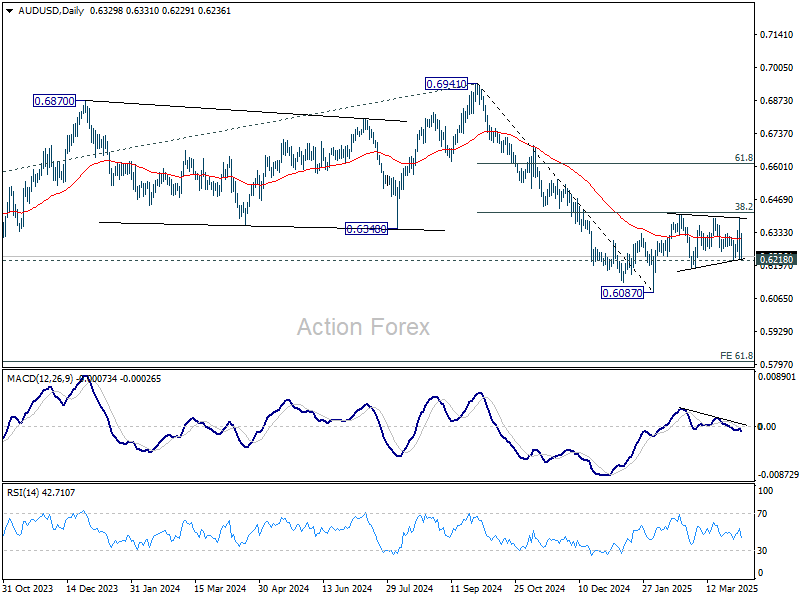

AUD/USD Daily Report

Daily Pivots: (S1) 0.6240; (P) 0.6315; (R1) 0.6403; More...

AUD/USD jumped to 0.6388 but reversed again. Intraday bias remains neutral for the moment. Overall, outlook will stay bearish as long as 38.2% retracement of 0.6941 to 0.6087 at 0.6413 holds. Firm of 0.6128 support will argue that corrective pattern from 0.6087 has completed and bring retest of this low.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6461) holds.

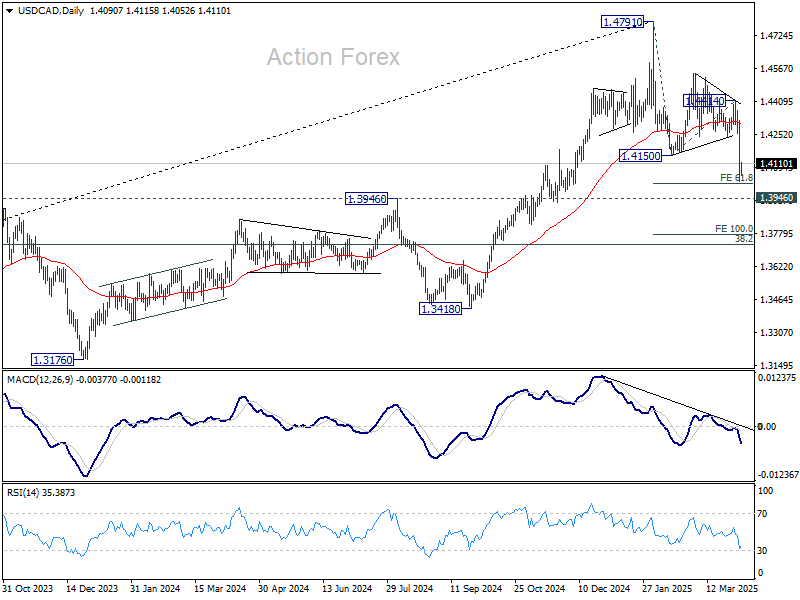

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3978; (P) 1.4148; (R1) 1.4269; More...

Intraday bias in USD/CAD remains on the downside for 61.8% projection of 1.4791 to 1.4150 from 1.4414 at 1.4018. Decisive break there would extend the fall from 1.4791 to 100% projection at 1.3773 next. On the upside, above 1.4158 minor resistance will turn intraday bias neutral and bring consolidations first.

In the bigger picture, focus is now on 1.3976 resistance turned support (2022 high), which is close to 55 W EMA (now at 1.3986). Sustained break there should confirm medium term topping at 1.4791. Deeper correction would be seen to 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727.

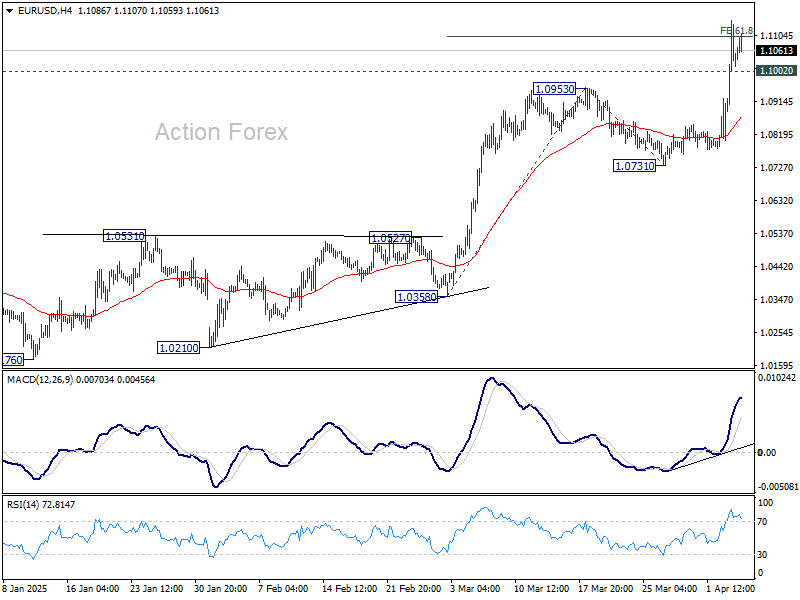

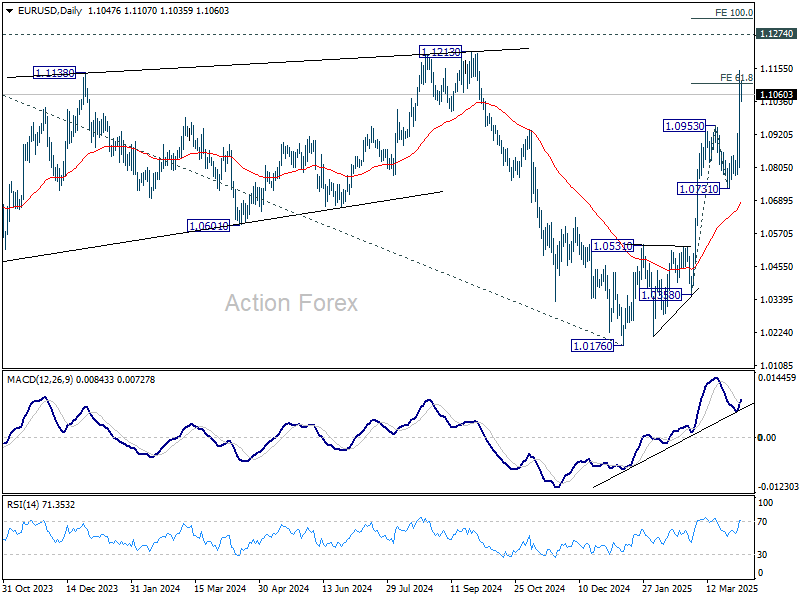

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0855; (P) 1.1001; (R1) 1.1196; More...

Intraday bias in EUR/USD remains on the upside at this point. Sustained trading above 61.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1099 will pave the way to 1.1274 key resistance, and probably further to o 100% projection at 1.1326. On the downside, below 1.1002 minor support will turn intraday bias neutral and bring consolidations, before staging another rise.

In the bigger picture, prior strong break of 55 W EMA (now at 1.0692) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0731 support holds.

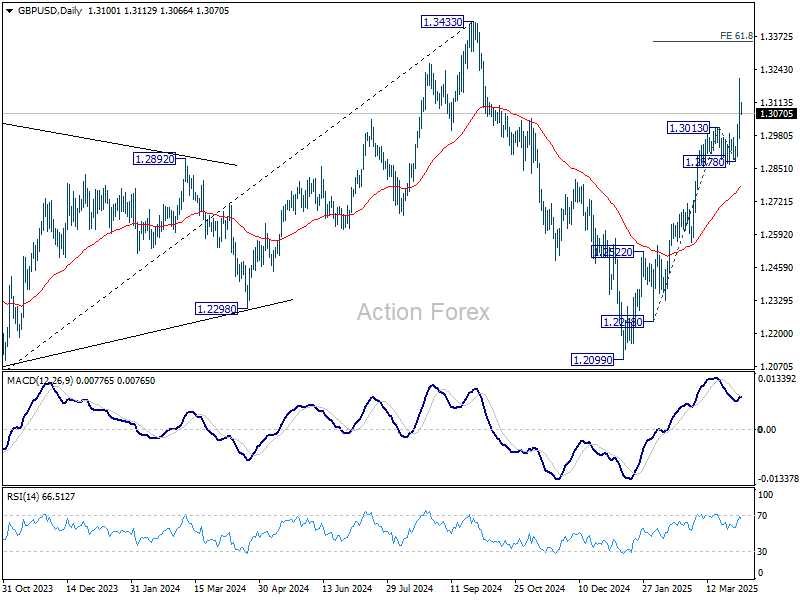

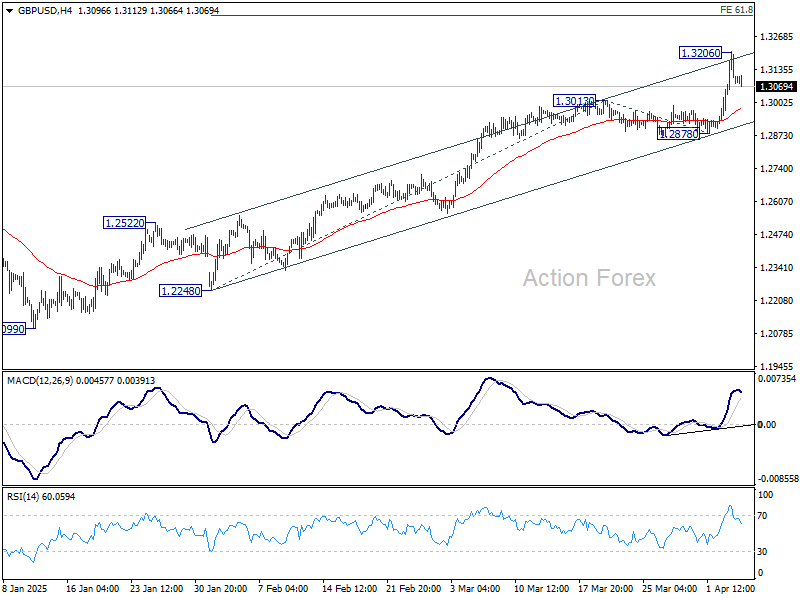

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2980; (P) 1.3094; (R1) 1.3215; More...

A temporary top is formed at 1.3206 with current retreat and intraday bias is turned neutral first. Downside of retreat should be contained above 1.2878 support to bring another rally. Break of 1.3206 will resume the rise from 1.2099 to 61.8% projection of 1.2248 to 1.3013 from 1.2878 at 1.3351.another rally.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance (2021 high). This will now remain the favored case as long as 1.2099 support holds.